dartmonkey

-

Posts

642 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by dartmonkey

-

I don't disagree with anything you said, but I don't seem to be making my point very clear. You said that Fairfax's top 10 holdings have done great over the last 5 years, and I am just saying that if you take any portfolio manager's top 10 holdiongs, they are quite likely to have done great over the last 5 years, just because having done great MAKES them a top 10 holding. A better test of how well their biggest investments have done over the last 10 years is not to take 2025's top 10, but rather taking 2020's top 10. These would be, from the 2020 annual report: Atlas (now Poseidon) US$979m Eurobank $800m Fairfax India $402m Quess $356m Blackberry $298m Recipe $293m CIB $290m Exco $238m Stelco $231m Kennedy Wilson $230m This would include Blackberry just because it was a big investment then. The fact that it is now only worth $134m means that it is now insignificant to results going forward, but it wasn't insignificant in 2020.

-

There is an important survivor effect in play here, since the top 10 holdings are very often the ones that have done well. Blackberry would have been a top-10 holding in 2020 for instance, but because it is down a lot, it is no longer top 10, and so it isn't counted. Doesn't change the fact that the equity investments have done spectacularly well in the last 5 years, but this is not the best way to show it.

-

Here's the grain of salt, then: the fee applies to book value gains beyond 5% of the issuing price ($10) every year. That essentially means that the highwater mark moves up by $0.50/share every year (5% of the issue price), so if $21.85 was the number at the end of 2023, it should be $22.85 now. Doesn't make a huge difference, but assuming I'm right, it means we still have a little runway beyond the current (end of Q3) BV of $20.73/share before FFH takes its 20% cut. Not that I have anything against them taking that fee, on the contrary, I hope they take huge fees, as long as they leave us the other 80%.

-

Easy for what to happen ? The article says that Berkshire’s 20% annualized returns, over 60 years, means it has outperformed the S&P 500 (9.9% annualized, including dividends) by 100%. Great, huh? Except that that would mean a Berkshire investor would have twice as much as an index investor, whereas the total return with Berkshire over 60 years would be 55,000 times your initial investment, whereas with the S&P it would be 391 times. In other words, the Berkshire investor would have 141 times as much as the index investor, not twice as much. Compound math is hard…

-

It’s worth pointing out that if you take Fairfax’s BV + float, you get $60b at the end of 2024, compared to its market value of $30b. Market cap is now $42b, a bit closer, but BV + float is up too. Buffett didn’t really answer the question as to how much the float was worth, because he just said he wouldn’t accept an offer to buy the insurance businesses for the same number of dollars as the float. Because the insurance businesses have always made substantial underwriting gains, in addition to the return on the invested float, this is a low bar. The way I see it, the insurance businesses have two components of value : the growing underwriting earnings (4-5% of premiums, in an average year) plus the stream of earnings from having the float invested in fixed income investments (mostly treasuries.) It is true that the float does not belong to Fairfax, but in my opinion, that does not lessen its value, as long as you think it is quasi-permanent (or even, growing.) And you could say the same thing about the underwriting- it is only worth a multiple like 15x as long as it is not going away in a few years. Since I think this is a tiny risk, I would assign 100% value to both of these earnings streams.

-

As long as you believe the float is permanent, its value is already included in the stocks and bonds valued in step 1. Typically, Fairfax is constrained as to how it has to invest the float, and it is all in the bond portfolio, while Fairfax's own equity is largely invested in stocks and in operating businesses (Poseidon, Sleep Country, Recipe, etc.). Float was $36.9b at the end of 2024, with equity at $23.0b, so the question of whether you count 100% of float as assets which effectively belong to Fairfax, as I do, or some lesser percentage, makes a pretty big difference.

-

I think it's a very good question, and I was thinking the same thing myself. Buffett suggests a 'five groves' technique for Berkshire and the same sort of thinking could be applied to Fairfax. Many people follow price book (around 1.6), given the facts that earnings can be quite variable, as the company's stock holdings fluctuate and underwriting is pretty variable from year to year. But I think earnings is really the crucial metric, ideally separating out the stock and bond investments (and valuing them at market value), and of course removing dividends from those stock and bond holdings, and taking some sort of average combined ratio (say 96%, although recent results have been better), and assigning some sort of conservative multiple (say 15) to the pre-tax operating earnings of the non-insurance businesses. I haven't seen such an estimate on these boards, but perhaps I am forgetting. Perhaps others would like to chime in on how this should best be done and then when we have settled on the best way of doing it we could divvy up the work. So as a first draft, my approach would be: 1. Calculate the value of the stock and bond portfolios, these will be valued at market value 2. Find the income from all of the above, so that it can be subtracted from pre-tax earnings 3. Calculate the value of associates (companies with 20-50% ownership) 4. Find the average combined ratio of the past 10 years; I'm guessing it's about 96%, so 4% underwriting earnings, but whatever it is, apply it to current net premiums written (NPW) 5. Calculate the earnings from all the consolidated businesses (positions with >50% ownership), and subtract minority owners' shares. 6. Calculate the ratio of earnings from 3,4 and 5, minus minority stakes, minus income from stocks and bonds marked to market. 7. Calculate the current market value of FFH, minus the stock and bond portfolios in #1. 8. Calculate what the P/E ratio of operating businesses is, i.e. #7/#6 This will not count the value that Fairfax occasionally creates by opportunistically selling holdings acquired at lower prices, but I think it would be a good metric to follow.

-

My message seems to have been swallowed up so I will try again, more briefly: I think we probably agree that E is being understated by accounting conventions by about 10% ($25b book value, probably about $2.5b difference between 'fair value' and accounting valuie for the 20-50% holdings, notably Eurobank, Poseidon and FIH.) But this would actually make the ROE look higher, not lower, since the equity is in the denominator of the fraction. Of course, at the end of the day, what matter is earnings, not equity, and accounting conventions probably ARE understating earnings, since part of earnings is the unrealized gains from equity holdings. For instance, Eurobank is held at $2.7b based on the price paid for the stake, plus undistributed retained earnings, minus dividends, whereas the stake is actually worth $4.9b, and an increase of over $2b just this year! If the stake were marked to market, that would be $2b of pre-tax earnings right there. If Fairfax is at 8.5x earnings despite having grown EPS by 21%/year since 2015, why the hell should I care about book value?

-

I am jealous of you, I would do the same thing if I didn’t have such an outsized position already. Buying more on share price weakness has been something that has been possible for a long, long time… But this conversation makes it seem likely that we are at something like peak pessimism. Maybe I will go a little more outsize, one last (?) time. You can’t often buy a bunch of assets growing at >10%/year at boxing day sale prices.

-

The European shares traded in Athens are much more liquid and trade with much higher volume, 5 million shares instead of 500, but they show a similar share price increase since the reorganization in effect since December 12. The company has also restarted its aggressive share repurchases, which may be why the share price has been rising :

-

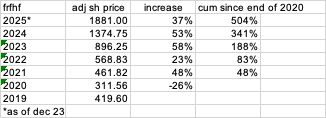

Looks like we won't get the hoped-for plunge. Price on Friday Dec. 5 at close, before the announcement: US$1679 Close on Monday Dec. 8, the first trading day after the announcement: $1751.53, so up 4.3% Close on Friday Dec. 19, the day of TSX60 index inclusion: $1830, so up 9.0% As I write this, on Dec. 23: $1880.43, so up 12.0% It's been another year of strong price gains. After dropping 26% in 2020, shares rebounded and have seen increases of 48%, 23%, 58%, 53% and now 37% in the last 5 years, adjusted for dividends. With the share price increase, my stake has become 48% of my holdings but I'm not selling. Shares may be up 500% since the end of 2020 but I think the company's performance has matched the share price increase, so they are not much more expensive now than they were 5 years ago. Current price:book is 1.60, but that book is undervalued both because it is based on end of Q3 share values (Fairfax's biggest mark to market positions are uip, 8% for the TRSs and 33% for Orla), but especially because other positions that are equity-accounted like Eurobank are undervalued compared to their publically traded values.

-

I’ve got to vote for the ‘old habits die hard’ side, as opposed to the ‘have learned from their mistakes’ side. I don’t see a lot of evidence of recent investments that are aiming for Mungerian quality as opposed to Buffettian value plays. And I’m not sure I want them to - why change a formula that works for them? There will be mistakes like Blackberry, and maybe Under Armour will be one of them, but no one bats 100%, and they don’t have to. And on the bright side, the occasional Blackberry will keep Fairfax’s share price from getting too high.

-

… or b) and this is somewhat related to point a), you have great managers of those businesses who understand capital allocation who buy back a large amount of stock if their stock price is disconnected from fundamental value to create per share value. … I think Einhorn has pivoted to the second of your options but it took a long time to get there. He has institutional constraints which makes the game even harder. I don’t understand - if Einhorn wants to avoid the problem of undervalued stocks not rerating because of the market structure changes you have described (so much money in index funds and quantitative easing funds that avoid such stocks), how can share repurchases solve the problem? Do you mean that Einhorn would only purchase shares in companies that are themselves repurchasing their own shares?

-

A couple of observations from me: 1) fih is not a $1 selling for 50c; it's a GROWING $1 selling for 50c and this makes a big difference … 5) what I care is PERFORMANCE, I.e. NAV/BV growth. I want fih to expand, make investment and compound at 15%+. … Nice point, we are paid to wait. 7) On the 100% fdi insurance rule, I hope this allows them to one day buy the godigit shares they do not own. They don't need to raise cash anymore or have public markets validation. Keep everything in house, 100% controlled! You probably know this, but GoDigit is not owned by FIH. And even Fairfax FFH only owns a little less than 50% of it, so while the new law may give FFH some options if their partners wish to sell, it’s not just a matter of liquidity. More generally, the point was made that 11 years is a long time to be patient, and someone should ask management about this. What can management say? The trip is going well. Yes it’s long. No, we’re not there yet. Stop asking. Try to think about something else.

-

Yes: The first performance fee was paid based on results at the end of 2017, and they took shares as per the contract, which was "7.7million subordinate voting shares valued at $14.93 per share (the weighted average share trading price over the last ten trading days in 2017)". The second performance fee was paid based on results at the end of 2020, also in shares as per the contract, but it was tiny: "a performance fee of $5.2 million was payable and settled with the issue of 546,263 subordinate voting shares of Fairfax India". The third performance fee was paid based on results at the end of 2023, and as per the contract, Fairfax had the choice of receiving the fee in cash or in shares: "Fairfax Financial elected to receive the performance fee of $110.2 million in cash to minimize dilutive impact to Fairfax India shareholders, as the number of shares issued to settle the performance fee would have been based on Fairfax India’s share price which is currently trading at a discount to its book value." And last year (not a 3-year milestone for the calculation of the performance fee), they summarized their performance fees thus far: "Under the investment advisory agreement, Fairfax Financial is entitled to a performance fee, calculated at the end of each three-year period, of 20% of any increase in Fairfax India’s BVPS (including distributions) above a noncompounded 5% increase each year from the BVPS at inception in 2015. For the first two three-year periods, Fairfax India was required to settle the performance fee with its subordinate voting shares, but at the end of the third three-year period, Fairfax Financial elected to receive its performance fee payable of $110.2 million in cash to limit shareholder dilution." And as Safety points out, it doesn't make much difference whether Fairfax takes cash or shares for the fee - they are using far more cash to repurchase FIH shares anyways.

-

Here are some more numbers. Actually, they sold 25m of their 56,817,229 shares, not 25%, although this may end up being somewhere near 25% of the full investment, when you include the investment in preferred shares and warrants which was of a similar size to the stock investment. For the shares, Grok tells me the cost basis is ~C$5.47 per share, close enough to your figure and I don't think they have announced the exact figure. So for the shares, a total cost basis of 5.47*56.8m = C$310.8m. (All currency numbers in $C henceforth unless mentioned.) At the announced sale price of $17.6435, that makes for aggregate proceeds of approximately CDN$441.1 million (US$316.1 million). Since they give the amount in CAD and USD, we can impute that the exchange rate was 1.39544, consistent with a sale on Friday (they say they announced today that they sold 25% of their stake, not necessarily that they sold it on the day they announced it, but it may be that the sale really was dated on Friday Dec 5th.) That would mean their profit is 25m*(17.6435-5.47)= $304.3m. Eyeballing it, most of the shares were purchased in Q3 2022, Q1 2023 and Q3 2023, so let's say February 2023 very approximately, so we have held the shares on average for about 1 5/6 years. The gain on shares would be $304.3 + the gain on the remaining 31.817m shares, or another 31.8m*(17.10-5.47)= another $370.0, for a total gain of about $713.3m. This is a stunning gain of 230% in CAD, or 92% annualized from Feb 1st 2024. And that's just for the share component. They also have, since November 2024: (i) notes with US$150 million principal amount, convertible at Fairfax's option into 26,582,275 common shares at CDN$7.90 per share (maturity in 2030, with interest paid quarterly). (ii) 17,544,302 warrants, exercisable into an equal number of common shares at CDN$11.50 per share (expiring in 2030). At today's ORLA price of $17.10, that means the notes, if converted today, would be good for another gain of 26.58m*(17.10-7.90)= $309m, and the warrants also have intrinsic value gains of another 17.5m*(17.10-11.50)= $98.2m. Adding up all the gains, we have $304.3m on the sale, $370.0m unrealized on the remaining shares, $309.2m on the convertible notes and $98.2m on the warrants, or a total of $1081.7m. The cost basis is $310.8m for the shares, from about February 2024, and US$150m for the notes and warrants, from November 2024. The exchange rate in November was about the same as now, say $1.40, so the total cost basis of the notes is about C$210m. In other words, they have turned $521m into $1604m over an average holding period of about a year and a half, plus a little interest. Amazing, and I think this would definitely merit more than one exclamation point next March!

-

so pullback and buying opportunity? I see no reason for a pullback, no. My guess would be a modest incrase monday, say 5%, with an increase of 10% by the 19th. Hopefully I’m wrong and it plunges.

-

I think it is likely that Carvana’s 8% short interest (I was once in this unfortunate position too) and short covering have more to do with the steep share price rise than the buying by indexers. By contrast, only 0.5% of Fairfax ‘s shares are sold short (hopefully including Muddy Waters…) and so the scramble to buy is likely to be much less hectic.

-

That's an interesting way of thinking about it, selling debt as opposed to selling. I guess it's hard to know for sure, since we don't know what their alternative use of the funds might have been. The way I was looking at it, the preferred shares are 'debt-like', and they are paying down that debt, in a way that is tax advantageous. If they are paying down that debt by issuing other shorter term debt, then there are just buying long-term in exchange for short-term, which might be what they want, but they are not reducing their risk. If on the other hand they are retiring the preferreds as opposed to making equity investments or repurchasing their own shares, then they are playing it safe. It could be either.

-

This is the opposite of battening down the hatches. Perpetual preferred gives more flexibility not less. This was a decision based on maximizing returns as they replaced the preferred with long term debt which has tax advantages as you noted. These preferred shares are in many ways similar to debt, but they have the advantage of being treated as equity by regulators, and the disadvantage of having the dividends non-deductible as opposed to debt. Now that they are not constrained by capital availability, and have better credit, they can repurchase the preferred shares without falling afoul of regulators. I'm just saying that paying down debt puts them in a stronger position than purchasing new equity investments or writing more insurance policies. Repurchasing the preferred shares might not be quite as much 'battening down the hatches' as reducing regular debt, but it still puts them in a position where they will have less fixed expenses, don't you agree?

-

Absolutely. I guess there were good reasons to issue these preferred shares as far as regulatory capital goes, but now that they are in a comfortable capital position and their own shares are more reasonably priced, and equity markets pricey in general, it’s hard to argue against battening down the hatches and redeeming these shares.

-

Normally preferred shares would only included in the diluted share if they are convertible, which is probably why Hoodlum’s Beacon preferred share repurchase example would reduce the diluted share count. In Fairfax’s case, the I- and J-series of preferred shares whose repurchase they have announced for Dec. 31st are not convertible. As far as I can tell, none of Fairfax’s remaining preferred shares are convertible, as opposed to the E-series which were redeemed earlier this year.

-

Maybe a tad optimistic: in the first 3 quarters of 2025, they have retired about 340,000 shares, slower than 2024's 1.3 million shares for the whole year: At March 31, 2025 there were 21,581,313 common shares effectively outstanding (December 31, 2024 – 21,668,466). At June 30, 2025 there were 21,591,832 common shares effectively outstanding (December 31, 2024 – 21,668,466). At September 30, 2025 there were 21,328,705 common shares effectively outstanding (December 31, 2024 – 21,668,466). True, there was the price dip in Oct/November, mostly recovered now, but to get to 700,000 for the year, they would have to buyback more in Q4 than Q1-Q3 combined.

-

Nice graph, and it shows that the biggest non-BIAL investments at Q3 end (IIFL FInance, CSB Bank, IIFL Capital) are all up 8-26%), whereas FIH itself is down 8%. The 2 that are down (5Paisa, Fairchem Organics) are tiny. Bought a little more today, which is crazy, because I already have way too much. Trading sardines.

-

IIFL has had a nice move up, gradually over the last year, to INR569, within spitting distance of the share price at the end of 2023 when it dropped from the low 600s to about 350, when the RBI suspended its ability to issue gold loans, and then even lower to about 310 a year ago. We don’t talk much about shares that aren’t called BIAL, for good reason, since that one stock is about half of FIH’s book value, and maybe 2/3 of FIH’s real value. But IIFL was #2, at 452 as of Sept 30, and has moved up another 25% since then.