nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

No question, the TRS was genius. I have only had a cursory look (a while back) and couldn’t find any examples of companies employing the strategy so I think it is also unique. Slightly off topic and hopefully the timestamp works, but I think those of us here that concentrate definitely share a similar philosophy to Druckenmiller where he was paraphrasing Andrew Carnegie:

-

The question of concentration is always a juggle. But if you believe in capital allocation machines like FFH, you’re getting more than adequate diversification. I’m more than comfortable holding large positions and copping the conglomerate discount which, in my view, is the margin of safety. We know Bradstreet is a 3–4 sigma event in fixed income. The equity positions, which I think are just as, but perhaps more important, over the long term, are finally getting some recognition in the market. But scorekeeping on a quarterly basis is no reflection of true IV. Anyone following the undelying IV evolution of the equity book knows there’s a lot more upside ahead. This is perhaps slightly at odds with my view that the TRS position should be wound down, but that view is more about risk management. In a deleveraging event, there’s nowhere to hide, and you’d hate to see cash drained to shore up the TRS just as the market is offering up gems. It’s an optionality issue, no doubt the asymmetry has worked to date but an outlier event could undo a lot of this good even if the IV of Fairfax remains constant.

-

5844 Kyoto Financial Group. It’s run on a bit since I wrote it up. Last buy from my end was a couple of months ago. There’s always the argument that it deserves a holding company discount. Hardly lit up the board but cheap is cheap, especially if you like the Kyoto based investments Nintendo, Murata, Nidac etc. there is always the possibility of some NIM expansion. https://thecobf.com/forum/topic/21225-5844t-kyoto-financial-group/#comment-604254

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

https://x.com/historyrock_/status/1948193918891311519?s=46

-

I am sure it will get taken down but this is pretty funny IMHO. Especially in the context of Colbert and Paramount. $1.5bn over 5 years well spent IMHO.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Beats me, but perhaps music is the elixir of life after all. Works for a few of us, I’m sure. “…and still jostling with Sharon”, that’s no mean feat! -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

@DooDiligence thanks for that. RIP Ozzie. Never was much of guitar player but the intro to Killer of Giants was a passion project for a while This version off the DVD was one of the better IMHO. The Jake E Lee solo is not bad either https://drive.google.com/file/d/1n7WF9V265OmNYRaXlsHvyc564nn09ZJV/view -

Each to their own, but I find it hard to get too excited about a ~20% ROE insurer at 2.8x’s book. I think Bill agrees hence no buybacks in Q2 and returning capital via specials etc. I think with WRB it is priced for much higher ROEs, hence the sell off. Great company and Bill is a legend. The obvious answer is to be using their shares as currency. OTH an ~18% ROE insurer at 1.6x understated BV I think you can make a case for

-

+1 that was my pick too. I think I have a better chance at predicting book value in 5 years time than any particular quarterly result but a useful exercise nonetheless. Rotated half my Eurobank into Fairfax a few days ago. Still think there is decent upside in Eurobank but like Fairfax’s prospects longer term (decades). Div tax and margin requirements were considerations too.

-

Slightly OT, but a nice call out on Fairfax paper

-

Depending on your timeframe, some useful price discovery

-

Thanks for posting this, what a masterclass. Hari navigates an incredibly complex web of infrastructure growth, regulatory frameworks, urban connectivity, and stakeholder diplomacy with the calm authority of someone who not only understands the system but is actively shaping it. The interview really underscores why BIAL is the natural lead contender for the second airport. Such diplomatic finesse, there’s a lot of nuance in what he’s balancing, and yet nothing feels reactionary. Just clear, long-term planning backed by competence and calm execution. Plenty to digest here. I’ll definitely be rewatching.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Agree. For me, she defined entire genres, not to mention looks and scenes. Post-punk and goth rock wouldn’t be the same without her. The ripple effect of her influence is still felt today in so many artists, Karen O is just one of the many who stand on her shoulders. A couple of my favourites, The Smiths and Joy Division, were also greatly influenced by her uncompromising style and sonic boldness. She didn’t follow trends, she made them “Without Siouxsie and the Banshees, there would be no Smiths.” Morrissey “We were very inspired by Siouxsie and the Banshees. We always looked up to them… they were the ones doing it right before us.” Peter Hook -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Spellbound is one of those ageless bangers for my money. Not bad for an early 80's video, too, along with some great comments. When that Time Machine finally comes along, the chance to see Robert Smith playing back to back with both The Cure and Siouxsie and The Banshees would be pretty high on my list. This performance from 1983 Albert Hall is pretty good: S&TB with Robert Smith A short doco on the period: When Robert Smith was a Banshee -

Nice post. I kind of chuckled at this statement, in a good way. I am sure many of us a saw/see this as debt dressed up as equity so agree it definitely falls under the leverage category. As you rightly point out it was a win/win for all parties. Another example of Fairfax’s creativity but one that is only possible with mutual trust.

-

Yep, all sorts of fascinating unintended consequences. https://timeleft.now

-

Great photos, it looks like you aced the weather. Congrats

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

+1, it’s a good hunting ground for new music. -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I recently came across the Pinkpop Archive Youtube Channel. An amazing collection of many of my favorite 90’s bands (as well as some later stuff too) all pro shot at the festival in the Netherlands. An amazing collection for those that were into the scene then. Brought back some great memories and well worth checking out. This Rage Against The Machine set is just brilliant. Damn Zack went hard, consider myself lucky to have seen RATM a couple of times but like all things when you are young kind of took it for granted. A truly epic era for live music. -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

A short KEXP set by Amyl and the Sniffers. I did get a chuckle when Amy said “Now you will have to excuse me my voice is a little ‘horse’, so hopefully Elon Musk doesn’t try to snort it…(then turning to the audience) ….it was a ketamine joke” Aussie humour lost a little in translation -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

A must for TOOL fans, pro shot magic. As one of the comments says this is like a Bigfoot sighting . Edit: Looks like most of the “Back to the Beginning” sets are now showing up on Youtube in similar quality. An epic tribute to Ozzy. Happy days https://en.wikipedia.org/wiki/Back_to_the_Beginning Edit: The Slayer set is epic. Tom Araya's vocals sound as good as ever. Edit: The drum off between Travis Barker (Blink 182), Chad Smith (RHCP) and the human octopus Danny Carey (Tool) was probably worth the price of admission. Human Octopus for the win. -

Good one, as the shares were issued from Treasury this makes sense

-

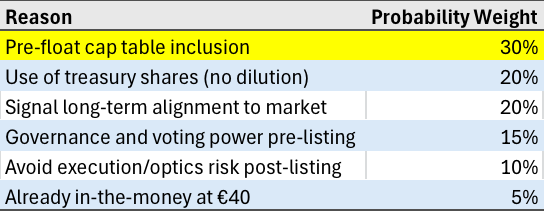

Thanks for this I must confess I find it a bit of a head scratcher. There’s no regulatory or listing requirement that I can find that mandates conversion prior to admission. Logically, you’d expect them to retain optionality, collect interest, keep a senior claim, and convert when the equity rerates post-float. These came up as possible reasons after polling various AI sources, none of them overly convincing: Does seem strange as the exchangeable were initiated in March 2025 and the LSE listing was well and truly on the cards then. I also can’t see a tax angle either. So perhaps it’s a simple as optics. BTW I think that closing price in your post may be a bit early but will be the case at some point

-

Thanks, an amazing story for Greece and Fairfax. Though not without some heartache and pain considering the relatively easy win with BoI. I loved this anecdote: Alexis Tsipras, the leader of the Coalition of the Radical Left, or Syriza, won power in 2015 with a promise to tear up the bailout agreement. After months of impasse with Greece’s fellow euro members, he called the referendum on whether to stick with the terms. Watsa met him and asked him straight. “I said to him, ‘you know, if you want us to leave, we’ll leave, that’s fine,’ and he said, ‘No, I want you to stay, you’re exactly the kind of investor Greece needs’,” Watsa recalled.

-

it’s only a number, but worth a post