John Hjorth

-

Posts

4,883 -

Joined

-

Last visited

-

Days Won

14

Content Type

Profiles

Forums

Events

Posts posted by John Hjorth

-

-

It is here, today.

Bloomberg [2018.02.12]: Trump Sends His Infrastructure Plan to Skeptical Congress.

The basic source - the plan itself: The White House: Legislative Outline for Rebuilding Infrastructure in America.

- - - o 0 o - - -

Happy reading!

-

Nell-e,

Some board members actually do not sell, or sell seldom. [i.e. longinvestor and Valuehalla are in that camp, and you can include me there.]

Some board members selling or reducing their positions prefer to post about it in the particular topic in the Investment Idea forum.

Some board members prefer to post about their rebalancings gathered as one post in the buying topic.

Some board members don't post in detail about their doings. [We don't have to.]

- - - o 0 o - - -

I appreciate you asking. It's a big board. It takes time to find out how things actually work around here.

-

Not exactly Max,

Say, some vehicle [, or I don't know what] takes control of Berkshire in future [Let alone, that scenario to commence, in it self need some analysis with regard to probability of feasibility], that acquring entity selling ie. BNSF will just have the sales proceeds of BNSF to add in the statements of regulatory capital for NICO, reduced by historical cost, in that case, increasing dividend room for Berkshire [subject to dividend tax].

-

... Berkshire has a unique ability among insurance companies to invest in common stocks and operating businesses, because so many of Berkshire's wholly owned businesses are actually owned inside of the insurance subsidiaries - and count towards regulatory capital because of that. So Berkshire's insurance companies are enormously overcapitalized and thus afforded permission to invest in "riskier" securities vs the bond portfolios that most insurers stick to for the lion's share of their portfolios.

So, long story short, Berkshire doesn't have to dividend cash out of the insurers to buy a large company or make a large investment. Many subs are owned by the insurers. ...

WneverLOSE,

To shed some light about what globalfinancepartners is talking about, please visit National Indemnity Company Financial Information webpage.

The overcapitalization of NICO is built up on the long haul by Berkshire since the acquisition of NICO many years ago, and a major part of the surplus capital compared to required regulatory capital is allocated to other businesses and listed investments.

-

Ouch. That's a pretty direct response for a new board member.

I have to agree with StubbleJumper. Not your usual posting style, Graham. I have always appreciated your posts here on CoBF, except this one. I just hope that you remember this topic from about two years ago. The point here being, that I learned something from the discussion in that particular topic about Berkshire leverage and Berkshire cost of capital.

-

... I always look at BRK compared to what else is offered by Mr. Market right now. ... I do think that buying RE at book is better than buying BRK at 1.5-1.6x book. ...

... I think geht RE might compound just as well as BRK.

Berkshire isen't trading right now at 0.3 x BV - 0.4 x BV above soft buyback treshold, but more around .15 x BV above soft buyback treshold.

-

Let's continue this Berkshire discussion here, so that we don't annoy other fellow board members with lengthy Berkshire talk in this topic.

-

From the "what are you buying today" topic:

I also bought some BRK.B recently although my logic might make some cringe. I'm a big believer in the "cover your ass" incentive. Barclays and UBS put price targets on the B shares for ~$240. I'm betting that money managers will herd into Berkshire by year end in a volatile market because it's easy to justify to unsophisticated retail customers.

Any thoughts on my reasoning?

A belated welcome to you here on CoBF, Nell-e! [: - ) ]

Personally, I'm more interested in tinkering with Berkshire earnings numbers like attached! BV and analyst price targets less.

-

I have a raw estimate of Berkshire equity YE2017 of USD 357 B ex. minority interests. With end 2017Q3 A share equivalents at 1,644,656, that gives me a BV per B share of 145, exactly as longinvestor has posted in a topic in the Berkshire forum a few days ago as a reply to wescobrk [longinvestor posted 143]. So to me, buying the B at 196 is equal to buying it at 1.35 x BV. We could go to that particular topic for further discussion, if needed.

-

For me, the best part of what's going on right now, is that I've finally managed to get mentally free and detached to these swings. They don't bother me one whit any longer. A condition for taking advantage of them.

John, take a deep breath, and make sure to ask yourself if this is because you yourself are ready to take advantage of them, or is it because the market has shown little to no volatility (beyond a week or two) over the last 6 years (since the 2011 drop)? I'm only asking you to take a moment because I respect your insight, and the help you've given me on many Danish names that popped up for me in the past, and I want to know your thoughts tomorrow and beyond as we find a floor or continue to build a top. :)

Sharad,

As you already know, I always appreciate your posts. [ : - ) ]

Everything is relative, depending on what you hold, and what you want to buy. [Please see attached file # 1].

Last night I studied with great interest a Danish company, that has just reported nothing less than minus 9,044.1 percent ROIC. [Please see attached file #2].

-

Somehow I personally consider this initiative an employer-owned PBM, that will be running on some kind of non-profit basis.

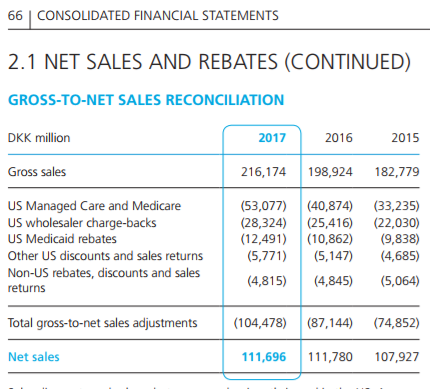

Attached is a part of note 1 from Novo Nordisk Annual report 2017 released yesterday. It's ludicrous. Gross sales af DKK 216 B, net sales of DKK 112 B, US rebates etc. alone of DKK 100 B.

Novo Nordisk diabetes US market share 39 percent. Very rough calculation of total potential savings [with a lot of short cuts with regard to not taking NVO product mix etc. into consideration], here assuming without diabetes pharmas earnings affected: Savings potential for diabetes alone ~ DKK 100B / 39 percent minus J/V internal operation costs ~ DKK 256 B minus J/V internal operation costs ~ USD 43 B minus J/V internal operation costs.

What US politics haven't been able to fix so far, will eventually be fixed by Corporate America.

-

-

I wonder if Chris will be updating his analysis for 2017 shortly, particularly in-light of all that has occurred at Berkshire. It still remains one of the best piece of analysis that I have read...way more detailed then JPM's coverage piece on the company.

Sincerely,

ValueMaven

I have now started looking daily on the Semper Augustus website for new interesting stuff from Mr. Bloomstran to read. It seems to be about this time of the year new letters are posted.

I'll post here if I see something new comes up.

-

Attached is an elaboration by screen shots of what LC said. This gives you one hit - every time. [ : - ) ]

-

Honestly, I've lately been thinking about ~33 percent probability of pulling this off to success.

- - - o 0 o - - -

What happened at the barge? Thank you in advance.

-

BRK.B, today [A lot, a lot just below 196, more just below 197, and some at 199] At around 35 percent position now.

-

-

Absolutely awesome! - World's best advertising stunt, and a success!

-

For me, the best part of what's going on right now, is that I've finally managed to get mentally free and detached to these swings. They don't bother me one whit any longer. A condition for taking advantage of them.

-

Pretty wild and violent movements around 3:10 PM NYSE time today. Berkshire hit hard, the big four US banks not quite so hard at that time. Perhaps the share buyback programs in the big four US banks here work as some kind of shock absorbers in the situation.

-

There is also the essay "Measuring returns" by Joel Stevens [fellow board member Razemice], which can be downloaded from here.

-

Berkshire Website Announcement [2018.01.30].

After reading it carefully, I speculate, that is an idea shared between [Mr. Dimon and Mr. Combs] and Mr. Bezos, without having any idea about who initiated the contact.

Somehow one get the feeling from the announcement, that Mr. Buffett must have said to Mr. Combs something like "It's "your idea" [in the meaning : "It's your idea" or "You came to me with the idea"], so you do it.".

-

... I don't know much about Kroc, other than what was included in the movie "the Founder."

I'd guess that innovative processes and a relentless drive would be the main things the two men share in common. ...

To me, a pretty accurate - and short - description from you about what these two men have in common, DooDiligence.

Thank you to villainx and Cigarbutt for bringing this up about Mr. Buffett's thoughts about compensation for the next Berkshire CEO. That has skipped my attention.

Cigarbutt, somehow, I like the concept of shooting fish in a barrel with an elephant gun!

-

... I thought Buffett already prepared folks for the bad optics by saying the next CEO would be granted some option based compensation. ...

What is your source for posting this, villainx?

What are you buying today?

in General Discussion

Posted

DooDiligence,

Somehow, I get concerned reading this, Sailor. Naturally, you can do both! Where there is will & determination, there is a way.