SafetyinNumbers

-

Posts

2,820 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Are you asking about seasonality in reserve releases? I haven’t investigated but my guess is 4 years after a particularly bad Cat quarter so maybe more likely in Q3s. If you study it please share. I’m also curious about regression analysis on cat losses between FFH and peers. The last three quarters we have seen a tick up which makes sense given when the hard market started. It’s hard to know how big the releases will be but once again it’s not like we are paying for it in the valuation.

-

Gift link if anyone wants it: https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/O2CNLFZ2JBGHFJOHYRCWASGEKE/ Obviously a super cat event would slow down BV growth in the year that it happens but unlike previous years it’s unlikely to result in a loss for the full year given the strong core earnings. Ultimately, it would harden the market and those earnings would be recovered over the next few years. The disclosure on historical cat losses in the ESG report gives a visual representation of how low losses have become measured by cat points as premiums have grown a lot faster than exposure. The more interesting thing to me is what can go right. No analysts are predicting reserve releases to grow very quickly over the next few years but that seems likely to me which means underwriting profit could beat expectations by a wide margin.

-

I know most here are long term so my flow explanations for short term moves may be annoying but I think FFH was weak today along with other P&C names because institutions were rotating into more economically sensitive names like banks, Brookfield etc… Just another opportunity to add for those that are looking to establish a position. It’s also easier to sell FFH this time of year as the stock tends to underperform XFN from June 30-Oct 31 b/c of hurricane season. I think this year can be an exception b/c of the exceptional Q2 that seems to be coming and a potential add to the RBC Focus List and the elusive S&PTSX 60. FFH has only outperformed XFN twice in the past 10 years during this period.

-

Just filling in the blanks from the article that the buyer also bought the underlying real estate from Eurobank which was presumably the partner in a sale leaseback. I’m making some assumptions for sure. Not that it matters much.

-

Yes but also potentially dividends. They clearly did a sale leaseback on the real estate as well.

-

Just because they have likely taken out more dividends than their original cost basis and potentially earnings since acquisition but you are correct if they have reinvested a lot of capital than it would be higher.

-

It looks like based on the purchase price, it was probably marked at zero.

-

@Daphne is spot on. This is on the Fairfax India website.

-

I think when Buffett talks about book value not being relevant he is saying that a P/B multiple of 1 is not a good representation of intrinsic value. If the value of the assets are higher than book value and they earn a good return than it should show up through a higher ROE like we are seeing. Historically, there is an exponential relationship between ROE and P/B which makes sense given the compounding effects of a high ROE.

-

Pretty amazing they can expect a 16% ROE and think that 8x earnings is the right multiple. Of course, that has been Fairfax’s story too.

-

Different story as it’s not liquid enough or the float big enough for the Composite yet so no listed options. The hope is some investors use it, instead of ETFs and given the increased liquidity, trade it more often too. If playing musical chairs with market exposure, it’s somewhat safer to do at a big discount to liquidation value.

-

Stock split will really help with multiple expansion as dealers require inventory and there are quite a few ETFs and individual investors that like covered call writing.

-

Ultimately it comes down to pricing and experience over time. If there were negative reserve developments we would have seen a true up already. That suggests we should see reasonably high reserve releases. I think it’s impossible to predict with any precision and I don’t see a reason to as an investor. It’s enough that it’s a tailwind. Expectations are for a ~95 combined so each point they come in below that boosts ROE by ~1%.

-

I’m not sure how helpful average reserve releases are when analyzing Fairfax. I don’t think excess reserves have anything to do with any specific event but just a very disciplined reserving culture and the long duration of their claims (average 4 years). In hard markets, reserves are higher because pricing is higher and expected profits are the consistent. That is writing to a 95 combined. Four years later assuming no unfavourable developments, the reserves start getting released. I know it’s more complicated than I am making it seem but it’s the framework that helps me appreciate the cyclicality of reserve releases. Raymond James in the chart below shows how reserve releases went up a dozen years ago and stayed elevated for the next 7 years. We could be at the beginning of that sort of cycle which means underwriting profits are a tailwind for years to come.

-

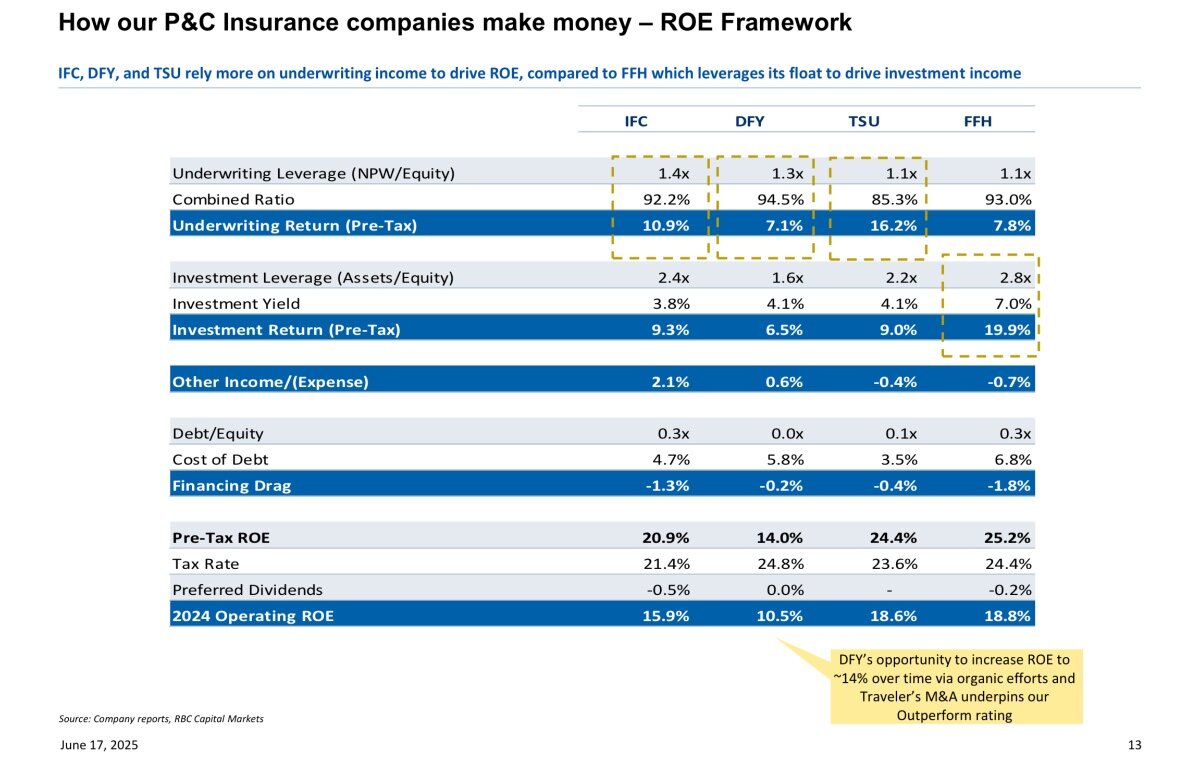

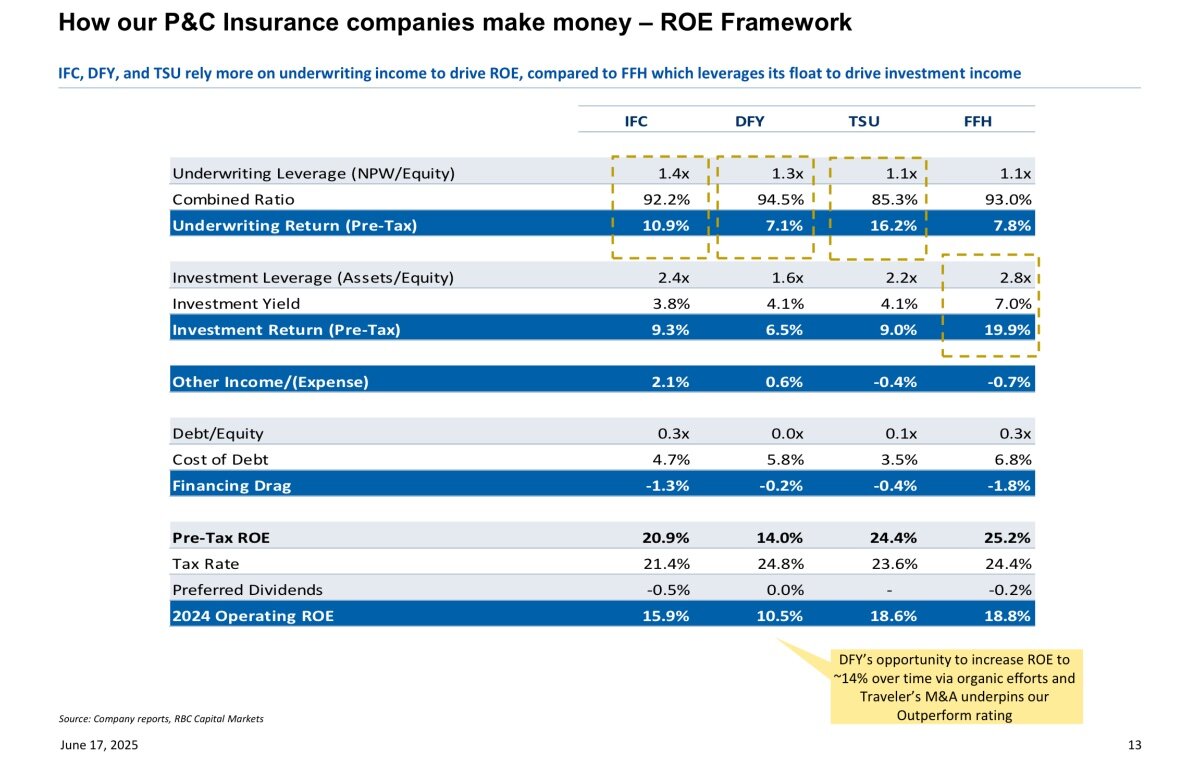

I like this illustration of the composition of ROE. Underwriting has tailwinds because of reserve release cycle even if the insurance market softens. Cost of debt is fixed. The wild card is investment returns but investment yield has a strong base given fixed income is contributing 5.1% and the average maturity suggests that persists. One can speculate on what equity returns will be but as Viking has highlighted there are a lot of unbooked gains that will boost ROE for years to come and some of the holdings are carried at high earnings yields like Eurobank. I find it really hard to see ROE averaging under 15% for the next five years. In fact, I think the odds of 20% are better than 15%. The beauty is I’m paying for 10% at best.

-

I wonder if it was just easier and maybe cheaper to issue exchangeables instead of equity. There didn’t seem to be a coupon on the bond and they exercised them just before the €1.50 dividend went ex. Increasing the share count will also help increase the float which helps ETF demand upon listing on the LSE.

-

Is some yield curve control already happening? The administration is trying not to issue long bonds to reduce supply and not lock in “high” rates. Presumably, the next Fed Chair will slash the short end of the curve next year if Powell doesn’t get started soon. I’m wondering what happens to corporate spreads in that environment. They in theory should be wider to reflect inflation risk.

-

The increase in the Eurobank share price won’t help the earnings to be clear but FV over CV should increase a lot which in theory should help with multiple expansion.

-

I think the biggest impact from the high share price is no listed options which keeps it out of all of the covered call ETFs and dealers don’t have to hold inventory to hedge their option positions.

-

Andrew Bary of Barron’s was on Fox Business and pitched Fairfax. Can jump to the 2:15 mark to get to Andrew. https://www.foxbusiness.com/video/6374971426112

-

Thanks for sharing! This looks like another attempt by a Fairfax company to take advantage of market structure. Metlen will attract a lot more passive buying listed in London. A big part of Strathcona’s bid for MEG is also to take advantage of market structure as none of SCR’s float is in any benchmarks.

-

Kudos to Bart (the RBC analyst) for creating it. It shows how much leverage there is to investment returns in a very concise way. The next step is to breakdown where the returns on investments come from (fixed income vs other), see if those expectations are also reasonable and determine a range of potential returns.

-

BRK is a tough comparison because of how successful they have been on the equity side of the book and how few insurance acquisitions they have done compared to Fairfax. Vs the other Canadian P&C’s Fairfax is at the low end of the range.

-

Attaching the article I wrote last year explaining why I thought FFH’s next 30 years will look better than BRK’s last 30 since this topic is getting some discussion. Probably more relevant than ever as some holders are thinking of reducing their position in BRK now that Warren is taking a step back. BRK won mainly because Warren was really good at picking stocks and less so because of the float leverage. In this inefficient market, if FFH can pick stocks well and enjoy the float leverage, the returns can exceed expectations. Based on the current multiple expectations are low. FFH G&M 5.1.24.pdf

-

Mr. Kant spoke to the group that went on the Fairfax India trip and I found him to be very impressive. Hopefully his influence and contacts will help move things like the Anchorage IPO along which will boost FFH and FIH book values meaningfully.