All Activity

- Past hour

-

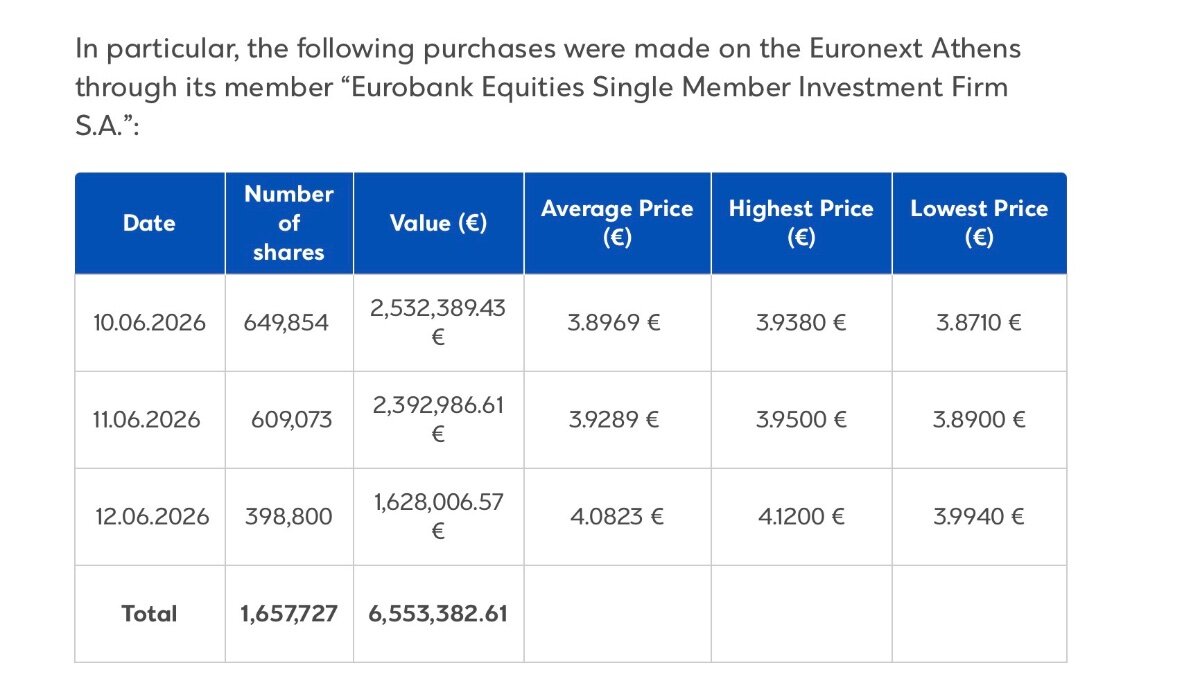

Eurobank got busy on the buyback again post dividend payout last week.

-

I continue to think this is a false choice. Equity investments at the insurance subsidiaries level shouldn’t have direct impact on capital allocation decisions at the holdco. They have $4b to dividend up to the holdco from the subsidiaries. My guess is they do half. They also have $400m of Poseidon at the holdco which I assume was also sold. Plus Eurolife proceeds and the 30-year debt raise means the holdco is well capitalized for buybacks even after buying out the Allied World minority interest.

-

https://finance.yahoo.com/markets/stocks/articles/andrew-peller-enters-definitive-agreement-110000838.html So Fairfax is buying a Winemaker Andrew Peller at an enterprise value of about 8x EBITDA. About $65M of Fairfax equity being issued for the controlling stakeholders. I assume the rest is in cash. May have some synergies with Recipe? I sure hope this is a better deal than buying back Fairfax shares. I think at the current prices everything needs to be evaluated from that lens.

-

You'd think, but no, thats what desperate oil bulls are saying.

- Today

-

I have a lot more empathy for these decisions. The risk generated by the GFC and a subsequent deflation were potentially existential. I don’t like participating in resulting.

-

There are opportunities now!

-

LOL Nothing like 2 days of continuous bombing to get the Iranians to "chicken out"...

-

-

It would likely depend on the rating of the convert, but in theory yes. But most insurance companies don't have this kind of in-house investing expertise, and don't want to build it.

-

I think you saw this with the Blizzard investment. Recall that was almost entirely debt, mostly secured on real estate, with laddered interest rates depending on the seniority. There was an equity sliver, but so little that it was really an option. This way, they used their regulated float to finance the acquisition, raising their average interest rate compared with investing treasuries, and also kept the equity upside. It's great, but limited: it is higher risk than investing in treasuries and they can't do it will all their float.

-

Iran doesn't know that because we haven't tried to put boots on the ground and we can either wait them out longer than they can survive or we can destroy their infrastructure. Just because we haven't done so doesn't mean it can't be done. Israel is also quite capable of destroying their infrastructure as a kind of US proxy. Iran knows all about proxies.

-

What I probably miss in the analysis of past FFH actions is the simple fact that sometimes a bad decision can lead to a good outcome and/or a good decision can lead to a bad outcome. Investing is about probabilities and you have to accept that. After the CDS trade they were geniuses and after the deflation and equity hedges they were idiots...and that is still the way most of us see it up to today. To me all those investments were bad decisions. The CDS trade was not better than the other ones. Those are all trades were timing is important. They were all done with the idea that you put very little upfront with huge payback if successful. But it misses the simple fact that FFH should be there for the long run and should simply let their businessmodel do the magic of compounding over many years and decades. Why try to do a quick shot? Don't get me wrong...I am a big fan of Prem and FFH. I am a shareholder since 2005 and never thought about selling, on the contrary. But I never liked those investments. But as Viking stated above, I just love the bussinessmodel and am amazed how well it has done even with decades of poor underwriting and some big investment mistakes. It says a lot about the long term potential.

-

The expected value investing style can look like gambling which is why most BRK and MKL investors who use a deterministic style of investing avoid Fairfax. They don’t like the portfolio. The goal of expected value investing is absolute returns not relative returns with the expectation of being wrong a third of the time. Post GFC, quality was repriced significantly higher and stocks that don’t screen well were repriced lower which hurt returns along with the accounting impact as ownership in more investments >20% increased.

-

This one gave me a good start on my otherwise semi-crappy monday!

-

Did Trump say that?

-

I didn’t have a clue what a CDS was at the time, but had a coworker who was involved, not with buying them, but creating and selling them to other companies on behalf of the property casualty company I worked for. We used to have quarterly q and a sessions with employees being allowed to ask senior management about the quarterly results. A few quarters in a row we recorded some losses from the part of the company that he was working in, which involved investing in and selling derivatives such as CDS’s. I was sort of the lone employee gadfly who was willing to ask questions about negative items to management, and I believe I’d been influenced by Buffett’s comment that derivatives were financial instruments of mass destruction, so a few quarters in a row I asked the leadership why we were involved in creating and selling financial instruments that we were losing money on, in an area we had no specific expertise in. Sometime later, but before the GFC in 2008, the company announced that they were shutting down that department and my coworker had to find a job elsewhere. All by way of noting how unusual it was at the time for someone like Francis Chou to be working with an insurance company, understanding what a credit default swap was, how valuable they would be in certain economic environments, and encouraging Fairfax to purchase substantial amounts of them. I was happy the company I worked for simply avoided a major problem and a near death experience such as AIG with their Financial Products division experienced by not selling credit default swaps to other parties. But I’m not aware of any insurance company other than Fairfax that took the right side of that trade…. Kudos to Francis!

-

Not sure how many people know this, but Francis would have been the first and probably only mutual fund manager to have bought CDS for his funds, if the regulators had been a tiny bit faster in approving his request. Francis had made a request to regulators to allow him to buy CDS in the Chou Funds, but by the time regulators approved the request, the CDS prices had started to move. He was also instrumental in Brian and Fairfax looking at the CDS in the first place and buying more as things started to look worse. Cheers!

-

I think Wade Burton talked about public versus private on the most recent conference call (strengths and weaknesses of each). I think he said they are agnostic - they want the best investment. The more I hear Wade talk the more I like him. Very logical and rational.

-

I don't know if it's intentional or not, or perhaps related to their bigger size allowing it, but I do see them doing more private equity type investments, a lot more control investments, or atleast having significantly more board representation rather than minority public market positions. An obvious exception to this being their recent position in UnderArmour. The lost decade errors not withstanding, I see them as vastly superior capital allocators than pretty much any of their investee management, who tend to be more operators. So their closer involvement is a good idea in this sphere. AGT foods recent balance sheet restructuring is a good example.

-

But the Treasury can - by sending direct checks to consumers (2020) or by writing checks to take over companies (Fannie/Freddie), or by coercing corporations to buy out failing competitors, or by deficit spending in the trillions. All while Fed Reserve holds rates at 0% and buys treasuries. You tell me which Congressman, elected by popular vote, is gonna say "fuck it - we've got to do the difficult thing and deal with the pain instead of the easy thing and print" And not just one - but enough of them to push through legislation. America doesn't have the will to do the hard/right thing Exactly. Which is why it's easy to know they'll do the easy thing - and print.

-

@Txvestor , one of my central ideas is something changed around 2018 with how they picked and constructed their equity portfolio. But it was even more - they started to focus more on optimization (like what got started in insurance in 2011). All you have to do is look at the companies they owed then - the biggest positions. It was loaded with very poor performers (putting it politely): - Legacy: BlackBerry, Resolute Forest Products/Abitibi, CIB, Sandridge Energy, Recipe - Purchased 2014 to 2017: Eurobank, Fairfax Africa, APR Energy, Farmers Edge, Boat Rocker, EXCO Resources, AGT Foods Issues: some combination of weak management, weak balance sheet, weak profitability/cash flow (some had all three). Eurobank, EXCO and Recipe are much improved companies today. The jury is out on AGT. Fast forward to today… the portfolio is loaded with queens. Common theme: all have strong management, strong/solid balance sheets, strong/solid profitability/cash flow. Complete 180 from pre-2018. That has to be by design. The change is simply too stark.

-

If anything, all of this takes time. I'm certain nothing will happen until we're peering into the abyss. There will be opportunities.

-

And you're right, they will print. But it's not that simple. The Federal Reserve can't fix a massive credit crisis just by providing liquidity to the Treasury market. Many of the systemic problems during times of extreme stress require fiscal policy, an act of Congress. The Federal Reserve is simply a lender of last resort; they legally can't spend money. Have you taken a good look at our Congress lately? I've been more impressed by the intellectual display of chimps at my local zoo. A fiscal crisis would leave everyone with nothing but bad options. I do not expect good judgment to come from our current government.

-

Exactly! On this last point I completely agree. Their corporate and business structure is a thing of beauty. They don't need to do a whole lot more than hit singles on the investment side to compound relentlessly and for a long time. I'm glad you mentioned the likely link between the big win with CDSs and the subsequent upside down macro bets and shorts. I highly doubt the lost decade would have turned out the way it did without that home run in 2008/9. In the aggregate it may even have cost more. Lastly even excluding the Shorts, the deflation swaps and the market hedges. Their investment returns were well behind most benchmarks. They sure had some beauties during that period, everyone and their mother knows about the infamous blackberry, but Sandridge energy, Resolute forest and a couple others that don't immediately come to mind. They lagged the benchmarks significantly to the extent that a colleague of mine said they look more like gamblers than investors. 2019/2020 was truly a turning point. I didn't see them do anything crazy during the Covid market selloff, in fact they doubled down on what they knew best ie TRS on their own shares. And masterfully handled the emerging inflationary environment on the bond side. They kept more to the private equity side as well. I think everyone here sees a relatively viable path to 15-20% annual compounding for the next 5-10yrs if they stay in this lane.

-

Yes. But we've seen what happens when it's time to collect. The losses are socialized and the government prints and deflation is avoided. It's not morally right. And you should invest in the companies owing the credit. But as long as we're the reserve currency, we'll print. No, printing is the alternative outcome to offset the contraction in credit. And they'll print. And they succeeded both times. And will do again.... because they'll print.