UK

-

Posts

3,440 -

Joined

-

Days Won

16

Content Type

Profiles

Forums

Events

Everything posted by UK

-

Do not mean to interupt the process, but I know a Canadian stock even better than Canadian banks

-

-

2025 Annual Report - Greg Abel's first annual letter

UK replied to backtothebeach's topic in Berkshire Hathaway

I do not see anything wrong with all the recent stuff too and I like what Greg said and did very much. Now if the only thing I do not like from the last ~5 years, which is not swinging enough:), will change too (not necessarely right now), I think we could declare that BRK is back:) -

Is carrying value still on the book will also be updated because of this?

-

https://www.reuters.com/sustainability/boards-policy-regulation/decision-turn-back-nuclear-was-strategic-mistake-eus-von-der-leyen-says-2026-03-10/ First step:)

-

Perhaps just some speculation. Definitely some boots should be involved...and maybe some new super weapons

-

https://archive.is/K13jT “What we want to do is to get such massive oil reserves in Iran out of the hands of terrorists,” Mr Agen, the executive director of the National Energy Dominance Council, told Fox Business. “Ultimately, we’re not going to have to worry about these issues in the Strait of Hormuz,” he claimed, referring to the passage between the Persian Gulf and the Gulf of Oman, where oil shipments have come to a near standstill following the outbreak of war. “We’re going to get all of the oil out of the hands of terrorists." Michael Rubin, a former Pentagon official and senior fellow at the American Enterprise Institute, said sending US soldiers to seize Kharg Island was a “no-brainer”.

-

Summary by Gemini: The conclusions drawn by Helima Croft in this discussion center on the shift from "geopolitical risk" to "active disruption." Based on her analysis, here are the primary conclusions regarding the conflict and the markets: 1. The End of the "Risk Premium" Era Croft concludes that the market can no longer treat the Middle East conflict as a theoretical "risk premium." With active strikes and retaliation occurring, the market has moved into a phase of real supply disruption. The primary conclusion is that volatility is here to stay as long as the conflict remains "uncontained." 2. The Strait of Hormuz is the Ultimate "Tripwire" The most critical conclusion for energy markets is that the Strait of Hormuz remains the single most important inflection point. Croft notes that while Iran may not physically "close" the strait, their ability to harass shipping and drive up insurance costs creates a "de facto" closure. If shipping through the strait is significantly curtailed for an extended period, she concludes that oil prices could surge into the $100s per barrel. 3. Limited "Shock Absorbers" in the Market A major conclusion is the fragility of the global supply cushion. Croft points out: OPEC+ Spare Capacity: Most producers are already at their limit; only Saudi Arabia has significant spare capacity to offset a major Iranian outage. U.S. Constraints: While the U.S. is a top producer, it cannot quickly ramp up enough production to stabilize a global shock caused by a regional war. 4. Shift in U.S. Strategy Croft concludes that the U.S. administration is in a "geopolitical bind." The Dilemma: They must balance the desire to punish Iran with the political necessity of keeping domestic gas prices low (especially ahead of elections). Result: This leads to "reactive" rather than "proactive" policy, which may increase market uncertainty as the U.S. oscillates between diplomacy and military strikes. 5. Systematic vs. Geopolitical Shock Ultimately, Croft suggests that for the global economy, this is currently a "geopolitical shock" rather than a "systemic crisis"—but that distinction depends entirely on duration. If the conflict lasts weeks or months rather than days, it will transition into a systemic crisis that could reignite global inflation and threaten the economic recovery.

-

https://archive.is/dxMXD For more than a decade, Beijing has worked quietly and methodically to turn Iran into the keystone of its Middle East strategy. That strategy has now collapsed.

-

Sorry if this already was posted

-

-

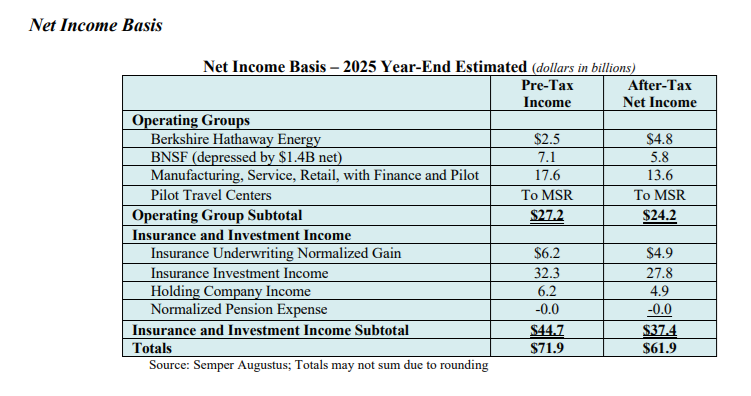

I think Semper Augustus does quite decent job at estimating the earning power (Net income basis, page 146!:)) https://www.semperaugustus.com/clientletter Adding some 10 percent growth for the coming year leads to ~31 USD EPS per B share, which is ~16x. Not bad comparing to SNP's 22-23x, almost 30 per cent cheaper for arguably not worse business, kind of obvious choice here. But perhaps also quite fairish on an absolute basis? But I used to think an obvious "undervalued" zone (where one could expect ~15 IRR), would be somewhere under 14x, which again translates into ~1.3 BV:). Nothing very wrong with the 10+ IRR though:)

-

I think the main difference is that the US government prioritizes the success of companies and capitalists after all (call it some spillage), whereas the CCP, while also doing this (but also having more goals, like 'common prosperity'), primarily cares about its own survival, even if it means sacrificing those same capitalists.

-

I do not see anything very wrong with the timing, especially from shareholders perspective, because it is right after biggest dose of annual information (results and the letter) is being disclosed. He perhaps could do better for himself (and for more active folks:)) by timing it opportunistically, but for general BRK shareholders it is as fair as could be, no?

-

Yea I understand, but everyone is free to estimate IV however they like and we could still measure the outcome against BV. Historically, from what WB used to say or write about it etc, it was somewhere between 1.6 BV and 1.7 BV I think, perhaps slowly creeping higher with time.

-

+1

-

I think all this (Greg buying and Berkshire buybacking) are very great news. It is interesting they are resuming buybacks at 1.5 BV though. I thought WB was more of a 1.3 BV guy:). Perhaps they are relaxing this a bit, which only makes all the sense now. Maybe this could lead to a new 'soft floor' at 1.5 BV? Now, anybody want to guess were this mysterious IV until buybacks continues is in their heads? 1.65-1.7 BV? More:)?

-

Date yourself without dating yourself - How many?

UK replied to rogermunibond's topic in General Discussion

-

LOL. No problem with colour selection though, I always go with black or dark grey:)))

-

Would you take $10k to stop using their product?

UK replied to bizaro86's topic in General Discussion

I second IBKR. But also maybe Google services (search, maps, waze, yt etc)? And also perhaps some pharma/healthcare products, where people just do not have a choice? -

I thought this might be interesting, so I asked Gemini, but it seems impact is very limited: In Iran and surrounding regions, demand for BTC and USDT has spiked as a direct response to the conflict's impact on local infrastructure: Currency Protection: As the Iranian Toman devalues due to war uncertainty, locals are trading fiat for BTC to preserve purchasing power. Sanction Hedging: With threats to the Iranian banking system and the potential for increased global sanctions, Bitcoin is being used as a non-confiscable "exit ramp" for capital. Operational Resilience: Despite an 80% drop in network activity during peak internet blackouts (Feb 28 – March 1), on-chain data shows that as soon as connectivity returns, volume surges as users rush to move assets out of centralized regional exchanges. Local Capital Flight (Estimated: $15M – $40M+) In the immediate aftermath of the February 28 strikes, demand in Iran spiked as citizens sought to protect their wealth. On-Chain Outflows: Data from firms like Chainalysis and TRM Labs showed that hourly outflows from Iranian exchanges (like Nobitex) surged by 873% above the 2026 average. The Volume: In the first 72 hours of the conflict, approximately $10.3 million in "excess" outflows was recorded. While some of this is internal exchange management, a significant portion represents retail users moving BTC to self-custody or global platforms. Infrastructure Bottleneck: This number would likely be higher, but a 99% drop in internet connectivity in Iran during the peak of the strikes physically limited the amount of demand that could be executed.

-

I have no idea, but am ready

-

-

+1

-

More than 80 percent of Iranian oil exports go to China?