SafetyinNumbers

-

Posts

2,814 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

If they wanted to juice fees they could just mark stuff at fair value or higher like most PE vehicles.

-

It’s a market structure issue. If not in the benchmark or not screening well, there are too many other options for active investors who have very high return expectations. Most of the recent interest in the stock is from event driven investors waiting for the airport IPO. It will be interesting to see if the discount to BV grows when it happens.

-

Not sure aggressive buybacks actually close discounts. Elf.to bought back half the float, paid special dividends, raised its regular dividend 30x and split the stock 100 for 1 and is still a 30% discount to book. It’s the lack of passive demand that keeps the shares at a discount and that’s not changing.

-

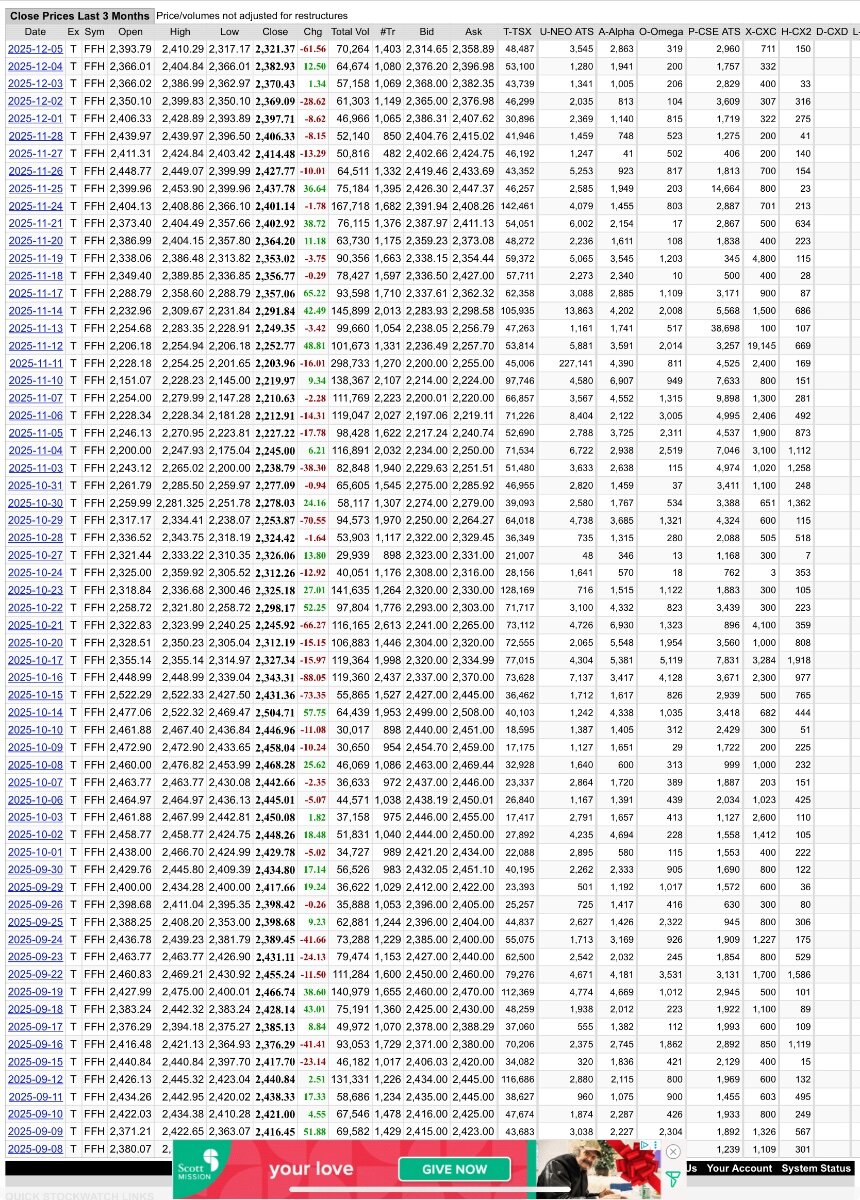

Volume has been big the last 3 days

-

They are also trying to run a business which means growing and strengthening their network. That means being able to do deals when they are available and keeping their investment professionals engaged. There is a balance. When the stock got hit in April, they did buy back stock.

-

I was referring to liquidity at the holdco level to make more investments etc… That being said, most institutions complain that the shares aren’t liquid enough for them to establish a position and believe buybacks makes that worse.

-

It was contractual they take the first two performance fees in stock. If I recall correctly, the first performance fee it was trading above book value, the second one was a big discount but it was tiny (~500k shares) and they bought almost 6x the shares issued for the performance fee back cheaper earlier in the year. You got the last round correct.

-

Thanks. NBF is 80. Scotia is 85 and they have the buyback. NBF put the order in the MOC facility it looks like. Any other markers on it?

-

Can you see the broker number?

-

I think intrinsic value is between $35-45. I think returns are pretty reasonable from a starting point of $9.50, after the IPO fees. They could be more aggressive with their marks and holders could have paid more fees up to the parent. The move from a premium to book to a discount to book has a lot to do with change in market structure. Management has taken advantage of it by buying back stock and I’m sure they will again when they have more liquidity. It’s not clear IDBI will take a big cash investment from FIH. They may contribute CSB at a premium and be the GP earning fees from LPs that are brought into the deal.

-

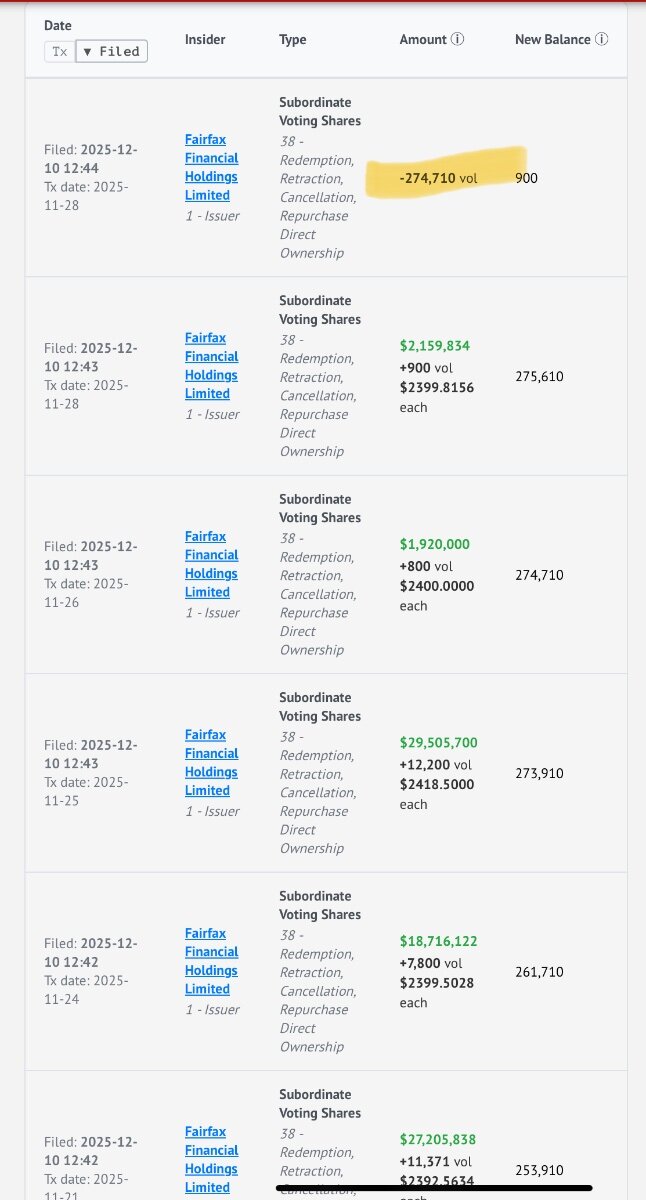

Fairfax canceled 274k shares last month.

-

This is an interesting discussion that I think applies tangentially to Fairfax too. To me it looks like Fairfax ramped technology spend a few years ago as premium growth accelerated. In theory, we should have seen more operating leverage but the expense ratio initially went down and then went back up again on more investment. This investment should have benefits so presumably at some point, the expense ratio will be lower and an improvement in the combined ratio could be more sustainable.

-

Farmers Edge launching a new division, Covian, to go after agtech. https://www.businesswire.com/news/home/20251210543212/en/Farmers-Edge-Announces-Corvian-A-New-Enterprise-Technology-Division-Built-to-Accelerate-Digital-Transformation-Across-Agriculture-and-Sustainable-Supply-Chains?utm_campaign=shareaholic&utm_medium=copy_link&utm_source=bookmark

-

Should use stockwatch.com to see all of the ATS volume as well. TSX is only part of the picture.

-

I don’t understand the assumptions but it’s traded 220k shares so far this week. They will get done but the price depends on where extant shareholders want to sell. Ultimately, they try to hold back enough demand for the last day/hour to ensure the 19th’s close is above their average cost.

-

Brokers are saying 550-800k of demand. The brokers are motivated to get the closing price on Dec 19 above the VWAP for the two-week period so they hold back some buying until the last day.

-

Awesome, thanks!

-

Check out my most recent article for the Globe and Mail about Fairfax. This is a gift article. https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/AKS47ZLUWZFSXEKQVGUNGOWYCU/

-

Is Fairfax any different?

-

My guess is the banks are fully hedged on the TRS. The buying will start on Monday as the APs begin to accumulate to prepare to cross the shares into the ETFs. The wildcards are how much closet indexers buy and who is left to sell. Fairfax has bought 8m shares plus in the last 8 years if we include the TRS so the most valuation sensitive holders are already out. How do you guys make sell decisions? Is it based on valuation, weight in your portfolio or something else?

-

It’s a bit more liquid than it looks when all of the ATS are included. Maybe 0.35%. This is a real test for how strong the hands are in the retail shareholder base. As has been discussed often, investors like Parsad think the stock is fairly valued or maybe even expensive so they might sell into a big move wanting to avoid the next drawdown.

-

S&P/TSX 60 demand is estimated at 3% of the float and S&P 500 is closer to 10% plus CVNA has a high short interest so a bigger move also makes sense from that perspective. Any guesses on where it closes on Dec 19?

-

Each addition is idiosyncratic based on prepositioning. Expectations weren’t high this quarter for addition and many institutions were rotating out of FFH because of insurance and non-CAD exposure.

-

The analysts are a reflection of their clients.

-

S&P/TSX 60 is committee based. Any pre buying was from index arbs and they have been “burned” 5 quarters in a row so chances are this was the least gamed quarter in the past 6.