gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

So my entire point.

-

Yeah I wasn’t at all saying that Lauren wasn’t qualified to be on the board and makes a good board member. I was saying a member of the board of directors shouldn’t be pitching the stock as a Berkshire from an earlier date. We do those comparisons here but we are not board members. Prem would NEVER do that. There’s no comparison to Wally Weitz because of where BRK is today but if you saw a Berkshire board member pitching it as “Home Depot but 30 years ago” at an investor conference there would be some eye rolls… Davis going on a podcast interview talking about the board’s responsibility to maintain the culture after Warren or dividend policy when excess cash overwhelms is not remotely similar to Ackman or Lauren putting together “the next Berkshire Hathaway” slides as a pitch for a stock they own a ton of. I think if it was any other company you fan-boys would see it

-

The one thing Prem would never have done with those same slides at the AGM was compare Fairfax to Berkshire and suggest a similar outcome to Berkshire from an earlier point in time. As shareholders, we can do that comparison, but a board member should not be doing that "here's your chance to own the next Berkshire" sales pitch and I think its just as shady when Ackman does it with his "modern-day Berkshire" while he feverishly reads "Ajit Jain for dummies" and buys an insurance company. Buy insurance company... Invest surplus in equities... PROFIT! Graveyard is full of hedge funds who had that game plan. Showing the results of the past is fine - they should be proud of their track record. Lauren's presentation was fine, just not appropriate for a board member of the company. If she were just a fund manager that had a long term position in the stock it's totally fair game to talk her book / pitch her favorite holdings - that's what all those people do at conferences. Raise money for Cancer? Pump a new undisclosed holding.. Again, Ackman figured out the playbook many years ago at Sohn and similar hedge fund events.

-

Does anybody else think it is completely inappropriate for a member of the board of directors to give a straight up stock pitch presentation? Why is she trying to convince people to invest in Fairfax? Never seen it before and I hope I never see it again.

-

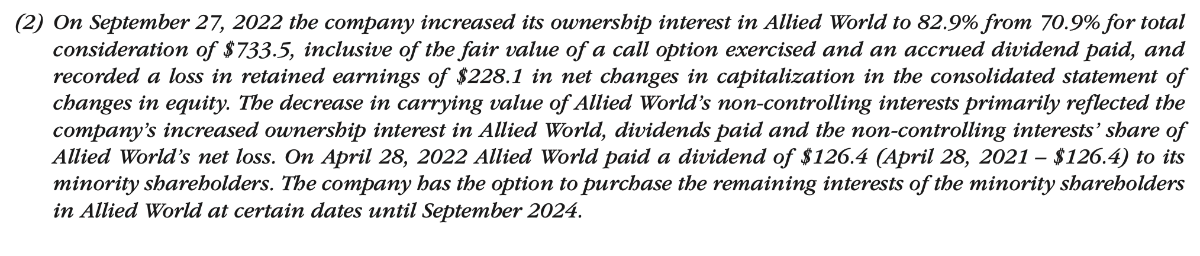

In 2022 they paid $733.5m to extinguish 12% non-controlling interest of Allied World that was on their books for something less than $733.5m (I don't know how much less, because the $733.5m included a partial accrued dividend to that date) and they took a $228.1m non-cash accounting charge (not through the income statement, through the equity statement - directly to retained earnings). So Allied was carried at X valuation on Fairfax's books... And Fairfax paid a premium to X valuation to retire the 12% minority interest. Part of that payment was the accrued dividend but they paid a premium to their carrying value for the 12% and took a loss because they didn't write up what they already owned (they wrote-down what they had just paid for)

-

But there was a loss recognized on excess of $$$ paid over carrying value on earlier Allied World minority interest buy outs right? As in, some premium to straight book value? Even old man Buffett requires 8% annually plus a one-time 10% kicker to get out of your preferred. We all learned from the best right?

-

By virtue of it being a call option that Fairfax holds to acquire the remaining 16.6% of Allied World, it is not mandatory that they execute it before it expires (it is not a put option held by OMERS and the others). The call option might be at a price that is better than what letting it expire would result in, so Fairfax may have every incentive to exercise it if they have the capital. They may also be able to do a partial exercise in connection with a re-negotiation for another option on a remaining minority interest. These minority interest financings are more like preferred equity financing than pure equity ownership by OMERS et al - if the implied rate OMERS is earning over time is satisfactory for them, they may be content to let it ride further. Especially if its better than what they could get, risk adjusted, on something else in today's market. The original "call option" to acquire the remainder of Allied World expired in September 2024 but Fairfax bought some of the minority interest and negotiated a 2-year extension of the "call option" on the remainder. It's nice to have fair and friendly partners and it swings both ways if you live by that golden rule don't ya know... What do they need to come up with to fully close out the non-controlling interest? Call it $2 Billion cash? Does it result in an accounting loss since they will be paying a premium over the carrying value of Allied World on their books or does it result in a write-up of the other 83.4% of Allied World they have on their books at a lower valuation?

-

Restaurant stocks (MCD, PTLO, WEN, CAVA, CMG, etc)

gfp replied to ratiman's topic in General Discussion

Steak n Shake Q1 2026 +10% 2025 FY +10.2% 2024 FY +6.4% -

They have renewed their ASPP (Automatic Securities Purchase Plan) alongside their NCIB (Normal Course Issuer Bid) each year. Think of an ASPP as being similar to a 10b5-1 plan in the USA in that you have a pre-defined set of rules and a broker executes it on your behalf - even during "blackout" periods. Most recent announcement (scroll way down for ASPP) https://www.globenewswire.com/news-release/2025/09/26/3156967/0/en/Intention-to-Make-a-Normal-Course-Issuer-Bid-for-Subordinate-Voting-Shares-and-Preferred-Shares.html

-

As Warren always liked to remind people, and it's probably true for Ajit as well, "I buy expensive suits. They just look cheap on me." Warren and Ajit operate on the telephone. They can do it in a sweatsuit for all I care

-

Everything that was reported in the FIH.u earnings release was already known by the market, right? Sanmar exit had been released, mark to market losses on public equities was known. Since last week they announced a material deal with IIFL Capital.

-

Thanks - so what I was reading as rumors of preferred shares was probably actually accurately describing a "preferential allotment" of common stock.

-

It's interesting as some of the early rumors hinted at a partial preferred equity structure for the new investment. I wonder why 51% was so important to them on this one? Either way, less of companies like Sanmar and more of companies like IIFL Capital should be a good recipe going forward.

-

new General Counsel bought some shares today https://www.sec.gov/Archives/edgar/data/1713777/000119312526209661/xslF345X03/ownership.xml

-

I Need a Laugh. Tell me a Joke. Keep em PC.

gfp replied to doughishere's topic in General Discussion

Honestly that interview was pretty embarrassing for Sorkin and Becky. They can count to $29 billion of cash. He is proposing half cash, half stock. So $29 billion of stock issuance gets you to $58 Billion. His opening offer is less than that. Sorkin and Becky must not understand that stock issuance isn't limited to your current market cap? Obviously GME would have to increase authorized shares but that isn't some mystic magic trick. -

Repurchases are very likely to resume tomorrow FWIW.

-

It isn't two types of TRS on their own shares. It is just timing differences on reset / remeasurement dates. A "realized gain" is actual cash that came their way. Unrealized movements are in between resets / the movement of cash. Separately there are changes to the cash pledged as collateral that shows up as 200 million or so of the holding company's cash. (this is cash they show on their holding company balance sheet but don't have access to and could be required to increase the size of - think of it as 'restricted cash' or a cash bond posted or whatever - they still own the tbills, they've just been posted as collateral to minimize the risk to their counterparty - a key difference from terms available to some pre-2009 when Buffett wrote un-collateralized naked puts) The swaps are cash collateralized total return swaps that reset (cash actually moves) either monthly or quarterly. That's why you can have a "realized gain" of $11.8 million in the same period where you had net losses of $341.8m and "unrealized losses" of $353.6 million. Realized means cash moved and unrealized means changes between remeasurement dates. There are multiple contracts in different amounts with different measurement dates.

-

Berkshire's 13F will be interesting this go round as it should make it fairly clear which positions were chosen by Todd Combs.

-

Yeah Ingrid is great (babyb) and as an added bonus she is a real person who lives and breathes (and puns!) I stopped going to that shrewdm site a while ago and forgot it still existed.

-

Yes, I criticized the AI for not phrasing it as a move towards normalization of the CR and scolded it on a few other issues. It says it will remember my corrections but I know it won't. It won't even be the same model this time next quarter

-

In case anybody is interested in this Opus 4.7 summary I had it prepare from the 10Q, I will copy and paste it below. It made some errors but minor. ------------ Berkshire Hathaway 1Q 2026 10-Q — Deep Read 1. Repurchases (Q1 2026 and subsequent) Q1 2026 repurchases (Item 2, Part II): Class A: 33 shares at avg $729,701.17 — all in March Class B: 431,462 shares at avg $486.92 — all in March Total: ~$235 million, or roughly 321 A-equivalent shares That's a token amount on a $1 trillion+ company — but the signal is what's notable. The last reported buyback before this was Q1 2024. Berkshire bought back zero stock for all of 2025. The fact that Greg Abel (now CEO as of 1/1/26) flipped the switch back on in March, even at a tiny scale, is the story. The $729,701 average A price puts the buyback meaningfully below quarter-end book value. [AI MADE AN ERROR HERE] Subsequent to quarter-end: Comparing the 3/31/26 share counts (Note 18) against the 4/14/26 cover-page counts: Class A went from 505,951 → 505,697 (down 254) Class B went from 1,397,927,677 → 1,398,308,677 (up 381,000) 254 × 1,500 = 381,000 — i.e., the Class A drop is fully explained by A→B conversions No additional repurchases occurred between 3/31/26 and 4/14/26. The Q1 buyback was a one-shot in March. (CNBC headlines suggest Abel personally bought stock too, but the 10-Q only covers company repurchases.) 2. Book Value Per Share & P/B Ratio Item Value Berkshire shareholders' equity (excl. NCI of $2,269M) $727,181 million Equivalent Class A shares outstanding 3/31/26 1,437,903 Book value per Class A share $505,723 Book value per Class B share $337.15 BRK.A price (close, 5/1/26) $710,300 P/B ratio (Class A) 1.405x BRK.B price (close, 5/1/26) $473.01 P/B ratio (Class B) 1.403x A P/B around 1.40x is below the post-2022 trading range and is the kind of multiple where Buffett historically said he'd be "aggressive" on buybacks. In this context, the resumption of buybacks at an average BRK.A price of $729,701 (~1.44x book at the 12/31/25 BV per share of ~$498,839) makes sense. 3. Under-the-Radar Disclosures Worth Highlighting a) The Tokio Marine deal — buried in BHRG section. On 3/23/26, NICO entered a whole-account quota-share reinsurance agreement with Tokio Marine Holdings subsidiaries assuming "a portion of the net non-life premiums written and related losses and expenses…on risks attaching over a ten-year term commencing April 1, 2026." Berkshire says it "is expected to generate meaningful premium volumes over its term." This is a major new long-duration reinsurance relationship — barely flagged in one paragraph. b) PacifiCorp wildfire reversal. On April 8, 2026 (after quarter-end), the Oregon Court of Appeals reversed and remanded the entire James Phase I liability verdict, finding the trial court's "evidence applies to all class members" jury instruction was prejudicial error. The appeals court also explicitly said the trial court can reconsider class certification. Phase II trials were stayed April 9 and the parties were ordered to mandatory mediation. The $719M in posted bonds "could eventually be discharged." Cumulative wildfire accrual remains $2.9B with $577M unpaid at 3/31; PacifiCorp paid $584M in Q1 settlements alone. c) PacifiCorp selling off Washington operations. On 2/15/26, PacifiCorp signed an Asset Purchase and Service Area Transfer Agreement to sell its Washington operations to Portland General Electric for $1.9 billion in cash, expected to close 1H 2027. Continued shrinkage of PacifiCorp's wildfire-exposed footprint. d) Massive Treasury bill settlement timing oddity. Unsettled T-bill purchases were $17.2 billion at 3/31/26 vs. $167 million at 12/31/25. This goes through both the asset side (in the $339B short-term Treasuries figure) and as a payable on the liability side. It means quarter-end "cash + Treasuries" optics are inflated by ~$17B that effectively cleared days later. On a settled basis, the cash + T-bill pile is ~$373.5B (per MD&A), not the $390B+ implied by the gross figures. e) Tax rate normalized hard. Effective tax rate jumped to 17.4% from 9.2% a year ago. The 9.2% in Q1 25 was distorted by the big investment loss; the 17.4% is closer to a normal run-rate now that pre-tax earnings include a $325M pre-tax FX gain (vs. a $936M FX loss in 1Q25), which together with much smaller equity mark-to-market losses made the denominator bigger. f) Equity portfolio rotation continues but slower. Berkshire was still a net seller of equities ($24.1B sales vs. $15.9B purchases = $8.2B net divestiture), but the gap shrank dramatically. In 1Q25, sales were only $4.7B. The big change: Berkshire is buying again — $15.9B in purchases vs. $3.2B a year ago. Tax gains on equity sales were $7.2B in Q1 (vs. $3.1B in Q1 25), implying continued trimming of long-held low-basis positions. g) "Banks, insurance and finance" portfolio shrunk dramatically. This category fell from $104.1B fair value at 12/31/25 to $84.6B at 3/31/26, with cost basis dropping $769M. Net unrealized gains in the bucket dropped ~$18.8B. Some of this is mark-to-market (BAC down, AmEx flat-ish), but cost basis reduction signals continued bank-stock selling. Meanwhile, "Commercial, industrial and other" jumped from $98.7B to $112.4B fair value with cost basis up $3.0B — net buying in industrials/Chevron/Apple bucket. [AI MADE AN ERROR, APPLE IS IN CONSUMER PRODUCTS, NOT C, I, & O] h) Apple still in "Consumer products" but cost basis declining. Consumer products bucket cost basis dropped from $11.9B to $8.8B — a ~$3B sale, consistent with continued Apple trimming. i) Float essentially flat at $176.9B (only +$500M Q/Q). Growth has stalled. j) GEICO's loss ratio meaningfully deteriorated. Loss ratio 73.9% vs. 69.0% — bodily injury frequency up 5-7%, severity up 12-14%. Underwriting expenses up 29.3% on "increased policy acquisition-related expenses" — translation: GEICO is spending heavily to grow again. Net effect: GEICO underwriting profit fell from $2.17B → $1.42B (-35%). That's a big reversal of the GEICO turnaround story. k) Goodwill impairment risk flagged. Four reporting units have estimated fair value not exceeding carrying value by at least 20%. Aggregate fair value $27.7B vs. carrying value $26.2B with $9.2B in goodwill at risk. That's a thin margin if conditions deteriorate. (This was disclosed in the 10-K too, but worth tracking.) l) The Kraft Heinz overhang persists. Carrying value still exceeds fair value by $1.4B (15.7% of carrying value).Berkshire concluded no impairment, but explicitly notes its expectations could change. The Kraft Heinz fair value actually dropped Q/Q from $7.9B to $7.3B even as Berkshire held the carrying value. m) Pilot swung to a $50M pre-tax LOSS vs. $168M profit a year ago — a $218M swing on a 7.8% revenue increase. Cause: hedging losses on rising fuel prices got recognized in earnings, while the offsetting inventory gains are deferred until sold. This is a timing artifact that should reverse. n) Mass complaints in the James case. 1,760 individual class members have filed nine mass complaints, each seeking $5M economic + $25M noneconomic + 25% punitive damages per plaintiff. Even with the appeals victory, the sheer number of claimants is staggering. o) Yen debt strategy continues. ¥272.3B ($1.7B) of new senior notes issued in April 2026 at 2.4% weighted average, maturities to 2056 — replacing ¥133.9B of maturing notes. Still funding the Japan trading-house position with cheap yen debt. p) HomeServices Texas DTPA exposure. Two pending antitrust cases include Texas state law deceptive trade practices claims for ~$9 billion in damages (separate from the $250M Burnett settlement that's still on appeal at the 8th Circuit). 4. Why Each Operating Business Performed the Way It Did Insurance Underwriting (after-tax: $1.72B vs. $1.34B, +28.5%) GEICO ($1.42B vs. $2.17B pre-tax, -34.8% hurt by higher private passenger auto claim frequencies (BI up 5-7%, PD/collision up 2-4%) and severities (BI up 12-14%) AND a 29.3% jump in underwriting expenses tied to policy acquisition. Loss ratio 73.9% vs. 69.0%; expense ratio 13.4% vs. 10.8%. Combined ratio worsened ~750 bps. BH Primary ($476M vs. $(144M) loss): swing driven by no Q1 catastrophes (vs. ~$300M from So Cal wildfires in Q1 25) and $176M of favorable prior-year reserve releases (vs. $212M of adverse development a year ago). Premium growth modest with RSUI down 14% (property), NICO Primary down 7% (commercial auto), offset by MedPro +7% and BHSI +3%. BHRG P&C ($637M vs. $68M): again, zero Q1 catastrophes (vs. $770M from So Cal wildfires in Q1 25). Premiums actually declined 6.2% on lower property reinsurance volumes due to "increased competition and lower rates" — a clear soft market signal. $260M of favorable PYD on property covers. BHRG Life/Health: $126M vs. $70M — gains in France, Asia, UK; partial offset by Australia decline. Retro reinsurance: $246M loss (vs. $209M) — purely deferred charge accretion. Insurance Investment Income (after-tax: $2.68B vs. $2.89B, -7.4%) Pre-tax interest income fell 10.3% — the explicit reason given is lower interest rates. Dividend income essentially flat. BNSF (after-tax: $1.38B vs. $1.21B, +13.4%) Volume +2.2%, revenue per car +2.8%, fuel surcharge benefit. The drivers: Ag/Energy +14.8% revenue (grain, petroleum fuels, oilseeds); Industrial +2.3% (despite housing softness hurting plastics/building products); Coal +1.1% (utility retirements offset by higher demand from elevated nat-gas prices); Consumer products flat (intl intermodal up). Operating ratio improved from 67.9% to 65.6% — fuel efficiency offset higher prices, productivity offset wage inflation. BHE (after-tax: $1.11B vs. $1.10B, +1.5%) — composition changed dramatically U.S. utilities -16.1% (PacifiCorp/MEC/NV Energy): higher operating costs (vegetation management, wildfire prevention, plant maintenance, insurance, technology) and higher interest expense; less production tax credit benefit. Natural gas pipelines +24.2%: rate case benefits and higher LNG variable revenue from cold Q1 weather. Other energy -26.5%: Northern Powergrid hurt by lower UK distribution tariffs from inflation adjustments + higher interest expense. Real estate brokerage: still losing money; "limited availability of homes for sale and high home prices" cited. Manufacturing, Service & Retailing (after-tax: $3.20B vs. $3.06B, +4.5%) Manufacturing pre-tax +12.6%: Industrial products +22.1% (revenue +23.6% boosted by OxyChem, Bell Labs): PCC +32.9% pre-tax: aerospace +9.4%, IGT +18.9%; lapping a Q1 25 fasteners-facility fire; mix improvements. Lubrizol +8.1%: volume + no-repeat of restructuring; raw material inflation noted as a Q2 headwind. Marmon +1.3%: mostly flat; copper spreads helped Plumbing/Electrical, Rail & Leasing weak. IMC +41.9%: customers accelerating purchases (likely tariff/inflation pull-forward); Berkshire explicitly warns this won't continue. OxyChem (new): small pre-tax loss in Q1 due to acquisition accounting amortization plus higher maintenance/utility/property tax/material costs. Building products -9.2% (revenue -2.9%): Clayton home unit sales -9.7% volumes, slow housing market. Clayton financial services up 9.6% on higher rates and balances. Consumer products +29.6% (revenue -1.5%): Forest River SG&A discipline, Duracell got more advanced manufacturing PTC, Brooks gains; offset by Fruit of the Loom exit of unprofitable lines and Garan/Jazwares declines. Service & Retailing: Service +21.1% pre-tax ($785M vs. $648M): TTI revenue +26.2% (customers responding to "potential further price increases and supply chain concerns" — translation: tariff front-running); aviation services +11.8% on more aircraft and hours; IPS +23.7% on life sciences and data center construction. McLane -20.4%: retail sales down 8.0% (net customer losses); restaurant business up; lower gross margins. Retailing +1.0%: BHA +3.7% (service contracts) on lower vehicle sales (-4.3%); other retailers down 11.9% on "higher economic uncertainty and changes in consumer confidence." Pilot -129.8%: hedging losses recognized as fuel prices rose, with offsetting inventory gains deferred — a timing mismatch that should reverse. 5. Other Items Worth Flagging OxyChem deal closed 1/2/26 for ~$9.5B, with assets preliminarily $10.8B and liabilities $1.3B — implying ~$0 of goodwill/intangibles bargain or near-asset-value purchase price. Occidental retained legacy environmental liabilities, which is a meaningful protective term. OECD Pillar Two: Berkshire says it does not currently expect material impact, citing the January 2026 OECD safe harbor for U.S.-parented multinationals. Capex guidance: BHE + BNSF expect ~$12.4B more in capex over the rest of 2026. Five largest equity holdings unchanged in identity: AmEx, Apple, BAC, Coca-Cola, Chevron — but down from 65% to 61% of the equity portfolio, suggesting some diversification. AmEx ownership at 22.2% (151.6M shares), still above the typical 20% threshold but still not equity-method due to Fed passivity commitments. NICO bankruptcy/environmental settlement: $535M to bankruptcy estate pending court approval; CDESA filed 4/3/26 with EPA and state environmental agencies — these should clean up legacy non-insurance affiliate environmental exposure once approved. Consolidated cash + T-bills (net of payables): $373.5B at 3/31. Continues to sit near record levels even with the $9.5B OxyChem outlay. Bottom Line The headline "earnings doubled YoY" is largely a function of (a) no significant catastrophes vs. $1.1B+ from the So Cal wildfires in Q1 25 and (b) FX swinging from a $713M after-tax loss to a $249M gain on yen/euro debt. Underlying operating performance was mixed: GEICO's combined ratio deteriorated meaningfully, U.S. utilities are absorbing higher wildfire-related costs, the property reinsurance market is softening, and the housing complex (Clayton, building products, HomeServices, retailing) continues to struggle. The bright spots are BNSF efficiency, natural gas pipelines, PCC aerospace, and TTI. The two most important under-the-radar items are (1) the resumption of buybacks under Abel (tiny but symbolically meaningful, and consistent with the ~1.4x P/B), and (2) the Tokio Marine 10-year quota share as a major new long-duration reinsurance relationship. The PacifiCorp Phase I reversal is the biggest post-quarter event, materially de-risking what had been one of Berkshire's largest open contingent exposures.

-

Why didn't your 1630 get filled? I got filled at 1624

-

Update this morning from Irrational Analysis - more a Semiconductor blog than a strictly AI blog, but always worth a read and highly entertaining. https://irrationalanalysis.substack.com/p/market-memo-intc-qcom-wolf-on-nvts?utm_source=post-email-title&publication_id=1509468&post_id=195937503&utm_campaign=email-post-title&isFreemail=true&r=oqhe5&triedRedirect=true&utm_medium=email

-

No I don't think there is a refund mechanism for that type of thing in the US or Canada. A few years carry back and something like 20 years carry forward if they truly had no income to offset it. But it wouldn't lose its deductibility

-

Fairfax Holding company doesn't need taxable income from the TRS in order to deduct the interest expense from borrowings at the holdco. Even though operating subsidiary dividends to the Holdco are generally fully deductible and not taxed, they still qualify as income that allows the interest expense to be deducted. The money was borrowed to create income from a property or business, which makes the interest deductible - despite the "income" also ending up being tax free as subsidiary dividends of income that was already taxed at the subsidiary level. To other posters' points, the TRS is not equivalent to repurchasing shares at all. If a profit is earned on the TRS, it sends money to the company. A repurchase sends money out of the corporation, basically permanently - like a slow motion liquidation. A successful TRS increases capital, all buybacks decrease capital (whether they are later thought of a being 'profitable' or not).