Ross812

-

Posts

1,344 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Ross812

-

It usually means something I own is down! No JOE for me, I haven't drank the kool-aid yet...

-

401k loan, Roth conversion ladder, 72t probably in that order for liquidity. At least fill out your tax bracket with a Roth conversion if that's important to you.

-

Damn, a 4 plate DL at 165# is stout. I hit 315 on DL and squat at 180# and started increasing reps instead of adding weight. I messed up a shoulder in September and it still feels like I'll never hit 1/2 plates on press/bench again.

-

The Villages seemed perfect for a second go at living young when I visited.

-

Barbell squats and deadlifts 2-3 times a week reversed all the knee and back pain i had. The human body is amazing.

-

@longlake95 I hate seeing a stock I own pop up on here!

-

I own real estate of the quality I want, surrounded by friends, and in locations where visiting is easy. Day to day spending is controlled by the cost of living in your local area and your affinity for luxury. I've found I don't ski any better behind a 120k nautique than i do behind a 30 year old 20 year old malibu. I can call my eff off nut 5M and buy luxe boat, but I'm happy with 3M and extra time to enjoy what I have. The 3M will likely be worth 10M+ over my remaining 50 to 60 years, but i don't see a huge difference between comfortably poor and comfortable!

-

more First Solar.

-

nibbled on fairfax at 1312

-

Added to fslr.

-

PROSY, FSLR, CPNG

-

@formthirteen agreed. VRSN isn't going to set the world on fire, but i only need 8-9%. It has a high probability of outperforming cash with a low probability of impairment. Its a one foot hurdle.

-

I bought a single share of VRSN. I've read the annual report, what's here, and a few seeking alpha articles. I like the company, but it's too expensive right now.

-

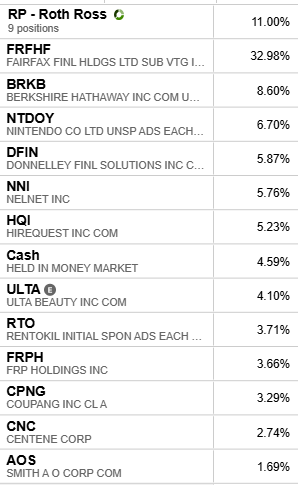

DFIN - picks and shovels of mergers and acquisitions.

DFIN - picks and shovels of mergers and acquisitions. -

Bought SWBI at $10.9 and CNC at $56.9.

-

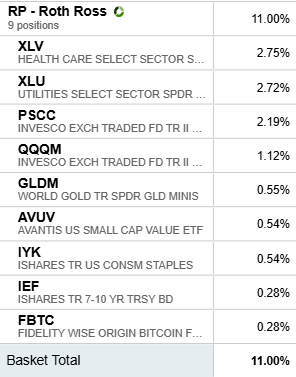

The basket portfolio is low beta and I treat it like cash so i would say I'm 15-16% cash right now.

-

Sold out of USB. TBV of 2.4 and got a nice bump over $50 this passed month. Great return holding for the last 18 months.

-

Sold out of a basket of durables: DE JCI TT CARR GGG OTIS SSD CRH AOS was in that basket and I increased the position substantially.

-

I sold out of GOOGL in multiple accounts. I've been losing some sleep weighing the long term impact of AI search results versus Google search. The DOJ cases mounting just add to the unease and I don't think all of these negatives are priced in compared to October 2022 when I established the position.

-

Added to CNC and ULTA today. Finally got all the cash from my LUV sale back to work.

-

Doubled my CNC position (now a 1.5% position) today at the 52 week low.

-

Adding a little DFIN at $57.

-

Well I have a standing buy order for 1500 shares of FRPH at $29. IBKR filled 500. The other 1000 are on order through Fido. I guess you get what you pay for!

-

Added back to HQI yesterday at $12.90 after selling a bit in the $14s. Also bought a big slug of ULTA today as a starter.

-

Sold out of HSY. The company could still be a good LT pick, but future estimates have come down from both analysts and the company and a 20x PE is too expensive with earnings below $10/share for the next several years.