SafetyinNumbers

-

Posts

2,810 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Why Q1?

-

I don’t think Day 1 matters as much as what they end up with. I’m not saying FIH as GP has been finalized but whatever the structure is must be acceptable otherwise they wouldn’t be able to bid.

-

Would they recognize a gain on a consolidated position if they aren’t selling any shares?

-

We should get the Eurolife gain in Q1 as well. Still a long way to go until March 31 but already bodes well for Q1 earnings over $50/sh.

-

That’s all been decided otherwise they wouldn’t get a chance to bid. The last three years was working out of these details. The final step is the price.

-

If they aren’t buying back stock then it’s safe to assume anything else they are doing at the holdco has a higher return.

-

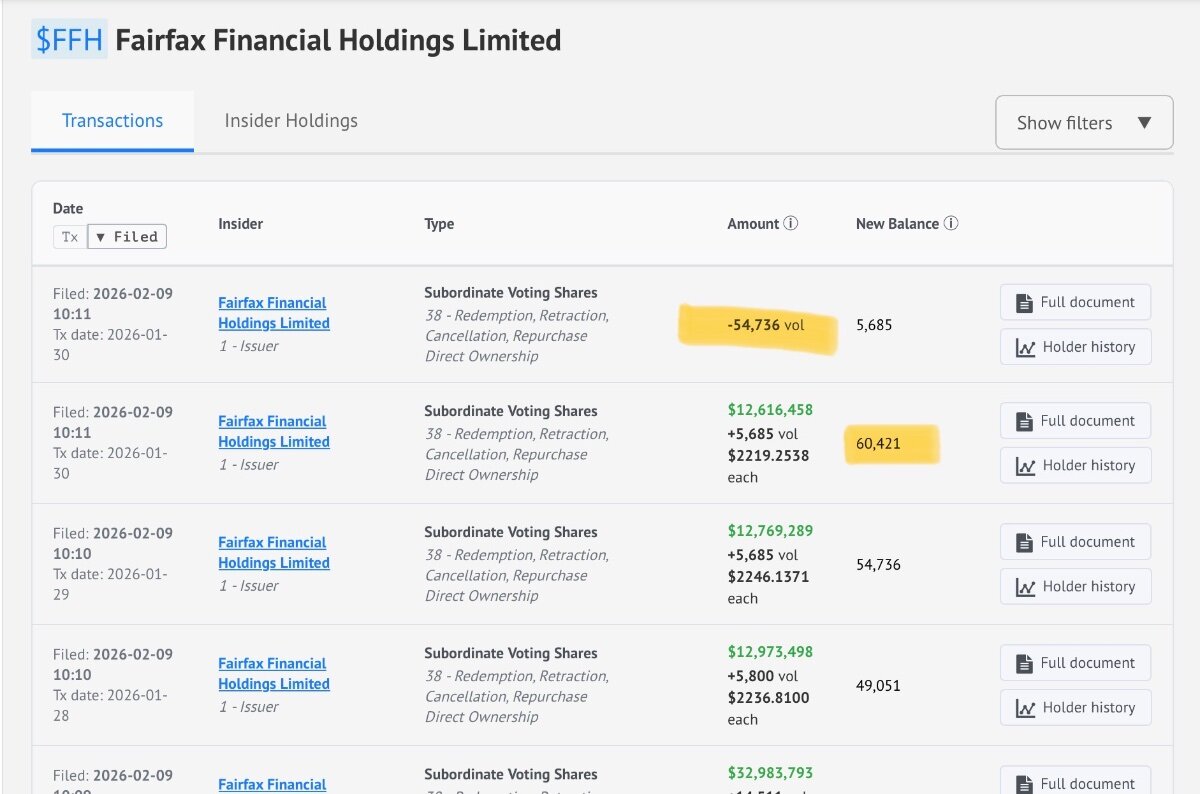

Buybacks continue albeit at a slower pace.

-

The other bidder does own another bank. So same hurdles I guess. FIH has the right to all non insurance acquisitions for Fairfax in India. They have the network and have been working on this deal for over 3 years. They bring CSB and the CSB management team who are used to managing much larger institutions. The stake will be material to FIH. That’s what they bring to the table.

-

I assume it will be part of the plan. The additional approval will be the minority at CSB and probably at IDBI too. I’m not sure why it worsens Fairfax’s offer. Why do you think so? I’m not sure what you are asking.

-

FIH has exclusivity on non insurance investments for FFH. They have to be part of the deal or presumably compensated if they are excluded. That’s why I think the GP/LP structure makes a lot of sense. They could put up some cash, use their line and then also contribute CSB to end up with an equity stake material to FIH as the GP.

-

If the remaining bids are cash, I expect them to pay less than the stock price. I think the offer has to be made to the minority too. KOTAK trades at a big premium to IDBI. If they were buying they would want the minority to also sell and could afford to pay a premium. I’m not sure about the Emirates but Fairfax probably wants to increase the float by having IDBI buy CSB for stock. They need a price where the minority doesn’t want to sell but Fairfax should be ok if they do. Like when a company does a rights issue and it’s backstopped by the biggest shareholder.

-

Emirates are back in the mix. https://www.cnbctv18.com/business/finance/fairfax-financial-and-emirates-nbd-submit-bids-for-idbi-bank-disinvestment-sources-ws-l-19844852.htm#

-

Big short interest and much tighter float might be helping.

-

I think after the FFH warrants are exercised there are 36.5m shares. At the mid point of the range, it adds about 15m shares to raise $425m. Is there something else I’m missing?

-

More colour on the AGTF IPO.

-

BAMI closed its deal to buy TBRD and is unsurprisingly seeing flowback from TBRD shareholders as most of the consideration was equity. I think Fairfax will drop under 20% post deal so will stop equity accounting for the position. It’s not material to FFH. The TBRD deal was struck 0.2165 shares of BAMI for all stock or a combination of cash and stock at $1.77 or $8.17 in BAMI terms. The current price of BAMI is $6.55. Cormark covers the stock and expects $1.40 in EPS for F’2027 which ends in August.

-

It’s just two thirds of those that vote. If FFH and CGF are in, it’s most likely a done deal. The risk might be on the ELD side as they are issuing cheap paper for more expensive paper.

-

He already has voting control. I’m not sure what the point is of taking it private but of course it could happen.

-

Could be they can’t agree on price with the selling shareholders so they are letting the market decide or they don’t want to own that much.

-

i guess they are issuing a bunch of primary shares as well to pay off the rest of the debt. I thought it was just secondary shares but that looks wrong.

-

I think they are getting good value in ELD shares and the premium will come from the rerate. Both the narrative and flows (index related) are supportive. Allows anyone who wants to defer the gains to do so and anyone who wants to take profits to have liquidity.

-

What do you think they have to pay?

-

Point North Capital is OMERS. They appear to be sellers only if the offering goes into the shoe. I don’t think that’s right. Fairfax is exercising 15m warrants at C$22.50 and that cash is being used to repay the Sponsor Notes. The shares being offered are from the co-founder and other specified employees.

-

Liquidity probably more important than anything else.

-

Also partly why returns on the equity portfolio likely have a higher floor than investors appreciate. The accounting of businesses where Fairfax has significant influence or control has the effect of writing down businesses more aggressively than writing them up. The effect of that is higher return on equity. Eurobank is a good example. We carry it at $2.7b but it contributes about $540m to earnings. That’s a 20% ROI which with 3:1 leverage contributes to FFH’s ROE at 60%. Our carrying value next year in theory should jump to $3.2b but EUROB pays dividends and buys back stock from us every day. Both reduce carrying value most of the way back to $2.7b. But earnings power at EUROB is unlikely to change so forward ROI should be going higher which bolsters Fairfax’s return on the equity portfolio that much more.