SafetyinNumbers

-

Posts

2,813 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

if I understand the IFRS reg correctly, book value would go up by about ~$48m with the balance credited to NCI. Does that look right?

-

Nice timing with the dip in rates. Also it looks like the spread came in about 65bps vs the 10-yr note it’s replacing.

-

See the FT article attached. BIAL is also working on their master plan which they revise every few years. It has some operational details included in the article. https://indianexpress.com/article/cities/bangalore/bengaluru-airport-master-plan-renovation-9049746/

-

FFH does any insurance investments and FIH does everything else so there is no conflict there. FFH has bought shares in the open market and FIH has bought back shares at a big discount. Almost no shares have been issued below NAV and they have bought back significantly more below NAV. We’ll see what they do this year. They might surprise and take it in cash and ideally tender for shares. The parties that really let down minority shareholders were those who negotiated on their behalf i.e. OMERS etc… The agreement incentivized minority shareholders to buy the shares into the measurement period at the end of a performance period but they haven’t shown up.

-

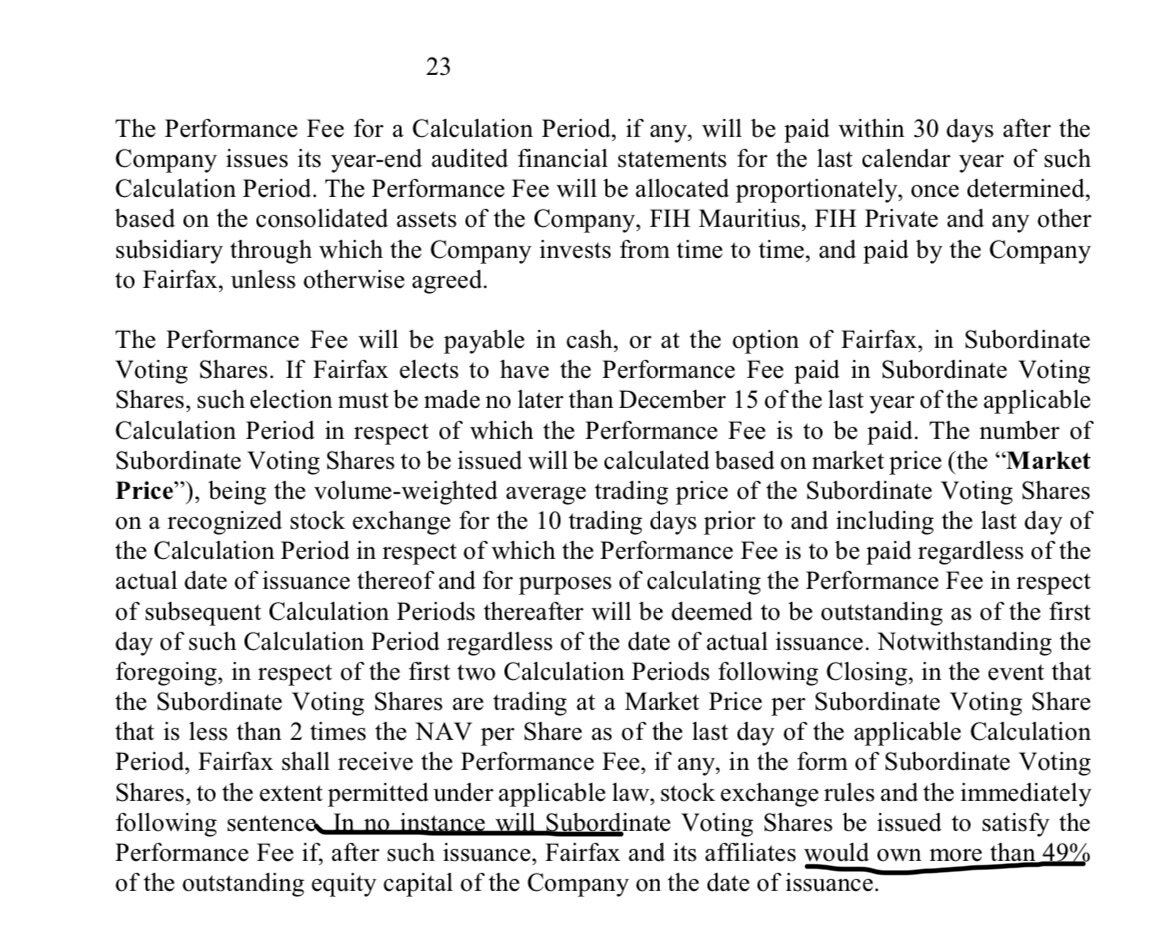

I don’t think they will take FIH private. With OMERS stake, they can never own more 90% but they could buy every other share back over time. There is no ownership limit, it just doesn’t allow FFH to elect shares for payment of the performance fee if it means FFH would own more than 49% of FIH. They should hit that by the next performance fee period end in 2026 assuming continued buybacks or big enough performance fee given they are at ~43% now. I don’t think institutions want to own it because it’s not in their benchmark more so than the liquidity. It seems pretty easy to buy most days and I know a small cap manager that recently bought some for his fund. I do think it’s interesting how no one wants to buy the shares that actually closes the discount which makes sense as it’s mostly active value investors that are looking. That sort of buying comes from quants and passive these days. FIH won’t ever have that kind of buying. Kind of like ELF in that way. One positive aspect of FIH, that doesn’t get mentioned a lot is the cheap leverage. $500m note that doesn’t mature until 2028 at 5% is a pretty cheap cost of capital. As you have pointed out often recently, Viking. FFH is pretty good at managing debt. Issuing 7 year 5% paper when the 10-yr was ~1.5% in 2021, was another stroke of genius. Buying FIH at these prices is ~2 to 1 leverage which is a lot better than an India ETF and that’s probably the switch trade investors should be making but no one on this board likely buys India ETFs as a long term investment. I think it’s impossible to know when the discount will ever close enough to realize the return but I’m invested anyway. I appreciate that people have better alternatives in what I believe is a very inefficient market.

-

Very good points TwoCities. I think the sentiment is the impact of passive and quants on ownership of a company that’s not in anyone’s benchmark and has no earnings estimates. Add to that a much more inefficient market and active investors think and probably do have better risk/rewards with much quicker payoffs. It’s hard to find the marginal buyer besides the company and FFH. Maybe that changes with the Anchorage IPO as it will dramatically increase the marked-to-market portion of the portfolio and potentially give FIH a vehicle to grow with that has a low cost of capital in India. Also as I believe @glider3834 pointed out, once Fairfax is at 49%, they can no longer accept payment of performance fees in shares so this performance period is the last one for which that gripe matters. Despite all of the consternation it hasn’t mattered for the first two performance periods for two reasons. First, the stock was close to NAV for the first performance fee period and the performance fee was only ~500k shares for the second period. Second, they have bought back way more stock cheaper before and since those fees were paid. If they choose to take stock this time then almost certainly if they want more they will have to buy them in the market and I’m guessing they will. Hopefully not too opportunistically but that has to be the expectation. Buying near the floor of the discount seems like a good risk/reward. I guess we’ll find out.

-

It doesn’t fit with what I understand Prem to be all about. Do most people agree with Stubble?

-

Prem seems to be saying never https://financialpost.com/executive/capitalist-manifesto-how-capitalism-and-canada-made-prem-watsa

-

I thought it was clear I was discussing FFH. Sorry for the misunderstanding. And no I don’t think he would ever take Fairfax private even if he had the resources to do so. I’m surprised you think that he would. Do you think Buffett would do the same to Berkshire?

-

I think you make great points which contributes to the moat. Another feature of Fairfax is that you know your optionality on the stock doesn’t get impaired by an opportunistic take-private bid from management. Arguably, the market gives Fairfax a discount for this feature as its participants are more interested in short term gratification.

-

At the time the hedges were put on there was real concern about negative interest rates. What’s float worth if interest rates are hugely negative? I think that’s what they were hedging so they could keep growing premiums.

-

Q. So you would pay a premium for any leverage or is this leverage more valuable because of its characteristics? A. Yes, in principle. Leverage from taking out a big loan would be worth a lot less than safe uncallable leverage from a steady self-renewing source of float like Fairfax's insurance business. Given the fact that float represents $28b at Fairfax, and equity is $26b (including non-controlling interests), and Fairfax is trading at only 1.1x book, you might say that Mr Market is giving very little value to that float, but I think it deserves a much more healthy premium. A huge loan that you never have to pay back is worth something. Sounds like a moat.

-

It makes sense in context with investor behaviour and typical institutional manager constraints. The narrative will change when price changes.

-

So you would pay a premium for any leverage or is this leverage more valuable because of its characteristics?

-

The short answer is that shareholders really liked the hedges when they were on. I didn’t own Fairfax back then but I was buying US banks in early 2016. A lot of financials were in free fall because the fears of the US and Canada going into negative rates seemed like they were at their highest point. A lot of the same PMs that now complain about the hedges owned Fairfax because of the hedges. The stock acted well when the market was down and especially when other financials were down so FFH had the effect of dampening volatility and increasing risk adjusted returns. Even now, anecdotally FFH tends underperform on big up days for the market and outperform on big down days and I think it’s partially because the historical hedges (including GFC-related hedges which worked out) still influence investor behaviour. The market wasn’t efficient back then and it isn’t now. Valuation and expected returns are just not that important to most active managers who are trying to beat the market in the short term. If they were trying to generate high risk adjusted absolute returns over long periods of time maybe it would be a different story.

-

I guess I misunderstood I thought it was the discussion of the moat that got us there. Using your mental model, I wouldn’t pay NAV+ for a levered bond fund. Would you? Sure insurance is a commodity business but Fairfax gets to choose how much business it writes when prices are low. Effectively that’s part of the culture/cap allocation moat, isn’t it? I’m curious for the people looking at the track record in CR, how can you tell how well the comps have been reserving vs Fairfax over time? If Fairfax, over reserves after every acquisition would that skew combined ratios higher? Do you track operating expense ratios vs comps to see if there is a delta in structural cost advantages?

-

Is it fair to say that unlike Buffett, you both don’t think float generating businesses are worth more than book value?

-

I’m just referring to liquidity. Cash is better than no cash even if there is a liability of the same amount. I appreciate your perspective.

-

I think it was confirmed to be a PFIC.

-

They would have more liquidity by adding the to the TRS vs share buybacks all else being equal.

-

If they bought the shares back, we would find out within the first 10 days of December.

-

If Fairfax added or reduced its TRS position this month what would you think? Keep in mind we wouldn’t find out until February and the news would accompany earnings so if it does happen it will be difficult to tell how the market takes it. There was a cross of ~216k shares last Tuesday at the close which is why I’m asking. That cross could be related to something entirely different but changes to the TRS are a possibility.

-

Glider hopefully is right that the tax losses on FDGE can be used by Fairfax and there could also the potential for lottery ticket returns based on making a further investment which probably be more difficult to do as a public stock. That’s a trade I might make too so I’m not put off by it. I think Fairfax is an expected value investor and I don’t think that will change as long as Prem is in charge. Most investors want them to use the same heuristics they do to make investments and so most investors will be constantly frustrated. Not averaging down is one of those heuristics. Investors prefer FFH get a steady 12% on their equity portfolio vs a lumpy 15% even though FFH itself is a lumpy 15% investment. Arguably the floor returns are higher for FFH now than in the past decade because of the change in the interest rate environment and the high float to book value ratio.

-

Quants love consistent earnings and analysts predicting growing earnings. Fairfax should have more consistent earnings the next few years given the structure of the bond portfolio.

-

On the face of it, it’s bigger, more liquid and has a larger dividend.