Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

he certainly feels the same way

-

Good episode. Talks about a variety of Berkshire related topic. it is interesting that Josh Brown although has heard of Markel, doesn’t know much about. The FFH and Markel crowd are really flying under the radar.

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

If you add Blackberry’ market cap to that of Apple, you get 2.77T -

great stuff

-

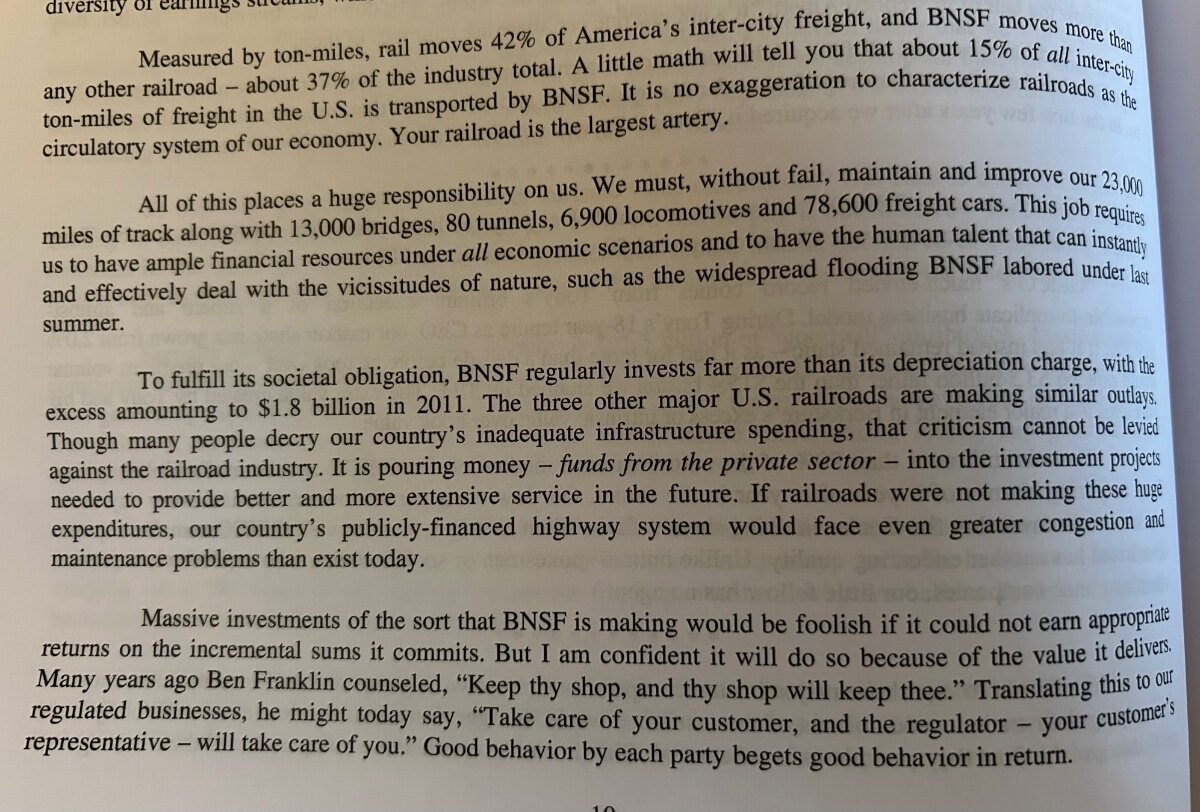

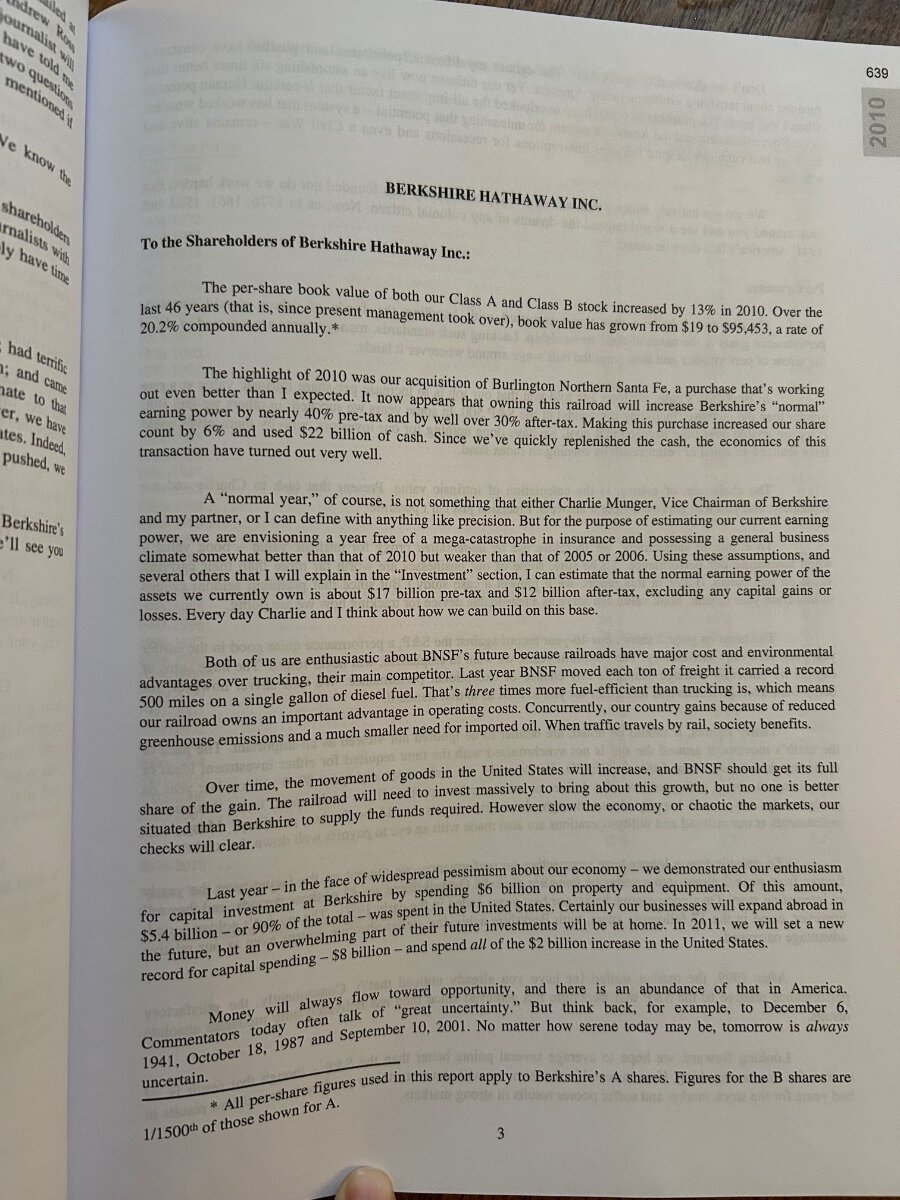

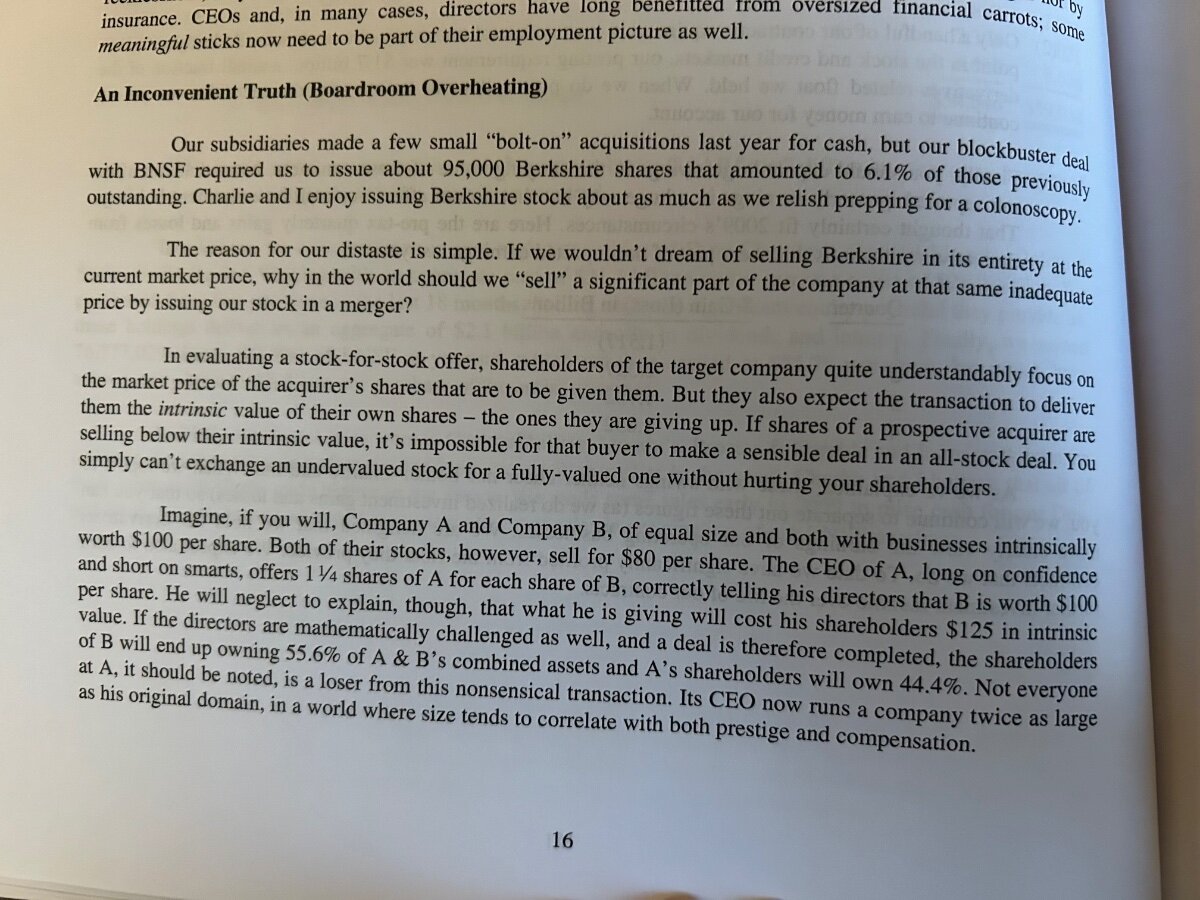

showing off from my new book. Excerpt from 2009, 2010 and 2011 letters on BNSF. $22B in cash + 6% of the company Excluding the stake they already had. Did Berkshire gave away too much by issuing away 6% of Berkshire. That is $54 billion on a market cap of $900 billion todays price.

-

Public Company Share Repurchase-Cannibals

Xerxes replied to nickenumbers's topic in General Discussion

MGM International "We started the quarter with great momentum across our businesses. While we were faced with a difficult cybersecurity issue in September, our employees rose to the occasion with incredible resilience and determination. With the incident now behind us, we are a stronger company having been through the challenge," said Bill Hornbuckle, Chief Executive Officer and President of MGM Resorts. "Going forward we have much to be optimistic about with Formula 1's inaugural Las Vegas race next week and early next year the debut of the MGM Collection with Marriott Bonvoy followed by the Super Bowl. Beyond these catalysts, MGM China is performing exceptionally well, and we have a pipeline of development opportunities including New York and Japan alongside the growth and development of our international digital business and BetMGM." "We continue to view share repurchases as an attractive opportunity to return value to our shareholders," said Jonathan Halkyard, Chief Financial Officer and Treasurer of MGM Resorts. "Year-to-date, we have repurchased approximately $1.7 billion in stock. Our buyback program totals $6.2 billion since the beginning of 2021, reducing our share count by over 30%." https://investors.mgmresorts.com/investors/news-releases/press-release-details/2023/MGM-RESORTS-INTERNATIONAL-REPORTS-THIRD-QUARTER-2023-FINANCIAL-AND-OPERATING-RESULTS/default.aspx IAC reflection on the name "Our largest holding, MGM is a keen beneficiary of growth in the travel & leisure sector, which has materially outpaced broader consumer spending generally for the last 20 years. Consumers’ ever increasing time spent on social media has elevated exposure and access to new experiences, making the top of the travel & leisure funnel – FOMO – only grow. As social currency moves away from ownership (less shareable online) towards experiences, MGM has gained. MGM is also the market leader in Las Vegas, which showed the world again this past weekend why it’s the global center for sports and entertainment experiences: nearly every major live tour, show, fight, race, competition, chef, and soon to be every major league sport, has a Las Vegas outpost, and MGM often plays host. Even as post-pandemic tailwinds fade, the shift from goods to experiences is a decades-long trend, not a fad, and the increasing premium on live events and experiences makes MGM a bona fide trophy asset. But the MGM secret seems to be safe with us, as the company has been able to buy back 35% of its shares outstanding since we got involved, still at incredibly attractive prices relative to earnings, especially for something so unique. We owned nearly 20% at the end of 2023 and, with continued repurchases, could still own more before the secret gets out." -

Why did so many smart investors miss making a killing on BRK stock?

Xerxes replied to Viking's topic in Berkshire Hathaway

I first owned BRK a year or so before Covid, increased to what I could and kept ever since. The pushback that I see from most people I talked to outside this forum vis a vis BRK is that “it is too late” “I can get better return on my own””the chairman is too old, what if” what i alway explain is that they should look at “risk-adjusted return” and not just “return”. Yes Nvidia did a 10x but could/would you put 45% of your entire wealth into it as a non-semi conductor insider. So if only say 5% goes to Nvidia, what goes to the rest of 40% and is that overall net return enough to match an easier pick like Berkshire with a 45% weighing. -

2009 !? That is one year before Satoshi Nakamoto posted his/her/their last post on Bitcointalk Forum. and then poooof disappeared … just like that plot thickens !!

-

^^ every time i have read anything on YAHOO News concerning this war .... it was always a "blow to the Russians". Even CNN (except for Fareed) gets on my nerve sometimes when they invite those overexcited retired general to "opine". I much prefer the good professor on Sky News or Koffman.

-

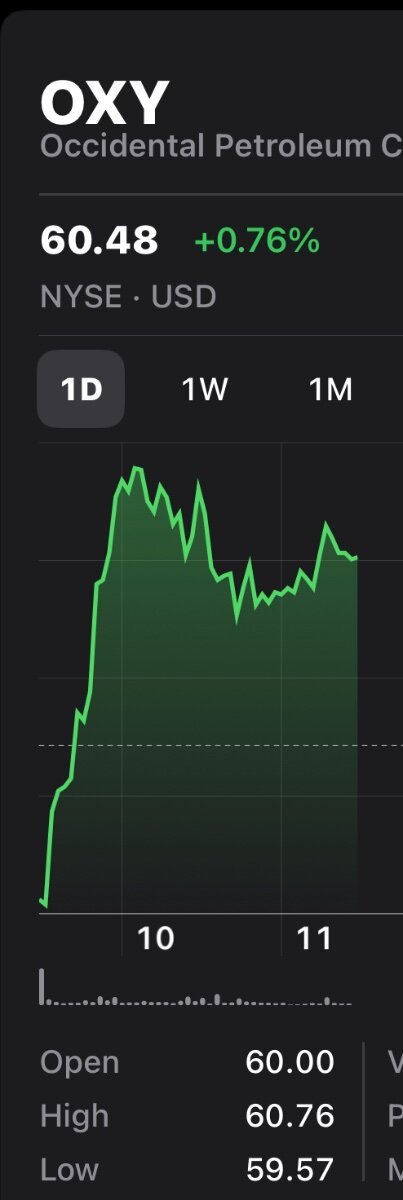

Clearly Berkshire was sold to generate funds to buy Occidental

-

thank you. I agree with the last paragraph.

-

@gfp Was wondering if you had any theory on why BNSF was dividend out of National Indemnity to BRK’ proper balance sheet. Is it about the roll-up of liabilities that the insurance outfit might have, capping exposure to the railroad. Any thought ? https://www.bnsf.com/about-bnsf/financial-information/pdf/8k-20231005.pdf

-

Thanks @LearningMachine very clear

-

Andrew Wilkinson Thirst Post/Book

Xerxes replied to TorontoChaosTheatre's topic in General Discussion

Do trust a Canadian, but verify -

If BHE and railroad needed some qualitative “kitchen-sinking” under the current incumbent CEO, rather than future CEO, perhaps the same can be said of the dividend. No one is going to argue with Buffett if he re-institute the dividend after 50 years or so of not having it. Or at least he can create a runway of expectations for it. But leave the final call to future management.

-

I recall you mentioning that before. Yet insurance is also be a form of liability to the whole group. Even if the risk is right sized etc. I find it interesting that both this letter and last year’s letter, he shared fond memories of Coka Cola and American Express. Just cool brands. Not much to do. Unlike BNSF, BHE etc

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

Started “Masters of the Air”. outstanding. just have to endure the first 10 min which was all 90210 stuff. But then it is the real deal. -

I don’t even know why people ever thought he would buy the whole thing (OXY). When he bought 30% of the company at no premium. He has been clear in 2020 letter that broadly speaking he won’t pay control premium. And he is happy to be a large minority shareholder when it suits him. The question would be, what he would gain from being a full owner of Occidental (that he does not get by being just a major shareholder). And is that aspect worth the control premium.

-

The boosters for years were saying BHE is where you could just park that excess surplus get that 10% regulated return. Amazing etc. look at that negative tax rate. At the end of nothing is guaranteed with government and regulatory environment. I am not even sure I understand the full picture. I guess Greg did do the right thing to liquidate his BHE and redeploy into the greater Berkshire. in any case, I trust the management to continue navigating the headwinds.

-

I think the Semper 2023 letter is released the day before BRK letter. So coming soon

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

a fair point if I was talking about the season finale. This is just a random scene mid-season. -

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

the last scene when they burned the house down and realize they don’t have the car keys, and have to walk in the middle of snow, kind of reminded me of Pauli and Christopher from Sopranos getting stuck in the forest in the middle of winter. -

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

I think for True Detective it was depressing but perhaps that was the intent. After all, it was in a small town in the middle Alaska after that the “last sunset”. I personally liked it. what is not clear yet to me what was the back story about the “tongue” How it ended and the number of people involved reminded me of Murder on Orient Express. Very cool -

2024 AGM Meeting poll - are you attending

Xerxes replied to This2ShallPass's topic in Fairfax Financial

I was there in 2018. You just walk in and I think they took my name down. didn’t have to prove or show anything. -

Public Company Share Repurchase-Cannibals

Xerxes replied to nickenumbers's topic in General Discussion

thank you @FCharlie this is very helpful.