changegonnacome

-

Posts

2,694 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

sorry to hear that @fareastwarriors what industry does she work in?

-

Of course the other thing I’ll say is that the math says in a full employment economy unable to get productivity above 2%…….any aggregate average pay increases across the economy that exceed 4%….see you breach your 2% inflation target….~5% nominal wage growth in 2023 would result in some measures of inflation reflecting that ~3% delta…… Which indicates what we’ve talked about - that last bit of inflation above 2%…..let’s call it the canyon between 2% and 3.5%…….closing that gap requires more than background noise of tech layoffs taking comp discussion from CPI down to 5-6%…..but rather down to 3%.

-

What kind of level you seeing anecdotally?

-

Cheers for data points - my circle it seems is a little skewed. Your macro stance lines up pretty close with mine.......as we've talked about here given the market goes up 70% of the time.....being long is the only rational thing..........I guess I add, like you, a little bit of Howard Mark'ism to my posture which is where are we in the cycle......I'm 85% long if I see lots of greed, bullishness & risk taking........and I'm 105% long when I see fear.

-

Ah well you know what I mean - thats a yoke i found online to illustrate a point...........lets just call them domestically produced services, consumed domestically....... Yep agree - but lots of intermingled things going on too.........so hard to fully untangle monetary & supply chain driven inflation.......and its they trillion dollar puzzle.......if it was all just red, all the time.........no problemo were getting out of the woods..........if some blue got mixed in there then its more problematic as I laid in the earlier post. Its gonna be so interesting to see how it plays out this year. Beyond fascinating.

-

Interesting seems like the high profile Big tech job losses were enough to soften the cough of lots of employees this year - and thats exactly how inflation gets fixed.............a round of wage setting negotiations across an economy are informed by restraint because the macro backdrop has weakened. Maybe the Fed has engineered a soft landing..........my thesis was that although they moved quickly last year.......it wasn't quick enough to inform 2023 wage negotiations enough to see the transmission of 2022 CPI into 2023.......perhaps they've broken the chain......BLS data coming up will be key then.

-

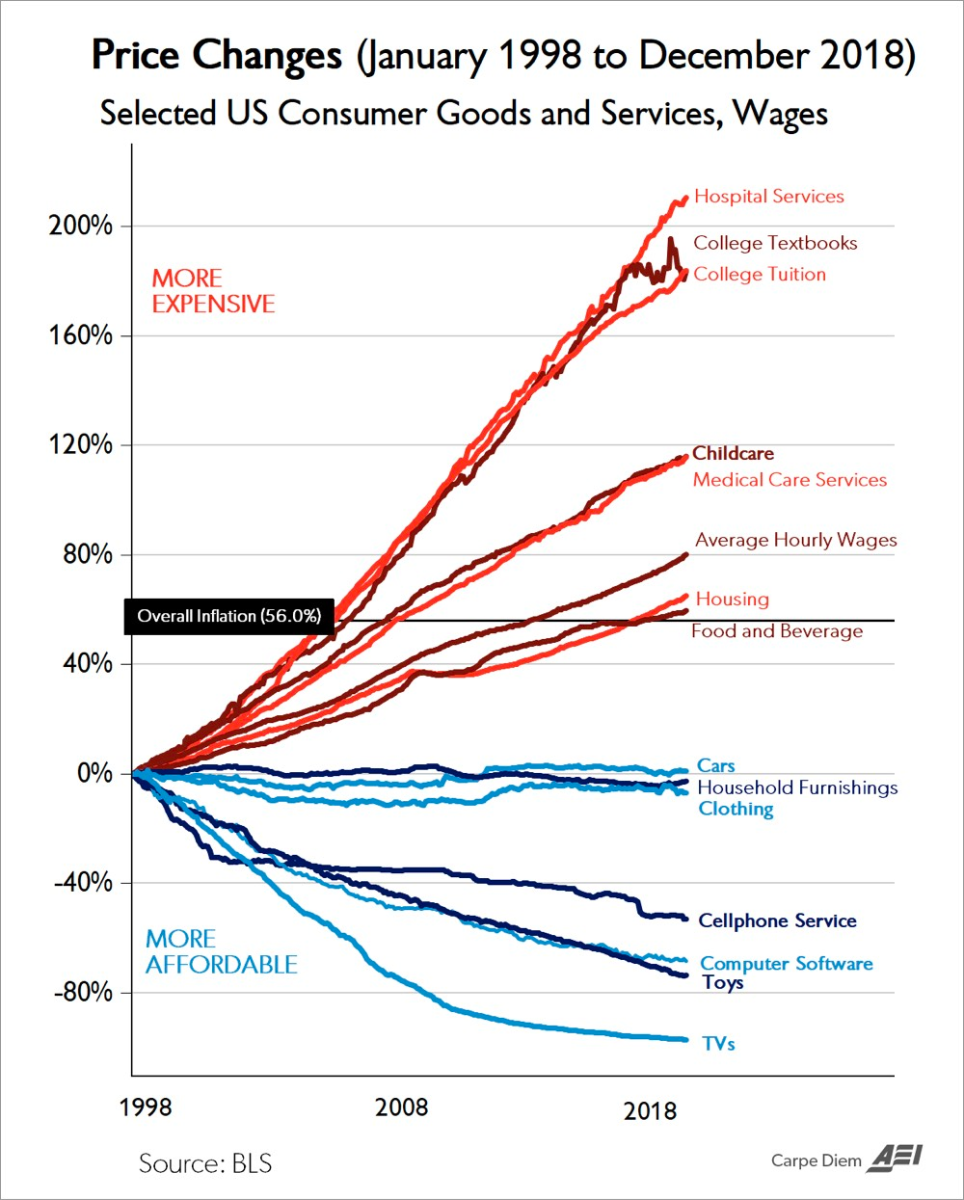

yep accept that but Made in China crap is not where the inflation I'm talking about might remain resilient/persistent - as I've mentioned the inflation to worry about isnt this stuff.......and you've seen the Fed acknowledge that its the core core as JP calls it - services inflation.........we've all seen the chart out there of eduction/health care/ prices versus the price of a flat screen tv/cell phone over decades........well this is what we are talking about again........one gets on a cargo ship and its price is set by globalization & exchange rates its had dis-inflationary forces..........the other is a domestic good, its supply is much more constrained by demographics, labor force participation etc.........you could of course "import" hospital services.......just let in a million Philippino nurses........but as we've talked about the one sure fire way to level off services inflation, immigration, is a hot button issue for left and right and nobody will touch it. Pulled out this diagram - everything in blue right now is deflating..........Jay Powell and the Fed is extremely worried about everything in RED......as this is where domestic monetary inflation shows up......the Fed pivots when YoY/MoM numbers for the stuff in red moderates significantly

-

yes yes should be clearer on some of this they are cumulative increases.....but some are actually retroactive to 2020 like the rail union one so a very big uplift in 2023 relative to 2022...so a bulk of the total pay increases is getting dumped into 2023......lets call them catch-up type inflation payments - https://www.usnews.com/news/politics/articles/2022-09-15/rail-workers-win-key-concessions-in-deal-to-prevent-strike . Nurses it seems the 19.1% over three years.....but again the offers would be front loaded into this year from what I read somewhere. These type of 'public service'-esque negotiations seem to have a front loading/backdating aspect to them. private sector obviously less where its year to year Interesting exactly what I was seeking out, guess some folks I know did a good job in 2022.......BLS data in Q1 will tell the aggregate picture.......anecdotes will have to do for now.

-

Just curious for pushback on my thesis that the US economy ( based a few assumptions which I'd be happy for people to quibble with) is: (1) about to absorb nominal pay increases across a multitude of industries that are reflective of past-CPI in 2022 (i.e. ~9%)....white collar workers straw poll in my circle are getting 9-10%.....NYC nurses on strike were offered 19%..railworkers 20%+ etc. (2) these nominal pay increases perhaps averaged out across the aggregate economy are maybe working out around 6-7% (3) the calendar matters here - wages do in the main reset around Jan 1...such that a "surge" in pay increases should be seen in Q1 BLS data?. I haven't come across much data on the intervals for wage resets perhaps I'm wrong here - new year, new salary sounds right to me. LMK? Folks applauding the slowing in wage growth coming into the end of the year in 22 seem to be completely ignoring the timing aspect. You negotiate pay increases in Nov/Dec....get them in Jan/Q1. No? Correct me if I'm wrong (3) these nominal on average 6-7% pay increases are being injected into an economy with a historically low 3.5% unemployment rate with absolutely nobody on the side lines left to call in......which is to say that the aggregate domestic goods and services produced in 2022 in the US represent an economy operating at full tilt, at a high watermark of production......and as such then the increase in aggregate goods and services that can be expected to be produced in 2023 can only be 2022's production level + plus whatever productivity gains were achieved through PP&E investments and innovation in the year. (4) This productivity gain number is likely to be disappointingly sub-2% again. Anybody seen any contravening evidence that suggests productivity growth accelerated last year or that one should expect materially better than 2% in 2023? As I've talked about before an economy can only consume what it produces......nominal pay increases do not increase the actual amount of goods and services available to be consumed........but nominal pay increases or the quantity of money chasing those services and goods can certainly result in the quoted PRICE of those services and goods changing. Given the above ballpark numbers then one would expect 2023 to be marked by services inflation (80% of US GDP) remaining stubbornly high around 4% as nominal pay increases, incorporate into higher overall spending against an increase in aggregate supply of those services that is at best a 2% increase..........with goods (20% US GDP) inflation being perhaps lower given its exposed more to global competitive forces & substitution and where strong dollar & lower input costs (energy/commodities) might mitigate full pass through of inflationary forces (too much money chasing too few goods in this case). The only way the above DOESNT play out of course would be a situation where aggregate increases in income were not translating into the same increases in spending......which is to say that people were beginning to display thrifty/recessionary behavior.........increasing savings rate for example such that nominal pay increases were being kept on the sidelines as opposed to being spent...........but this should be showing up here https://www.bea.gov/data/income-saving/personal-saving-rate.......December numbers dont come out to Jan 27th...but no sign of any increased savings rate....folks are getting pay increases and they are substantially spending every penny of those increases. The other source of income/spending in any economy is credit creation - I'm seeing interest rates that have a REAL yield attached to them now being offered to consumers which is clearly effecting credit demand/creation.......seen in autos etc. so we are seeing drop of in demand which is credit fueled but the biggest source of spending, income, has shown very little moderation.......unemployment hasn't risen, savings rates haven't increased.......credit creation has slowed but I'm not sure by enough. Need to look at some data here to see. So short version not sure how the hell you get inflation down to 2%......if the status quo continues..........there's a clear contradiction with the goldilocks view of the broad market in 2023 i think...........something has to give..........either the real economy goes such that equilibrium is restored and inflation comes down (bad for earnings/bad for indexes) or (2) the Fed stupidly pivots and you get a sucker rally which will be dashed once another tightening cycle has to be implemented again later for higher and for longer (short term good for the indexes but terrible later on). Overall bad for equities. The Fed is killing itself right now trying to warn people it wont be doing No.2.......that its going to hold firm in the face of a deteriorating economy. Why wouldn't it of course? It knows that a deteriorating economy is how monetary domestic inflationary issues are cured. To do anything else would be like going for haircut and stopping the guy half way through and telling him your going to pivot out of this haircut thing and walking out with half your head shaved!

-

Mixed bull & bear which I think is reality- is that inflation is indeed falling but its the easy COVID/supply chain/energy stuff underneath peeling off now giving a false sense of linear progress .....in the main historical inflationary bouts have never come down in such a beautifully straight line. This false sense on the momentum & progress on inflation is holding up index prices right now as the thinking goes that given the progress to date rate cuts/pivots are just around the corner & we are heading back towards ZIRP soon........this is a lazy wishful thinking extrapolation of the progress to date on the inflation curve & I think a mis-understanding on how dis-inflationary forces which dominated the last 40 years have switched to inflationary forces (but thats a longer term & harder debate) However IMO we are about to hit the much more sticky 'wage-price-productivity' inflation that has been embedded inside the much higher core number for the last couple of years of which I've talked about alot..................think of it like digging through soft dirt (supply chain/energy inflation) and then getting to bedrock, that bedrock is monetary inflation & it requires stronger resolve & heavier machinery to make progress on it. Progress on this type of inflation.........the monetary kind........ will be much more non-linear & frustrating. My guess is we will see a flair up or at least a sticky plateau in domestic services inflation in H1 2023 which will smash the linear inflation progress thesis to pieces................pushing out the pivot timeline by alot with likely pre-requisite fall in index prices. Why? Because CPI++ wage increases negotiated in late-22 in a strong full employment economy are getting incorporated into 2023 wages then prices........given there has been no meaningful increase in the productive capacity of the USA to absorb such income/spending increases & no meaningful decrease in aggregate demand at the same time. The question becomes where does additional nominal income/spending go in an economy at already at FULL FULL employment - the answer is it goes into prices....the amount of goods and services can NOT be materially increased. So I anticipate that incrementally (as result of pay rises) too much money will continue to chase too few goods/services in early-2023 as this wave of lets call it on average 6% nominal pay increases hits an economy that likely only grew its productive capacity 2% real in 2022 (probably worse).......the delta between those numbers = 4% inflation.......inflation failing & a very strong economy/labor market is kind of an oxymoron....the mistake folks are making is that the fall from 9% to 5% was indeed done in a strong economy, the problem is that this inflation truly was exogenous & one-time - COVID supply-chain/energy/ukraine. Underneath is the 5% to 2% inflation journey, bedrock monetary type inflation...........pernicious, persistent & obstreperous .......hence while I remain open to a goldilocks landing, I'll be shocked if we get one.

-

For sure assuming everybody here has some long run way to go being fully invested makes total sense and in fact is the only rational thing to do - but you know not even clear to me at age 60 (as long as you have the stomach for it and have spent a lifetime learning to love volatility) that you shouldnt really down shift your equity allocation......of course all dependent on circumstances.......but as I think about heading towards 60 I can't see my equity allocation shifting too much at all.....now around that fully invested posture and for the first time ever in my investing career have I put some bearish hedges they served me well in 2022 and I dont see much reason to take them off........yet..........but we are getting closer

-

Absolutely the correct default posture is bullish.......ALL the time.....a coin toss with 70% probability of coming up heads requires you to bet heads EVERY time

-

As I've said last year was multiple compression.........this year its earnings compression............both combined likely take you to a shiller PE that looks more like the mean of 17 above..........reflecting what is likely to be a secular normalization of underlying interest rates & lower overall broad indices pricing.......where future return will come from pure earnings growth + dividends.......and not the multiple expansion that defined much of the 2010's stock outperformance versus underlying economic performance

-

Yep agree only addition I'd add is that the price you pay matters more than it has for 20+ years........broad multiple expansion bailed out a lot of bad cash flow forecasting in the last decade.........multiple contraction or even stagnant multiples leaves no where to hide if you've mis-forecast the underlying business fundamentals.......its time to raise ones margin of safety, raise the FCF yield hurdle..... as well as a prioritizing the predictability of those cashflows.

-

SOFR forward curve has rate cuts forecast in for H2 2023….Fed holding at ~5% isn’t priced in….and I would suggest (with no data to back it up)….only opinion….that what’s most definitely not priced in is the lack of central bank easing when economic conditions emerge that would have ordinarily triggered such actions in the past (rising unemployment, bankruptcy’s, market stress/bordering on panic). I’m skeptical that the Fed will show resolve on this last point but pronouncements to date show a Fed mentally preparing itself to do just that. Let’s see. 2022 - was the year of multiple compression this part of the story is mostly over I think Possibly some more to go as folks begin to think of world where 3-4% risk free rate might exist longer term on the far side of this sea change and so the longer term ERP built on top of that assumption needs to decrease multiples a bit more but not much. 2023 - is the year of E compression….all those 2023 pay increases are coming out of operating margins….you can’t push price anymore on a weakening consumer….& you can’t maintain volume without cutting price. It’s a year of tough choices at an operating company level.

-

I think so too - and I think they've been crystal clear now that they see the risk of easing too early to be much greater than the risk of holding rates too high for too long................given the former would potentially see inflation come back as it did in the 70's........requiring another painful round of tightening later......this Fed is focused on one and done.......this bias towards doing too much versus too little is the big disconnect between what I see priced in the bond/stock market & what might play out this year. The idea IMO that the FED will be cutting rates in H2 2023 is wishful thinking. The Wily Coyote moment later this year will potentially be when the economy & stock markets are clearly weakening and the Fed does nothing and re-asserts its resolve.....lets define it as a VIX 35+ moment........cash used to be trash.........but IBKR is paying me nearly 4% to hold it and wait, UST 3-M 4.5%.......its getting to be attractive to wait around relative to whats out there and this trade from equities to cash.......will require equites to provide a greater equity risk premium to reverse the flow. Its going to very interesting indeed to watch it play out.

-

I'm somewhat thinking that actually a soft landing of sorts maybe (big maybe) possible.......but a soft landing for labor, not capital and by capital i mean not a great out turn for broad SPY/QQQ.......let me explain........I think in the last few decades capital has beat the hell out of labor.....just go look at the relative returns to each, stagnant middle class etc...........this recession may actually be an earnings recession where the brunt of the pain/contraction is seen in the corporate sector vs. household sector......and given the labor shortage, job losses in some parts of the economy will see labor re-allocated much more quickly than in the past meaning unemployment will not rise so high. So I remain open to idea of a soft landing.....however on the balance of probabilities and based on 2023 wage increases I expect to see flood the economy in Q1/2 2023.....I think domestic led goods& services inflation will remain stubbornly above 4% & flaring back up in H1 2023.....as I mentioned before I believe a single round of wage setting negotiations across the economy needs to be informed by strongly & demonstrably weakening inflation data peppered with macro/recessionary weakness such that FY2024 pay increases of 4% get to be in line with productivity growth (2% real/2% nominal) bringing us back into equilibrium.........fall/winter 2023 is the 'right' timing to get this done and so I suspect the Fed to keep their resolve in the face of cries to pivot....think David Tepper said something to the same effect recently.......the market loves to believe the Fed when it speaks about loosening financial conditions.....every word is gospel then....... but sticks its fingers in its hears when it talks about its resolve to tighten/weakening the economy. You can see why its human nature. I remain into 2023 somewhat they way I was in 2022.......I'm a fully invested bear.......core portfolio positions around which negative market & individual company hedges should provide downside protection, even upside as it did for me 2022.......I'll do better much on balance if we enter a bull market but i see no real signs of that yet....and I wont be fighting the Fed like Tepper says.

-

Best time to buy home is when you need a home - and broadly unless terribly unluckily it works out very well as an investment over time (inflation/population/GDP growth) then add on the enforced savings/discipline aspect of it too and really it works out well for almost everybody.

-

As a pond to go fishing in - i totally agree.......I would add an extra kicker for the brave....probably braver than me........Small Emerging Market Value

-

Hostelworld (again) - remains ridiculously cheap relative to steady state FCF and prospective growth guided at capital markets day.... final leg of COVID re-opening of HSW regions with Oceania & Asia coming out of the traps in H1 2023 to make it an OTA finally back to running on all regions for the first time since 2019 with its most profitable customers (long haul) back with a vengeance.....+ the continuation of the companies differentiated solo system/social strategy.....the metrics of which are confirming business turnaround obscured by COVID carnage. Recession resistant - given core demographic & lowest cost provider of tourist accommodation across all types. Inflation beneficiary - given capital light nature and carry fee......plus a nice balance sheet/FCF catalyst in 2023 with re-financing/payoff of large high yield COVID loan with cash on-hand ( ~20% of current EV)

-

Up about 15% across accounts…… Biggest losers - Got killed by USD strength against GBP/EUR! Then MSGE, GLV, CDLX……some I’ve held on to through the pain (MSGE/GLV) knowing the underlying intrinsic value & willing to accept the lower mark to market……..I could have traded them around & considered doing so once I developed my Fed/liquidity view but moving in and out of names on macro/liquidity has not worked well for me in the past too many opportunities for psychological misjudgment in the future, better to sit and hold what you know and own even if market is throwing dumb prices at you….…I expect to be rewarded for the pain in these two names in the future……....others like CDLX i sucked up and dumped once Fed got serious and luckily saved myself a shit load of pain later on if I hadn’t pulled the plaster off…..truth be told when I was buying CDLX I deep down knew it didn’t make sense given their marginal advertising positioning, cash burn etc.. Should listen to little voices more in the future! Biggest winners - - Hostelworld by a mile pretty much up 90%+ on my cost basis - got aggressive on dips on this name this year and broke some self-imposed portfolio concentration rules in the process….breaking those rules & getting aggressive paid off. I listened to the little voice on this one - Bank of Ireland +69% - worked as I expected given interest rate environment - Various shorts, bearish options hedges, selling vol & merger arb……could have been more aggressive here of course and I would have had a 50%+ year……..but they were fundamentally always sized as hedges and for all my bearish talk on the “bottom” thread…….being positioned ultra ultra-bearish works 1 out of what every 10 years?…..this would have been one…..but making any real money on the short side is dangerous…..as you might be tempted to do it again and its usually the road to ruin over time! Reflecting on my positioning & thinking about alternative outcomes to this year……..I think I got it about right in terms of a posture/positioning….….the alternative universe where everything say rallied in H2 2022 would have worked out better for me on a performance basis……..the fact it didn’t and I still did acceptably well on a full year basis feels like I got the balance about right and wasn’t too skewed to any particular binary outcome.

-

Yep I was on the high side - doing post on the run.....it was dumb. Right to be called out. My bad. My point still stands though which is F&E is not an unimportant part of wallet share........food also has an outsized impact on inflation psychology........driving more aggressive future wage demands etc.

-

Haven't had time to dig around in these latest reads properly......but dont need to on one point.......those that exclude Food and Energy have no idea about real life..........and that F&E makes up about 70-80% wallet share of those less well off than they are....housing the rest.....and that is not a small amount of people out of the total population.......inflation pressure is the difference between running out of money on the 27th of month and running out of money on the 20th of the month. Only a tenured professor at an Ivy league business school would say something so dumb with a straight face as in - price inflation data excluding food to stay alive and energy to stay warm/cool apart from that for everything else is awesome. Quick read so far - as predicted the trip from 9% down to 5% is kind of a mathematical certainty......this journey 9 to 5 is indeed the COVID inflation/supply chain/Ukraine stuff going away..........its the trip from 5% to 2% that will be the bitch.....that 3% is god damn monetary inflation.......and its pain in the A to get rid off.

-

How Bad Will The Recession Be in 2023?

changegonnacome replied to Parsad's topic in General Discussion

Thanks for the charts. Interesting. The important factor with comparing 1945 to today and when thinking about debt, inflation and the money supply is that in 1945 the US was sitting in the middle of the golden age of its productivity growth curve that was sloping upwards with high YoY real (not nominal ) GDP/income gains the period ~1920 - 1970......the US through immigration, industrialization, innovation, increases in female labor force participation (& post-world war boom where it wasn't wrecked! like Europe) was making more and more 'stuff' each year in effect its REAL income was rising.....the incremental goods and services that you could sell to the world and each other meant in effect the nation was getting wealthier for real & more able to support its federal debt (which was falling as percentage of growing GDP).....real wages were rising as a result too....as discussed in other threads money is just a claim check on goods & services changing the amount of money doesn't change the amount of goods & services......in effect you don't get rich by printing more money or indeed borrowing money (which are claims on future productivity)....you actually get wealthier/increase real incomes by producing more & more goods and services over time....but also by under spending your income and investing in your productive capacity (infrastructure etc.) Today but really since 2015 the US has been in the opposite of the above - a productivity trap....over spending incomes, borrowing, not investing in infrastructure/productive capacity......its been lousy, it was good for financial assets but the underlying economy didnt perform quite as well as SPY would suggest......and so when both the fiscal and monetary authorities opened up the flood gates in 2020 with direct stimulus to consumers they did too much, in an economy which in 2018/19 was already operating at historically low unemployment (in effect the US was already at full output)......the incremental nominal increases in incomes (via stimulus/credit creation) couldn't change the amount of goods and services being produced only their quoted price so we got monetary inflation (mixed with supply shock/energy inflation)....real output & productivity growth have remained lousy since....who by 2021 was left to entice off the couch? Didnt help that the boomers started quitting in droves. The incremental nominal income/spending just resulted in higher prices.....real output/productivity growth remained lousy. Whats knowable is whats actually required to bring inflation down.....its productivity growth and nominal spending/income growth converging with one another.....we know productivity growth is stuck & aint going higher YoY......so I'm afraid its income/spending that needs to adjust downwards to bring back price stability....how get there via a 'one and done' recession next year.....or double dipping recessions across the next 24 -36 months is the question IMO. Lets see. -

How Bad Will The Recession Be in 2023?

changegonnacome replied to Parsad's topic in General Discussion

Answer: BAD I think its clear that the US consumer is going to hit a wall sometime in H1 2023 - various money centre bank CEOs (Jamie Dimon et al) have alluded to what they can see in their proprietary data and I can see it in public data......consumers are running down cash balances, driving up credit card/loan balances and the other metric I came across recently is that emergency 'hardship' withdrawals/loans from 401k/IRA's have increased to levels last seen before the GFC. Its also clear that the Fed is prepared in 2023 to prioritize its inflation mandate over its employment mandate (for a time), and certainly in the early stages of demonstrable weakness in the economy/labor market/stock market, to do something it hasn't done in perhaps 30+yrs.......absolutely NOTHING. Zilch. This moment of 'why aren't they doing something?' will be the point of maximum opportunity in markets I believe. Things will get hairy and its why I think we'll break the lows seen in 2022. The two unknowns are the actual level of pain required to quell inflation & the other unknown is the intestinal fortitude the Fed will show. I don't envy their job....its hard/impossible to know how much disinflationary momentum is required to 'get back to 2' sustainably and while your unsure how much is required all your stakeholders & constituents are screaming at you to STOP and STIMULATE. It's why my base case now is that they likely stimulate too early, inflation re-emerges and they have to go back again later and do another hiking cycle possibly in 2024. In this respect then a double dip recession is very possible if past is prologue....obviously better if its one and done.