gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

CIBC raises FFH target to C$2000 from C$1700 fwiw (not much)

-

https://www.reuters.com/business/finance/indias-iifl-finance-raise-242-mln-via-rights-basis-non-convertible-debentures-2024-03-13/

-

I guess the closest we have is Matt Levine's column at Bloomberg. Usually pretty hilarious.

-

Awesome thanks - they obviously hired a talented designer and put a bunch of work into producing it. I figure somewhere there is a big stack of them.

-

Why did so many smart investors miss making a killing on BRK stock?

gfp replied to Viking's topic in Berkshire Hathaway

Yeah, I am definitely not advocating for borrowing against Berkshire or any other stock with margin debt (despite the fact that I sometimes do it - but I'm a big boy and I understand the risks). There are other ways to add leverage to your financial life that are far less dangerous for those that are impatient or whatever. -

I don't think the insurance companies have that type of dividend capacity to send the money to the holdco for repurchases. And, of course, you couldn't successfully tender for 2/3rds of the stock at current prices and get it (or much at all).

-

Why did so many smart investors miss making a killing on BRK stock?

gfp replied to Viking's topic in Berkshire Hathaway

On the subject of Buffett and debt and Berkshire board members making well timed moves with the stock... In 1976 Warren convinced his Mother to sell her 5,272 shares of BRK.A to his sisters Doris & Bertie for $5,440 plus a $100,000 note (to Mom, not the bank or margin). They each got 2,636 A-shares at about $40/share while coming up with only about $2/share in cash. 95% leverage. Kind of puts his stories from this year's annual letter about his sister being one of the greatest investors of all time all on her own into perspective. Charlie Munger did a similarly well-timed masterstroke of estate planning near the absolute bottom of stock prices in the GFC - he got 2,000 A-shares out of his estate, sold to family members in exchange for a promissory note. On 11/20/2008, with BRK.A at $77,500. https://www.sec.gov/Archives/edgar/data/1067983/000118143108063602/xslF345X03/rrd224408.xml -

Why did so many smart investors miss making a killing on BRK stock?

gfp replied to Viking's topic in Berkshire Hathaway

The first Laguna beach house was $150k and I think Warren paid in cash. He had recently shut down the partnership and that gave him $16 million cash but he pretty quickly spent every dime of it buying shares of stock (and presumably the Laguna house). Then he ran out of cash and had to live on only the $50k annual salary Berkshire paid him and some fees he earned from running a pension fund for FMC Corporation (a sort of favor for a friend). A few years later, Warren paid $300k cash for Howie's first farm in Nebraska. Howie paid Warren rent. I'm not sure if that farm was mortgaged or not. -

I finally got it. Fairfax India is having some website issues. This is the full AR not just the letter FIH_-_Annual_Report_2023.pdf

-

I'm looking for India, not FFH

-

Who's got the Fairfax India 2023 letter to upload? I can't seem to access it

-

I'm starting to feel sorry for the old guy. He reads all these newspapers every day - opens up the Journal: Apple fined $2 Billion, about to be sued for antitrust, Pacificorp wildfire verdicts, HomeServices, BHE sued for billions!, Haslam's screwing you! It's rough out there for the deep-pocketed.

-

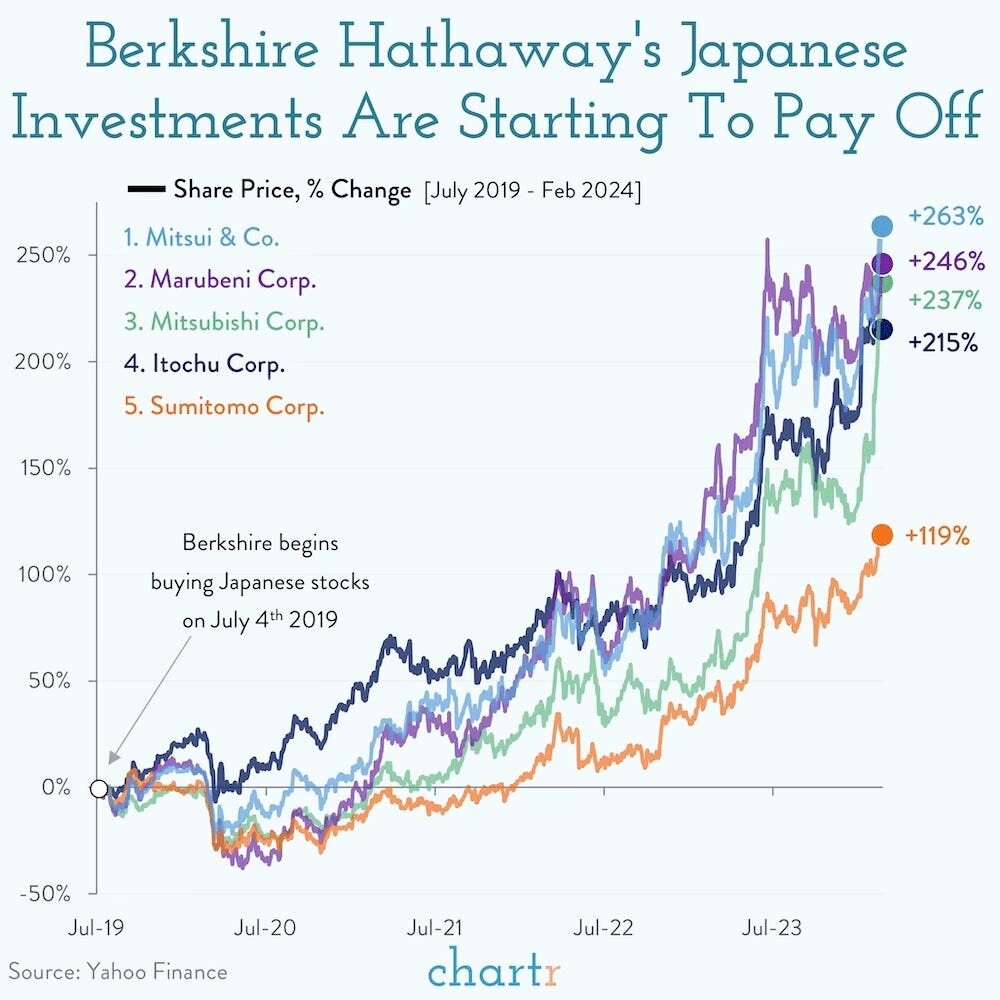

The best I can tell about the Japanese investments is that Berkshire doesn't actually take the JPY they borrow from the bonds and use that to buy the Japanese stocks. They borrow the JPY at the Berkshire Hathaway Inc. (BHI, parent, holdco) level and receive JPY and probably immediately swap almost all of it into US treasury bills. They pay the interest in JPY. Then, separately, they buy shares of the 5 sogo shosha companies inside National Indemnity, an insurance subsidiary of BHI. They transfer National Indemnity's treasury bills and some USD cash to Wallachbeth Capital to settle up their trades.

-

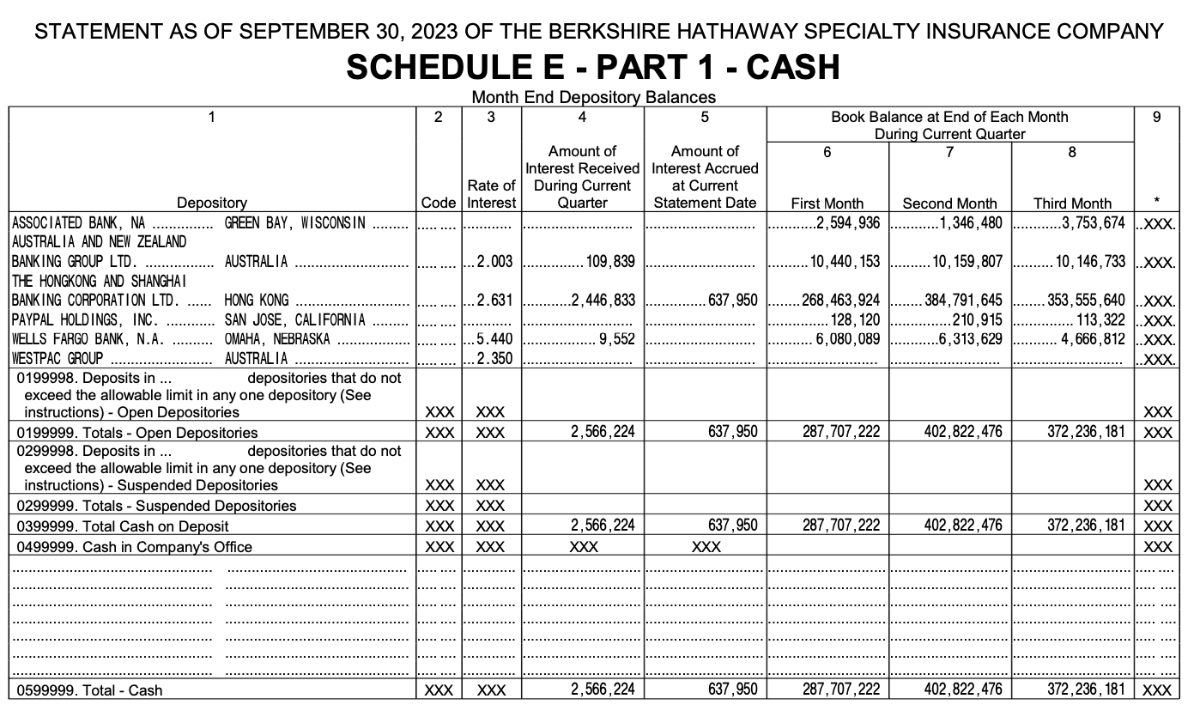

It's kind of funny, @valueinvesting101, you got me checking into various depository / banking relationships for the BRK subsidiaries and Berkshire Hathaway Specialty (the newer, fast growing Excess and Surplus lines primary outfit) actually has a bank account at Paypal Holdings. Surprised me. Everyone has a venmo account I suppose

-

Re: ICICI Bank, that is literally only $1,500 USD worth of bank deposit cash sitting in the bank. I don't know where Berkshire "custodies" the Japanese shares but it is probably a division of Citi (or BNY). The shares are purchased using Berkshire's go-to large block trader, Wallachbeth Capital (which is who Warren uses for almost all large trades for the last several years). I have no idea which bank wires the JPY to Wallachbeth to settle up since the bank account balances are just shown in their US Dollar equivalents here. Maybe I could tell by looking at past filings right after a Yen bond sale was completed but I've never wondered myself. *edit: I looked around and none of the Berkshire insurance subsidiaries have a banking relationship with a Japanese bank. I don't know what they are delivering to Wallachbeth to settle up or from where. Might come from Wells but the main National Indemnity Wells Fargo bank account pays t-bill-like interest so there isn't any JPY in there. FWIW, as far as I can tell Ted Weschler tends to trade through this 'woman-owned' broker dealer - "Glen Eagle Wealth" https://gleneagleadv.com/institutional-markets

-

How many hits for FOMO (not counting this one)?

-

I assume the chart is translating back to US dollars but I didn't make it or know the data source. Chart source for me was https://www.kingswell.io

-

Like Deja Vu with IIFL securities getting in trouble last year. Glad FIH has sold some IIFL finance shares. We'll see if this one works out like the IIFL securities issues with a slap on the wrist.

-

Well Charlie also had this quote on Warren's investments in Japan, "It was like having God just opening a chest and just pouring money into it." I'm not even sure I can calculate the return on investment because the equity sliver was so small, the carry was so positive and the debt used to float the purchases and hedge the currency was so profitable. If we pencil in that we used insurance float for the tiny "equity" sliver then I guess this is as close to warren giving a master class on free money as we will get. h/t kingswell newsletter for the chart

-

I mean, it is a crypto thread on a value investing message board so not super surprising.

-

Like turning a battleship... I have other filings for them but there isn't a lot of undisclosed equity trading that will make headlines. Most of the selling we knew about from the first three quarters and SEC disclosures. Whatever "secret" buying is going on is being hidden in both Harney Investment Trust (National Indemnity) and Dewey Investment Trust (Columbia Insurance).

-

This happens to me all the time - often in securities that “officially” didn’t trade at all that day. I think there are so many places other than the stock exchange that match orders that these trades get matched - and appear to not count toward official volume. Also an odd lot bid above the current bid will usually not move the posted bid or show up as the best bid. I use this quirk a lot to get shares in difficult to buy stocks where I don’t want to move the bid and just get stepped in front of by a Penny again

-

Well finally somebody lays it out in a way I can understand it

-

Look at Spek with the Johnny Cash picture! Awesome. I never noticed that before. I don't even know how to make my G a photo LOL I like to try to say "cash" with a thick bruce berkowitz accent but its like Christopher Walken for me - a very hard accent to get right.

-

It's funny because Trump's main criticism of Powell (who he appointed of course) was essentially that he wasn't political enough. Trump wanted low rates, Powell wanted to maintain Fed independence. There is zero chance of the US going back to a gold-backed currency even if that is something that Donald Trump wanted, which I'm sure he doesn't. Elasticity is a (necessary) feature not a problem.