SafetyinNumbers

-

Posts

2,824 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

I think the average maturity was already 3 years or better. Duration is always shorter than average maturity because of coupons.

-

Fairfax has reduced its exposure to cats as a percentage of total premiums so it would take a particularly bad set of circumstances to cause the CR to go that high. Of course, it could happen. What happens afterwards would be more important as the market would harden up and they would be able to grow fast which I think will trigger momentum funds to jump back in.

-

I could see them buying more 2 years but given what they said at the meeting I don’t think they would have extended more.

-

It’s just Morningstar 2028 and beyond. They expect a big cat loss in the forecast period. Not sure if they model the same for all of the peers. Bret is the only analyst that has the same number for adjusted EPS and IFRS/GAAP EPS.

-

Does this mean the TRS income would be useful to offset head office and leverage costs at the holdco assuming there was no other income at the holdco?

-

Thanks I didn’t realize that. So they would get a refund at the holdco for the interest expense even if they didn’t have any taxable income in Canada?

-

I think the taxable income from the TRS is actually a feature because we need it to offset interest expense at the holdco. To me the TRS strategy is very well thought out and not appreciated enough.

-

I think that is what ultimately will happen but the multiple it’s transacted at really doesn’t matter as they locked in the price when the swaps were put on. To that end, it makes sense to buy in shares via NCIB first as long as valuation stays low. If the multiple goes up they can unwind TRS instead. The most important thing for me is that I know excess capital has a high return home and that the share count is ultimately heading a lot lower.

-

What makes a really good compounder is that they have high returns on excess capital. Fairfax has in order the ability to buy stock back in the open market, buy in minority interests and closing out the TRS. My assumption is they will buy in the open market below 1.5x BV and close out TRS above that. The beauty is that it’s 3+ years of free cash flow where we know the returns on excess capital are high and help maintain the investment to equity leverage.

-

They can unwind the TRS i.e. exit the swap at various points when they come up for renewal. Whatever gains or losses are marked to market every quarter so that shouldn’t impact timing. When they exit, the counterparty is likely long FFH so the most efficient thing to do is for FFH to buy back the stock. I think they plan to retire all of the TRS via buybacks although I’m not surprised they don’t guide to that as it’s nice to keep flexibility. I think the timing is tied to valuation. Under 1.5x BV my guess is they will buyback stock in the open market and over 1.5x BV they can retire the TRS as the price paid on the TRS doesn’t really matter as they locked it in when they entered into the swap. For shareholders, the key is maintaining the investment to shareholder equity leverage. Ironically, the higher price / book on buybacks, the easier it is to maintain the ratio close to 3:1.

-

I think it’s interesting to look at the 25-35 yr trailing returns of BRK and compare them to an expected forward range for Fairfax. I think BRK was a much harder buy back then than FFH is now. My expected return on FFH is also higher than what BRK actually did. I think the market structure is why the opportunity exists.

-

Estimates ticking up plus short covering is my guess.

-

Prem made it clear they are not proud, they are grateful. I think they are just trying to explain to the shareholders they want to keep why they should hold on to their shares. I think the annual report did a great job doing that as well.

-

I appreciate these look backs on individual investments that you do @Viking. The stock is arguably pricing in <5% returns on the equity portfolio which is low vs recent history and inconsistent with fair value vs carrying value.

-

I never liked this reason for not making an investment in something which is probably why my portfolio is littered with microcaps.

-

We wouldn’t know if they did unless they owned more than 10% because they wouldn’t have to file otherwise. @kodiakand I have discussed this before and I agree with him that it’s because Buffett sees Prem as real competition and doesn’t want to lower his cost of capital. If Abel can get away from that line of thinking BRK should buy as much as they can up to 1.5x BV.

-

I’m relatively new to the company but the culture seems more collaborative than Berkshire. Hamblin Watsa reminds me of my own experience on a prop desk where everyone was encouraged to speak their mind but with much better capital. The Investment Committee does their job I’m sure.

-

Love to see it. Exactly the kind of holders we need before the next hard market.

-

Are you planning to speak at the AGM next week? We disagree on almost everything. I think it’s because we have different time frames and different views on market structure (doesn’t seem to factor in your analysis), not because I’m conflicted, a Trump cabinet member or a mullah but you are entitled to your opinion.

-

Sanmar has been a problem for a long time and most of the valuation was based on its publicly traded subsidiary unlike DCFs for the other private holdings. Definitely annoying but I don’t think it’s systemic.

-

They have an ASPP. They do seem to drop the limit when they are in blackout period though.

-

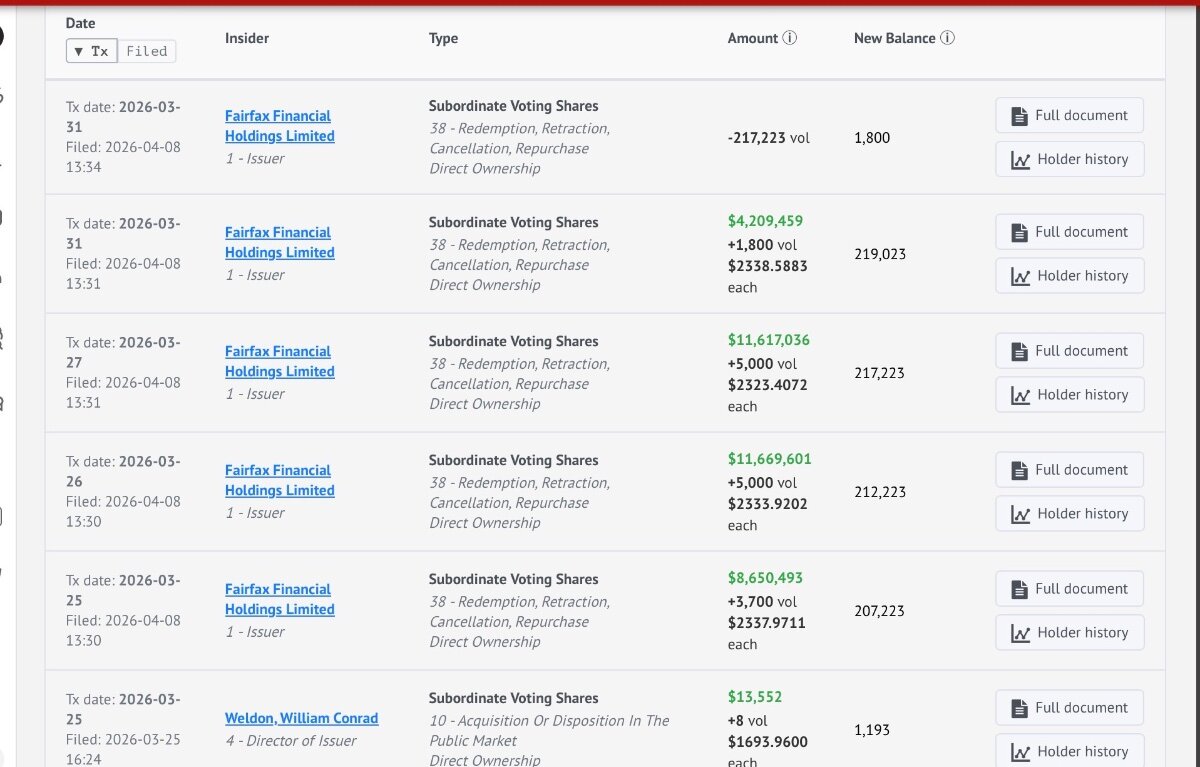

FFH got more aggressive on the buyback in March cancelling more than 1% of shares outstanding. I haven’t calculated it carefully but I think they have spent over $600m on buybacks so far this year which is about a quarter of what I think they have available for buybacks this year. So right on pace I suppose!

-

Diversified by project, more liquid and cheaper are pretty good attributes too. Will be interesting if they hold on.

-

Makes sense. The reserve price must be falling fast with the number of shares trading 70 and below.

-

I think they buyback the shares like they did with the first lot of 200k. It makes the most sense but we’ll see.