All Activity

- Past hour

-

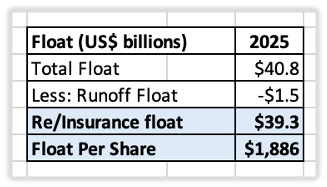

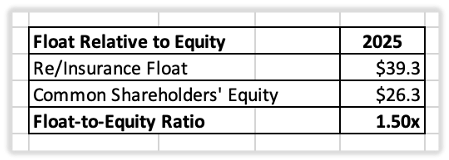

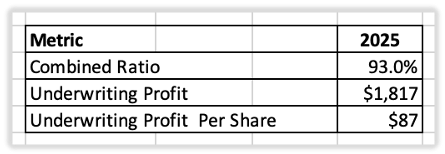

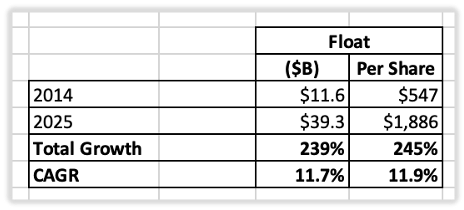

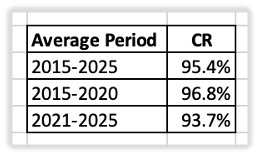

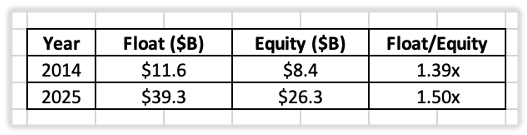

Article 2 in our series on Fairfax's insurance business Applying Buffett’s Float Framework to Fairfax In the previous article, Warren Buffett explained that investors should focus on three factors when evaluating an insurance company: The amount of float the company generates. The cost of that float. The long-term outlook for both. Let's apply Buffett's framework to Fairfax. Size: Fairfax Has Significant Float Warren Buffett's first test is simple: how much float does an insurer have? At December 31, 2025, Fairfax had total float of approximately $40.8 billion. For the purposes of this analysis, two adjustments have been made. First, runoff operations have been excluded. Runoff float has different economic characteristics than float generated by Fairfax's ongoing insurance and reinsurance businesses and is best analyzed separately. Second, Fairfax does not own 100% of certain subsidiaries, including Allied World and Odyssey. As a result, a portion of the float generated by those companies is attributable to minority shareholders rather than Fairfax shareholders. To keep the analysis simple and consistent with Fairfax's reported figures, no adjustment has been made for minority interests. After excluding runoff operations, Fairfax's insurance and reinsurance businesses generated approximately $39.3 billion of float, or about $1,882 per share. Exhibit 1: Insurance & Reinsurance Float Breakdown (2025) Fairfax has built a substantial float base. Before considering shareholders' equity, the company controls nearly $40 billion of investment capital generated by its insurance operations. Economic Significance: Float Exceeds Shareholders' Equity The size of float is important, but its significance becomes clearer when compared to shareholders' equity. At year-end 2025, Fairfax's common shareholders' equity was approximately $26.3 billion. Compared to insurance and reinsurance float of $39.3 billion, Fairfax's float-to-equity ratio was approximately 1.5x. Exhibit 2: Float Relative to Shareholders' Equity (2025) This means Fairfax had approximately $1.50 of float supporting every $1.00 of shareholder capital. Put differently, float was 50% larger than the equity supplied by shareholders. This is what makes float so valuable. When managed properly, it allows an insurer to control a substantially larger investment portfolio than shareholders' capital alone would support. Fairfax's investment portfolio is therefore funded not only by shareholders' equity, but also by a large pool of insurance float that has been built over decades of underwriting operations. Buffett's first test is therefore easily met. Fairfax has built a large and economically significant float base. Cost: Better Than Free Buffett's second test is the cost of float. Exhibit 3: Fairfax's Cost of Float (2025) In 2025, Fairfax reported a combined ratio of 93.0%. The company generated underwriting profits of approximately $1.8 billion while holding $39.3 billion of float. Viewed through Buffett's framework, Fairfax's float was better than free. Instead of paying to access this capital, Fairfax was paid to hold it. Trend: Growing Float Buffett believed the long-term trend was the most important factor of all. A large amount of float is valuable. A growing amount of float is even more valuable. Exhibit 4: Fairfax Insurance & Reinsurance Float Growth (2014–2025) From 2014 to 2025, Fairfax's float grew from approximately $11.6 billion to $39.3 billion. On a per-share basis, float increased from $547 to $1,886. This represents compound annual growth of approximately 12% over the past eleven years. Growth alone, however, is not enough. Buffett's third test also considers the long-term cost of float. Exhibit 5: Fairfax Combined Ratio (2015–2025) Fairfax delivered an average combined ratio of 95.4% from 2015 to 2025. The record includes years with elevated catastrophe losses. More importantly, underwriting performance has improved in recent years, with the average combined ratio declining from 97% in 2015–2020 to 94% in 2021–2025. Many insurers can grow float by sacrificing underwriting profitability. Others maintain underwriting discipline but struggle to grow. Fairfax accomplished both. Over the past eleven years, float increased by 245% while underwriting remained consistently profitable. Growing float is valuable. Growing float at a negative cost is even more valuable. A Fourth Question Buffett's three questions provide an excellent framework for evaluating an insurance company. I would add a fourth: How important is float to the business model? The answer depends on the relationship between float and shareholders' equity. The larger the float relative to equity, the greater its potential impact on shareholder returns. At year-end 2025, Fairfax's insurance and reinsurance float was approximately $39.3 billion compared to common shareholders' equity of $26.3 billion. Float was about 1.5 times larger than equity. Exhibit 6: Float Relative to Equity (2014 vs. 2025) What makes this particularly noteworthy is that the relationship has remained remarkably consistent over time. In 2014, float represented approximately 1.39 times shareholders' equity. By 2025, the ratio had increased modestly to 1.50 times. This means Fairfax has not only grown its float; it has preserved its importance within the business model. Despite substantial growth over the past decade, float remains larger than shareholders' equity and continues to provide meaningful leverage to shareholder capital. This distinguishes Fairfax from Berkshire Hathaway's evolution. As Berkshire grew into one of the world's largest companies, shareholders' equity expanded much faster than float, reducing float's relative importance over time. Fairfax has followed a different path. Insurance remains the foundation of the business, and float remains one of its most important competitive advantages. Buffett's Scorecard Viewed through Buffett's framework—and the additional question regarding the importance of float—Fairfax performs well across every measure. Float is large. Float has grown consistently over time. Float has been obtained at a negative cost. Float remains a significant contributor to shareholder returns. Individually, each characteristic is impressive. Together, they describe a valuable insurance franchise. Over the past eleven years, Fairfax has grown float from $11.6 billion to $39.3 billion, maintained profitable underwriting throughout that growth, and preserved the importance of float to its business model. Few insurers have accomplished all three simultaneously. Buffett's framework was designed to identify insurers with durable economics. By that standard, Fairfax appears to possess one of the strongest float franchises in the property and casualty insurance industry.

-

@Saluki - Do you expect your former regulator to have more teeth on some of they craziness in these markets? Or are their hands tried now? The administrations under Biden and Trump are vastly different. Did you feel it during your time there?

-

Insurance is the foundation upon which Fairfax Financial is built. The company's insurance operations generate underwriting profits and float, which provide the capital that supports Fairfax's investment activities and long-term value creation. I the coming days I will be publishing a series of posts on Fairfax's insurance business: why float is so important, how insurance cycles create opportunity, how Fairfax built its global insurance platform, and why the company appears well positioned for the future. Together, these articles explain how Fairfax built its insurance franchise and why it has been such an important driver of shareholder returns. We will start with two articles on float. ----------- Float: The Engine that Drove Berkshire Hathaway’s Growth For more than fifty years, Warren Buffett has described insurance as one of the greatest business models ever created. The reason is not underwriting profit. The reason is float. Float is a little like compound interest as an investing concept. It is easy to define but much harder to fully appreciate. Yet understanding float is essential for understanding companies built on the Berkshire Hathaway and Fairfax business models. Back in the 1990s, property and casualty insurance was the primary engine driving Berkshire Hathaway's growth. GEICO was acquired in 1996 and General Re followed in 1998. Given the increasing importance of insurance to Berkshire's future, Buffett used his 1998 annual letter to explain what investors should focus on when evaluating an insurance company. He wrote: "With the acquisition of General Re — and with GEICO's business mushrooming — it becomes more important than ever that you understand how to evaluate an insurance company. The key determinants are: 1.) the amount of float that the business generates; 2.) its cost; and 3.) most important of all, the long-term outlook for both of these factors." Notice what Buffett is saying. The most important factor in evaluating an insurance company is not earnings, premium growth, or even underwriting results viewed in isolation. It is float—how much the company has, what it costs, and whether both are likely to improve over time. That is a remarkable statement given how little attention float receives today from analysts and investors. What Is Float? Buffett's definition is straightforward: "To begin with, float is money we hold but don't own. In an insurance operation, float arises because premiums are received before losses are paid, an interval that sometimes extends over many years." When an insurer writes a policy, it collects cash immediately. Claims, however, are usually paid later—sometimes months later and sometimes years later. During that period, the insurer holds the money and can invest it. That money is called float. Consider a simple example. An insurer collects $1 billion in premiums today and expects to pay claims gradually over the next several years. Until those claims are paid, the insurer can invest that $1 billion in bonds, stocks, private businesses, or other assets, subject to regulatory and liquidity requirements designed to ensure claims can be paid when due. The money does not belong to shareholders. Eventually it will be used to pay claims. But until then, it is available for investment. This is what makes insurance different from most businesses. Manufacturers must build products before they can sell them. Retailers must purchase inventory before customers walk through the door. Insurance works in reverse. Customers pay first and the service is provided later. The result is a large pool of investable funds. Why Float Matters Float creates a second source of earnings. The first source comes from underwriting. If premiums exceed claims and expenses, the insurer earns an underwriting profit. The second source comes from investing float. As a result, a well-run insurer can earn money both from writing insurance policies and from investing the funds generated by those policies. A growing insurance operation can therefore produce an ever-expanding pool of capital that management can deploy into attractive investments. Over long periods of time, this can become a powerful compounding engine. The Cost of Float Not all float is valuable. To understand why, investors need to understand what Buffett calls the cost of float. An insurer receives premiums today but eventually must pay claims and operating expenses. If claims and expenses exceed premiums, the insurer records an underwriting loss. Buffett views that underwriting loss as the cost of obtaining float. He explained it this way: "Typically, this pleasant activity carries with it a downside: The premiums that an insurer takes in usually do not cover the losses and expenses it eventually must pay. That leaves it running an underwriting loss, which is the cost of float. An insurance business has value if its cost of float over time is less than the cost the company would otherwise incur to obtain funds. But the business is a lemon if its cost of float is higher than market rates for money." This point is critical. Float is not automatically valuable. An insurer that consistently loses money underwriting may be paying too much for its float. In that case, the benefits of investing float can be overwhelmed by poor underwriting results. The insurer has effectively borrowed money at an unattractive rate. The best insurers achieve the opposite outcome. They generate underwriting profits while simultaneously investing their float. Better Than Free This is where insurance becomes truly interesting. If an insurer consistently earns underwriting profits, the cost of float becomes negative. Instead of paying for its float, the insurer is actually being paid to hold it. Buffett often described this as one of Berkshire Hathaway's greatest advantages. For decades, Berkshire generated billions of dollars of float while also reporting underwriting profits. The result was a rapidly growing pool of investment capital that cost nothing—and often less than nothing—to hold. This combination helped fuel Berkshire Hathaway's extraordinary long-term success. The Three Questions Every Investor Should Ask Buffett's framework remains remarkably simple. When evaluating an insurance company, investors should ask three questions: 1. How much float does the company have? A larger float base provides more capital to invest. 2. What does the float cost? Consistent underwriting profits suggest the company is obtaining float on attractive terms. 3. What is the long-term trend? Is float growing? Is underwriting disciplined? Has management demonstrated skill over many years and across multiple insurance cycles? The answers to these questions often reveal far more about an insurer's long-term economics than short-term earnings results. Why Float Is So Important For Buffett, float became one of the primary engines that powered Berkshire Hathaway's success. Understanding float is therefore not simply a lesson about insurance. It is the first step toward understanding the model Buffett helped popularize: using insurance float as investment capital. Berkshire Hathaway perfected this approach, and Fairfax later adapted it. In both cases, float became much more than an insurance liability. It became a source of low-cost investment capital that could be compounded for the benefit of shareholders over many decades. In the next article, we will apply Buffett's framework to Fairfax and examine the size, cost and growth of its float.

-

The Moscow Times [June 28th 2026] : Putin Vows to Ensure Russia’s Security Amid Ukraine Retaliatory Strikes - - - o 0 o - - - Naturally, everybody can count on that and take it as a given, despite other puclicly available facts. [*shrugg* }

-

I don't know too much about Norway's sovereign wealth fund, but I understand that it is a vehicle to invest surplus tax revenue coming from oil. The fund does not act as a political or strategic owner (if you look at its holdings, it may as well be an index), is not permitted to own more than 10% voting shares, and is mandated to invest only in assets outside of Norway.

-

+1 Love to see it. This has been the thesis since I first found the company in 2012 when they had a single producing royalty, $200M in cash, and a hopeful Kami development. The path didn't end up quite that simple and the progress was hidden for years behind share issuance/debt service for the Potash royalties and a weak commodity market in general until 2021. It still seems under followed and under appreciated - the share price took days to move following the sale of the gold royalty for an amount that was a significant chunk of the market capitalization of the whole company. And it took weeks more to appreciate the reinvestment of those proceeds by taking out Lithium Royalty corp. Plenty of opportunity in this name to buy AFTER the news has been announced and I had added after both. All that being said, I reduced my position by ~10% last week. Altius has been the only name in my portfolio performing YTD and all other names are flat to down over a 6-12 month period so took some off the table near ATHs to buy other names.

-

I talked with my mom and the temperatures in the city she lives reached 40 DegC. It’s unbearable for some especially older people. not great but sooner or later German homes and apartment will need air conditioning. I lived in Germany recall the hot summers in 1976, 1983 and 2003 occurred after I left. The currently one beats them all by quite some margin and the official summer has barely begun. Climate change looks pretty real to me and countries e8ll have to adapt. I think air conditioning units and heat pumps (which can heat and cool) should sell fairly well.

-

THAT makes all the difference.

- Today

-

Because the oil is a valuable resource. That doesn’t mean it easy to get out, but it does mean the state can charge 80% taxes in Norway and the exploration and production is still profitable for Equifor. But there is no AI resource lying in the ground to be explored and produced. It‘s IP and needs to be created by entrepreneurs or there won’t be AI. Thats why it is entirely different.

-

Lou Brock: "Show me a guy that is afraid to look bad, and I will show you a guy I can beat every day"

-

Mark Twain: "What's an expert anyway? Just some guy from out of town" ...Learn to think for yourself

-

I'm not totally sure how to read your above post @Spekulatius, but Norwegian O&G exploration was in the early Norwegian O&G days almost also a merely a concept, which took a lot of O&G engineering, R&D and CAPEX to bring it to reality, production. The practice of what I would call Norwegian successful state capitalism in the Norwegian O&G venture is an interesting study, that we perhaps should descuss in a topic outside this topic.

-

It’s a bad analogy, because the oil in Norway was already there. There is no AI sitting somewhere above or below the ground waiting to be unlocked -it’s has to be build first. If you don’t build it, there will be nothing.

-

How do you know their products are great? What does this even mean in cosmetics? For me, there are only two kinds of products in cosmetics - those that sell and those that don’t. If they sell, they are great. I think there are more straightforward fish to fry in Korean Markets.

-

My suspicion is that they clear like bucket houses as of forgone times, which means sometimes they don’t.

-

Yeah, @Sinbius, Here at CofB&F, we are a bunch, a community, of individual DIY investors, that do our very best to steer clear of the costs related to the involvement of the institutional imperative, and we all know it's not in our power to save world from it. But we can actually still make a difference, a material difference for others than our selves, for some near and dear to us. Keeping the bulwark up, intact and running some times calls for, requires mentally venting to decompress, which is what I think Greg [ @Gregmal ] did here by starting this topic.

-

Check out my comprehensive 13F / Mutual Fund trackers (alphafiling.com)

gym97 replied to gym97's topic in General Discussion

Supplemental HEICO data

-

Check out my comprehensive 13F / Mutual Fund trackers (alphafiling.com)

gym97 replied to gym97's topic in General Discussion

I've improved this significantly by adding financial data. You can now easily layer-on fundamentals when evaluating another manager's portfolio This is Giverny for example. You can then click-through to see the fundamentals of the actual stocks he owns, i.e. full 3 statements for Google, Heico, etc. US Stock data was reasonably easy to extract but I'm slowly going through some companies/industries in categories and enriching the data. Starting with IT Services, Software, and Serial Acquirers. Improvig by the day.

-

Mohnish too....

-

Amore Pacific had a channel conflict issue. They built out their own proprietary wholesale channel selling Amore-Pacific-Only products. That channel was competitively disadvantaged (couldn't sell competing products) and that led to a huge channel mess. The products themselves are great and they invest LT behind their brands, etc. Combine that with a slowdown from Chinese consumers and trends, etc. and you have bad operating margins.

-

@Red Lion - I don't like lax customer service and accounting... it's a recipe for fraud and counterparty risk.

-

https://share.google/lLA1kAKXRiewU3Jfi They are already doing it. I think the harder part is clearing. Some of these new entrants, I think there are something like 19 of them in the pipeline I'll still have to find that clearing House to agree gre to clear the trades.

-

AI infrastructure as a resource could be compared to oil - do you think Norway's wealth fund is a similarly bad economic idea?

-

Newsom is proposing that “every American owns a stake in the future being built by AI through a national public equity fund that takes a major stake in the new economy.” https://gavinnewsom.substack.com/p/its-time-for-a-national-billionaires. Sanders suggests a much more aggressive plan that's unlikely to gain traction. https://www.nytimes.com/2026/06/01/opinion/artificial-intelligence-bernie-sanders.html. As we know, over the past decade or so, the Republicans have moved away from supporting relatively free markets and have embraced protectionism, pushing the Fed to lower rates, and taking equity stakes in companies that the administration deems vital to the national interest. At the same time, the Democrats, far from a free-market party to begin with, have moved further to the left on economic issues (see the recent NY primary winners). I don’t think proposals like Newsom’s will play well with primary voters who don’t want the government picking winners and losers or subsidizing AI, and I hope other Democratic candidates don’t pick up on this. On the other hand, I am concerned that (in my view) bad economic ideas will proliferate in times like these, particularly once primary season gets underway and if the AI mania is still in full swing by then.

-

Don’t you hold cash/t-bills? Or am I mistaking you with another poster?