All Activity

- Past hour

-

I'm having a poor year, up about 6%. The biggest detractor has been software stocks I bought back in December.

I'm having a poor year, up about 6%. The biggest detractor has been software stocks I bought back in December. -

Am I the only one here who's had a rubbish first Half of the year?

thowed replied to thowed's topic in General Discussion

Thanks to you all, wise words, but also good to. know there are a bunch of smart people out there in similar situations, and owning similar assets. When you're doing this on your own, even though you know rationally your portfolio is full of good companies, it's still easy to doubt yourself. And this sort of environment irritates me with all the Memory fanboys gloating. -

I'm a glutton for punishment so I've been nibbling on some Volkswagen

-

I mean, yeah, obviously. The problem isn't winning the war. It's the next 50 years with a 5500 mile border, potentially 40 million newly-minted terrorists, largely indistinguishable from Americans, many of who would view the Geneva Conventions as naive suggestions. It is super strange how Americans keep on believing that "winning the war" is the end of things, not the beginning. When was the last time that was true? WW 2 or Korea?

-

New starter position in HONA (Honeywell Aerospace spin off)

-

Dividend Portfolio for Retirement Income: 6% or higher club

Rainier replied to dipod's topic in General Discussion

Any ideas for companies in this category? CME has declined enough that, with the special dividend, you’ll probably end up around 6% (maybe a little below 6%). VZ is over 6% now. -

down YTD with Fairfax, Stryker, and TCEHY causing most pain

down YTD with Fairfax, Stryker, and TCEHY causing most pain -

BRK, MKL, and FFH probably make up half of my portfolio, so I am under performing as well. I trimmed some google and boosted mkl and ffh on the big earnings drops which came around the same time Google hit its high. I am definitely lacking positions that add torque to a portfolio.

BRK, MKL, and FFH probably make up half of my portfolio, so I am under performing as well. I trimmed some google and boosted mkl and ffh on the big earnings drops which came around the same time Google hit its high. I am definitely lacking positions that add torque to a portfolio. - Today

-

Am I the only one here who's had a rubbish first Half of the year?

lnofeisone replied to thowed's topic in General Discussion

Absent LQDA I'm up 2%. CPNG is a big detractor for me as it was about 15% of my portfolio. I'm not excited about my portfolio but I go to sleep knowing it's probably sound. -

CVRX common. Don't say any reason for the big drop today so increased my position by about 40%. Now the 2nd largest in my portfolio.

-

Am I the only one here who's had a rubbish first Half of the year?

gfp replied to thowed's topic in General Discussion

I'm up for the year to date but it's been hard-ass work. Would have much preferred a peaceful buy and hold.

-

Am I the only one here who's had a rubbish first Half of the year?

ICUMD replied to thowed's topic in General Discussion

Ytd returns of 13% 1 yr return of 62% Thanks to Canadian banks and good timing with Google purchase. Terrible timing with Go Easy. -

Am I the only one here who's had a rubbish first Half of the year?

Libs replied to thowed's topic in General Discussion

Me too. Flat YTD. CSU, FFH, Terravest dragging me down. Also bought AJG and BRO too early. These things happen......I'm not worried. -

Which brokerage do you use? and will the timeline work(i.e isn't it close?)

Which brokerage do you use? and will the timeline work(i.e isn't it close?) -

Am I the only one here who's had a rubbish first Half of the year?

Castanza replied to thowed's topic in General Discussion

I only care about underperformance if I'm out of cash or more so think my thesis has changed on the companies I own and continue to buy. I in no way want massive exposure to SPY with 40%+ sitting in the MAG7 who has mostly underperformed. -

It's just like someone with severe TDS to go back to all the debunked law fare initiated against the Trump family. Look at the assholes that launched it - Fani Willis, Letitia James, James Comey, Joe Biden - all criminals trying to jail their major political opponent on bogus/fake charges - just like a banana republic. And of course, when Americans realized the lengths these assholes would stoop to - Americans rejected THEM and elected Trump. What idiots they were to try and put Trump in jail and remove him from the Presidential ballots. Americans are not stupid and understand corrupt politicians that have NOTHING to offer except "We don't like Donald Trump" Imagine that as your campaign platform.

-

Insurance - The Engine That Drives Fairfax

Maverick47 replied to Viking's topic in Fairfax Financial

This (flexible and intelligent capital allocation) is a really important differentiator for top notch insurance companies/conglomerates @Viking. There are plenty of publicly traded insurers who attempt to maintain underwriting discipline through an insurance cycle, but they unnecessarily restrict their capital allocation options. Too many of the insurance CEO’s limit their capital allocation decisions (when underwriting opportunities become less attractive) to share repurchases, dividends and possibly acquisition of other insurance companies. They either don’t appear to be able to think outside those boxes, or perhaps they just don’t have an optimal holding company structure for insurance company subsidiaries that would also allow them to acquire subsidiaries outside of insurance. If they are focused on Return on Equity, when profitable underwriting growth for the numerator is difficult to achieve, they typically will turn towards returning capital to shareholders as a means of reducing the denominator. This can result in a relatively efficient insurer, addressing the issue of “excess capital” if it would otherwise be invested in low return fixed income instruments and damage the Return on Equity measurement. But the problem can be that in their urgency to “return” excess capital to shareholders, they forget to consider whether the price at which they are repurchasing shares is favorable or not. Both Fairfax and Berkshire have been (and are) proving themselves to be adept at rationally scanning a much wider global opportunity set of places to invest any excess capital that can accumulate during softer markets. -

Anyone with a high allocation to Berkshire and Fairfax has likely under-performed and if the name of this site in any way selects for those types, it is likely that many have lagged the markets. But so what? What is six months over a lifetime horizon?

Anyone with a high allocation to Berkshire and Fairfax has likely under-performed and if the name of this site in any way selects for those types, it is likely that many have lagged the markets. But so what? What is six months over a lifetime horizon? -

Am I the only one here who's had a rubbish first Half of the year?

Eldad replied to thowed's topic in General Discussion

@thowed I think we own a lot of the same stuff. CRAWA saved me last year and TFII this year. But it has been a struggle for 2 years. Don’t worry, I’m pretty sure that means you are doing it right. -

Taking his cues from Trump, Carney's renovating the "Canadian Whitehouse". Canada’s Most Famous Fixer-Upper—the Prime Minister’s Home—Is Getting a Makeover https://www.wsj.com/world/americas/canadas-most-famous-fixer-upperthe-prime-ministers-homeis-getting-a-makeover-1a5b2b6d?st=85eDLt&reflink=desktopwebshare_permalink

-

Best Ideas 2026 - Half Time Report

treasurehunt replied to phil_Buffett's topic in General Discussion

Yes, I'm well aware that @whatstheofficerproblem is the man when it comes to LQDA, but I I don't think he turned in any picks in the best ideas thread. Or I missed the post with his picks. -

@Malmqky I prefer my Tencent undiluted. The Prosus guy is a nuisance. He is more of a threat to Prosus than the CCP is to Tencent.

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

Spekulatius replied to tnathan's topic in General Discussion

I would rather buy more AJG but I don’t own as much of it than you do. RYAN traded at a substantial premium to other brokers due to faster growth but the latter has largely evaporated. -

Am I the only one here who's had a rubbish first Half of the year?

Saluki replied to thowed's topic in General Discussion

I've underperformed this year too. A some of my midsize positions (NTDOY, META and CPNG) got cut down by a lot, and a few others that did well last year are just trading sideways or down a little. It happens. You can't outperform in the long run and the short run. -

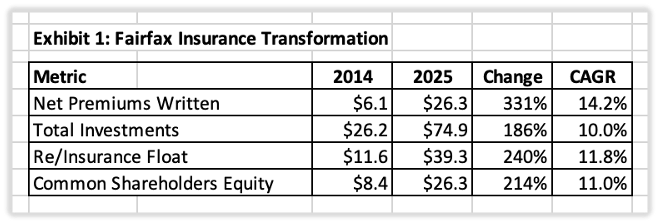

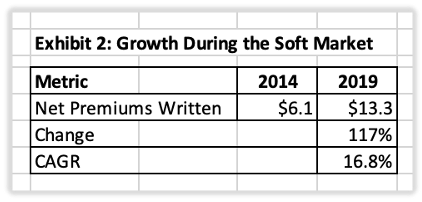

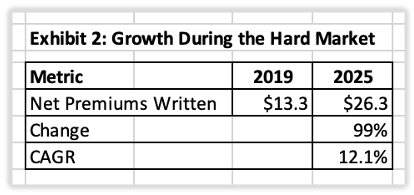

Article 4 into our deep dive into Fairfax's insurance business. What did they do in the last soft market? Fairfax's Insurance Transformation (2014–2025) One Insurance Cycle. One Management Team. One Remarkable Transformation. One of the best ways to evaluate management is to examine what it accomplishes over an entire business cycle. The eleven years from 2014 to 2025 provide an excellent test for Fairfax. During this period, the company navigated both a prolonged soft insurance market and one of the strongest hard markets in decades. The result was one of the most significant transformations in Fairfax's history. Several observations stand out. First, Fairfax dramatically expanded its insurance franchise. Net premiums written increased from $6.1 billion to $26.3 billion, while float grew from $11.6 billion to $39.3 billion. Second, shareholders ultimately participated in that growth on a per-share basis. This outcome was far from inevitable. Fairfax issued shares and partnered with outside investors to help finance several acquisitions. Over time, however, strong organic growth, improved underwriting profitability, rising investment income, share repurchases, and the purchase of minority interests largely offset that dilution. Finally, Fairfax created value under two very different insurance market conditions. During the soft market, management focused on expanding the business. During the hard market, it harvested the benefits of those earlier decisions. The transformation can be divided into two distinct phases. Setting the Stage In 2011, Andy Barnard was appointed Chief Operating Officer of Fairfax's insurance operations. His priority was not rapid growth. Instead, management concentrated on strengthening underwriting discipline, reinforcing Fairfax's decentralized operating model, recruiting talented leaders, and building a stronger insurance culture across the organization. These efforts attracted little attention from investors at the time. In hindsight, they laid the foundation for everything that followed. Phase One: Growing Through a Soft Market (2014–2019) “Someone’s sitting in the shade today because someone planted a tree a long time ago.” Warren Buffett Much of the period from 2014 to 2019 was characterized by a soft insurance market. Pricing was generally weak, competition was intense, and attractive underwriting opportunities were limited. Many insurers responded by chasing premium growth. Fairfax took a different approach. Rather than competing aggressively for underpriced business, management used the soft market to expand through acquisitions while maintaining underwriting discipline. Despite operating in a difficult insurance environment, Fairfax more than doubled net premiums written during the soft market. Premiums increased from $6.1 billion to $13.3 billion, representing compound annual growth of 16.8%. Most of that growth came from acquisitions rather than increasingly aggressive underwriting. Fairfax was deliberately expanding its insurance franchise while many competitors focused primarily on writing more business. The most significant acquisitions included: Brit (2015): $1.7B Various international insurance businesses (2015–2016): ~$1.0B Allied World (2017): $4.9B Between 2015 and 2017, Fairfax invested approximately $7.6 billion to acquire eleven insurance businesses. These acquisitions significantly expanded the company's geographic reach, product offerings, and underwriting capacity. The timing proved important. Late in a soft market, attractive underwriting opportunities are often scarce, but acquisition opportunities can be plentiful. Weak industry profitability frequently depresses valuations, allowing disciplined buyers to acquire high-quality insurance businesses at attractive prices. In effect, Fairfax was buying insurance assets when they were on sale. This strategy required significant capital. Fairfax issued shares and brought in minority partners to help finance several acquisitions, accepting short-term dilution in exchange for the opportunity to build a much larger insurance franchise. Whether that trade-off would create long-term value remained an open question. By the end of 2019, Fairfax had assembled a much larger and more diversified insurance business. Investors now had to wait for the next phase of the insurance cycle to see whether management's strategy would pay off. Phase Two: Growing Through a Hard Market (2019–2025) The insurance market began to harden at the end of 2019. Premium rates increased, underwriting conditions improved, and attractive growth opportunities emerged across much of the industry. Fairfax entered this environment with a significant competitive advantage. Years of acquisitions had created a much larger insurance franchise through which to deploy capital. Rather than pursuing additional acquisitions, management shifted its focus to organic growth. The results were exceptional. Between 2019 and 2025, net premiums written increased from $13.3 billion to $26.3 billion, representing compound annual growth of 12.1%. Unlike the previous phase, this growth was driven primarily by improved market conditions and disciplined underwriting rather than acquisitions. The hard market validated decisions that had been made years earlier during the soft market. Fairfax entered the cycle with a much larger insurance franchise and was well positioned to capitalize as pricing and underwriting conditions improved. The result was strong premium growth, improved underwriting profitability, and significantly higher float. Just as importantly, it answered the question investors had been asking since the acquisition program began. The larger insurance franchise was creating real shareholder value. By 2025, growth on a per-share basis closely matched the growth of the underlying business. Much of the dilution incurred while building the insurance franchise had been offset through organic growth, improved profitability, share repurchases, and the purchase of minority interests. What Was the Impact? Viewed as a whole, the results are striking. Between 2014 and 2025: Net premiums written increased from $6.1 billion to $26.3 billion. Total investments increased from $26.2 billion to $74.9 billion. Float increased from $11.6 billion to $39.3 billion. Book value per share increased from $395 to $1,260. Shareholders fully participated in the growth, with per-share results slightly exceeding the growth of the underlying business. More importantly, Fairfax successfully adapted its strategy as the insurance cycle evolved. During the soft market, management expanded the insurance franchise through acquisitions. During the hard market, it used that larger franchise to drive strong organic growth, improve underwriting profitability, and generate significantly more investment income. What Have We Learned? The transformation of Fairfax's insurance operations was not the product of a single acquisition or a favourable insurance market. It was the result of disciplined capital allocation across an entire insurance cycle. As the insurance industry begins to soften again, many investors assume growth opportunities will disappear. Fairfax's experience suggests otherwise. The opportunities change, but they do not disappear. Successful management teams adapt. They allocate capital differently as conditions evolve, but they remain focused on the same objective: creating long-term shareholder value. Over the past eleven years, Fairfax demonstrated exactly that.