Canalyst

-

Posts

33 -

Joined

-

Last visited

Canalyst's Achievements

")

-

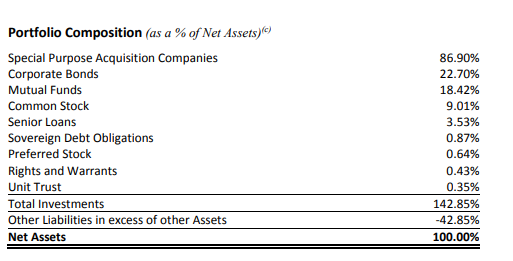

I have started looking more closely at Closed-End Funds. It seems like depending on the portfolio, you can buy a pretty good, levered spread at a discount. Like all discount to NAV plays, you may never see the discount close, but currently some of the yields on these seem to be both rich and reasonably safe. I recently initiated a position in BRW in my non-taxable that was heavily in cash from a bonus. BRW is managed by Boaz Weinstein's Saba, excellent write up here: (Boaz’s Curious Lure of Fat Dividends - Red Deer Investments) Most of the portfolio is SPACs that are going to get liquidated (2-4% yields), levered 40% while the CEF trades at an 8% discount. Portfolio from 10/2022 annual report: This is an interesting fund, and even if you aren't interested in owning a CEF, it is worth looking through some of the holdings for high-yielding or special situations. It has me digging in to some of the other larger CEF holding in here, as Saba is fighting proxies to liquidate after buying at deep NAV discounts. IRL (The New Ireland Fund) which Saba disclosed a position in in November of 2021, announced liquidation in October of last year and has closed an almost 20% discount to NAV in that time period. BRW should file their next portfolio update towards the end of March, and it will be worth taking a look at how things have changed. Any experienced CEF investors on here have any thoughts on the space, or if there are more worth looking more closely at? Most recent annual report here: saba-capital-income-opportunities-fund-ar-20221031.pdf (alpsinc.com)

-

Anyone know if any longer form article about Trott or BDT?

-

Have been adding VNQI to my non-taxable account. Portfolio is heavily weighted to Japan with some (~13%) exposure to HK real estate with the rest in developed Europe and UK. It's inverse correlation with the weakening Yen has shot up during the Yen's collapse, and I bought it because a) I am partial to REITs and b) it seemed like a reasonably levered way to play the potential for a dollar reversal. Is this the right way generally to think about international RE? If your thesis is that foreign currencies will at some point strengthen, but still face inflation, is RE a better way to get international exposure into your portfolio?

-

I'm wondering if anyone knows of any good investment letters/primary writings about Brazil. Not concerned if they are dated or not, in fact, the older the better in some sense, just trying to get a better historical context of investment in the Country.

-

Alternative Asset Managers Getting into the Insurance Business

Canalyst replied to Canalyst's topic in General Discussion

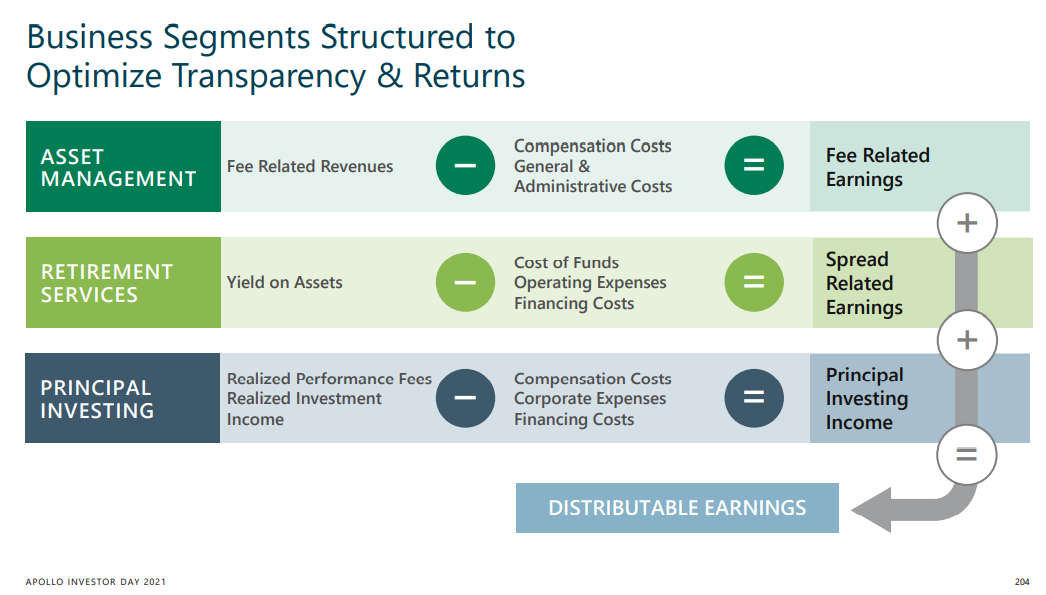

Great points, I would highly recommend watching Rowan's talk from the investor day. The below slide from Kelly's presentation was especially helpful in terms of how new reporting will look but also for the strategy in general

-

Alternative Asset Managers Getting into the Insurance Business

Canalyst replied to Canalyst's topic in General Discussion

Despite nominally similar business models I find the overall strategies of BAM, BX, KKR, APO and CG to be fairly differentiated. BAM & BX are fundraising machines and successfully going "down market" to retail/HNW through various products. KKR and CG are still primarily institutional managers with some retail product either via BDC or feeder funds. Then APO which is kind of mid-transformation into a permanent capital spread business with diversified funding sources. I think the intra-PE sales are representative of those strategies and shifting asset bases to have alignment with funding sources. -

Alternative Asset Managers Getting into the Insurance Business

Canalyst replied to Canalyst's topic in General Discussion

Athene has essentially been an Apollo property since its inception, MDD ROE and 20% 5 CAGR of assets -

You could do worse than simply betting against any "next Berkshire/Warren Buffett" subject in recent years but the alternative asset managers pushing in to insurance remains interesting to me. Apollo/Athene merger is probably the biggest in terms of strategic importance, Brookfield also moving more in this direction with the addition of American National. At the Goldman US Financial Services Conference at the end of '21, Rowan put the strategy succinctly: "If you think about the alternatives business generally, in the private equity business, everyone understands it, 20% above 8. In the nontraded BDC, the nontraded REIT business, 12.5% over 5 or some metric like that. In the retirement services business, I get 100% over 2.5, but I have to put up $0.08 in capital. Now that $0.08 in capital earns 15% rates of return. So to your point, I can decide whether to hold all that myself or I can through ADIP allow my limited partners to take 2/3 of it." These combinations create a larger permanent capital base, but they come with greater regulatory scrutiny and limitations. They are also generally commodity businesses that on their own trade at low multiples, especially relative to "pure" alt asset managers. I guess my question is how are people going about valuing these? SOTP doesn't seem appropriate, but neither does counting the insurance flows as simple AUM growth. Do companies like Apollo run the risk of turning into financial conglomerates that trade a perennial discount?

-

Next Thirty Years - Real Estate or Equities?

Canalyst replied to valueinvestor's topic in General Discussion

As Gregmal alluded to, I believe the real attraction to RE is that there are few (maybe none) places where man-off-the-street can get 4x leverage at close to prime rates. This can lead to tremendous compounding, but also occasional disaster. If you are earning and saving, it's hard not to make a case for REITs where you can be buying across a cycle without sacrificing liquidity. You can even simulate the leverage through moderate use of margin or ITM options. Of course, you don't get the tax advantages of direct RE ownership, but I think those are relatively expensive when you consider the headache of being a sub-scale landlord.