SafetyinNumbers

-

Posts

2,816 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

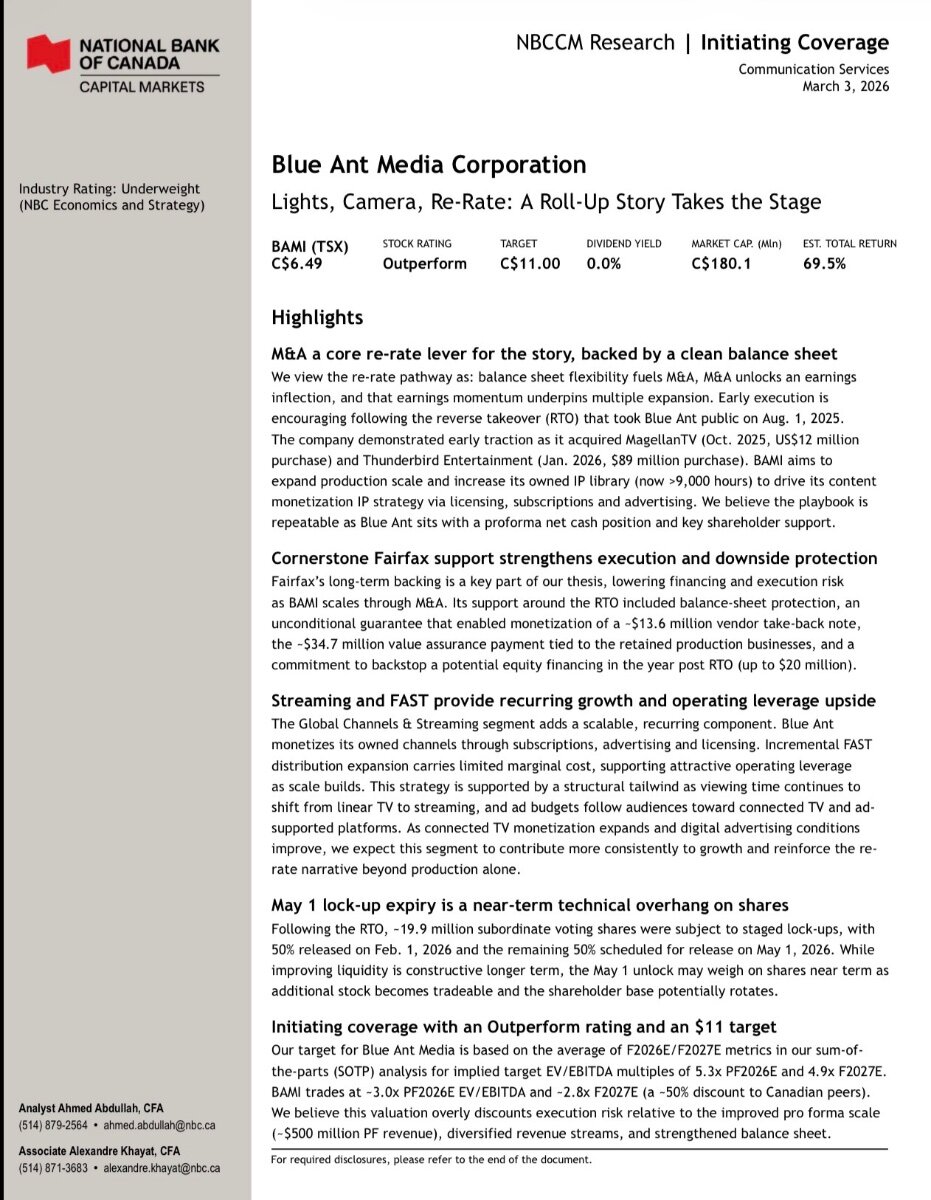

BAMI initiation at NBF last week

-

IDBI might dwarf everything in terms of related fees but not sure about in size. We likely contribute our CSB stake but not necessarily a ton of cash.

-

I agree it should be addressed but once again FIH has positions where they have significant influence and Marval owns small positions in bigger companies.

-

FIH is trying to achieve absolute returns. If successful, they will beat the market over the long term. This is another situation where investors think the market is efficient when it’s clearly not.

-

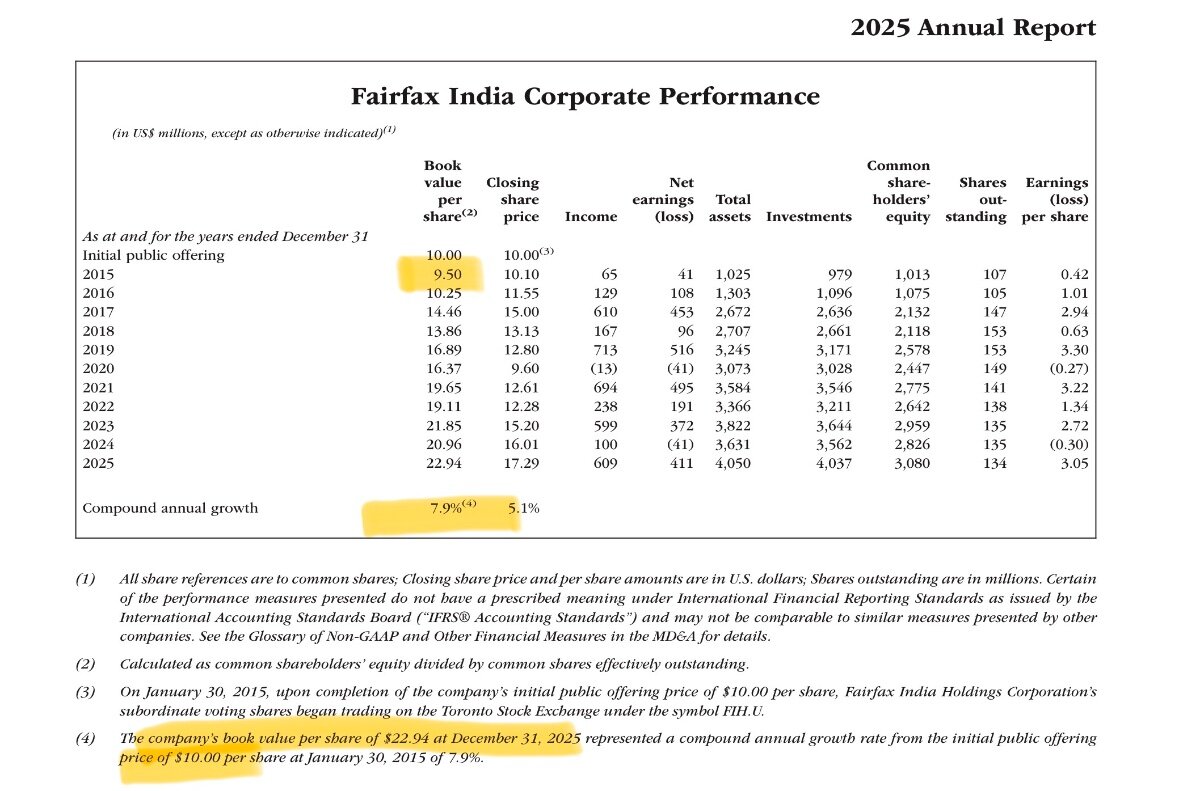

FIH has a different strategy than Marval but has had strong returns in public investments and in private/public monetized investments. I think the Track Record suggests that its private investments are either not performing well or are conservatively marked. Based on what we know about Fairfax’s culture the latter makes more sense. We also have other confirmation given we know BIAL might be marked at less than half its fair value. We can also see the discount rates and other assumptions in their DCFs to value the other investments. They are conservative by most standards. This suggests the whole private book might be undervalued. That’s the bet in a nutshell on FIH. If BVPS was $40/sh which is where liquidation value might be, it would be closer to a 14% CAGR from $9.50 instead of 7.9% to $22.94. A big change recently that will help BVPS momentum is the BIAL model price is now above the price paid to Siemens and has been for the past two quarters. We should continue to see that accrete which should help the stock perform and make it easier to own waiting for other catalysts like the BIAL IPO and IDBI.

-

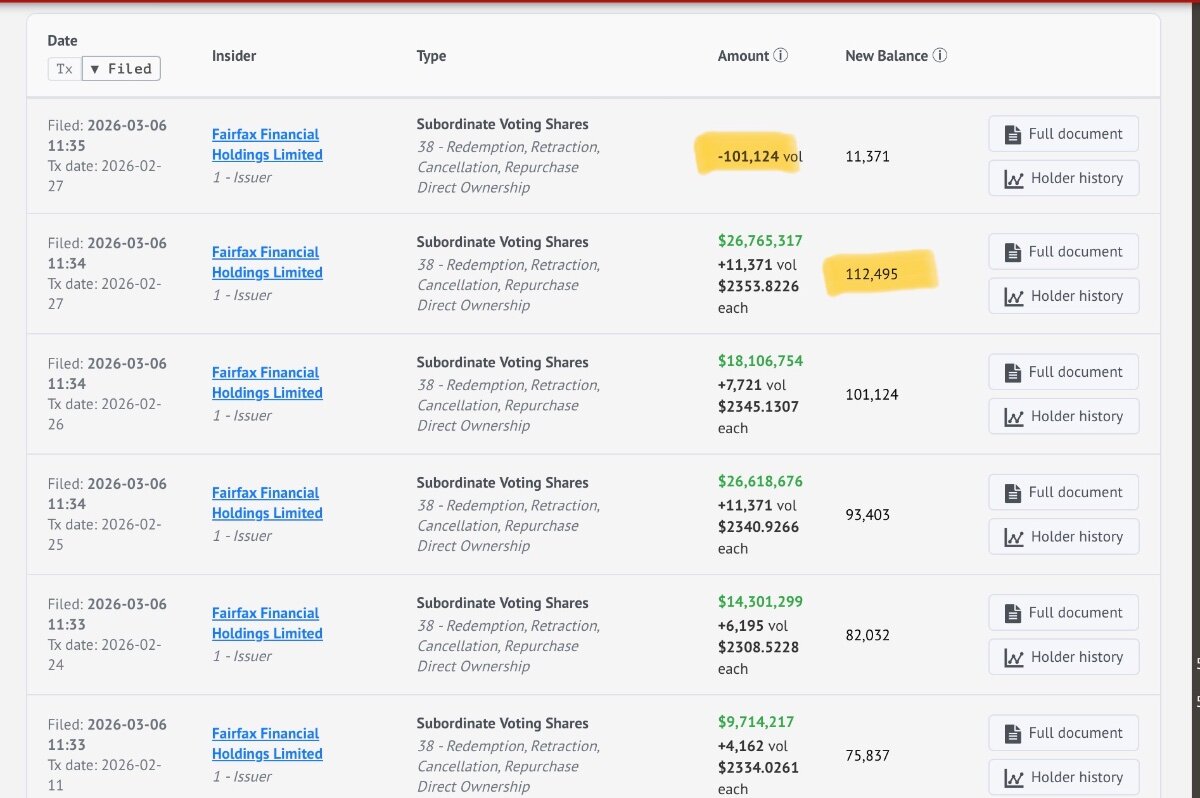

Fairfax bought back ~107k shares and cancelled ~101k shares in February. Presumably the buying continues this month at these bargain prices. The most they have paid is C$2475 back in December.

-

I think an under appreciated reason for the underperformance during this period was because they starter doing significant influence and control positions in the insurance subsidiary portfolio which by the nature of the accounting recognizes losses immediately and defers gains. This makes the equity returns look worse than they are. Much like FIH, now that these investments have had more time to season, the gains are being recognized as assets are monetized.

-

Would AI be useful in analyzing this file vs the last one to tell us what changed?

-

Interest rates do matter. At Fairfax, we get approximately the return on the equity portfolio (about the same size shareholder’s equity) + 2x current yield on the fixed income portfolio (2x shareholder’s equity) plus underwriting less holding company expenses including cost of holding company leverage.

-

This is by design as Fairfax tries to maintain the 3:1 investments:equity leverage. Even the approach to financial leverage for controlled businesses shows a the difference in how each “sweats” the assets. Fairfax puts on leverage while Markel doesn’t or is less aggressive. The risk is not that high as more capital can always be injected if needed. It’s not like a non control position where the decisions on capital allocation are being made by others that may have differing incentives.

-

I thought Markel’s 10% hurdle rate was interesting in contrast with Fairfax’s 15%. The podcast also made me think that Prem might have inspired Steve Markel to follow the Berkshire model as well given the timeline. They partnered on Fairfax first.

-

$3.5b of this is mark to market. How big is that bucket for the whole portfolio?

-

I think it happens during the next hard market. It could take years. Meanwhile we’ll have to get by with 15-25% returns more in line w/BVPS growth plus potential multiple expansion to the most Fairfax will pay for stock. So far that’s about 1.5x BV. That number should inch up over time as forward ROE goes up the more we buy back.

-

Exco is pretty gassy and I assume they like the exposure. Not sure why they would sell it. Same goes for SCR and GFR which are oily. OXY seems like the most likely candidate to sell. I continue to think there is plenty of excess cash at the insurance subsidiaries to do IDBI and not have to sell anything.

-

I’m not sure about the regulatory ramifications but from an accounting perspective, ROE is higher because Fairfax has a ~20% return on carrying value. If it was marked up we would get a one time benefit in ROE but post that ROE would then be lower all else being equal.

-

We aren’t going to wake up at 3x so I assume once it starts trading above 2x, you start selling, out by 3x? My plan was to base my sell decision when forward ROE can be forecast below 10% because I didn’t want to cut off the potential multiple expansion. The recent selling pressure associated with slowing revenue momentum makes me think that the next hard market we’ll see big multiple expansion. The longer it takes to get to the next hard market, the more shares we’ll be able buy back in the interim. The more shares we buy back, the bigger the multiple expansion.

-

At what multiple do you start selling?

-

The IPO definitely did not go well but my guess is at $23, the dividend yield might be in line with the cost of debt after taxes. I assume the investment will be made in the insurance subsidiaries though. Still a nice switch from cash on an after tax cash flow basis, is my guess.

-

I asked the question at the 2024 AGM (although they butchered my name in the transcript ). Prem seemed to tell us exactly what is going to happen but it remains to be confirmed. Only 5% of the IDBI float is listed so it’s impossible to get a size position. I think the deal will be done at a discount because the minority will be offered the same deal and the price has to be low enough that they don’t tender. I’m not sure if it’s possible but if was them I would simultaneously have IDBI offer to buy CSB for stock. That immediately increases IDBI float. The deal would have to be done at a premium to convince the CSB minority to sell. My guess is it won’t be hard sell given CSB management likely has a plan to increase IDBI ROE that is been refining for the past 3 years and it won’t be hard to find investors that can see the upside. If this comes to fruition, the benefits to FIH book and intrinsic value could be dramatic if we consider the premium on CSB and the NPV of the fee stream for the GP. It also flips a key narrative for not owning FIH, the fee structure.

-

I assume the AMC on 6th given its the date of record for the AGM.

-

I think IDBI co-investment will happen at the insurance subsidiary level not at the holdco which is where the Eurolife proceeds show up. Maybe they use that for Allied World since that’s also a holdco investment. I don’t know if they need to sell anything in the equity book to do this deal. They have a lot of extra cash/fixed income they could use to do the deal. They have communicated previously that the biggest new equity position they will take is 10% of shareholders equity so they will definitely need partners. This might include what they own through Fairfax India but it remains to be seen.

-

Fairfax is selling about ~130-140k shares a day at these prices as they participate in their share of the buyback. Doesn’t really move the needle on the position size but it’s another source of gains that analysts are ignoring while earnings power is increasing.

-

I think characterizing these gains as “rabbits out of a hat” doesn’t give enough credit to funnel they have developed over the years. They have moved most of the portfolio over to significant influence and control positions since 2012. The accounting by its nature defers any gains so FFH only gets credit for its share of earnings until they sell. That means these gains are compounding over time. Any mistakes get written off immediately even if they ultimately recover which increases the accounting ROE on holdings and makes the potential gains even bigger. The size of deals has also been going up with the float, so the ultimate gains should grow assuming execution. The annual report is super helpful in figuring out what fair value over carrying value might be for the private investments. Looking forward to reading it next week.

-

Anything interesting highlights from the text? Price, structure etc?

-

What are the chances you would still own any at 3x book?