SafetyinNumbers

-

Posts

2,811 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

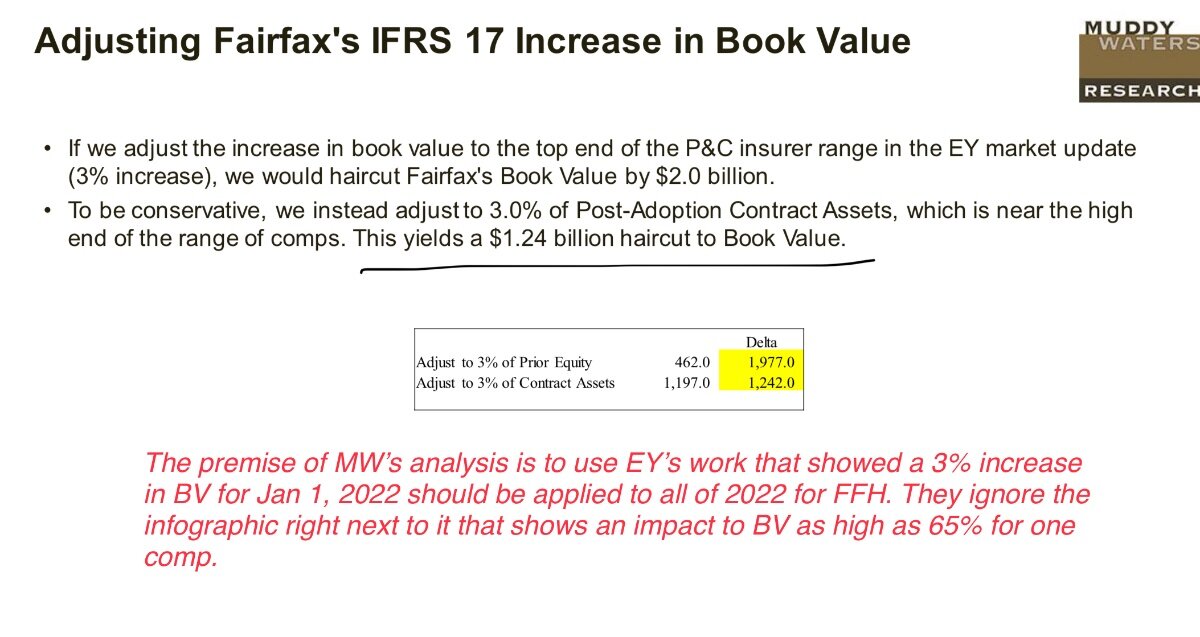

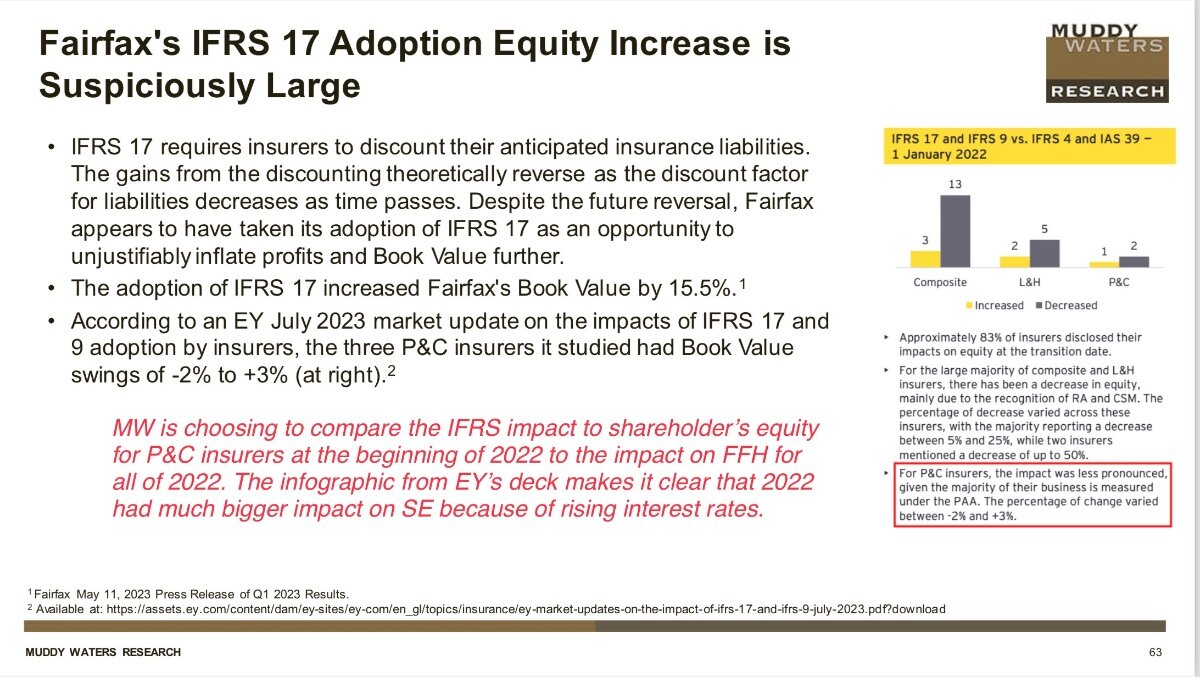

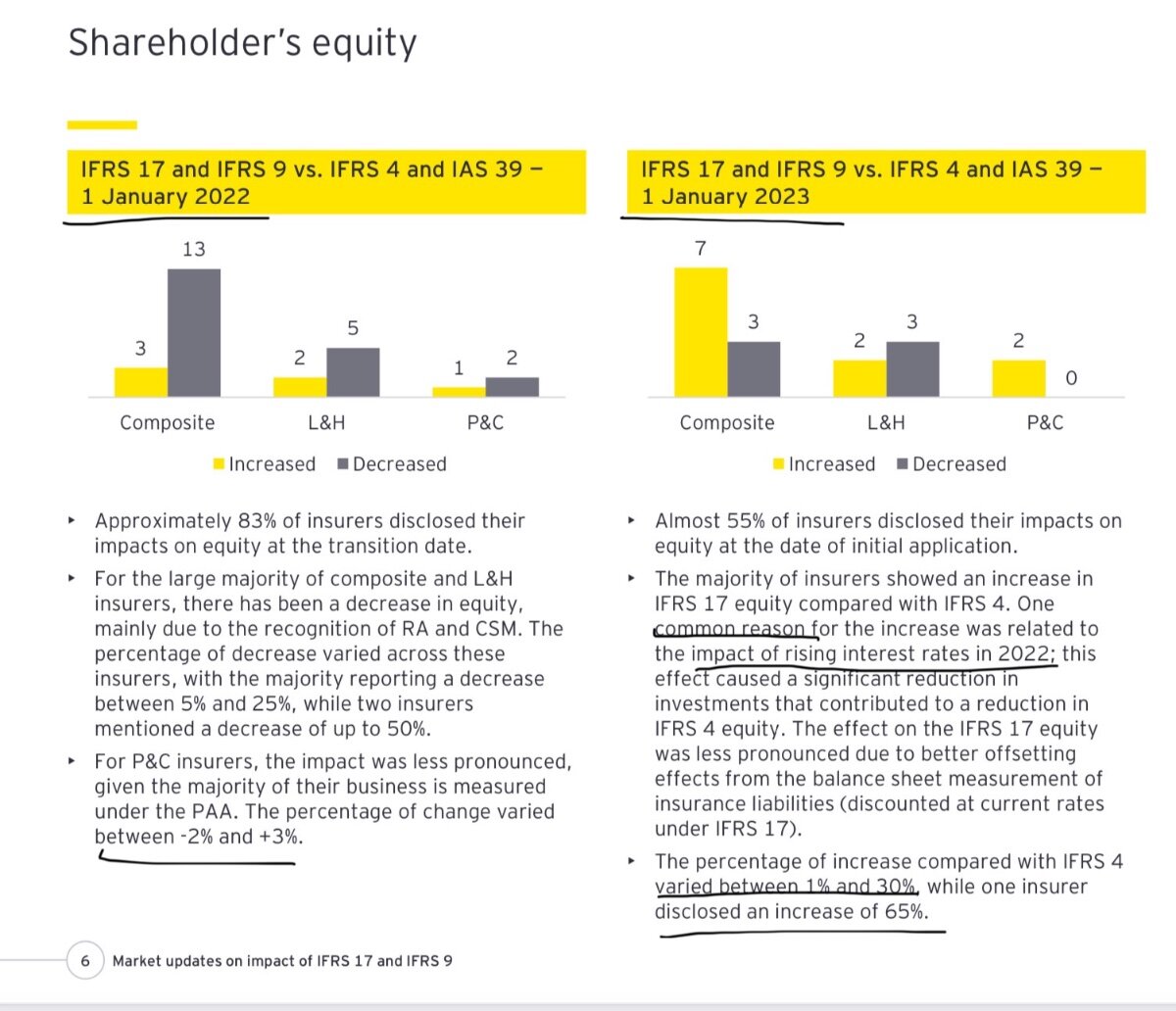

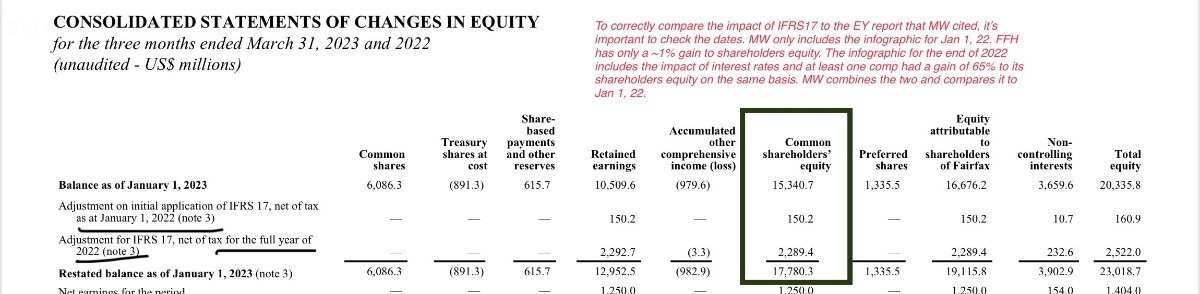

I appreciate all of the good analysis on the board today. Thank you. I spent time with a few PMs today that were buying positions for the first time so they certainly saw it as an opportunity. I tweeted about the MW IFRS 17 proposed haircut and the work is incredibly sloppy. If you disagree, please let me know.

-

I think all of the equity issuances that were well north of book value probably created a lot more value. The most important might have been for Allied World at 1.3x BV in the midst of the zero interest rate era. It really put a damper on ROE and an overhang on the stock which they took advantage of with the moves you noted. Prem's painting quite a masterpiece, it will make for a good book some day!

-

Thanks for sharing Glider! Was a good listen. Overall, the commentary on culture was very interesting and encouraging. I think the most disappointing parts to me were that they think markets are efficient and they manage money the same way they did at Schroders. I think FFH best chance for significant absolute returns is not acting like everyone else and taking advantage where others have constraints that FFH doesn’t.

-

Why 2009-10? The stock wasn’t particularly cheap then from what I can tell.

-

FFH has for the most part traded their stock brilliantly including issue equity well above book value on many occasions. It’s a part of BVPS growth that gets ignored for the most part since with the exception of the TRS, it doesn’t flow through the PnL.

-

I’m not sure but I think with these agreements they buy back at the same multiple they sold at which in Odyssey’s case was 1.9x BV.

-

There is a committee (4 people from S&P & 3 from TMX) that decides. Generally the TSX 60 (XIU) tries to mimic the sector weights of the TSX Composite (XIC) while also trying to beat it. Historically, they have replaced components when they go under 20bp but I don’t think it’s a rule. Financials are already overweight in XIU vs XIC so that might make the hurdle higher for FFH to get in. IFC took a long time to go in for that very reason. When IFC was announced in to XIU in March 2022, its weight at the end of Feb was 104bp and it was the 25th biggest company in the XIC. It was almost inevitable that IFC was going to get into XIU given its above average growth. Now its weight is ~124bp and it’s the 20th biggest weight in the XIU. They would have been better off putting it in sooner. I would argue FFH is a good analog for what happened with IFC. Given the high certainty of near term earnings, FFH’s weight in XIC is only going to increase. Today, I estimate, it jumped from 29th to 27th biggest passing GIB and TRI. Its weight is probably close to 101bp. At the end of 2022, FFH was #41 and 65bp. It’s like a freight train and if the committee can see that, they may want to get it in soon so they don’t lose ground to XIC. I estimate, AQN is only ~21bp in XIU after today’s trading so it’s flirting with the historical replacement precedent of 20bp. Please correct me if I’m wrong but I believe they will use Feb 29 as the measurement date. Presumably, it will be a live every quarter going forward or if a member of XIU is acquired. Recently ABX was rumoured to be interested in FM. If that transaction was consummated, it would open up a spot for FFH as well. Of course, they could always skip FFH and go to TFII but it’s less than half the weight. The biggest impact of Scotia and now NBF socializing the idea of FFH going in XIU is that shareholders who really want to take profits for risk management or because they are afraid of a drawdown might hold on instead. This is important, because most buying is institutional and it’s usually done on a % of volume. It’s a constraint placed by investors on asset managers to protect against them manipulating share prices. The side effect of that is, sellers set the price. Knowing there is likely a significant amount of buying coming sometime in the next year at a time when the company is growing incredibly fast might decide to at least lift their offers. Some shareholders might even hold on and see if they can get a better price when there is an indiscriminate time constrained buyer and reported BV is likely somewhat higher. The float in FFH is relatively tight and underowned by Canadian institutions who are benchmarked to XIC. If shareholders start believing what NBF is telling them, the multiple expansion could be significant. P/B could get out of hand. It’s happened before from 95-98, a period when FFH put up 20%+ ROE for 4 years in a row. Maybe 2023 was year 1. P/B went over 3 back then before coming back to earth. It seems more likely to happen in this kind of market (meme stocks etc..) but it might take analysts starting to believe FFH can grow earnings consistently as some quants also set prices. Morningstar coming around would be a huge signal. I don’t expect that to happen but it’s possible.

-

It’s a really good note. Hopefully makes it harder for those funds underweight vs the benchmark to ignore!

-

Canadian exchange traded debt

SafetyinNumbers replied to SafetyinNumbers's topic in General Discussion

The strategic review that ECN announced is what peaked my interest. SKY ended up doing the private placement and apparently wants to buy Triad but wants nothing to do with RV/Marine. Everything ECN has done since is to try and clean itself up for SKY. Ultimately, they still have to execute though. The ACD bonds don’t seem very interesting to me. Like you pointed out, the reward is much higher in the equity. -

He provides the earnings estimates and the moat rating. The quant machine spits out the target price. But he’s especially bad at estimating forward earnings. They don’t make any sense. Ironically, his earnings estimates make other quants want to avoid the stock because they show high variability in earnings estimates and show earnings declining. Things that are not generally associated with quality and what quants prefer.

-

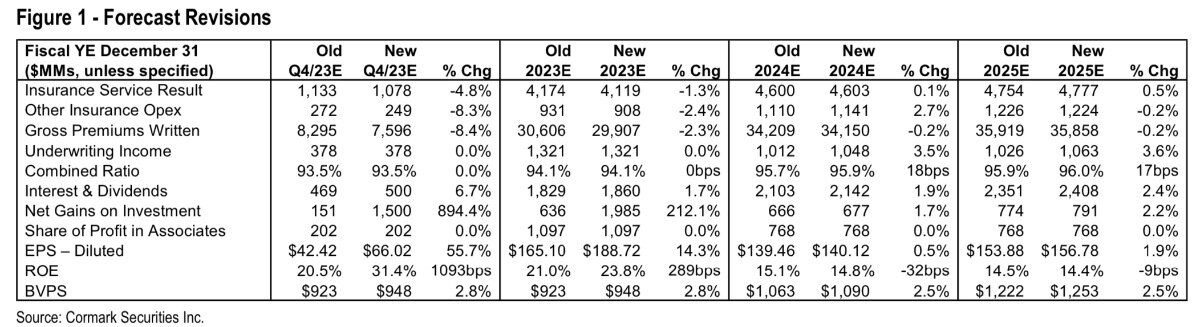

Pretty much the only reason, I think FFH has stayed cheap is because of quants. Volatile earnings streams are by definition not quality. Earnings growth modeled by analysts is also a necessity for most quants to get involved. This rules based approach has worked on a portfolio basis so they won’t make exceptions to over rule the model. Will analysts finally start modeling in earnings growth as the multiple expands, we’ll have to wait and see. Even Cormark with their US$66/sh estimate for Q423, still has them earning only US$140 in 2024. There is no point being a hero when the stock trades at ~ 7x conservative estimates.

-

Canadian exchange traded debt

SafetyinNumbers replied to SafetyinNumbers's topic in General Discussion

Thanks. A big part of the ECN trade is its event driven nature. If they sell the business which is pretty much what they are telling us they are going to do, then ECN.DB.B gets 104.875 + interest until the end of 2024. The sooner a deal is done the better and of course they actually have to do it. I disagree that the goodwill/intangibles aren’t worth anything. Most value/debt investors don’t want to pay for them but origination is valuable because with the right structure it can create significant ROE. I assume that’s why SKY was willing to invest new equity above TBV. On a related note, it will be interesting how much CHW and ACD trade for when they are sold. If you haven’t looked at ACD, it trades at close to half TBV and I think they have every reason to go private given the current conditions. Agreed on the DRT. I like that one of major equity backstops for the rights issue also owns a lot of bonds. I think the rights issue was a clever way of getting a larger stake in the company while ensuring the debentures get paid off but they have to execute too. Equity holders have a lot more faith than the debt holders! Thanks for taking a look. -

I’m guessing the buyer is already short. Coupon probably not too high, relying on the volatility and optionality to pay the majority of the financial cost. I’m not a convert expert but my guess would be a conversion price 30-50% above the recent price and a coupon in line with the reference risk free rate. Maybe 5% dilution and that’s only if the stock goes up a lot which no one seems to believe can happen. It looks optically expensive but it’s a pretty tiny market cap. I’m not sure if there is room for margin improvement and or growth but with a new CEO it might happen and create a lot of Social Value. I don’t own any. If anyone does, please consider sharing your thesis.

-

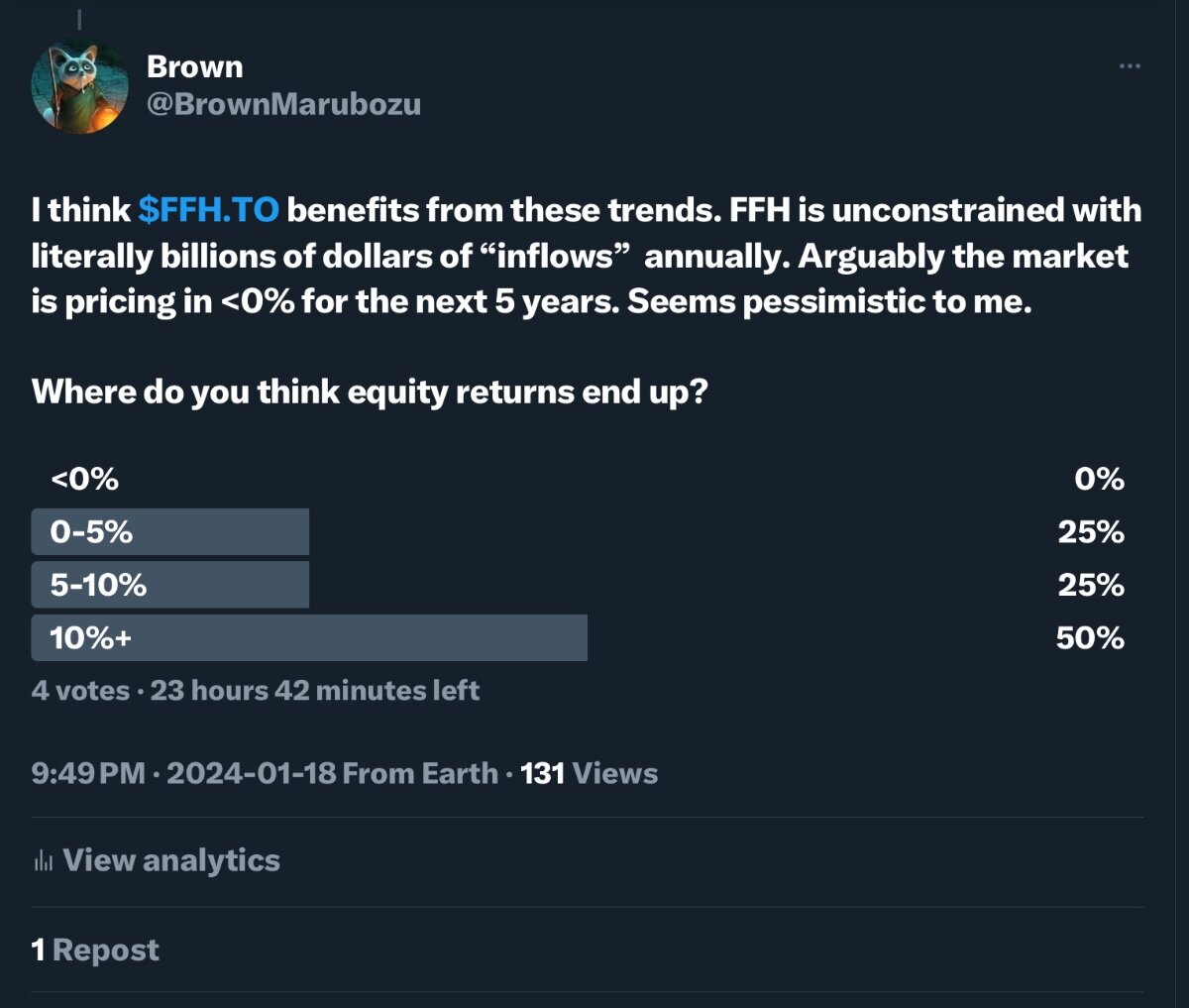

I set up a poll. Please vote!

-

Market expectations vs CoBF expectations

SafetyinNumbers replied to SafetyinNumbers's topic in Fairfax Financial

That’s interesting. I think quality tends to trade in or above its intrinsic value range if the underlying is very liquid and has predictable earnings streams. I think picking idiosyncratic ideas from everything left over has a good chance of success. -

This poll was inspired by this terrific interview w/ Bill Nygren. I posted the same poll on Twitter and thought it might be interesting to see how the responses differ if at all. https://www.fool.com/investing/2024/01/17/next-great-value-stock-bill-nygren-explains/

-

it would be interesting if they found a single buyer for it like a pension plan or endowment fund. That could be structured very creatively too.

-

I don’t think it’s necessary to get multiple expansion to justify keeping the TRS on given BV growth + dividend is well north of the cost of keeping the position on but the optionality is pretty great.

-

I think you’re correct. The multiple is open ended so if FFH can keep up a strong ROE, the flows could take multiples above fair value (north of 3x) but I doubt most of us will have the patience to hold on that long. I think it’s important to think about the outcomes probabilistically to avoid selling too soon and letting in the institutions that are underweight in too cheaply.

-

All great points. I think most investors are focused on the downside risk and not the optionality which is open ended on forward ROE and multiple expansion. With the stock trading ~1x BV, the market is assuming a forward ROE of 10%. Based on Viking’s analysis, it’s pretty clear that the odds of only a 10% ROE for the foreseeable future are pretty low. I would argue the odds of 20% ROE over the next 3-5 years are higher. If forward ROE does surprise i.e. exceeds 10% for a few years, the multiple might expand to where IFC trades or where FFH has traded historically I.e. 2.5-3x+ P/B. I think with Fairfax’s near term outlook, the stock is unlikely to trade below 1x so the multiple expansion optionality also seems to the upside. Multiple expansion so far has been relatively slow. Lifting 0.1x P/B in past 6 months. That could change dramatically once those benchmarked to the S&P/TSX Composite/60 figure out that FFH is likely next in line to go in the 60. That equates ~1m shares of buying in a short time frame which has a greater impact than buying spread out over long periods of time. Further, all of those benchmarked to the index may feel compelled to get to market weight so as not to underperform. It makes sense to do that before the add and not after but plenty of both is possible. Inevitably a spot in the 60 will open up and it could happen at any time either on active deletion or M&A.

-

Thanks for sharing. The EUROB position is ~US$100/share so a significant chunk of the share price. Coincidentally, Fairfax’s share of EUROB’s expected dividend for 2024 is about US$5/share or the same amount as FFH’s dividend increase. European bank valuations are low so lots of room to rerate but hard to bet on. It might mean that earnings estimates are too low though as high returns are available for excess capital like the Hellenic Bank acquisition.

-

I think FFH and ELF would be diversified enough and provide decent returns. FFH has exposure to fixed income and inefficient markets. ELF is a good substitute for index funds as on a look through basis it owns VOO and diversified global GARP stocks. Both offer cheap leverage for structurally higher returns.

-

We’ll find out if FFH added to their position when they report earnings. Recall, they adjusted their agreement to be able to add late last year. The stock hasn’t really done much in two months, why do you think it looks particularly bad now?

-

Thanks for sharing. I assume the Committee also has to consider the relative size of FFH vs whatever it’s replacing in the 60. Perhaps that mitigates the historic 20bp rule of thumb. It would be interesting to know the ratio of weights of every add to every deletion historically. That might give us a clue as to when they might act voluntarily or when Fairfax might become an outlier. My guess that this likely happens in 2024, is somewhat predicated on strong book value growth and multiple expansion leading to a much higher weight than 96bps by the end of 2024. Lots of things have to go right but I still like the odds.

-

Terrific post as usual Viking! It made me think about what could be on the 2024 list. We already had the 50% dividend increase. I think there is a decent chance Fairfax gets added into the S&P/TSX 60 in 2024. It's already 29th biggest in the S&P//TSX composite so when the next spot opens up, it has to be near the top or on the top of the list. That would generate ~750k-1m of buying in a very short period of time. I would expect a lot of managers benchmarked to both of those indices will have to take another look at Fairfax and increases the chances they decide to go to market weight from no position. Chances also are PMs will have to revisit being overweight IFC, if FFH becomes a bigger weight. IFC is currently 22nd biggest in the Composite at ~121bp and FFH is 96bp. The anticipated Eurobank dividend might have a very big impact on valuation as Viking pointed out. IPOs of Digit and BIAL would be huge. It was easy to come up with 5 potential Top 10 items for 2024. What else would you throw on the list or is there anything on my list have less than a 50% chance of happening? Top 10 (mostly predictions) List 2024 (in no particular order) 1. Dividend increase 2. Addition to S&P/TSX 60 3. Eurobank dividend 4. Digit IPO 5. BIAL IPO 6. ?