cwericb

-

Posts

2,848 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by cwericb

-

Anyone who held shares in Fibrek when Resolute took them over back 2011 knows that the “Fair and Friendly” Fairfax motto applies only to Fairfax self interest. However, I would reserve criticisms of Ben Watsa until someone can show evidence of his performance or lack thereof. If he does a good job I don’t care who his father is. But until someone can show that he is doing a poor job it is a bit unfair to criticize him simply because of his age or who his father is. As far as PW’s salary is concerned, how many other companies of Fairfax’s size has a CEO with a $600k salary? Sure he also gets the $10 dividend, but so do we.

-

"We've seen multiple instances of earnings coming out for FFH where price movement is relatively stable for 1-3 days only to see a significant move up (3-5%)" That is absolutely right. I have noticed the same thing several times over the years. Any guesses as to why? The only thing I can think of is that FFH is just so far under the radar its like "Oh gee look at that, Fairfax posted some good results perhaps I should pick some up." At times for me, it has been like having inside information about the results before they are posted. I'd be picking up more but I am already over concentrated in Fairfax. FIH.U is up 4% though.

-

It is definitely going to be interesting to see how this all settles out. They have been very patient sitting on their cash, so they must be pretty sure they have picked this up at the right price. (Reuters) - Insurer Fairfax Financial Holdings Ltd said on Monday it would buy some Canadian assets of bankrupt UK-based construction and services company Carillion for an undisclosed amount. The deal would include facilities management at airports, commercial and retail properties, defense and select healthcare units, Fairfax said. Carillion collapsed on Jan. 15 after its banks halted funding, triggering Britain's biggest corporate failure in a decade and forcing the government to step in to guarantee public services from school meals to roadworks. Fairfax will also assume certain liabilities related to Carillion's Canadian operations. Canada is one of the largest markets for Carillion outside the UK. Canadian unions had previously urged Ontario's provincial government to end hospital services privatization after the collapse of Carillion.

-

But they are not buying ALL of Carillions operations...

-

The Outland part of Carillion might be a good fit with Cara ? Outland, a Carillion company, is a leading provider of remote site accommodation and associated services, including camp management, catering, maintenance, housekeeping and tree planting to public and private sector customers across a wide range of industries, such as mining, utilities, forestry, oil and gas. This partnership complements the existing skills and capabilities of Carillion's support services business and enhances prospects for growth of our support services activities for clients across Canada. For more information on Outland, please visit: www.outland.ca.

-

Added to T-WCP, T-PPR, T-BTE. Initiated T-CJ. Sold some T-OBE

-

RBC 1.2267 Jan 25/18

-

Yes, they are quite different situations, I was referring more to the fact that Prem was able to put the right guy in to run The Brick and I believe he has probably put the right guy into run Blackberry with Chen. I too had shares in The Brick back then and one of my sons was running their flagship store in Calgary at the time. It was a quick rescue and turn around. Bottom line is that I believe that Fairfax is a good investment - for me at least. Bought a few more Fairfax shares this week and started a position in Fairfax India as well.

-

Don’t necessarily disagree with you. But it will be interesting to watch BB over the next few years. Prem has orchestrated some significant turn-arounds in the past, The Brick comes to mind when he put Gregson in control. Think Chen may well do the same with Blackberry, it is just taking a lot longer than anyone expected and it is a different company today than when Prem jumped in with both feet.

-

“Working from memory, the credit default swaps were a collective position of less than US$400m.” Yes SJ, but consider that $400m (actually about $435m) represented a much more significant gamble in 2003 than $435m would be today given inflation and the size of Fairfax 15 years later. And Prem has warned us that results would be "lumpy".

-

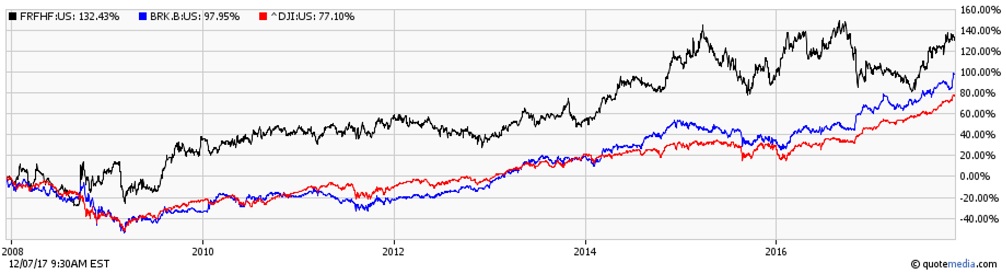

I am also one who has been very comfortable holding Fairfax for the past 10+ years, perhaps because I am a rank amature at investing. Yes Prem has been widely criticized for his hedges, just as he was for his Credit Default Swaps when he purchased them. As they say, hindsight is 20/20, some things work, some do not. My investment in Fairfax with its hedges and deflation swaps acted as a hedge for me that allowed me to make other investments in the market with a certain amount of confidence that my FFH shares would help protect me if things went south. As a Canadian, Fairfax also tends to act as a hedge for the Canadian dollar. When the CDN dollar drops against the US dollar, FFH shares tend increase in value which is why FFH shares have performed better in Canada than in the US. According to the TMX chart comparing FFH to FRFHF, since 2013 FRFHF is up 40% while FFH is up 80%. Works for me. I don’t know why it is expected that he has to be right every time. I certainly am not right on all my investments, but overall I seem to do okay, I don’t demand more of Fairfax.

-

Good point, chart is from TMX Money. I reduced the size of the previous chart (sorry) Here is the 10 year chart in U$ for BRK.B, FRFHF & DJI Actually I think this supports the fact that Fairfax did quite well during the 2008-10 period

-

Pertinent thread. I feel I am probably sitting on too much cash right now. My largest holding by far is FFH as well as some reasonably well balanced mutual funds. But when I look at people who are making 15-20% or more in the market I get a little uncomfortable with that much cash. Therein lies my interest in the question posed here. However, my thinking is that at some point reality will prevail and Mr. Trump will be gone. When that happens I think it may precipitate a major (overdue) correction. And remember, the longer the time between corrections, usually means the deeper the correction. But this is just the way I see things in my little mind. In the meantime I am comfortable trusting FFH but ask myself if I want more shares at the present level and I don’t like having too many eggs in one basket. Here is the 10 year chart for FFH vs BRK.B if I can get it posted.

-

Bought FFH at $228 in 2007. Have no regrets. Wanted to buy it earlier at under $100 but didn’t have a trading account back then. Once the account was set up FFH was the first stock I purchased and have added to it from time to time. When I compare FFH to BRK.B since 2007 the charts appear to show that FFH considerably out performed, but then I may be missing something. I think FFH is still as good as anywhere to have money invested.

-

Think one may have landed in Washington DC back about a year ago.

-

Trying to figure out if these guys in Washington are crooks or just delusional. Or both.

-

Off Topic - What was your used car buying experience like?

cwericb replied to LongHaul's topic in General Discussion

Last couple of cars I bought new because there was not enough price difference to justify buying used. In buying used cars or boats I have always found that in private sales, the quality of the individual is every bit as important as what you think of the vehicle. Last year I bought upscale model of the Kia Sorento EX V6, all wheel drive, panoramic sunroof, leather and more standard features than I know how to use. Had to swallow a little pride, but Kia is making some of the best cars on the market today. They robbed Audi's chief designer and BMW's chief engineer and they apparently use a better grade of steel since Hyundai makes their own steel. Watch out for KIa! Rated #1 in initial quality by JD Power of all brands sold in North America in the last 2 years - and that includes all those fancy upscale brands. AND the 5 year warranty means a lot. -

If you use Google Finance, now might be the time to...

cwericb replied to Liberty's topic in General Discussion

augustabound: Ditto, If you ever find a good replacement let me know. Google comes up with features like the personalized home page - which i found excellent - and after a while you tend to rely on it but then Google just drops it. I have used igHome but it is not near as good as Google was. I don't know how much it would take on Google's part to keep features like these going but one would think it would be very small in the overall picture. -

If you use Google Finance, now might be the time to...

cwericb replied to Liberty's topic in General Discussion

Google is soooo annoying. It seems that every time I have set up something with Google it gets discontinued after a few years. Google’s personalized home page, Picasa, Google’s portfolio feature. They have had some very nice features, but as soon as you begin to rely on them they tend to vanish. -

A little bit more of POE - PAN ORIENT ENERGY CORP Speculative, but a lot of short term upside potential and reasonably limited downside.

-

Good move boss.

-

Thanks for this Dazel. Think you are right on in what you say. A lot of people seem to overlook the fact that Fairfax has been building a world class insurance company over the past few years. Believe Fairfax are releasing Q2 results next week. May be interesting. Brian Bradstreet didn't buy 2,000 shares last month just for fun. Welcome back "newbie". :) Any chance of getting your 2 cents worth over on the ALS thread?

-

“Michael Wacek, VP & Chief Risk Officer at Odyssey Re, has also picked up 500 shares” So between Wacek (500 shares) and Bradstreet (2,000 shares) they have accumulated over $1.5 million dollars in Faitfax stock over the past week and a half. That has to tell you something when they are purchasing that sort of volume of Fairfax shares. The short write up in the Canadian Insider said... “F. Brian Bradstreet, a Subsidiary Executive, acquired 1,000 Subordinate Voting Shares on a direct ownership basis at a price of $562.314 and 1,000 Subordinate Voting Shares on an indirect ownership basis for registered holder The Bradstreet Family Foundation at a price of $562.416 on June 16th, 2017. This represents a $1,124,730 investment into the company's shares and an account share holdings change of 4.9%.”

-

This popped up today: Insider Filings: Jun 21/17 Jun 16/17 Bradstreet, F. Brian Indirect Ownership Subordinate Voting Shares 10 - Acquisition in the public market 1,000 $562.42 Jun 21/17 Jun 16/17 Bradstreet, F. Brian Direct Ownership Subordinate Voting Shares 10 - Acquisition in the public market 1,000 $562.31 https://www.canadianinsider.com/company?menu_tickersearch=ffh

-

investmd My portfolio sucks right now, especially since I have so much FFH, but I just bit the bullet & bought a few more shares at about $565 CDN. When I buy it is usually a signal that the stock price will take a dive. Hope you can benefit :) eb