Crip1

-

Posts

749 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by Crip1

-

People want to partner with us...India is ripe with opportunity...the government will privatize business...Poseidon going public...these notions have been around for a looong time, and, honestly, the more these things are said, the more they ring hallow. I feel like Charlie Brown having the ball pulled away right before kicking it. Please understand, FFHI is my #2 or #3 holding, depending on the day, so I did drink the Kool-Ade, and I still believe in the company and the potential, but it's interesting to see these attachments from April of 2024 26 months later realize that minimal tangible progress has been made. We have to trust that intangible progress is being made that is unseeable right now. i THINK that's happening, and really hope it is, but the fact that it hasn't yet does bring up the notion that either it won't, or that my patient capital would be better off being patient elsewhere. The above comments are well over 90% frustration with the rest being concern, anger or bewilderment. And, yes, one has to think that management is as frustrated as this shareholder. -Crip -Crip

-

The recent capital allocation success, IMHO, is due to a confluence of factors. First, I agree with Viking that after years of trial and error, experience has honed the edge of their Capital Allocation knife...they are simply better at it than they were. However, as I think "old Fairfax" ran into it's fair share of bad luck, "new Fairfax" has had it's own share of good luck as well. The Pet Insurance deal is an example of the latter. Yes, they recognized that it was undervalued, but I can't believe that at any point early in the process did they think they could get THAT much money for that business. It was extraordinary. We humans have a tendency to discount how much luck or randomness plays into our fortunes, good or bad. Being good at something brings the odds in our favor, but it's not universal. Example...if Steph Curry and I each take 5 shots from 3 point territory, he's going to make more than me the vast, vast majority of the time. Randomness/luck suggests that, if we did enough of the 5-shot competitions, I would tie or maybe even win on occasion. Investing is like that...all we can do is to hone the skill (Steph Curry) to maximize success. The reason to bring this up is that, down the road, they will run into a "cold streak" in terms of Capital Allocation. It may be argued, if and when that happens, that Fairfax "lost their touch". In that instance, and in the 7-year "hot streak", we need to acknowledge/understand that randomness/luck is a contributing factor. -Crip

-

Thank you for the Leucadia reference...it's been forever since I even thought about the company, much less saw something in writing about them. -Crip

-

First, I've not said this but I (and likely many others) really appreciate your contributions to the forum. The insurance-industry experience gives a very useful perspective to the discussion. Thank you for that. Second, you point out temperament above, and it really is hugely important. When I first heard Buffett talk about it, I really did not comprehend HOW important it is. My son, 26, started his investment journey a couple years ago. Technically, he's not a brilliant stock-picker, but his decision process is rational and long-term oriented. He's not going to break records with his returns, but he's gonna do better than most, solely because of his temperament. -Crip

-

Assuming she selected these investments at your behest, hoping you get a nice bottle or two of your favorite libation for the recommendations. -Crip

-

Yeah, I was kinda reaching that conclusion myself, you just stated it far better than I could. -Crip

-

I am still not sure of buying back shares is better or worse than taking out the minority interests in Allied World and Odyssey, but one has to believe that they've done the due diligence on this. Clearly, they have more information with which to make this decision than I do, and far more acumen in terms of allocating capital. It just seems that taking out minority interests is like buying a well-run insurer at an attractive price with virtually no chance of any "surprises" one receives when buying an insurer outright. Maybe it's a timing thing where they can take out the minority interests at any time but the open market share price is likely to only be this low "for a limited time, only". -Crip

-

I don't have any idea, it may not ever do it, and it really doesn't mean much to me, personally. Achieving a long term 15% ROE, lumpy or otherwise, is all I'm concerned about. P/B or P/E will fluctuate, and that allows us to buy when the opportunity is right, which is where we're currently at, or sell a little opportunistically if we want to add to our dry powder. As I've said before, the closer the price gets to being fully valued, the more tempting it is to sell. Being perpetually undervalued for a company that continues to grow value is a great place to be. -Crip

-

If memory serves, you've posted on more than one occasion how quants drive much of market direction. I did not agree with that but am slowly realizing the level with which quants exacerbate market sentiment. This is a good example, I think, of "*** is going up largely because *** is going up", and the same in reverse. Not exactly sure how to use that to one's advantage except for situations like we've seen over the past 6 months with Fairfax where the price declined but company did not. -Crip

-

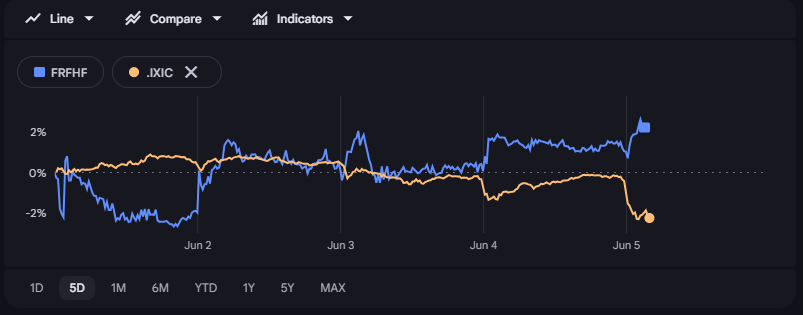

To the point made a day or two ago, before things got squirrely, of capital flowing into Tech and out of Financials, this is the past week comparing the Nasdaq vs Fairfax (US). The Nasdaq high for the week late in the day on Monday occurred with the Fairfax low, and since then they've gone in opposite directions. This does not explain all of the FFH decline in share price this year, but it is definitely a contributing factor. Occam's razor. -Crip

-

It would/will be interesting to get cwericb’s take on the original question, but I thought the original question was more than fair; zero offense was taken. Alternative viewpoints should be welcome as it spurs conversation. And open-ended questions and opinions which are contrary, at least in part, to the general consensus are equally welcome. Munger’s quote of “invert, always invert” is paramount, IMHO. One other aspect of the FFH share decline needs to be considered. Specifically, over the past several months, AI stocks have gone ape shit. Micron has more than tripled YTD, Nasdaq is up over 14% YTD and over 6% in the past 4 weeks. While Berkshire, Markel and JP Morgan Chase are down down 4.6%, 15.9% and 4.2% respectfully YTD. All three of those companies are doing fine and are as strong as ever, but money is flowing out of financials, CLEARLY, and into Tech. This will not go on forever. The market is a voting machine and, without question, it is voting for Technology/AI.* Today is a perfect example, and there have been several days like this throughout 2026…Tech is pulling back and financials are gaining. So, Bearprowler, honest question to an honest answer…the #1 thing to look at is company performance and stock price is a distant #2. If the price moves up faster than company performance/value, then selling should be considered. When the opposite happens, buying should be considered. It seems easy, but if it was that easy, we’d all make millions. Emotions get in the way of logical thinking. If it only took intelligence to invest, then all PHDs would be millionaires. -Crip * Please do not interpret this as me calling Tech stocks over-valued or disparaging them in any way. There are winners now and will be winners down the road. Right now, I think the market is voting for them at the expense of financials, and pendulems swing both ways.

-

Regarding how long I am willing to wait, I don't have a specific time frame. It's too limiting. In terms whether or not I'm absolutely sure we have not entered into another seven lean year period, It's hard to be absolutely sure of anything. My focus is less on the stock price and more on what the company is actually doing. In the first quarter we had solid underwriting results and the monetization of an asset that was worth more then it's carrying value. The other investments did not perform terribly well, in line with the markets, but nothing I saw looked like a permanent loss of capital. From everything I can see, the company is worth more now than it was on January 1st. If that changes and the worth of the company declines, a reevaluation would need to take place on my part. In terms of my spouse, she has heard this from me before: "If you think it's best to buy or sell an investment, give me the reason why and we will talk about it openly and objectively." The only thing to add is that I guarantee you that I put a hell of a lot more pressure on myself to invest well than my wife does. -Crip

-

Impossible to say. Depends a lot on what other options are available at that time and any other moves that FIH may make between now and then. My hope is that value grows at an acceptable pace but price lags behind, which is what we've seen over the past 6 years with FFH. That provides a good return and does not tempt me to sell a underpriced, growing asset. -Crip

-

Wow, that's was really kind of you to say, I really appreciate it. Back in those days, it was Cardboard and BSilly, as well as James East and others who I remember being the voices of reason. And, of course, you're welcome. No doubt I've received insanely more knowledge and wisdom than I ever gave, but if I helped, I'm happy to have done so. Funny that you had a similar conversation, and funnier still that you had it on Saturday morning as I'm pretty sure that's when we had our conversation. -Crip

-

You ain't alone. It's less about waiting for a pop in price and more about that BIAL alone is worth a helluva lot more than it's selling for. At some point price will catch up with value. Part of me is pretty happy if management can continually grow value, but part of me is frustrated that value has not yet been monetized. -Crip

-

Every month I get with my wife to review our financial situation. This month the of Crip-Family net worth was not impressive, and when returns are compared against the S&P, it looks even worse. I gave her the low down, specifically, that Fairfax really killed our returns YTD and in May especially. She asked "What happened with Fairfax?"...response was "Not a damn thing, literally no bad news". This is instructive...company moves notably lower with, from what I can see, zero reason. Yes, it is frustrating to see the impact on the net worth, this is the kind of thing we live for...company getting better and price getting cheaper. We have been buying on the way down, but hindsight says we should have waited a little longer. -Crip

-

I would have to think that they've done plenty of analysis on share buybacks vs. Allied World buyout vs. any possible insurance companies that may be available for purchase at an attractive price vs. other opportunities about which we have no knowledge. They know first two options (buybacks and Allied World) better than anyone. If something comes up that looks better to them than the first two, then that would be really interesting. -Crip

-

Those of you who want to point out the shortcomings of HWIC for not holding MIcron, congratulations on the gains on which you're sitting from your personal portfolio. -Crip

-

I understand pushing out maturity dates, but that interest rate differential is substantial, and bewildering. This is outside of my circle of confidence so I would appreciate thoughts of anyone who has more knowledge. -Crip

-

"If you don't know the horse, know the jockey" - Fascinating how simple Buffett/Munger-isms hold true as much today as they did when he first said them. -Crip

-

* Tongue firmly planted in cheek * Wow, I posted those graphs late morning today and look what happened. I move markets. -Crip

-

In regards to the earnings, the write down on Sanmar and the currency loss were both more than I expected. If others pegged that, then mea culpa. Regarding the 2026 YTD difference, it's difficult to argue that FIH has had a better 4 months than FFH. I gave up trying to understand market sentiment a long time ago...it will always confound me. -Crip

-

Voting machine - Weighing machine A week ago is when earnings came out. It's hard to argue that FFH had a notably better Q1 earnings report than did FIH, yet FIH share price has outperformed per the first graphic below. Looking at the YTD comparison, again, the news out of FFH outside of the earnings report (Poseidon) has been notably better than FIH (Sanmar) but, again, not only has FIH share price outperformed, it's outperformed dramatically even accounting for the FFH dividend. Efficient markets? I don't believe so. -Crip

-

The knee-jerk is that they expect to be able to monetize a certain asset of theirs's. IF that's the case, and I really don't think it is, than it's a pretty bold move or they have a high degree of certainty that regulators will approve said monetization. Absent of that, your guess is as good as mine. -Crip

-

Regarding the TRS position. Seeing as I was a proponent of selling those back when the share price was below $1,000, one should take anything I say with a grain of salt (If one can't admit errors in one's judgement, one hinders their ability to learn) There is one major concern I have with the TRSs, specifically, the black swan event. Example, a rapid increase in inflation that reduces the value of the bond portfolio concurrent with a Cat 5 hurricane or some such thing. Both of those would cause the stock price of all insurers to decline, perhaps significantly. Should that happen to Fairfax, it would be a "triple whammy" as, in addition to the first two, one of their biggest investments, the TRSs, would fall sharply in value, and then it could spiral. Market sentiment may not give a crap if the intrinsic value is north of $2,500 and could continue to sell off with the stock price below $1,200, or $1,100 or... One has to think that management has modeled scenarios like this and others as well. In doing so, they either made the determination that the damage was absorbable or they have some counter-measures. After all, insurance is all about risk-assessment and risk-management, so one has to assume that they've accounted for this and still deem the risk-reward of the TRSs to be favorable...that's why we allow them to be stewards for our hard-earned capital. So...if the question is whether to keep or close out, there are many others who have far better insight into that than I do, so there's limited reason to offer an opinion. If the question is whether or not you trust management to make the right decision, the buy order that was filled for me increasing the position of my biggest holding by over 10% shows that I do trust management. -Crip