Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

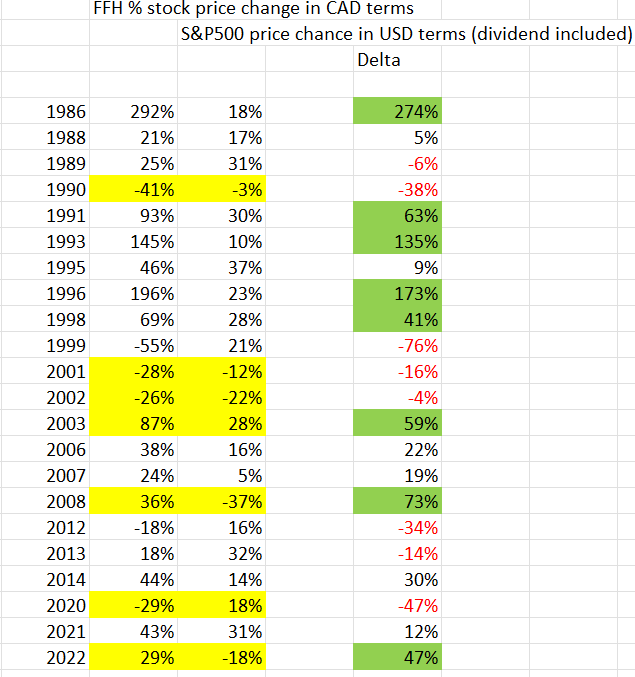

@nwoodman @Viking If the big technology firms get a bid and S&P500 bottoms out and money flows into them (ala post Dec 2018), wouldn't that take some air from FFH like names. I am not talking about the underlying business just the stock price. Prem himself endlessly talks about how FFH does outperform the S&P500 coming out of a crash (not FFH book value he is talking, but FFH share price). We had that massive contrarian outperformance in 2022, which followed outperformance (though mild) in 2021 by FFH. What is the likelihood of that repeating itself, if S&P500 rallies hard, third time in a row. I think low. I get all the "it is cheap" arguments. That is being for me, as a core position at 11% (not counting FIH), it is a hold, so it is not like I am missing out on anything but I will wait before adding more money in 2023. Lastly, the mountain has two sides, as I like to say. At some point when FFH rallied hard in 2014 from $400 to $700. There were all kinds of reasoning that made sense at the time, why it was a buy at $700. "Don't you see the deflation coming". Hindsight is 20/20, 8 years later now we know better. That was the "left side" of the mountain. And 2020 was the "right side" of the mountain. When the share price revisited the same dollar value. I could say the samething about any other stock. Say Microsoft. $248 today in Q1 2023. And it was $248 in Q1 2021. In 2021, you were crazy for not owning, and in 2023, there is a "tectonic shift". FFH may go (will?) to +$,1200. But there could be really good reason for it to take a dive some years down the road. I guess, i am looking at this with an eye to long-term capital deployment. I am too busy enjoying life than trade around. Of course one could trade Microsoft around that step change in outlook etc. And one can trade FFH as well.

-

-

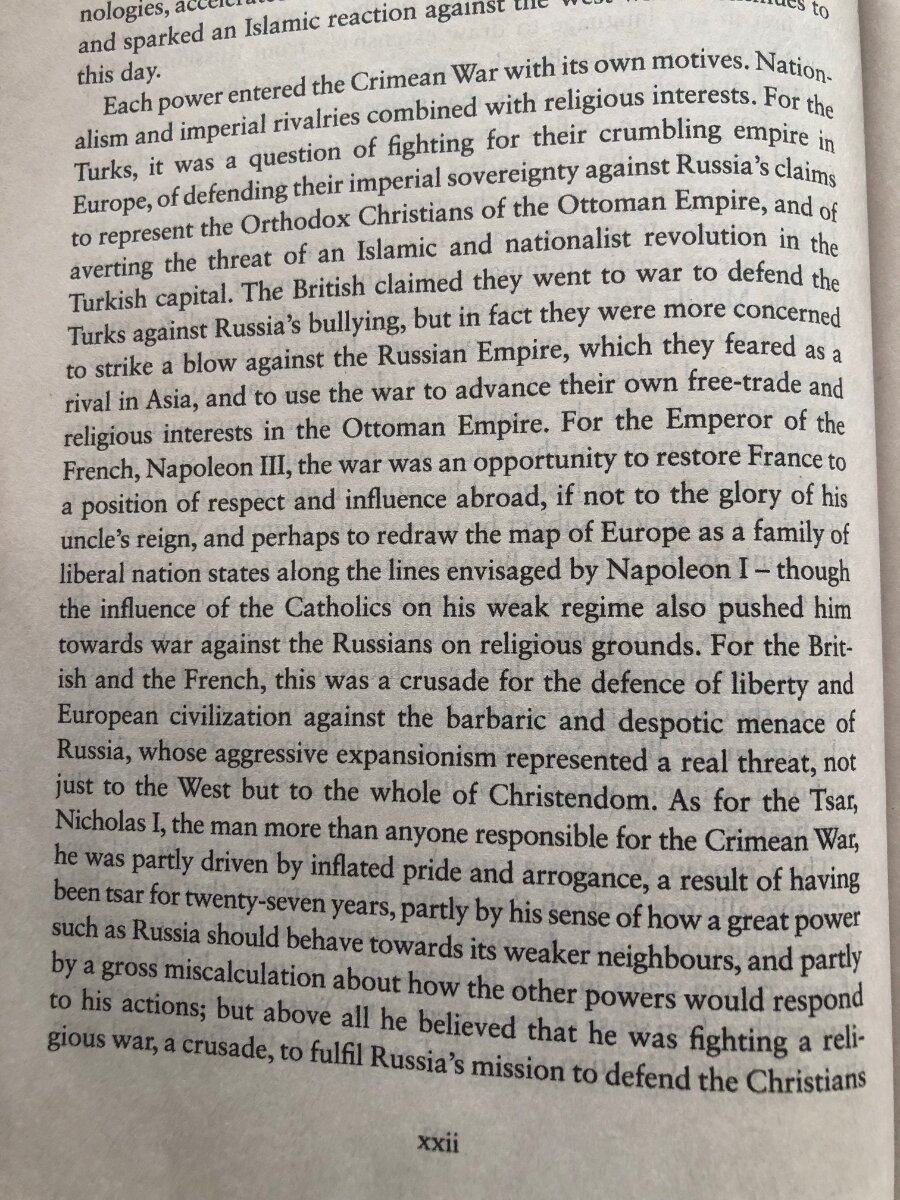

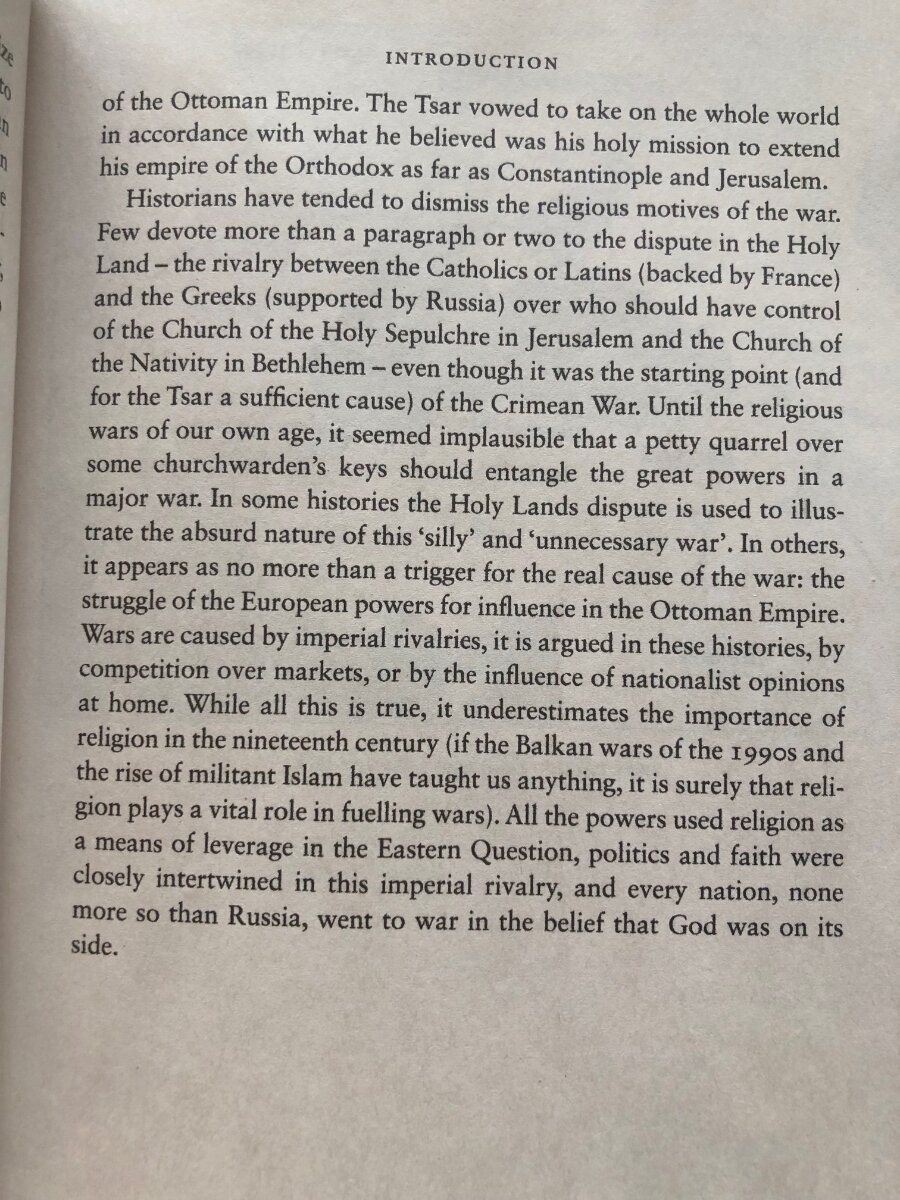

After having finished reading Robert Massie's massive work on Peter the Great, I took a break and read short ones: Feathermen, a not so clear if it is real story about the aftermat of an SAS operation in Oman, and Psychology of Money, I am now back to my Russian studies. I started reading this book on the Crimean War, another world against Russia story. A major conflict that defined an entire generation. A war that brought hints of how future wars may look like. I will skip Robert Massie's work on Catherine the Great for now, and come back to it after Crimean War, eventhough the chronological order is in reverse. That said, I also bought the recently written work of Lawrence Freedman: Command: The Politics of Military Operations from Korea to Ukraine. Will be reading this in parallel. The Crimean War: A History: Figes, Orlando: 9781250002525: Books - Amazon.ca Command: The Politics of Military Operations from Korea to Ukraine: Freedman, Lawrence: 9780197540671: Books - Amazon.ca Below are few snapshot from the introduction of the book, now doesn't that (specially the first snapshot) sound familiar and can it not apply to 2022-23

-

I heard about 100, 31 of which are M1s. I agree about the "land bridge". That said, I don't think you will see Abrams being used in Crimea directly. I think there is an unspoken understanding with the Americans in terms of priorities and objectives when it comes to Crimea. Ukraine may consider Crimea its soil, but I don't think any U.S. administration (republican or democrat) would be pushing Kiev hard to re-conquer Crimea. Air strikes against military targets are of course legitimate. Besides, there is a ton to do, before even getting there. First of which is to blunt the coming Russian offensive. EDIT: we are sending 4x Leopolds ! Ukraine is saved. https://www.cbc.ca/news/politics/trudeau-donate-leopard-battle-tanks-1.6725868

-

We both seem to have gas turbine background. Yours I think is in industrial application and more hands-on than mine. I think it is exactly as you say, or as Petraeus framed it : "jet engines with armours around them". And jet engines needs maintenance. The other thing aside logistics, I think is the military doctrine (how to use it). These are not going to be used (I think) in the same way the Russian used their tanks advanving toward Kiev. Abrams are powerfull machines but if misused, or without proper infantry support, they could be sitting duck as well. And this could be compounded by the maintenance requirement. When the U.S. forces were dashing toward Baghdad in 2003, unlike the 1991 Gulf War, they were advancing on a narrow path, which really exposed their flanks and overstrechted their lines of communications. The Americans could handle that given the training etc. and all their war planning. You are not going to see that level of complexity of operations with Ukrainians. Petraeus also talked about Abrams being the 'core' around which battalions and brigades are built. That notion of the tank serving as a 'backbone' to a brigade may be well understood in the West as a doctrine, but the Ukrainian military may not be there in terms of doctrine. So to me, it is less so about Ukrainian being able to operate these machine. They are afterall an extremely industrious folks. But more to do with their field commanders understanding how to use them. The last thing Pentagon wants it to see Abrams getting disabled and sitting duck around Bakhmut in an artillery kill zone.

-

Folks, I hate to break it to you, but Fairfax's performance in 2023 probably has a lot to do with how S&P500 performs in 2023. A 15-20% (Grantham style) drop on S&P500 by year-end, would probably have Fairfax rally to a healthy premuim to BV. A major bounce back at the indices level, would probably be a flat/modest gain for Fairfax. So what is your bet on S&P500 for 2023 ....

-

I love this line/expression. I got to try to use this more often. Which would probably apply to a lot of things.

-

Ehhhh ... What happened here, folks ... I thought we were talking about M1 Abrams

-

“The New York City taxi cab drivers are now bearish on Big Tech” ~ Dan Ives on CNBC

-

Every American general’s wet dream has been to see M1 Abrams roaming the fields of Eastern Europe. Even if they are symbolic to allow to more available Leopoldo get released. I think the purges in Kiev, the secret (not so secret) visit by CIA director and the tank approval are all linked. Message to Zelensky: clean up the corruption in your government. PS: There is a lot of good commentary on line about Abrams. It is clear that they would be “few months” away at the very least given all the logistics that is needed to support them vs the readily available diesel engine powered Leopolds.

-

They learned this from Jack Welch

-

In Canada, tipping has completely gotten out of hand since the pandamic. It was one thing to tip those who went out during the Dark Days to deliver food etc in 2020, it is entirely different thing to have the machine set in such a way that the 15% is now lowest of the three options. A place where I buy flowers (had to go to two different funerals) after telling them I was paying via credit, I was told I had to answer option on the credit card machine. What she meant was that I had to choose to tip on the machine for the funeral flowers !

-

Nothing to do with people getting away or not getting away. Donald Rumsfeld, Dick Cheney and George Bush all got away from it. The world didn’t stop turning. Support should continue (or not continue) for the right reason: geopolitical, humanitarian and economical (ramp up the war industry or not). The combination of these vs. alternative.

-

There is an interesting bit on why M1 are not suitable for Ukraine and why Leopold II are the best bet. M1 is indeed running on a gas turbine engine. Powered by Honeywell !! https://aerospace.honeywell.com/us/en/products-and-services/product/hardware-and-systems/engines/agt-1500 A shame though as those armoured beasts were design to operate in the battlefield of Eastern Europe fighting off the Warsaw Pact, and we are not going to get see that.

-

@hardcorevalue @giulio Thank you

-

Anyone seen this from 2014

-

hi i vaguely remember the $1000 figure by Prem. Do you remember if he meant US or CAD$ ? also is it normal for CEO to quantify an actual share price target. I know Brookfield does it with “plan value”, but based on framework.

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

^^^ I watched it only because I knew C Bale wouldn’t be in movie with bad writing. Yes based on a book but still writing and directing can be bad. I finished “Treason” the so-called “spy thriller”. OMG. Who wrote that thing. So cheesy, and predictable. Good actors and good budget but clearly the actors are just there to squeeze a fist full of dollars. Contrast that to “Tinker Tailor Soldier Spy”, that you need to watch a few times and still not catching the whole plot. https://en.m.wikipedia.org/wiki/Tinker_Tailor_Soldier_Spy_(film) -

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

“Pale Blue Eyes” with Christian Bale is a really good movie. Really well made, you really feel the pre-Edison look of it, even during the day time where most of the lighting comes from the sun when the scenes happens in a room. (surprisingly for Netflix) -

lol. Yeah. That is true. FIH own dry powder was used to buyback at $14 and $12. And I am heading less aggressively at $9. You just don’t know how low it will get.

-

The WW2 analogies are based on a snapshot point in time. If you add a time dimension to the analogies, a symblic Doolittle raid on Tokyo in April 1942 snowballed into Lemay firebombing of Tokyo in May 1945, some three years later !

-

I Need a Laugh. Tell me a Joke. Keep em PC.

Xerxes replied to doughishere's topic in General Discussion

-

FIH recent rise is a catch-up proxy for those who missed out FFH’ Q4 last year rally.

-

Romulan warbird de-cloaking off the coast of Hawaii https://www.cnn.com/videos/us/2023/01/19/coast-guard-russian-ship-off-hawaii-liebermann-cnntm-vpx.cnn

-

Russia’ massive multi-time zone landmass which was competitive advantage during Swedish, French and Germanic invasions is a liability in this current context of an enemy not interested to mount an invasion but to wage asymmetric warfare.