SafetyinNumbers

-

Posts

2,812 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Are you familiar with the financials? They contributed $38.8m in profit in Q3 but maybe that’s not repeatable?

-

The US$108m included the regular dividends and the special distribution. The regular dividends would be income. The special distribution will reduce the cost basis from US$129m to ~US$35m.

-

The exchange rate is ~1.40 so ~C$130m distribution is closer to ~US$90m not US$70m. I don’t agree with you that they will elect as a dividend and choose to pay tax now as opposed to defer it and I’m not sure if we’ll find out. The ongoing dividend is C$1.20/yr which is closer to US$11m per year not US$75m. It’s supposed to go up with production but that was before they sold the Montney. I suspect they still might do it though.

-

No question. With the regular dividend they will have taken out ~US$108m by the end the year. Also SCR should be going into the S&P/TSX in December which might help the mark.

-

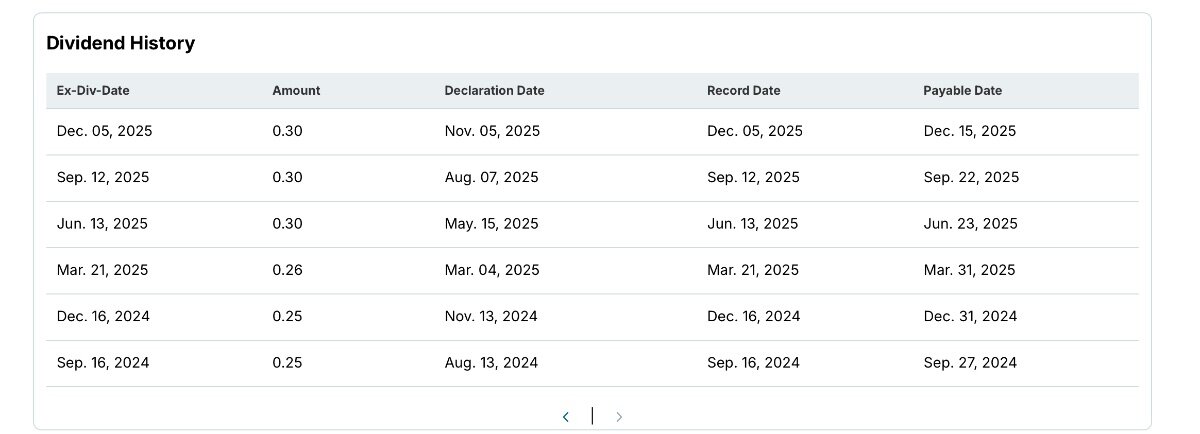

Strathcona is part of limited partnerships. Based on the disclosure, Fairfax owns ~13.1m shares of SCR. The C$10 distribution can be elected as a return of capital so unlikely to contribute to income in Q4 for FFH.

-

Currently this investment is all Greenfire Resources (GFR). It’s doing a rights issue in December so this investment is going up in Q4. Post rights issue I expect this investment to do well assuming they execute well on the capital program and oil prices can stay around here or better. I assume they will also look to do acquisitions which may result in more capital being called from Fairfax.

-

That all makes sense but Berkshire and Markel aren’t making venture investments like this so to ignore it in the returns calculations seems unfair.

-

Would Digit be included in equity investments? I don’t think it’s considered core and would certainly pull up returns of the equity portfolio. Ki is core but was still a venture style investment. It’s probably also a 20x+ type of investment. Both are on the insurance side but created a lot of value.

-

It’s more about returns than growth.

-

Also, FFH didn’t put up any new capital. They just rolled their shares in.

-

They seem to act more like Berkshire and say this is our price, take it or leave it and no hard feelings if they leave it. In insider bid scenarios a bump is sometimes necessary to get minority holders over the line.

-

Also long duration assets with inflation protection for those concerned about the short duration of the bond portfolio, this is a significant offset along with the other equities in the portfolio.

-

I don’t think it matters much who the marginal buyer is. After the rights issue, they won’t need any equity. If the stock is too cheap they will probably try to buy other assets with cash or stock at a fair NAV ratio. GFR is the only thing in WEF III, there will be more deals.

-

I would like to read the transcript. My interpretation of the situation is that they signed a lock up and were bound to it. Having been in that situation I know first hand it can be incredibly frustrating.

-

Fair and Friendly means it’s not hostile and minority shareholders get to vote. A majority of the minority is required. It also means when they make an offer they don’t drop the price later. It doesn’t mean the price is fair value. They want to buy at a discount. That’s what it’s all about.

-

Fairfax didn’t increase their stake in Atlas. Their partners wanted to take it private.

-

How do you determine FFH is fairly priced?

-

The capital treatment for the insurance subsidiaries is the reason. You should ask the question on the conference call Friday.

-

NAV discount started in 2013 and efforts to close it started in 2020. Of course, the bigger the discount, the lower the historical return. It doesn’t mean the intrinsic value didn’t increase. Still a ~40%+ discount to liquidation value for very marketable assets including 1.48m shares of VOO!

-

Not going to happen with Fairfax India. Private Indian companies won’t get the same capital treatment as a TSX listed company.

-

I really like this deal. Diversified, asset backed, growing capital light management business and a good place to pick up returns above treasuries if the yield curve goes lower. The business benefits from lower interest rates so should help assuage concerns of those who think duration is too low and the whole yield curve is going lower.

-

This is pretty cool

-

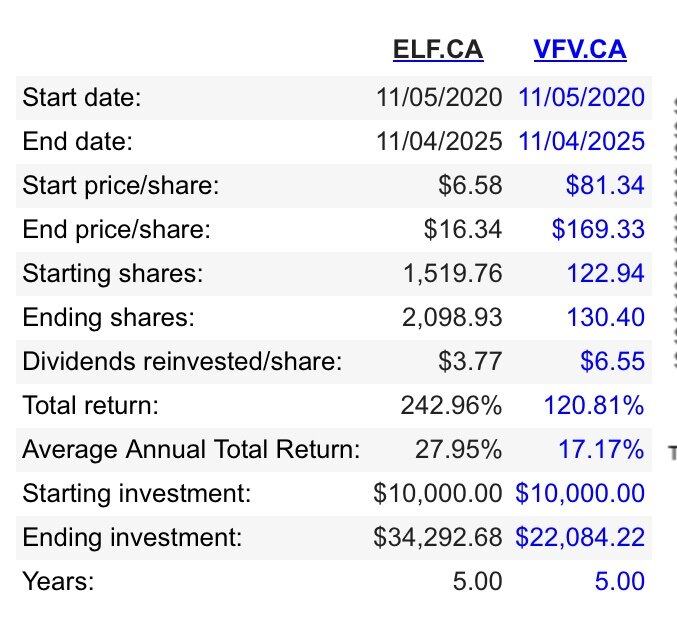

I still think it makes sense to buy ELF.TO instead of VOO. Give up some liquidity for margin of safety.

-

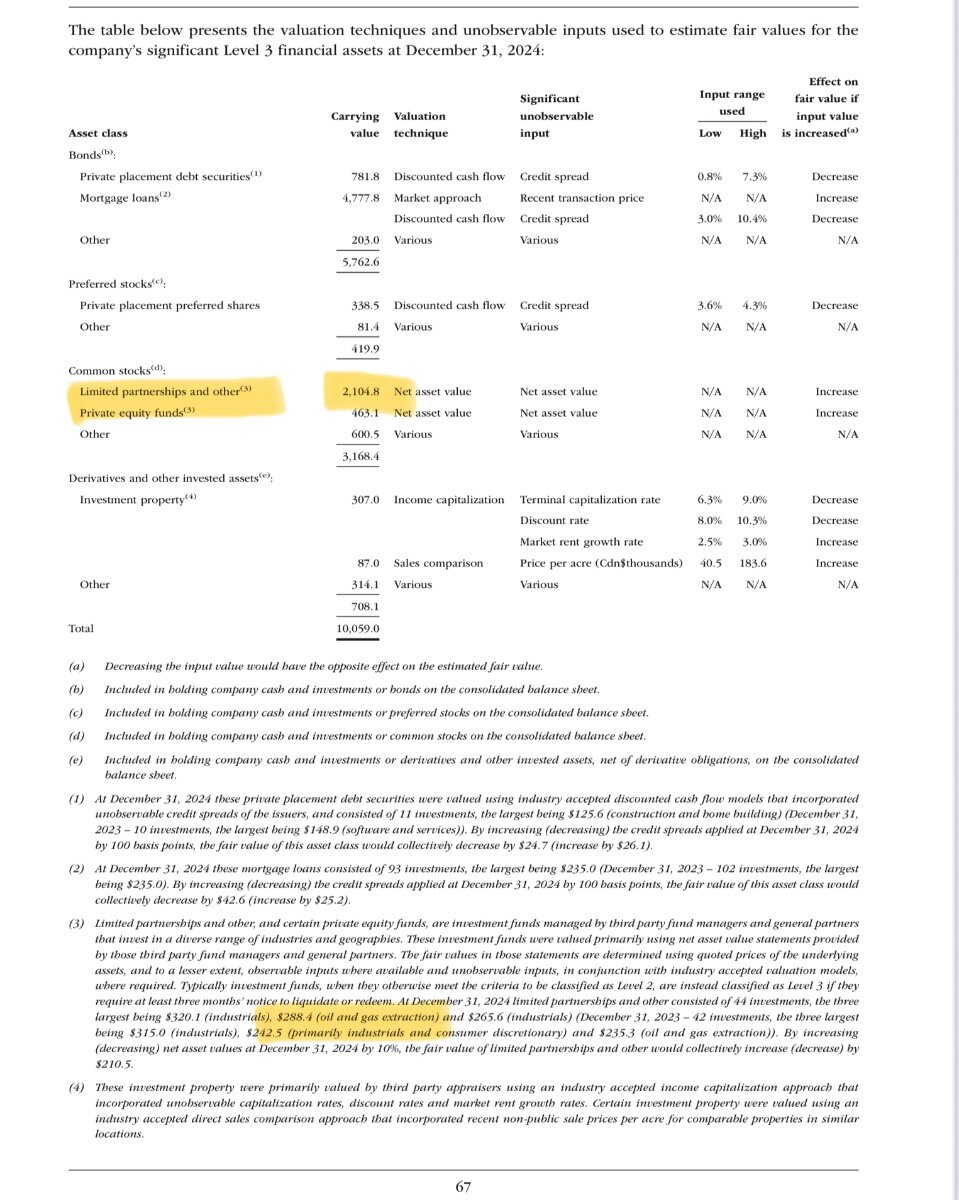

Yes, AI got it wrong. This disclosure is in the 2024 AR:

-

I think he made the purchase on margin too which likely influenced the decision.