SafetyinNumbers

-

Posts

2,811 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

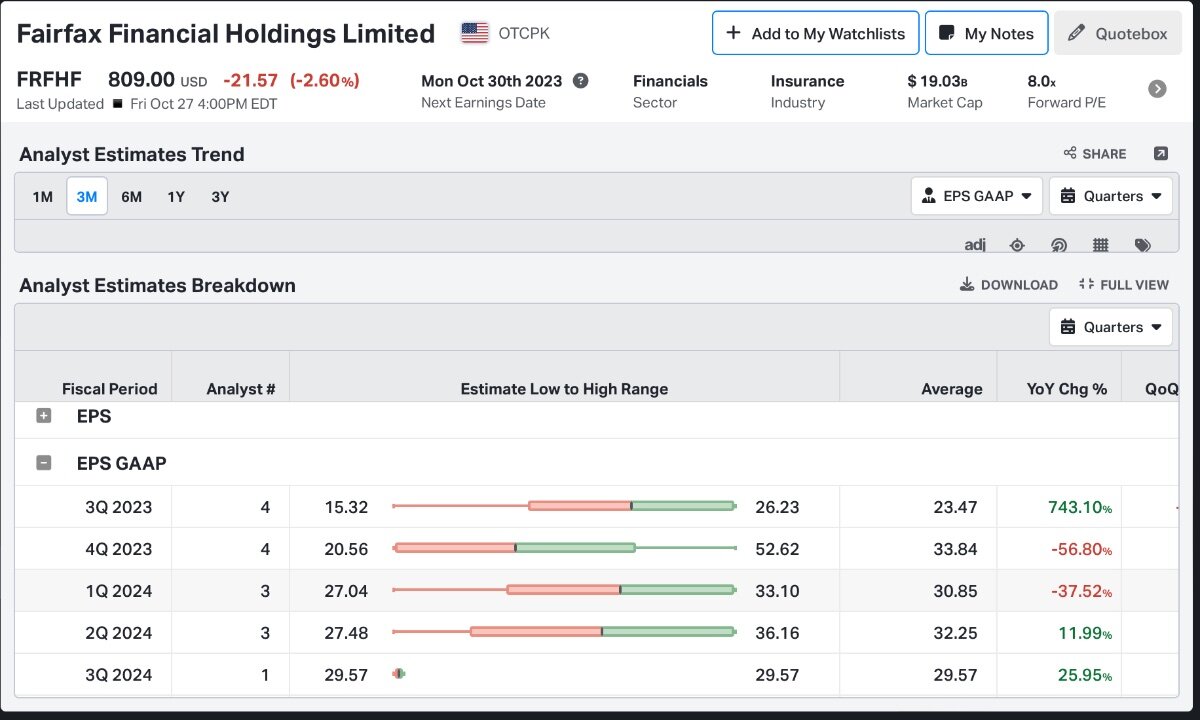

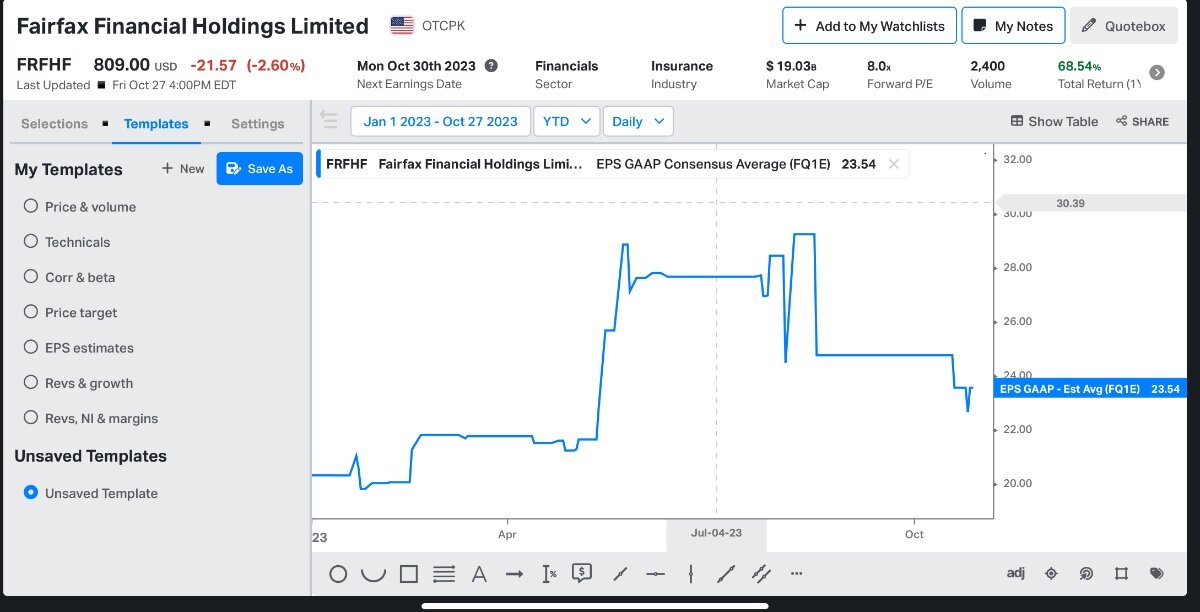

I expect we’ll get some more previews this week before they report but here’s the lay of the land with respect to analyst expectations

-

Unfortunately I can’t share the note but it’s really well done.

-

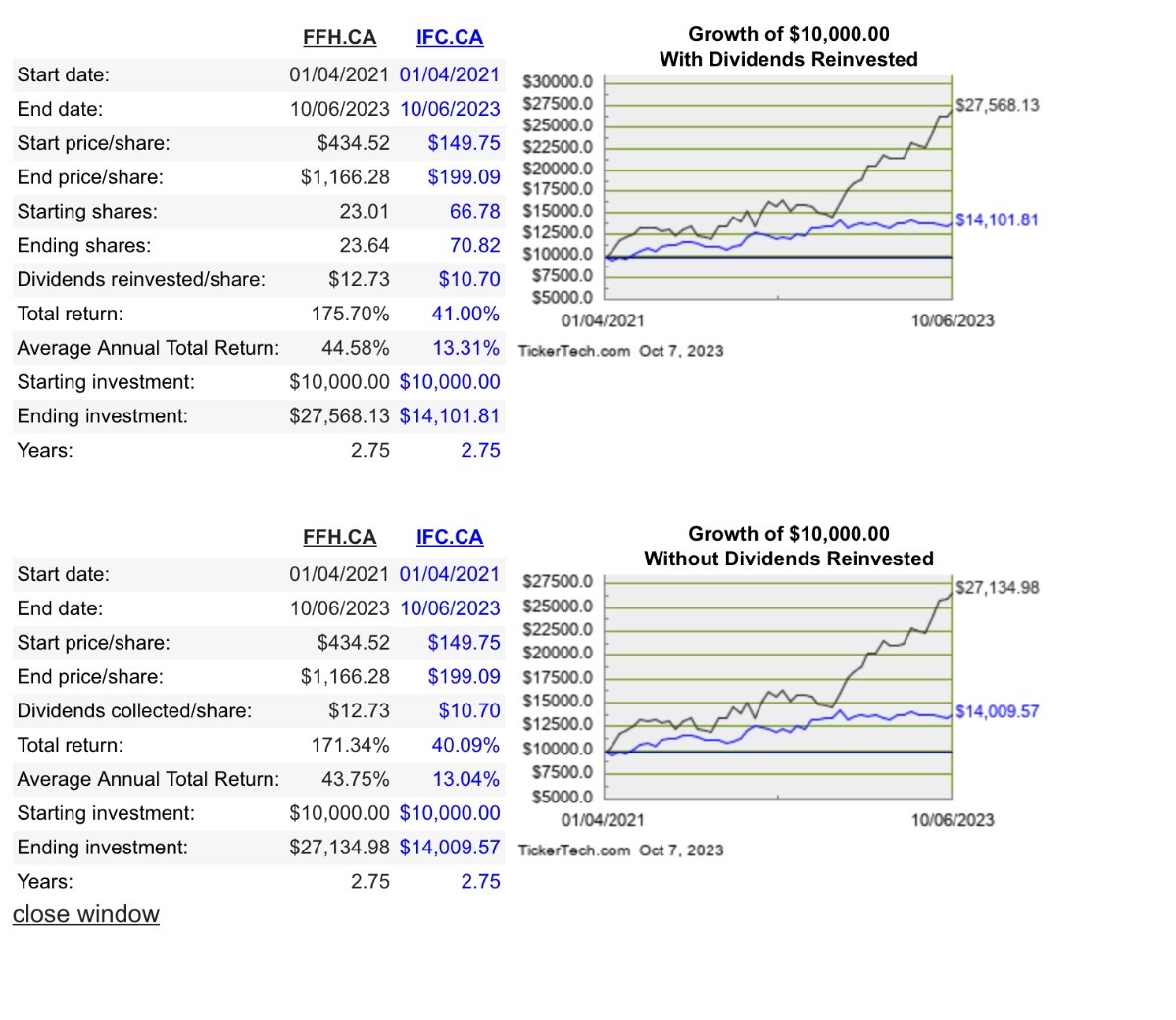

This is very interesting. Does Fairfax own the same class of shares as Blackstone directly or a different class with different terms?

-

Thanks for sharing! Probably why the stock was up almost 5% last week while the Greek market was flat.

-

I try to think about it context. Shareholders were cheering the shorting at the time and rewarded Fairfax with a 1.3x BV multiple while they issued equity for the treasury and Allied World in 2016 which was the end of the shorting. They didn’t like the shorting in retrospect because it didn’t work out and book value growth stagnated for 7 years. The share count also went up ~35% over that period while revenues were up ~2.5x. It’s not surprising a lot of those newly issued shares were dumped in the following hears with Fairfax buying back more than half of them. I think a lot of people share your view and those who have been burned may not come back. I’m sure others are selling now because “it’s had a nice run” and they don’t want to own it for Prem’s next mistake. None of that matters as long as book value growth is double digits. With the float as big as it is and interest rates where they are, it’s hard to imagine that not happening over the next three years. Nothing is a guarantee as these are all probabilistic bets after all. If Fairfax executes, institutional investors will find it again and the multiple should increase. I think a lot of investors will miss out by selling too early trying to avoid a drawdown when the path for high growth in book value seems so promising.

-

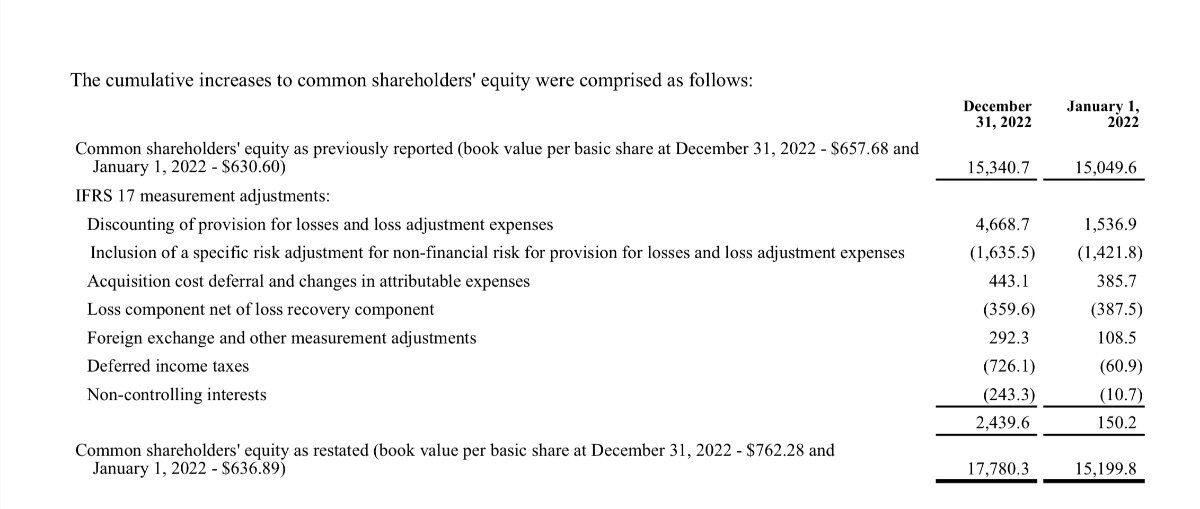

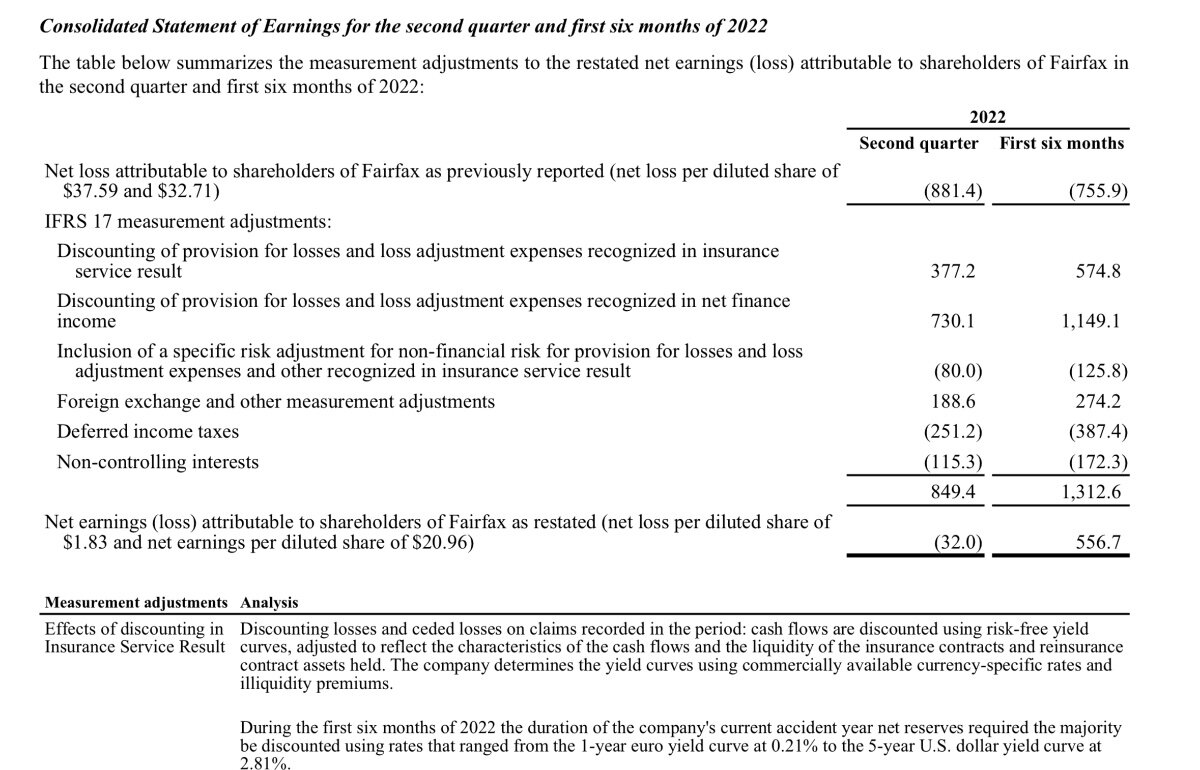

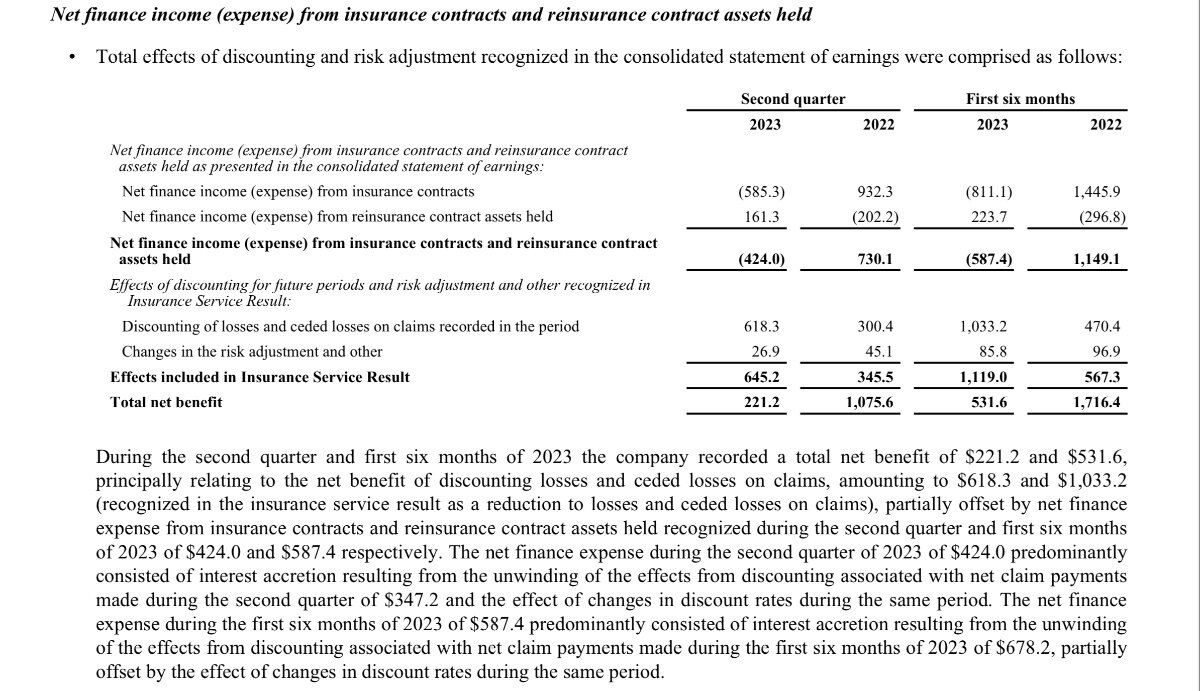

I don’t think I fully appreciated how much Fairfax would have earned last year if IFRS 17 had been implemented a year earlier. I know they got the full benefit in the book value at the beginning of year and it’s helped by half a billion or so this year (so far) but to actually report the earnings would have had a bigger impact on valuation I think. It also really highlights the spectacular macro call of keeping short duration on the bond portfolio. IFRS 17 only increased book at Jan 2022 by ~$150m. The majority of benefit actually came in 2022 as rates increased substantially. The restated H12022 results go from a big loss to a profit.

-

It’s funny, I read the same post and it made me think I was right. I think to take out the IFRS17 plug, you have to assume no premium growth which isn’t consistent with the rest of the forecast.

-

We didn’t see an SIB but the buyback picked up just over 1m shares in September

-

I want to make it clear I’m not an insurance expert, my MAcc degree is 23 years old and I let my CA/CPA expire a few years ago to save on the fees! My premise is that as long as interest rates are positive and rates are unchanged, the discounted combined ratio will be lower than the undiscounted combined ratio assuming a growing business. I assume when a policy is sold, premiums are collected and reserves are set aside. If those reserves are discounted, the underwriting profit is by definition higher all else being equal and that should happen every quarter. The quarterly offset, however, is the reserve balance must also accrete at the same discount rate. Before IFRS17, in order to model underwriting income, an analyst will most likely estimate a combined ratio based on the trend in the reported undiscounted combined ratio. After, IFRS17 that’s still all Fairfax is giving us explicitly so that’s still how underwriting income is being modelled. But there is a plug needed. I don’t know if $480m is a fair estimate. If the discounted combined ratio is 300bps lower than the reported combined ratio and Fairfax writes $25b in policies, does that mean $750m in additional profits? In theory that includes any accretion from the reserve balance. I’m not sure at all but it makes sense to me.

-

I know you asked Viking but I think about this a lot so I hope you don’t mind my thoughts. My understanding with IFRS 17 is as long as interest rates aren’t zero there will be some sort of adjustment. The reported combined ratio does not include any impact for discounting reserves. But every quarter, the existing reserve balance accretes and any reserves for new policies have to be discounted. If rates are flat or going up, that should be a sizeable benefit every quarter. If rates are going down, the reserve balance will be revalued higher but the discounting of the new policies will still be positive. I think most analysts are ignoring this and that’s part of why their earnings estimates are too low. Intact breaks out the discounted combined ratio (see below) and for them in the first half it was a 440bps difference. I’m not sure what the right number is for Fairfax but it’s not zero. That being said at some point in the future if rates fall fast enough, the discounted combined ratio might be higher than the reported combined ratio.

-

They are at US$980. The increase in interest rates means a structural increase in ROE vs the last 20 years. Should be interesting what the narratives will be when the multiple expands and how quickly holders will jump ship. There will surely be lots of drawdowns that investors will want to avoid.

-

-

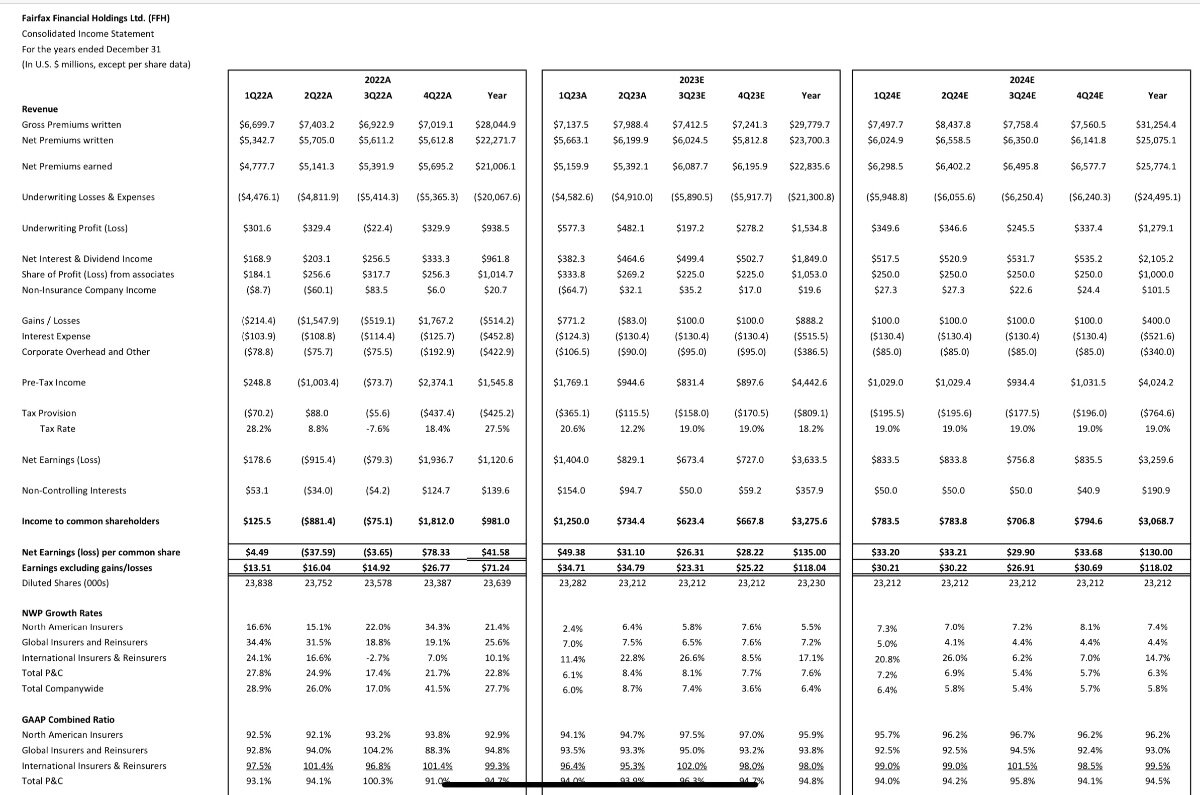

I think part of is it they miss the IFRS 17 impact on earnings because they model underwriting income on the stated combined ratio while the IFRS adjusted combined ratio has been lower. Viking has something in line 4 of his model above. When I look at RBC’s model, they have the combined ratio down but also have underwriting income down year over year. When I was in equity research we would say that’s not internally consistent. For 2024, the growth in investment income is underestimated based on current rates, associates income is held flat from 2022 despite H123 at ~60% of 2022 already and gains expected on the equity portfolio are very small. He’s at $130/sh for 2024 and he might be right but the odds seem low.

-

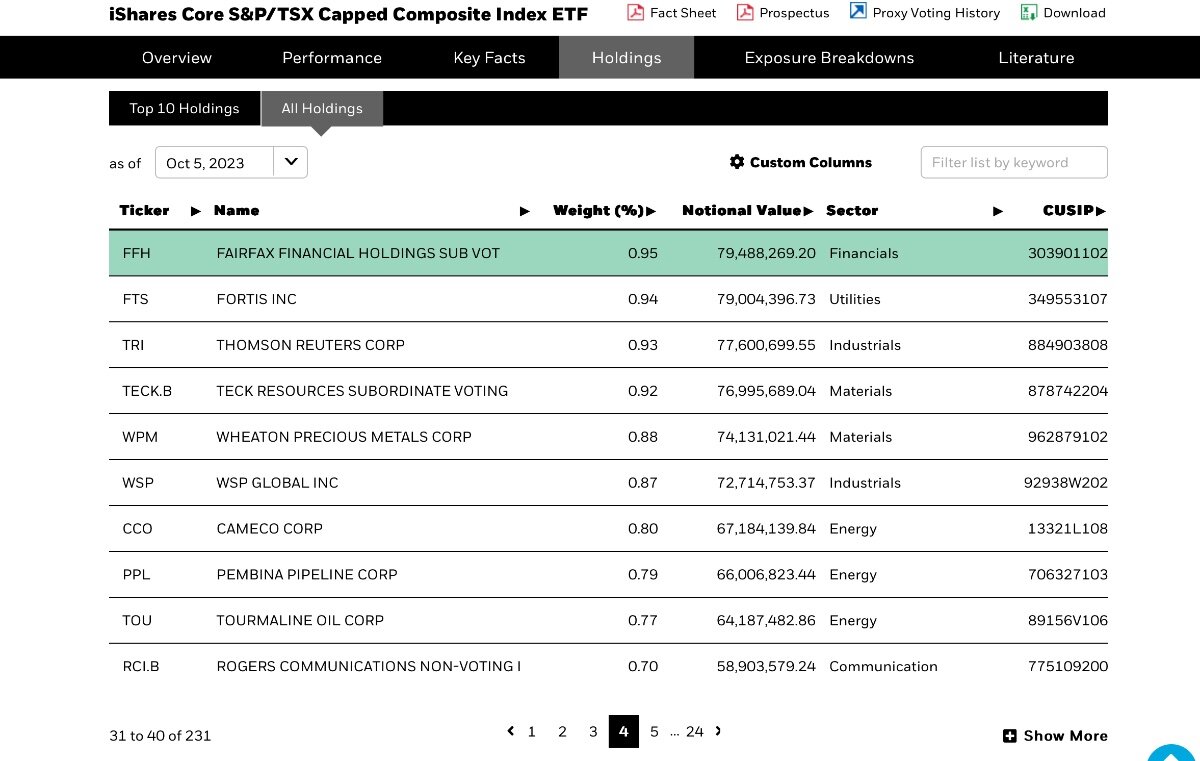

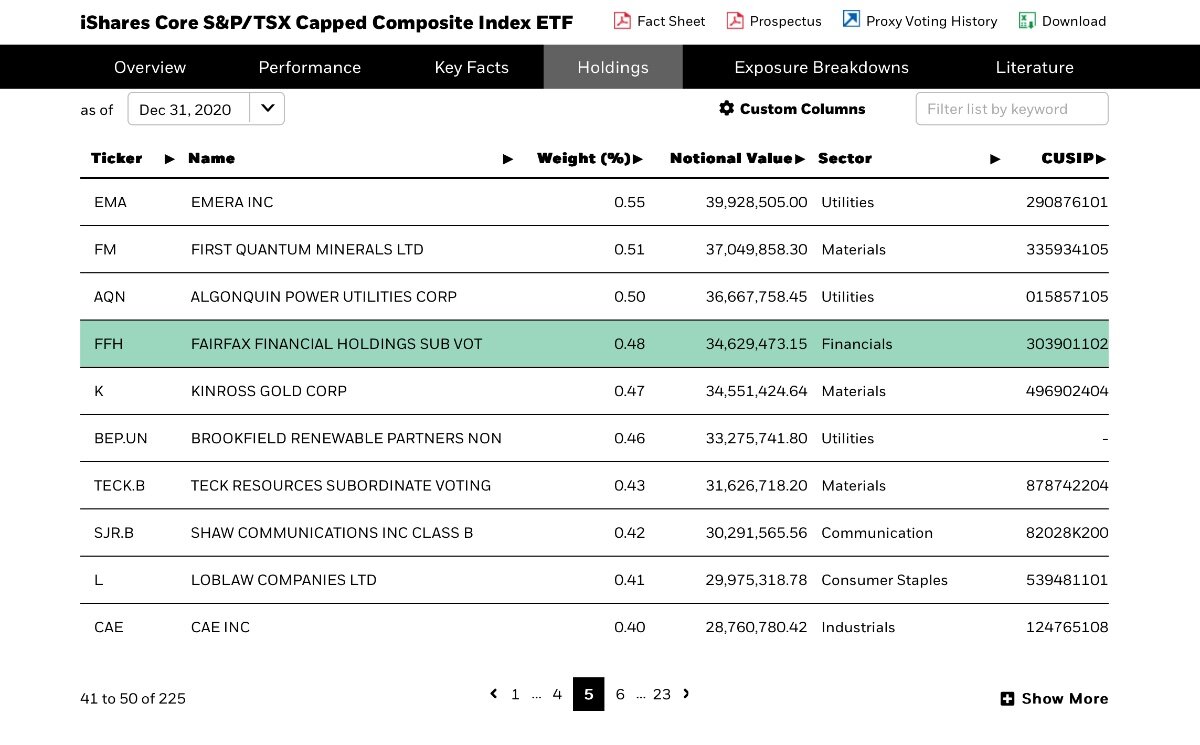

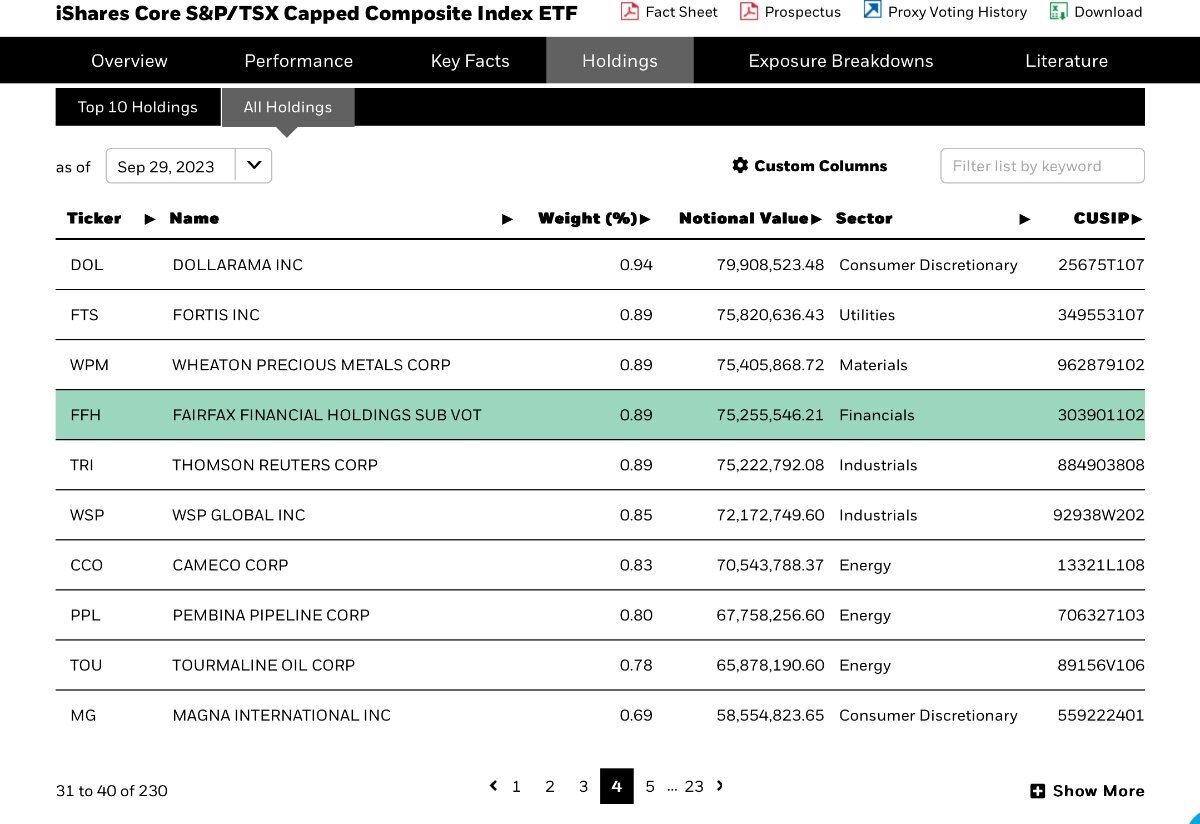

I’m more focused on the weight in the S&P/TSX Composite. While it’s counterintuitive to most value investors, the higher a stock in a major benchmark goes, the higher it will go as long as returns are consistent. For Fairfax, that seems highly probable given the proportion of income coming from investment and associates income. Fairfax has almost doubled its weight in the index since YE2020 to 95bps. My understanding is that active institutional managers benchmarked to the Composite will likely reconsider Fairfax again when it crosses 100bps. That seems likely to happen in the next month as Fairfax reports Q323. My guess is that book value is closer to $875 which will drag the shares higher as our fellow shareholders will hopefully not want to sell below book. If we go through 100bps, that I think can lead to multiple expansion finally which along with strong earnings will encourage analysts to raise their estimates and target multiples. The next step will be getting bigger than Intact Financial which is heavily owned by those benchmarked to the Composite. It sits at ~125bps. A lot of managers arbitrarily decide they only want exposure to one P&C and there is no reason to sell IFC except it has really underperformed Fairfax recently.

-

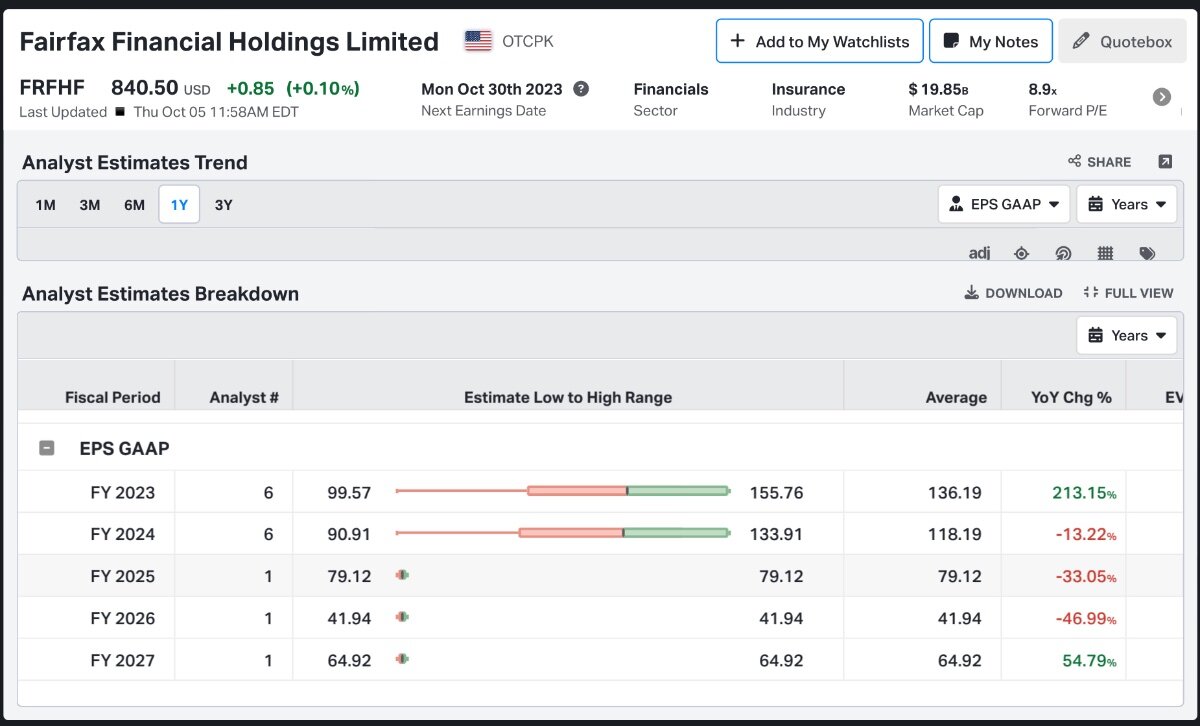

It doesn’t matter if you don’t think he’s credible. His estimates influence quants and those who use quant screens (most active management) such that they can’t even consider Fairfax. In the long run, it doesn’t matter as long as Fairfax keeps executing which seems highly probable given the sources of earnings but it’s part of the reason why the market still hasn’t valued Fairfax in line with peers. It also looks like he just cut his earnings estimates again.

-

I don’t think he speaks to any actual investors in these names or risks any of his own capital so I wouldn’t expect the analysis to be any good but it doesn’t explain why his earnings estimates for Fairfax drop so precipitously while staying kind of flat for the other comps. Also, recall, he doesn’t set the target prices, a Morningstar computer does that based on his financial forecasts and moat assessment.

-

Does it have the chance of being a hot IPO? I think stand alone IOT and Cybersecurity businesses both trade at high P/S multiples relative to where Blackberry trades. Maybe rebranding and making it a pure play will get the new ticker a big audience. M&A would also be easier for both segments once they have price discovery. It makes sense to do a marketed offering to get the multiple. It will presumably be a tight float so has meme potential given Blackberry’s iconic brand. I don’t know how to value these businesses so won’t participate but it does seem like it has event driven potential for someone with the right skill set. Could get interesting for Fairfax too.

-

Found it. Morningstar-MKL9.23.pdf

-

The style drift is getting a macro call wrong that shareholders were big fans of at the time they were placed.

-

I think the large transition from value investing to passive and quants has amplified the desire for a smooth 10% to a lumpy 15%. Social value is also a much more relevant factor and BRK/MKL enjoy very loyal shareholder basis. They never think about selling. Meanwhile, almost every Fairfax bull I talk to is waiting anxiously for Prem to make a mistake so they can sell before experiencing a drawdown.

-

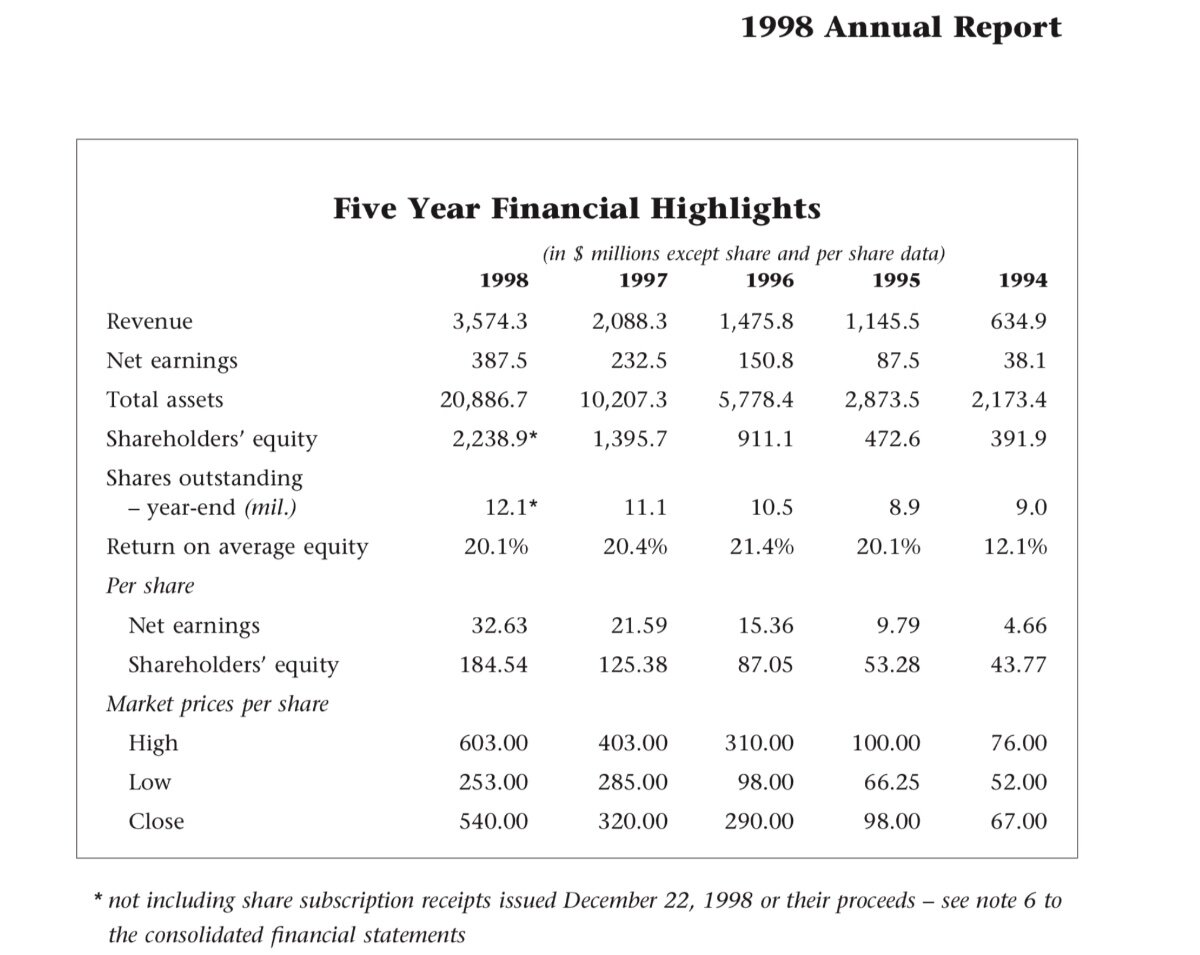

I agree with your take @MMM20. The float to market cap ratio locks in so much ROE vs the comps. Fairfax’s equity portfolio is also a lot cheaper on traditional measures of value so arguably adds relatively high long term built in ROE. Plus they have a disproportionate amount of earnings to redeploy in safe acquisitions like buying the rest of Allied World, Brit and Odyssey over the next few years which will just makes them all the more durable. I’m betting the index huggers chasing the stock will start using the increased durability as a narrative for why they are buying stock at 1.5x book value. It will still be the right thing to do as it might even get to 3x like it did in 1998. For that to happen, the ROE has to be elevated for a few years in a row. We are off to a good start in 2023. The low risk income off the float, hard insurance market, high level of associates income, Digit/BIAL IPOs make it seem likely the ROE can stay strong for a few years which is why I continue to think Fairfax is a fat pitch. @Viking’s earnings forecast could be conservative. Value investors rightly focus on the margin of safety but I think most investors actually interpret that as avoiding drawdowns. While a lot of us here spend a lot of time thinking about Fairfax almost no one else does. It’s still well under owned by Canadian asset managers despite its weight in the S&P/TSX Composite at ~89bps at Q323. Today, it outperformed by almost another 5%. 100 bps is within spitting distance but passing Intact which is around 125bps might be the bigger deal as PMs likely only want to own one P&C insurer even though Fairfax is special because of its equity portfolio and capital allocation strategy. Ironically, the higher it goes, the higher it’s likely to go which means most value investors will likely sell too early. Earnings estimates still show declining earnings for the next few years mostly because expectations are for lower interest rates and low investment returns on equity portfolio. These analysts from what I can tell haven’t actually taken the time to appreciate how cheap, for example, Eurobank might be and how big a chunk of the portfolio it is. While it may be conservative to assume low single digit returns on the equity portfolio, it doesn’t mean it’s a probable forecast. Quants and active manager that rely on quants (i.e. almost every asset manager) can’t even see Fairfax because of the declining earnings forecasts and high variability of historical results. I think there is a good chance analysts will start increasing their estimates to something more realistic if Fairfax keeps executing which again should be easier given the composition of earnings is more predictable. That will finally get the quants thinking about Fairfax. Of course, anything can happen and nothing is guaranteed in markets. It’s always a bet and we mostly all see the odds differently.

-

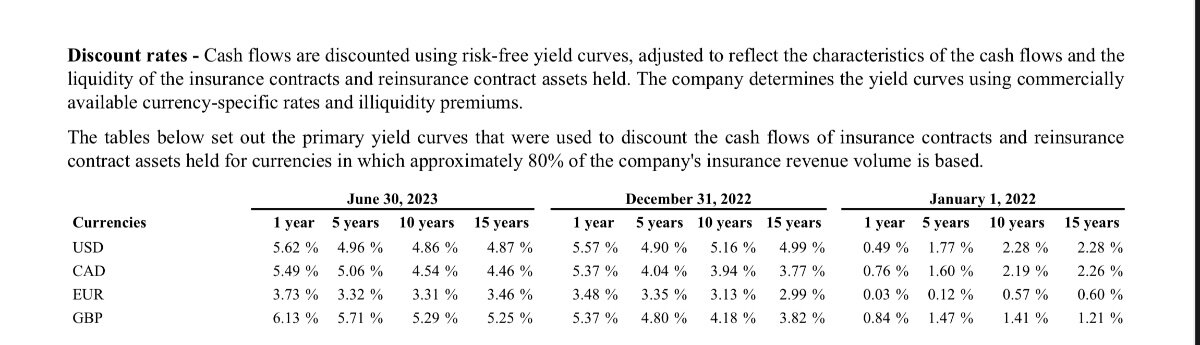

Shouldn’t be much. I think the 3 year was up ~20bps last quarter. There should be some offset from IFRS 17 as the discount rate is up. That should also help the actual combined ratio (vs the reported combined ratio which is not discounted).

-

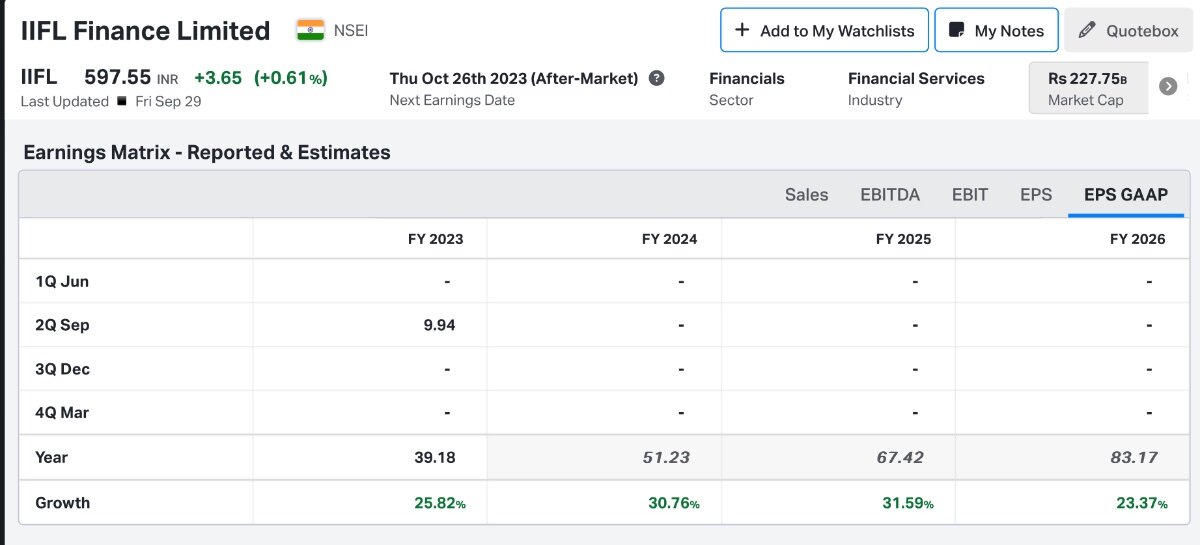

IIFL Finance also looks cheaper vs consensus estimates. It’s interesting they sold some recently to help fund the additional BIAL purchase. If they also use it for buybacks, arguably, they buy IIFL Finance back at a big discount too! From sharing the idea with others it seems like the biggest reason I hear from investors for not owning Fairfax India is the fee structure. In reality, cheap NAV plays without known catalysts to close the discount seem like they will permanently trade cheap (see E-L Financial). The real reasons are no analyst coverage, low liquidity, unpredictable earnings and not being in a relevant benchmark. There is just too much competition from liquid cheap stocks with catalysts i.e. energy, uranium etc and the fee structure is a narrative to explain the discount for not wanting to own stock since markets are supposed to be efficient. What do you all think?

-

I think you are referring to algorithmic quant trading which is an absolute return strategy. I’m referring to quant-based investing which is a relative return strategy with the relevant benchmark being the S&P/TSX composite for Fairfax. It’s also called factor-based investing. You are correct that liquidity is important and only a few quants will go into smaller names but they do exist. Liquidity is probably one of the reasons Fairfax trades cheaper than others. A direct reason how liquidity impacts the share price is not having listed options. Just having listed options means dealers would have to have inventory which would increase the share price. Ultimately, it’s just supply and demand (i.e. a voting machine) in the short term.

-

It’s already in the index (32nd biggest component). Passive and quants have taken so much market share from active managers that active managers are forced to act like passive and quants. They need to buy whatever is getting more relevant to keep up and sell whatever is underperforming. They need to buy what quants buy to keep up with their performance so they don’t lose market share. Ultimately, when Fairfax is added to the S&P/TSX 60, passive will have to buy an additional ~4% of the float but that will take a long time as the index is already dominated by financials. What makes you think quants aren’t active in Canada?