gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

same doctor. must be in it for that fat dividend.

-

And to everyone saying, "doctors don't make $95 million" or whatever, I just want to point out that I'm talking about doctors who also found the last Berkshire Hathaway and are only now looking for the next Berkshire Hathaway because their guy is hanging up his spurs.

-

1200 bottle at your age! Y'all are crazy. currently drinking an espolon blanco on ice splash of water - affordable and sensible

-

Yeah I agree with all of this and I am using it more and more every day. I just subscribed to Gemini Pro (it's on sale right now for like $100 for a year and you can invite several people to share the account if your family is into it. Mine isn't). You can use @YouTube extension to summarize a podcast video, focus on specific questions, find stuff it would take you a while to find instantly. You can upload around 1500 pages of files and ask it anything you want. Devils advocate / getting into both sides of an argument really thoroughly. It even had full access to everything said at Bay County (FL) board of commissioners meetings because it has access to all the minutes of every meeting. Just crazy how quickly these AI agents are progressing to a full on jr. analyst where it was basically a LLM parlor trick not that long ago. I'm still learning about "Gems" which are basically little macros you can write to do the same thing to different sources over time. I'm not as in to voice mode but a lot of people talk to Gemini or Grok and debate things out verbally when they are driving or taking a walk. I'm not there yet. A lot of Tesla drivers are talking to Grok instead of listening to music I guess.

-

That is always something to sell to finance a great deal. As Warren always said - 'we'll find the cash!' It's the great ideas that are scarce

-

POTUS leaked the Jobs numbers 12 hours before the report... https://truthsocial.com/@realDonaldTrump/posts/115862513677602476

-

You know how it goes. Some doctor reads a bloomberg article about the next Berkshire Hathaway but he has to go to work early so he puts in a market order for $95 million before the market opens and starts his shift. Checks back after work to see how the execution went.

-

Little by little the story is getting picked up by the mainstream.

-

Everyone everywhere hates it completely. Same as it ever was

-

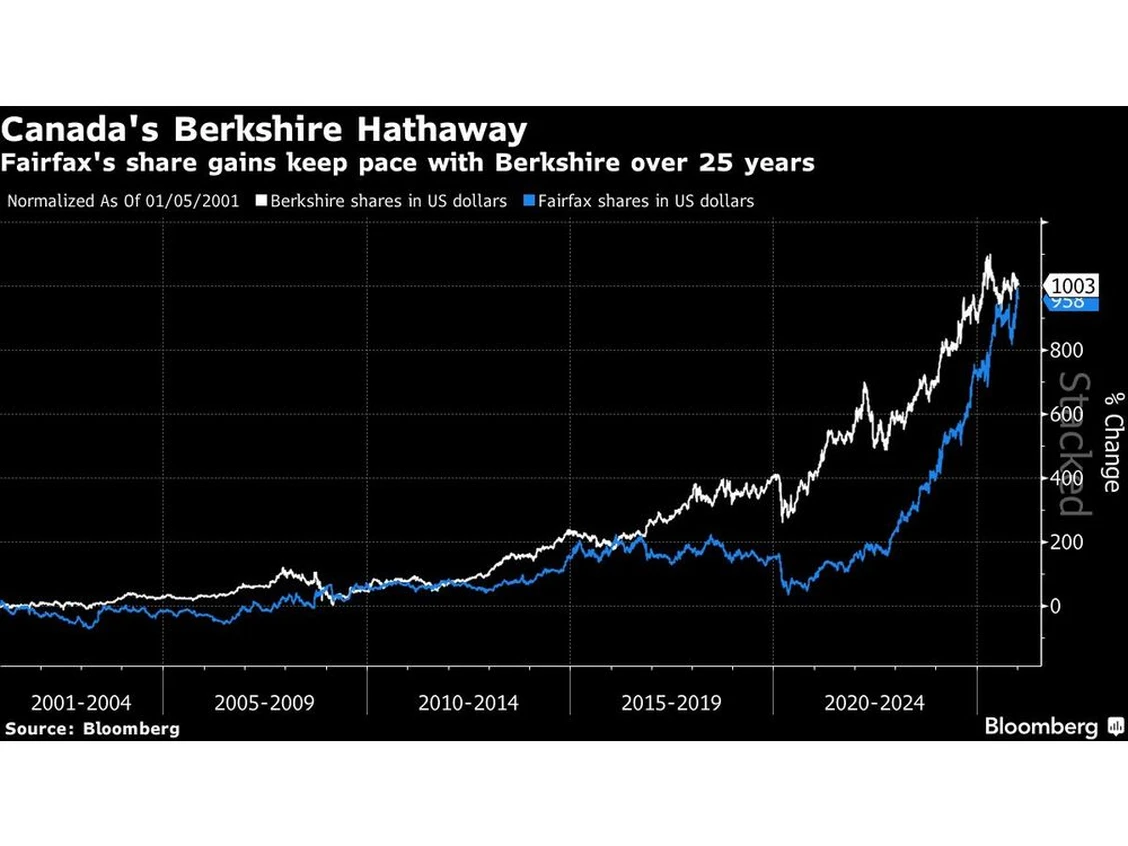

Yeah, Prem owns just over half of Sixy Two and Sixty Two owns about 1.6 million shares plus Prem owns 467,196 shares himself. Half of 1.6 million is 799,310 plus 467,196 gets you to 1,266,506 and Fairfax las reported a share count of 21.221 million shares so that spits out less than 6% economic ownership of Fairfax.

-

I am selling Biglari Holdings class A stock.

-

I asked Gemini for an update on JCP Fund V ---------- JAB Consumer Partners (JCP) Fund V (often referred to as JCP V) is a $5 billion buyout fund that closed in 2022. It represents a significant shift in JAB’s strategy, moving from a primary focus on coffee and fast-casual restaurants toward a massive expansion into Pet Insurance and Insurance/Financial Services. Because JCP V co-invests alongside JAB Holding Company, its specific portfolio is integrated into JAB's broader "platforms."1 Here are the key investments made or held by Fund V: 1. The Pet Insurance "Powerhouse" JCP V was the primary vehicle used to build JAB’s Independence Pet Group (IPG) and Pinnacle Pet Group.2 This is currently the fund's most active investment area. Fairfax Financial Assets (2022): A cornerstone deal for Fund V was the $1.4 billion acquisition of Fairfax Financial’s pet insurance interests, including Crum & Forster Pet Insurance Group and Pethealth Inc.3(which includes the 24Petwatch registry). As part of this deal, Fairfax itself became a limited partner in JCP V.4 +1 Embrace Pet Insurance (2023): JCP V acquired a majority stake in Embrace, a leading provider in the US. Pumpkin & Spot Pet Insurance (2023/2024): Acquisitions of these high-growth, tech-forward pet insurance brands were folded into the Independence Pet Holdings platform.5 Pets Best (2024): Acquired from Synchrony Financial, further consolidating JAB's position as a top-three player in the global pet insurance market. European Expansion (Pinnacle Pet Group): Fund V capital was used for the acquisition of Agila(Germany), Veterfina, and AssurO’Poil (France) to build a dominant European pet insurance presence. 2. Insurance and Financial Services (JAB 3.0) In 2024 and 2025, Fund V began moving JAB into broader insurance sectors beyond pets, a phase JAB calls "JAB 3.0." Prosperity Life Group (2025): JAB (via JCP V) announced the acquisition of Prosperity Life, marking a major entry into the life insurance and individual annuity markets. Columbian Mutual Life (Late 2025): Most recently, JAB announced an agreement to acquire Columbian Mutual as a centerpiece for a new insurance rehabilitation and growth plan.6 3. Core Consumer Holdings While JCP V is heavily weighted toward insurance, it also holds co-investment stakes in JAB’s traditional "staple" companies, which are currently being prepared for liquidity events: Petcare (NVA): JCP V holds a significant interest in National Veterinary Associates (NVA) and Ethos. JAB has announced plans to IPO the specialty and emergency portions of NVA in 2026. Panera Brands: This includes Panera Bread, Caribou Coffee, and Einstein Bros. Bagels. Like NVA, Panera Brands is being prepared for a public listing (expected 2025/2026). JDE Peet’s: In late 2024, JAB significantly increased its stake in JDE Peet’s by acquiring Mondelez’s remaining shares, some of which are managed through JCP vehicles to increase the "free float" of the stock.7 Summary Table of JCP Fund V Assets Sector Key Portfolio Companies Recent Notable Action Pet Insurance Independence Pet, Pinnacle, Pets Best, Figo, Pumpkin Aggressive "roll-up" of the US and EU markets. Life Insurance Prosperity Life Group, Columbian Mutual Newest platform; diversifying away from retail. Pet Health NVA, Ethos, Sage, Pet Labs Platform Expected IPO of specialty division in 2026. Indulgence Krispy Kreme, Insomnia Cookies Sold majority of Insomnia Cookies in 2024. Would you like more details on the specific terms of the Prosperity Life acquisition or the upcoming IPO timelines for NVA and Panera?

-

That's the problem with an investment that still trades at a 4.95% earnings yield on suspect GAAP earnings after a huge decline and disconnect into "value territory" - is anybody getting rich buying risky 4.95% earnings yields? I guess some are but not on downslope of the story. (if you are paying me 4.95% you better be the sovereign issuer of the paper)

-

Warren's got a new favorite sorry Apple you old news

-

The share price traded above $20 twice in the last 12 months. People on this thread make it sound like this hasn't traded anywhere near book value in ages. There are worse things to deal with as an investor than multiple opportunities to buy and multiple opportunities to sell.

-

This is what Gemini thinks about it -

-

Economic Times is reporting 30-40% stake is possible with a tender offer to other minority shareholders. https://economictimes.indiatimes.com/industry/banking/finance/tpg-nears-deal-to-buy-30-40-stake-in-nirmal-jains-iifl-capital-open-offer-likely/articleshow/126381174.cms?from=mdr

-

They're gonna pay Greg $25 million cash salary https://www.sec.gov/ix?doc=/Archives/edgar/data/1067983/000119312526004727/d32284d8ka.htm

-

There was also a strange large trade on FIH.U at today's open. 45k shares traded around the open? weird

-

There has been a weird open on FFH for several days in a row.

-

just a quick comment on this line of thinking - the combined ratio is calculated on earned premium. It does not invert to a return on float. Earned premium can be close to the amount of float but they aren’t the same. Offhand I think they are at least $10B apart at FFH

-

The only detail I have seen is that he had worked at a Transformer company that Charlie was involved with in the 50's in Southern California and had that reputation as a turnaround specialist. Charlie introduced him to Warren. From a 2003 interview when he was in his 80's: Between 1959 and early 1962, I worked as a consultant for a very successful turnaround specialist here in Los Angeles, and in so doing gained considerable expertise in assisting companies in distress. Charlie introduced me to Warren in early April 1962 and after some discussing regarding his need for an operating manager for a farm machining company he owned in Nebraska, we very quickly came to a mutual employment agreement and I departed for Beatrice two days later. More stuff here on their idea to raise the price of replacement parts that were proprietary (could only be bought from them) and turn $300k worth of inventory into $2m of revenue https://www.gurufocus.com/news/369605/warren-buffett-harry-bottle-and-the-story-of-dempster-mill?utm_source=chatgpt.com

-

OxyChem deal closed https://www.oxy.com/news/news-releases/occidental-completes-sale-of-oxychem/ https://www.berkshirehathaway.com/news/jan0226.pdf

-

I don't think QE will be effective at driving down long rates more than a few basis points, all else equal. If they want to target MBS spreads or something like that they can have an impact on that specific spread but long rates are going to be set off growth and inflation expectations. The best way to get low long term treasury rates is to have a horrible economy.