SafetyinNumbers

-

Posts

1,570 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

I don’t think a probabilistic investor would come to that conclusion. The complexity is designed to reduce risk and increase returns. Regardless, it’s a poor argument to make now based on the outlook in which surplus capital is about to skyrocket. The thing that makes Bloomstran pick BRK over FFH is its surplus capital. FFH is about to be swimming in it. In theory the increased durability should increase social value and returns.

-

I’m glad the article is being associated with Berkshire. Quite frankly, it’s the biggest source of like-minded long term investors for FFH after the Canadian institutions. I rather get those individual shareholders first since the institutions don’t really care about the price they pay just the performance they get. I wanted to highlight how much better the set up is for FFH vs BRK both based on the size of the insurance business on a relative basis and the starting valuation. Of course, the forward macro conditions, execution and asset allocation decisions will determine what the future returns look like but I can see how quality investors might flock to FFH if they execute on the strategy of adding quality stocks on a big market dislocation. i think it’s important to note that BRK has been way better on the equity investments which is why it has so much more surplus capital than FFH. It’s the reason Bloomstran prefers BRK. FFH is now in a position to stack surplus capital which will increase durability and the potential to add high return equities.

-

Thanks! Many thanks to @NormR for helping so much with the editing and connecting me with his editor. I’m so excited to see it in the paper when it gets delivered tomorrow. Long time subscriber, first time contributor

-

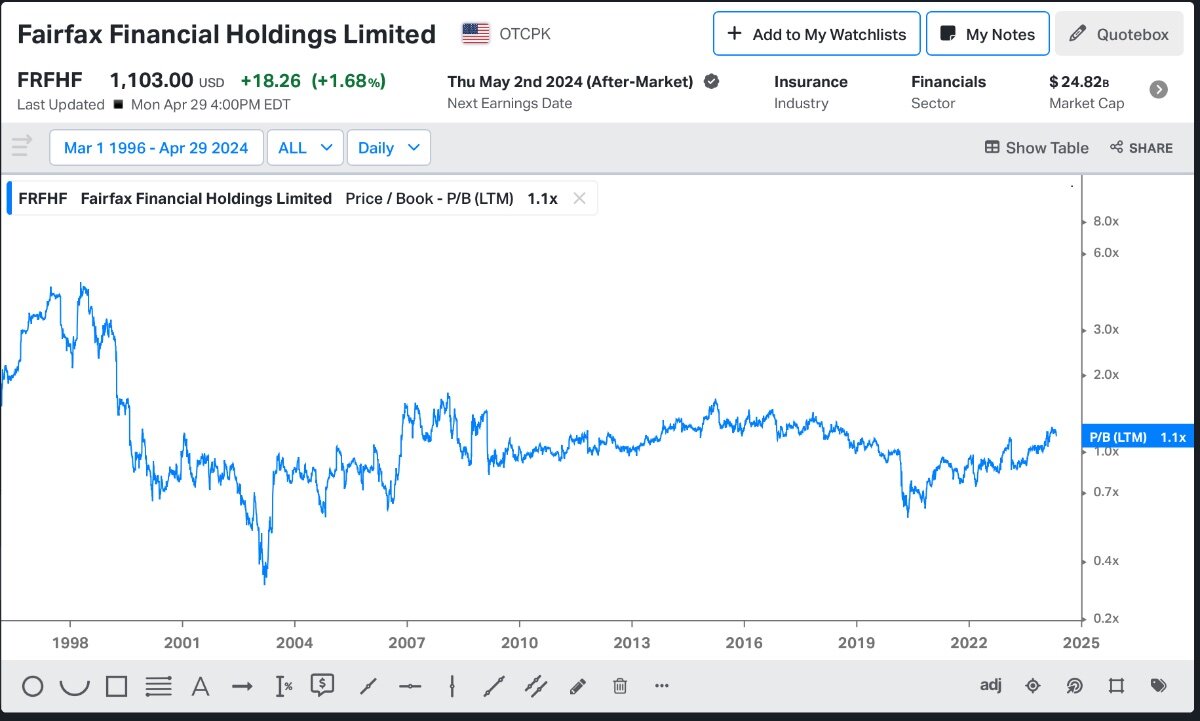

It was a dumb joke that we get more snow in Toronto than Omaha (about 2x actually!). In reality, when BRK first hit the same market cap as FFH is now in 1995, it wasn’t set up as well as FFH is. BRK was trading at ~2.5x BV and had insurance premiums of only $3b. With that set up, I think FFH has a good chance of outperforming what BRK already accomplished in the last 29 years.

-

It’s one of things that gets me very excited about owning shares for a long time and being very resistant to selling too soon. In the late 1990’s we used expensive equity to buy float cheap but the combined ratios were high. The equity got expensive because FFH booked 4 years in a row of 20%+ ROE. Back then, the starting point was 1.8x BV and the stock went to 5x BV. It was really smart to sell back then but this time the earnings quality is so much higher. Instead of buying underperforming insurance companies if our stock gets expensive we may buy large quality companies at a fair price. This will dramatically increase surplus capital and increase returns. The snowball could get huge quickly which should probably be expected to happen easier in Canada vs Omaha from the same starting point.

-

Fairfax also used expensive stock in the late 1990s to do a series of insurance acquisitions in part to pick up cheap float. A smart move by both BRK and FFH, IMO.

-

I think they are telling us their sweet spot is quality at a fair price and they are waiting for fat pitch. That should send the multiple higher but the market might wait until they actually pull the trigger. Does anyone have an estimate of how much they could deploy into equities from fixed income if an opportunity presented itself?

-

My guess is that if estimates go up post quarter that eventually the stock will resume moving higher but thankfully I don’t have to bet on it.

-

2.5x+ BV starting to seem expensive or is something else going on?

-

Thanks!

-

Thanks for sharing. Do they have the FIH.U transcript as well?

-

Thanks for sharing. This moment at the AGM forced me to add even though it’s a full position. If I can paraphrase Prem here: We’re sitting with the bat on our shoulders waiting for fat pitches and virtually every one we have swung on lately has been knocked out of the park. We should have a rating system based on dollars. If a trade makes $1b it’s a home run like the TRS, duration decisions which allowed for the premium growth and saved billions, the SIB etc.. Right now, I think they are stating plainly that quality compounders on sale is their sweet spot. The beauty of the giant float is that just stacking cash gets them over a 15% ROE. I can see how buying a crash could increase returns and increase the multiple i.e. decrease negative Social Value. Lots of investors won’t buy Fairfax because they only buy quality and Fairfax does not own quality i.e. Fairfax owns stocks they would never buy. Part of Markel’s premium is because they are associated with quality as it’s certainly not because of recent returns. I had a PM friend say FFH’s reputation is as a junk collector but that could change quickly if price changes quickly. They also seem to have a lot of excess capital. Float is $33b but they have $45b of fixed income. If there is a market dislocation like the pandemic etc… Fairfax might be in the position to deploy 20% or more of its market cap in high quality stocks or the index at a fair price. VOO on the 13F maybe isn’t much of a head scratcher anymore but a capital allocation decision consistent with a new mentality. Of course, we’ll have to see what they actually do but each fat pitch they swing at could super charge ROE and BV if they get a hit and it seems to me like an environment rich in potential fat pitches including a market dislocation.

-

I use 10% as my hurdle rate since that’s an estimate of long term equity returns. I’m not sure what they use.

-

I think Fairfax is an absolute return investor and not a relative return investor. They aren’t trying to beat the S&P/500.

-

My guess is it should increase the deferred tax liability all else being equal by the increase in the inclusion rate. Anyone have a better idea? If my estimate is right it would increase the deferred tax liability by ~$412m or ~$18/share.

-

What did you learn this week at Fairfax Week?

SafetyinNumbers replied to SafetyinNumbers's topic in Fairfax Financial

I asked the question about using a structure where FIH was the GP. I thought the answer suggested it was the likely possibility but others in the room didn’t have the same takeaway. -

What did you learn this week at Fairfax Week?

SafetyinNumbers replied to SafetyinNumbers's topic in Fairfax Financial

@hardcorevalue presented BAT so he can probably help. -

What did you learn this week at Fairfax Week?

SafetyinNumbers replied to SafetyinNumbers's topic in Fairfax Financial

There was no explicit mention of IDBI but it was alluded to that the decision would be post India election (early June). Generally I got the sense that activity will pick up across the board in India once the election is over. Also, I was the “someone else” who had the opportunity to sit on the panel with Viking at the dinner. I hope I made sense even if I wasn’t memorable! -

Thanks! I’m still confused about what @John Hjorthis upset about.

-

You think they are lying in these two slides?

-

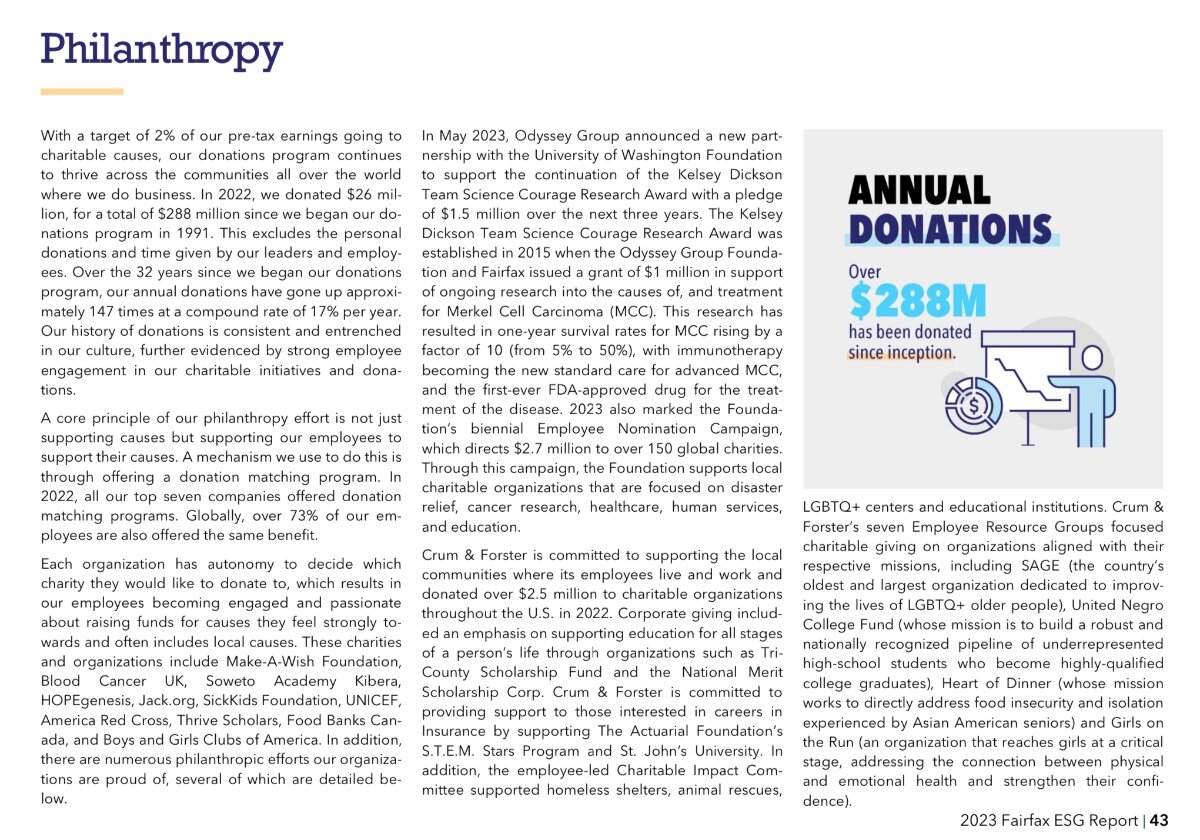

I think this is what he’s referring to. https://www.fairfax.ca/wp-content/uploads/2023-Fairfax-Financial-Holdings-Limited-ESG-Performance-Report.pdf

-

Those were the old estimates unless they are unchanged.

-

That doesn’t make sense. They shares held for employees haven’t vested yet. He probably doesn’t understand the accounting. Also it’s weird because the computer sets the target price so he’s working backwards.

-

I’m proud of my CFA but it doesn’t make someone care about the quality of their work. I care about what I share on Social Media and I’m not getting paid by anyone.

-

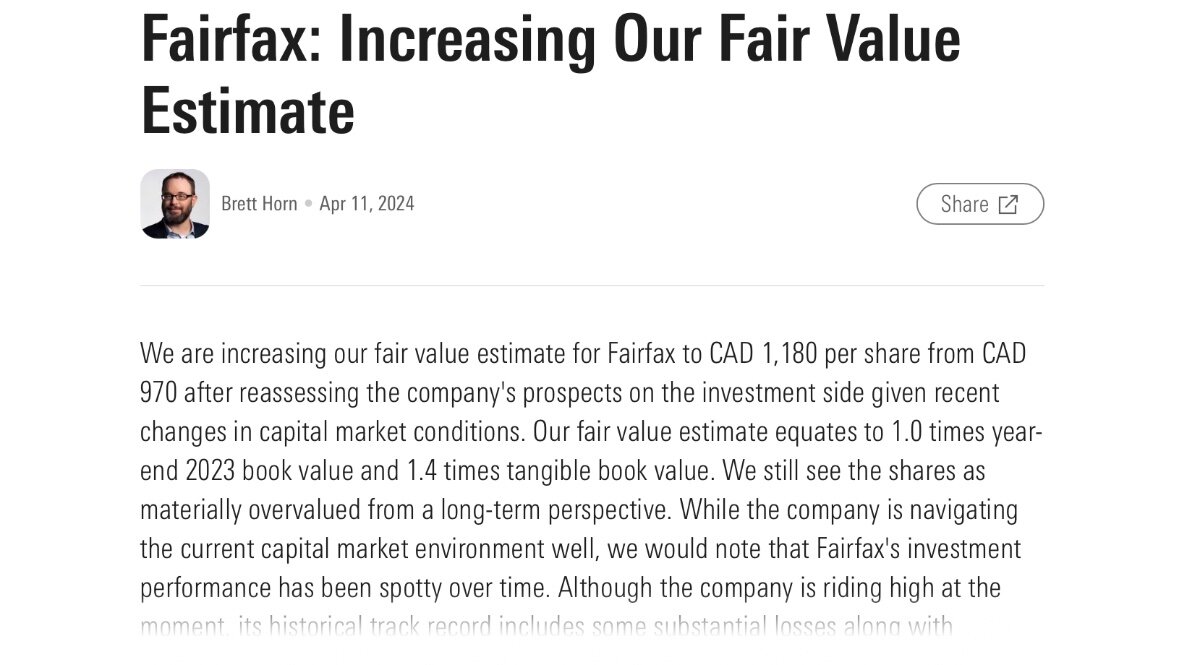

He says his target is 1x 2023 YE BV but C$1180 is US$862 and 2023 YE BV was ~US$940. How does this stuff get published?