All Activity

- Past hour

-

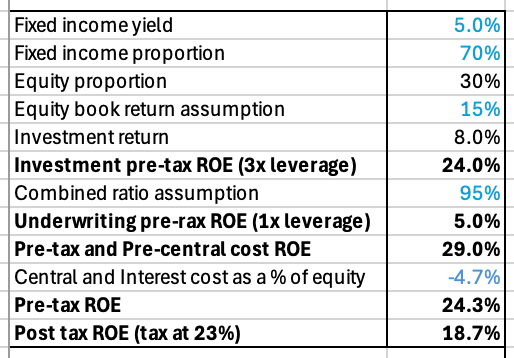

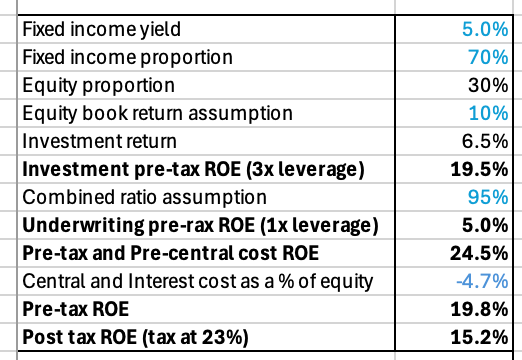

I agree I am a big fan of buybacks too given where the share price is. The good news is assuming a 10% forward equity return you can estimate a ~15% forward ROE, assuming a 15% forward equity return you can estimate a ~19% forward ROE. And this is before any additional unlock of latent value eg. Bangalore airport and situations like Poseidon where book value << market value.

- Today

-

An additional factor to consider is they were working with millions and hundreds of millions early on, now it's Billions, I believe around $28B, and size is a headwind. Though certainly not as much of one as for Berkshire. Yet another reason I'm a huge fan of their buybacks.

-

God bless AI!

-

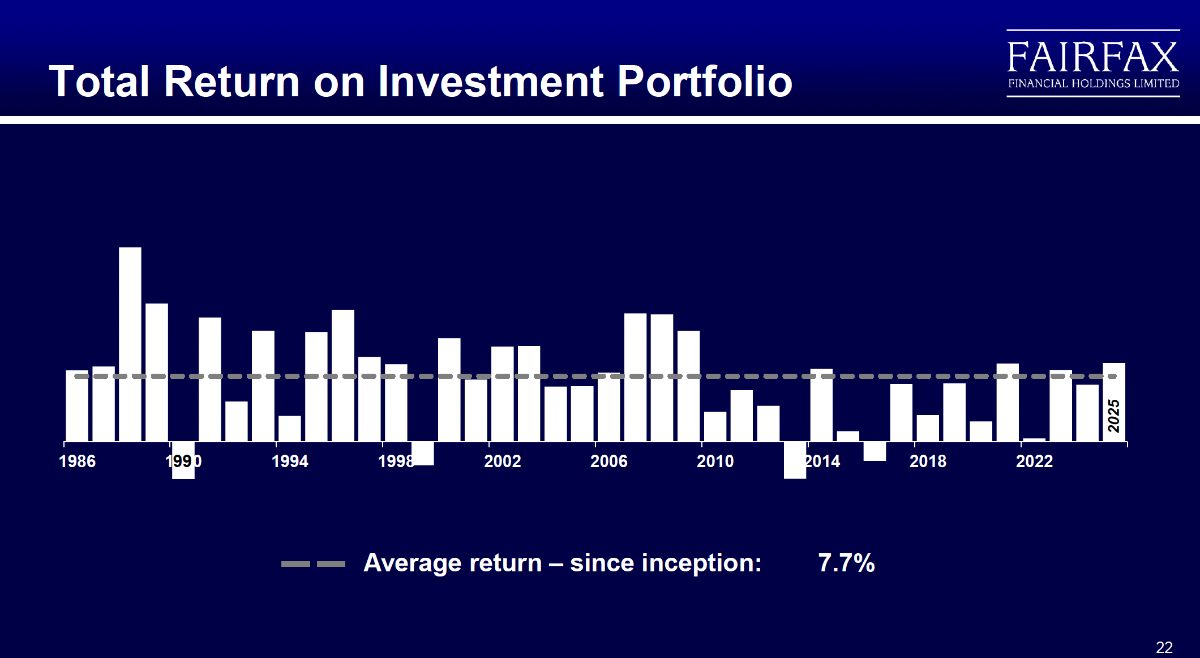

Btw @Maverick47 I just had Claude estimate the Geometric return based on the AGM chart, and historical annual reports and given the low volatility in returns (due to high FI %), it calculated the Geometric return is 7.5%, not far off from the average.

-

Agreed.

-

Yes I agree @Maverick47 good point, I had thought about that and yes its only a rough approximation. For example, on the other hand, their fixed income return in the calculation is likely overstated as i) the realised fixed income yield would be less than the approximated 5 years Fixed income yield given short duration cash held will reduce the overall yield. ii) There have been times when they have been significantly short duration relative to their liabilities (i.e assuming the 5 year yield is overstated for those periods). That would imply an equity return higher than I calculated above. In aggregate, their equity returns may be somewhere 15-20% annually over 40 years but I am quite confident to say they have trounced the S&P500 over that period.

-

I think you’re directionally on the right track with trying to approximate the equity returns by backing them out of the total investment returns. One caution I would make is to be clear in differentiating between an arithmetic average return and a geometrically compounded return. My guess is that the S&P 500 11.2% return is the CAGR over the period, meaning the geometric average. Meanwhile, the 7.7% Fairfax investment return looks to me as if it might just be the simple arithmetic average of the individual years. The geometric average is what we’d want to have in order to compare with the equity index, but I don’t them we have that here. And generally speaking, when you take into account the possibility of negative return years, which have occurred four times in the Fairfax history, then the geometric return, which is what we want for comparison purposes to the index, is always going to be less than what appears to be an arithmetic average return of 7.7%. My guess is that Fairfax’s equity returns on a geometrically compounded basis probably have still exceeded those of the index over 40 years, but that they likely may not have not been quite as high as 18.2% annually.

-

Nobody hinders you to look somewhere else.

-

But I will not deny that a lot of these problems have been building underneath the surface for quite some time. Our current state with Trump is simply a reflection of just how bad those problems have become. We should feel shame for the things Trump is doing. Yet when I look around all I can find is apathy.

-

The US is the land of opportunity. Which doesnt mean folks aint free to sit around wasting that opportunity bitching and moaning about stuff they have no control over....

-

I feel like United States is currently in a mania. It seems like irrational thinking is pervasive everywhere, most of all in our current administration. What a shame. America should be better than this.

-

Average total return of their portfolio (FI and equities) over the last 40 years is 7.7%. We don't have a direct number for the equity return but can approximate it. Last 40 year average 5 year fixed income yield is 4.2%. Lets assume Fairfax earned that yield. Split between fixed income and equity book has changed over time but I think 75% vs 25% is a good approximation for historical average. So, 75% * Fixed income return + 25% * Equity return = 7.7%. Lets assume FI return = 4.2% so equity return over 40 years = 18.2% Note that calculation is rough but S&P return over 40 years is 11.5% with dividends re-invested. So unless you meaningfully disagree with my rough calculation, over 40 years Fairfax equity returns have trounced the S&P 500.

-

Not precisely, but anytime you are making an acquisition you can always trade expected returns for risk by adding more leverage. It might not show up immediately, and in Fairfax's position you might even tell yourself, we can always bail out the subsidiary if needed, but ultimately it's risk. Of course if there is business stability for some period of time that risk dwindles and certainly that's a reasonable strategy given Fairfax's position. And yes they've employed that strategy in recent acquisitions. Thats what Fairfax investors need to understand. Between the leverage at different layers in the corporate structure they are taking on risk and you are to some extent betting on the prudence of their risk management.

-

I understand how BNPL is currently implemented is perhaps hard to repliacte - but why not by the card issuers themselves on payment terms for the credit cards? AmEx used to be a charge card you paid off every month. And then over the course of 1-2 years back in the late 2010s, they opted to allow consumers to roll balances, charge interest, and have a BNPL option of paying off large purchases at a lower interest rate over the course of 3-, 6-, or 9- months. Why couldn't a credit card issuer simply adopt BNPL-like terms for a specific card they issue and then no infrastructure, buttons, or merchant partnerships need be had? I doubt AmEx would do this given their upper-income focus on consumers, but it doesn't strike as difficult for any card-issuer partnered with a bank focusing on mid- to lower-income consumers a la Capital One/Discover.

I understand how BNPL is currently implemented is perhaps hard to repliacte - but why not by the card issuers themselves on payment terms for the credit cards? AmEx used to be a charge card you paid off every month. And then over the course of 1-2 years back in the late 2010s, they opted to allow consumers to roll balances, charge interest, and have a BNPL option of paying off large purchases at a lower interest rate over the course of 3-, 6-, or 9- months. Why couldn't a credit card issuer simply adopt BNPL-like terms for a specific card they issue and then no infrastructure, buttons, or merchant partnerships need be had? I doubt AmEx would do this given their upper-income focus on consumers, but it doesn't strike as difficult for any card-issuer partnered with a bank focusing on mid- to lower-income consumers a la Capital One/Discover. -

One of the most pro-Trump leaders in Europe: https://www.bbc.co.uk/news/articles/cgqj77909jpo A perfect example, if one was ever needed, about why it’s pointless to try and be Trump’s friend. Because if you aren’t kissing his ring constantly he’ll turn on you.

-

Ya come into my kitchen buddy, ya gotta take the heat The art of the haggle was well practiced, well before the art of the deal. Global Inventory will continue to drain, along with high US gas prices, all the way through the midterms. On his own admission, at about a US month of demand left in the US SPR, Orange Boy ain't got the cards. The haggle is just being friendly; recognise the entertainment value, and play the game. Play well ... and we can make you a deal between friends . SD

-

Counter drone technology is way behind and needs to catch up.

-

Netjets doesn't fly to small towns in BC. Also I would feel ridiculous flying on a Citation jet or slightly smaller all by myself every month or other month...even with a couple of other people it seems like such a waste of resources...money and jet fuel! That's a lot of other luxury trips I could take around the world flying in business class! Plus I'm not at Eff You Money yet...I'm at I Don't Need Your Dumb Ass, So Don't Waste My Time Money! Cheers!

-

I think it was 19% over 39 years but I can’t find the reference. Last three years have been good as we know but most of it hasn’t shown up in accounting returns yet.

-

The market structure changed a lot during the period you are focused on. I think if you are uncomfortable with leverage you shouldn’t own Fairfax. I see the leverage as a feature not a bug. They did change their investment style by taking more control and significant influence positions (which hurts reported returns up front) but not their process of looking for margin of safety. Again beating the index is an outcome of the process not the goal. Most institutions since the GFC are focused on short term relative returns b/c they want to keep the AUM. Thankfully we don’t have to play that game.

-

I doubt there was much of an uptick in oil getting out of the strait, with the mines still in place. It found it interesting to see oil drop below $80 without much changing in the flow of oil shipments. I think we will see another 2 months of little oil movement, with oil reserves continuing to drop.

-

Yes and no. Yes, you cannot eat relative returns, but if the S&P returns 15% per annum for 15 years while your equity portfolio returns 10% per year for 15 years, then clearly the people running the equity book are incompetent. As markets change, your investment style has to change. With all due respect, you could have bought plenty of incredible business at low multiple of earnings - ASR in 2004 is a good example (airport concessions in Mexico at 5x free cash flow.). If you need leverage to make your equity portfolio match the S&P then why not just be long S&P and avoid the issues that come with leverage?

-

The SOH is now closed but good deal for you my friend. We are in the bargaining stage where every barrel of oil comes with unlimited middle eastern haggling. The rug merchants are now in charge.

-

Sure, that is even better. What is the company's 40 year track record when it comes to its equity book?

-

How about 40 years?