nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

One pleasing development in Atlas’s Q2 numbers: “The consolidated weighted average interest rate for June 30, 2025 was 6.02% compared to 6.93% at June 30, 2024. The weighted average interest rates for the vessel leasing segment and Atlas Corp. (on an unconsolidated basis) were 6.03% and 7.13%, respectively, for the three months ended June 30, 2025 (June 30, 2024: 6.93% and 7.13%, respectively). This seems to be driven by a smarter capital mix. The company has quietly retired some of its most expensive finance leases and term debt, refinanced into lower-spread sale-leasebacks, and leaned more on long-dated secured notes with coupons as low as 3.92%. With floating-rate costs cushioned by hedges and SOFR easing from late-2024 peaks, the debt stack now carries a lighter interest burden. This shift suggests Atlas has a bit more financial flexibility than I’d previously given it credit for. On APR we must be getting towards the end of the make good. Decent YoY decline: “Fairfax remains a counterparty to certain indemnification and compensation arrangements related to the acquisition of APR Energy which occurred in 2020. During the three and six months ended June 30, 2025, the Company received $12,000,000 and $12,000,000, respectively (2024 – $42,500,000 and $42,500,000 respectively) from Fairfax related to these indemnification arrangements.” Happy to see that one in the rearview mirror!

-

Agree, tiny baby steps but good to see Japan is on their list of hunting grounds

-

I’d actually add a third reason to that list, the compositional change in Fairfax’s underwriting portfolio. I am sure you have covered this before but it’s worthwhile reiterating that over the past decade, Fairfax has shifted materially toward global specialty and reinsurance via Allied World, Brit, and Odyssey, and expanded into high-growth regions like the Middle East through Gulf Insurance. These segments are often less correlated with the mainstream North American commercial cycle and can pivot more quickly to profitable niches. That means even within underwriting, Fairfax’s risk is more diversified, by geography, product, and client base, than it was in the past, which further reduces its vulnerability when the current hard market turns. I have a hard time quantifying exactly what this means in terms of combined ratios or defensible gross written premium, but I think it’s lazy thinking by analysts to assume Fairfax has no edge when the market turns soft. The combination of global specialty, reinsurance, and high-growth international platforms gives Fairfax levers that many peers simply don’t have, both to protect margins and to redeploy capital into better opportunities as conditions change. Q1 2025 – Peter Clarke: “Our insurance and reinsurance companies are in great shape, writing over $33 billion of annualized premium worldwide. We benefit greatly from our scale, diversification and exceptional talent and experience of our long-serving presidents and teams that run our insurance and reinsurance companies, and nothing was more evident than that than this quarter.” “Our international operations now make up approximately 20% of our total gross premiums and the long-term prospects of our international operations are excellent and will be a significant source of growth over time, driven by excellent management teams, underpenetrated insurance markets and strong local economies.” Q2 2025 – Peter Clarke on pricing trends: “Just on the pricing front, I think it depends on each company and by geography. But generally, the theme is that on the property business, rates are coming down in some countries, low to single rate increases. But in many, it can be down low single digits to up to 10%. While on the liability side in casualty, we’re still seeing strong rate and anywhere high single digits to up to 20%. In Canada, Northbridge, their commercial lines are about mid-single digit in total with property down, casualty up. Same at Crum & Forster, their liability business is up about 7.5%, property low single digits. Odyssey on the reinsurance side, property is down single digits, casualty up single digits, and probably where we’re seeing most of the rate — negative rate pressure, that’s in Lloyd’s at Brit and Ki, where we’re seeing small single-digit decreases. So at a high level, that’s where it is, but we write $33 billion of premium, and we benefit greatly from that diversification. So there may be some lines that are going down, some lines going up, and we have the flexibility to be able to grow. And of course, number one is discipline. Underwriting focus is #1 for all our companies, and we take a long-term approach. So there’s no top line focus at any one of our companies.”

-

Adam Waterous is the shining example for my money. I am tipping that, collectively, their WEF exposure will be a top 3 holding by 2030. In the Eurobank and Poseidon league, on pure free cashflow it’s probably in spitting distance now.

-

MS note on Metlen attached, they have a PT of €66 and forecasting: Mid-term EBITDA target €1.9–2.1bn (up from €1.1bn in 2024). ~60% of growth from core Energy, Metals, and Infrastructure/Concessions. ~40% from new ventures – Defence, Circular Metals (recycling), and Critical Metals (gallium). “Our new mid-term EBITDA forecasts of €1.8-1.9bn for 2028-2030, imply a solid 3-yr EBITDA CAGR (2025-28) of 16% and offer 11% average upside to consensus. We incorporate growth initiatives such as the €150mn/yr EBITDA target in Defence, but are more conservative on: (1) Circular Metals as we bake in ~€110mn EBITDA (50% of target), allowing good upside as more visibility emerges, and (2) Integrated Utility as we are ~€100mn below guidance in 2028-2030 (~€490mn vs €590mn) given the volatile nature of energy markets. We project ROCE (post tax) and ROE averaging 16%/20% in 2028-2030 respectively, with new initiatives such as Defence offering an impressive 70% ROCE (post tax, MSe).” “We are Overweight with a PT at €66 on a DCF-based approach, while an illustrative peer-based SoTP yields an even higher valuation of€78-93/sh. On this basis, Metlen's Enterprise Value would roughly equal the valueof the Energy segment.” METLEN_20250807_1545.pdf

-

Bless his cotton socks, Brett does long term shareholders an immense service

-

@Viking, thanks for the hard work pulling the pieces together. Based on the current underwriting profile and reserve redundancy, a 15% ROE for 2026 has a high probability of being achieved. Even without leaning on TRS marks, the combination of disciplined underwriting, steady investment income, and clever capital deployment comfortably supports mid-teens returns. The reserve cushion acts as both a shock absorber and an earnings lever, while accounting changes under IFRS 17 may provide a modest smoothing effect in a flat-book scenario. That means Fairfax should reach 15% without unusually benign catastrophe years or extraordinary investment gains. Upside exists if reserve releases are larger, capital redeployment accelerates, or the TRS overlay delivers again. Looking further out, the more important test will come in a soft P&C market. The current hard market makes combined ratios look exceptionally strong across the industry, but the next leg in Fairfax’s multiple expansion likely depends on demonstrating through-cycle CRs and proving that underwriting discipline holds when pricing power fades. We need to be careful what we wish for, but a soft market may ironically be a welcome development for long-term Fairfax shareholders. It would give the market the proof it needs that Fairfax’s underwriting engine is built for all seasons and that could be the real unlock for sustained re-rating. I am part way thru Marc Adele’s fantastic book on C&F. This passage made me laugh out loud: “Prem is a value investor in the school of Ben Graham, who famously recommended buying cigar butt companies (his analogy for finding value in seemingly unattractive situations). A better analogy for P&C insurance companies in the late 1990s would have been cigar butt companies where the butt had been dropped in toxic nuclear sludge, rolled in asbestos, then stepped on a couple of times for good measure. Consequently, Fairfax acquired a few clunkers.” It directly follows with this rather salient passage “Even after the massive restructuring — and all the capital Xerox pumped into it — C&F was still one of those clunkers. The company continued to have reserve issues, but probably more critical was that C&F had been stripped of its specialty businesses and the remaining regional middle-market package business had suffered years of neglect. The customers, agents, insureds and employees had been battered by years of restructurings and re-underwriting. It was a tough starting point.” There’s still a lot of scar tissue associated with Fairfax even if it’s fading. In my view, that lingering caution is part of why there’s still a margin of safety here.

-

Not really a Fairfax "position" but attached are some notes on Fairfax Digital Services run by Sanjay Tugnait. Prem had this to say in the 2024 AR: In only the third year of its existence, Fairfax Digital, led by Sanjay Tugnait, continues to make great progress working with our companies building digital solutions throughout the group. In 2024, working with Eurolife and Colonnade, in partnership with a leader in global visa and consular services, we have launched a pioneering Gen AI platform for embedded travel insurance, starting with travelers to Schengen countries. Working with Eurolife and LTIMindtree the team developed AI-driven tools like “Ask Me Anything” and “Case Summarization” improving customer and employee experiences. Fairfax Digital also facilitated cross border digital payments working with Eurobank, revolutionizing the process of international money transfers from Greece to India. In 2024 Sanjay was also appointed co-chair for the Sustainability Task Force at the G20, Startup 20 in India. Another great year establishing digital solutions throughout Fairfax, with many other initiatives in the pipeline we are very excited about the future of Fairfax Digital. While it’s an internal division, it reminds me of what we tell our Scouts, you learn by doing. Fairfax Digital Services feels like more than just a support unit; it’s quietly becoming an incubator. At the very least, they’re solving real-world problems that plague financial services globally. And in some cases, like the launch of what they claim is Europe’s first agentic AI platform, they’re not merely catching up; they’re pushing into territory with a genuine competitive edge and business potential. It must be breaking Fairfax’s capital allocation heart to sell down Eurobank into the buyback just to stay under regulatory thresholds. Fairfax Digital Services.pdf

-

Marc Adee has been doing the rounds on the book. A couple of recent interviews: https://cpcusociety.libsyn.com/unpacking-200-years-of-insurance-history-with-marc-adee

-

It’s my understanding that even if Trump replaces Powell, he can’t immediately force the Fed to cut rates. Powell’s term runs to May 2026, and even then, Trump can only nominate a successor, Senate confirmation isn’t instant (even if our friends in congress are captured). More importantly, he can’t remove or replace the Fed’s regional presidents, who hold 5 of the 12 FOMC votes. The other Governors are presidential appointees but can only be replaced by yes men as the seats become vacant. So while Trump can pretend, he can’t actually snap his fingers and cut rates. What he can do is spook the bond market, especially the long end. If markets fear politicised rate policy or fiscal largesse, yields might jump despite the rhetoric. Having listened to Bradstreet at the dinner and watching him over the year's I am extremely comfortable with the moves he makes. It’s the one aspect of Fairfax that I don’t worry about.

-

Some coverage of Metlen’s opening on the LSE https://www.londonstockexchange.com/stock/MTLN/metlen-energy-metals-plc/company-page

-

Extra holdco liquidity gives them a bit more optionality/buffer too.

-

Easy, Nidar Iqbal does a pretty good job even if she has been a bit conservative. I know there is a reticence among some board members to consider analyst reports. I certainly don’t rely on them, but I find them helpful as prompts for further primary research. What’s been particularly useful is comparing her projections to actuals over time, it gives a sense of how Eurobank’s management guides versus what actually transpires. She’s not infallible, but as a sanity check or to highlight blind spots, she’s more useful than most. Eurobank is still optically cheap, so even if there is some further NIM compression it’s priced in. I think many of us are also watching the evolving tie-up between Eurobank, LTIMindtree, and Fairfax Digital Services. What began as a multi-year IT transformation contract now looks more like the early scaffolding of a deeper strategic alignment. Eurobank is leveraging LTIMindtree’s Temenos expertise and India-based delivery capacity to overhaul its digital backbone, modernizing core banking systems, boosting efficiency, and accelerating product innovation across Greece, Cyprus, and other European operations. “Temenos, for context, is a leading global provider of core banking software used by over 3,000 financial institutions worldwide. It powers everything from account management and payments to digital channels and compliance. Implementing Temenos allows Eurobank to consolidate legacy systems and operate on a modern, scalable platform that supports real-time banking, faster time-to-market, and a far more agile digital experience.” What’s more intriguing is the role of Fairfax Digital Services. This isn’t just a back-end integrator or passive stakeholder, it’s functioning as a strategic enabler, effectively bridging India’s digital delivery capabilities with Europe’s banking modernization needs. The establishment of a dedicated Global Delivery Center in Pune and the launch of a digital innovation hub in Cyprus suggest this isn’t a one-off project, but a long-term platform. Early days, but reminds me that I need to to do a deeper dive into Fairfax Digital Services

-

MS with a short note (attached) on Eurobank’s Q2. They maintained both their recommendation “overweight” and PT €3.53. Note attached. @Viking thanks for the very thoughtful post above. Eurobank has a very bright future EUROBANK_20250731_1633.pdf

-

Agree, quality/reliable recurring is the next step in this dance.

-

Some key quotes from the Eurobank call (attached). A pleasure to listen to these guys, the CC always gives color that the interim report lacks Financial Performance Highlights CEO Fokion Karavias on strong results: “Eurobank reported robust financial performance in the first half of 2025, achieving an adjusted net profit of EUR 711 million and a return on tangible book value of 16.6%.” — Fokion Karavias, CEO On revised loan growth and return targets: “The strong pipeline allows us to revise upwards our full year loan growth target from EUR 3.5 billion to EUR 4 billion.” — Fokion Karavias, CEO “Consequently, we anticipate that the return on tangible book value will exceed the initial annual target of 15%.” — Fokion Karavias, CEO Dividend and Capital Strategy First-time interim dividend: “The strong first half performance allows us to align with other European banks policy by introducing for the first time a 2025 interim cash dividend of EUR 170 million. This is EUR 0.047 per share to be distributed in the fourth quarter.” — Fokion Karavias, CEO On payout ratio guidance: “We reiterate our commitment for a payout ratio of more than 50%.” — Fokion Karavias, CEO Net Interest Income Guidance Maintaining targets despite ECB rate cuts: “For NII, we have run a top-down exercise some weeks ago. And based on that, we reaffirm our initial target of EUR 2.5 billion, even assuming the ECB terminal rate reaching 1.5%.” — Harris Kokologiannis, CFO Regional Growth Commentary Greece’s lending momentum: “Let me remind you, I’m sure you have seen the data based on the ECB 2025 – May 2025 data, the credit growth in Greece and the private sector has been the fourth highest in the euro area.” — Fokion Karavias Bulgaria euro adoption and NII impact: “In Bulgaria, we expect about – if I recall correctly, roughly EUR 1 billion of liquidity to be released because of the reserve requirements. So this is going to boost the NII ’26 onwards.” — Fokion Karavias Asset Quality and Cost of Risk Stable credit environment: “Asset quality remained resilient for another quarter with the NPE ratio decreasing to 2.8% and coverage exceeding 90%.” — Fokion Karavias No change in provisioning guidance: “We do not expect any changes to the cost of risk guidance of 60 basis points for 2025.” — Fokion Karavias, CEO Q2 25 EGFEY - Transcripts.pdf

-

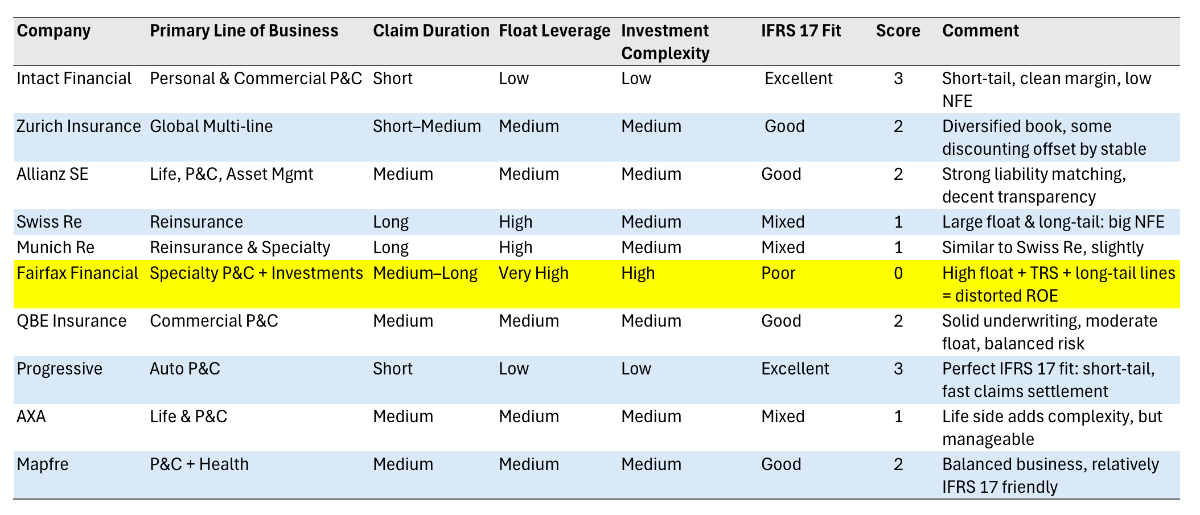

The more I think about it, IFRS 17 probably obscures more than it reveals, at least when it comes to Fairfax, and especially in the short term. They’ve been running high float leverage, and during a growth spurt like they’ve had over the past few years, the distortion is amplified. That $903m net finance expense is a good example. It’s not a cash cost, and it doesn’t reflect poor performance, it’s simply the accounting unwind of discounted future liabilities. But it hits the P&L hard, while the returns Fairfax generates on that float are real. The result is a distorted picture of true earning power. It reminds me of how the excess of fair value on investments quietly builds but is not yet reflected in reported book value. To gauge true performance you need to the annual change in adjusted book value + divs. Even then you don’t fully capture the true change in IV because many of the positions are not marked. Anyway, both effects are real, but delayed. They make Fairfax look “less impressive” (hard to believe) in the short term and more mispriced as a result. Especially if you’re anchoring to P/B and ROE to frame valuation. I guess that’s why we put in the work to understand it. The table below is a qualitative attempt at gauging the two handles of NFE - float growth and discount rate: The table below is a rough indication of who likely does better short term (3-5 yrs) under IFRS 17 but ultimately the economic strength of good capital allocation makes the NFE less of an impost. So for the moment consider it another margin of safety for Fairfax.

-

Eurobank reported Q2. https://www.eurobankholdings.gr/-/media/holding/omilos/grafeio-tupou/etairikes-anakoinoseis/2025/2q2025/2q-2025-results-presentation.pdf A quick round up: The Good TBV/share €2.38 (+7.6% YTD, post-dividend) SEE diversification paying off: 53% of adjusted net profit now from international ops (€374m), with Cyprus +42% YoY and Bulgaria +10.6% Fee income acceleration: Commission income surged 28.9% YoY to €364m, driven by wealth management and CNP Insurance acquisition Credit quality momentum: NPE ratio improved to 2.8%, coverage at 92.8%, net NPEs down to just €0.1bn Strong capital position: CET1 15.5%, CAD 19.8%, MREL buffer of 290bps above target Organic loan growth: €2.2bn in 1H25, with strong pipeline across all markets Shareholder returns: 2025 interim dividend of €170m (~4.7 cent/share) declared, following 2024 DPS of 10.6 cent/share Bargain acquisition: €38m negative goodwill from CNP Cyprus deal - got assets for less than fair value (but one off, so kind of bad in terms of masking earnings) The Bad Profitability decline: Adjusted net profit down 2.9% YoY to €711m; EPS fell to €0.19 vs €0.20 NIM compression accelerating: Down 32bps YoY to 2.51% as deposit repricing outpaces loan adjustments Cost inflation biting: OpEx up 34.3% YoY (6% like-for-like); cost/income ratio deteriorated to 37% Margin defense struggling: Deposit betas remain elevated while loan repricing lags ECB cuts Things that make you go hmmm Cyprus profit pressure: Core PPI down 19.5% YoY despite strong market position - rate sensitivity higher than expected Operating leverage reversing: Revenue growth (+13.8%) not keeping pace with cost growth (+34.3%) Bottom line: Still a well-capitalised, geographically balanced bank with strong recurring earnings, but the operating leverage is heading the wrong way for now. Management execution in 2H25 (on cost control and margin defence) will be key.

-

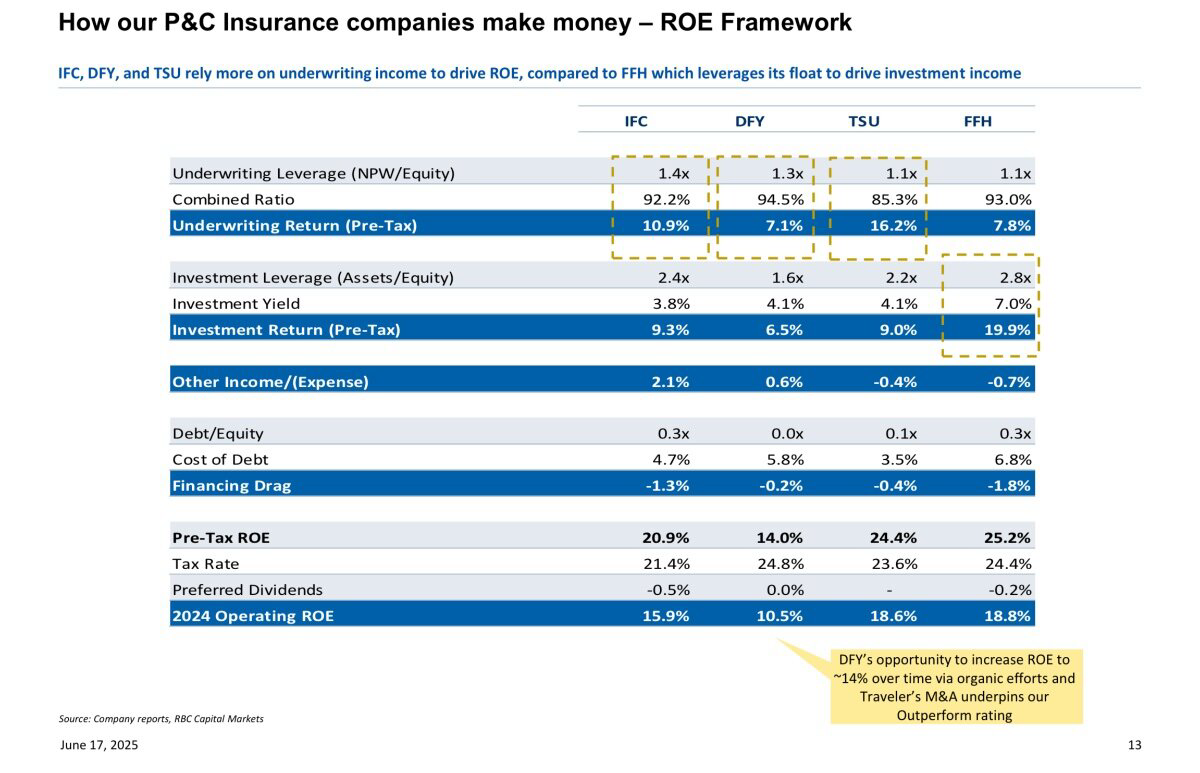

I had another crack at this. I still can’t fully reconcile bottom-up ROE with reported ROE, I’m off by about 80bps, but it’s close enough to be confident in the mechanics. The table follows the format @SafetyinNumbers posted and uses figures from H1 2025 (first 6 months). What really stood out was just how much of a short-term ROE handbrake IFRS 17 creates, especially for a capital allocator like Fairfax. The standard imposes a mechanical expense based on the size and duration of the float, but it doesn’t capture the returns Fairfax generates with it. For a passive bond-heavy insurer, that might be fine. But for Fairfax actively redeploying float into prefs, TRS, and equity-linked structures it creates a structural underreporting of true ROE at least in the short term. I am sure it washes thru in the end but it would be easy to draw the wrong conclusion while: -Growing premium volume -Writing longer-dated liabilities -Expanding float faster than investment income can catch up

-

Good point. That number should $70.3. I will re-run those numbers after work. It was the wrong number but it has raised something interesting about the methodology though.

-

Access to high-quality data is going to be a differentiator IMHO. Berkshire has a real edge here, decades of accumulated underwriting data across geographies and verticals, coupled with the cultural discipline to use it well. Fairfax is on their way, especially with Digit and Ki building tech-forward platforms. They’re vulnerable, yes, every incumbent is, but their edge isn’t just data, it’s also capital flexibility, underwriting culture, and time-tested risk frameworks. Oh and that intangible of all attributes, trust. Balance sheet helps too

-

Background article on Sleep Country’s advertising ramp with Eugene Levy as brand ambassador. https://mediaincanada.com/2025/07/08/sleep-country-largest-media-buy-in-30-years/ “It really took off, especially on YouTube and connected TV, with consumers resonating strongly with the messaging. We saw significant lift – nearly 20% in the first couple of weeks – and those learnings helped us further refine our messaging for Sleep Daddy,” Bamberg says. “This gave us confidence that levity can spark serious conversations about sleep health, driving awareness and consideration in a way that resonates with consumers.” The new campaign is based on a Sleep Country and Leger study of 1,619 Canadian adults conducted last month, which revealed that 69% of respondents desire a better night’s sleep. The poll also indicated that 26% of participants reported obtaining the necessary seven to eight hours of sleep, while 65% slept for six hours or less. The Publicis pitch: https://www.publicis.ca/work/sleep-daddy-reignites-canadas-relationship-with-sleep

-

MS with a wrap on Digit’s Q126 results along with some AI notes that cover the results and the conference call. Conference Call https://www.marketscreener.com/news/transcript-go-digit-general-insurance-limited-q1-2026-earnings-call-jul-28-2025-ce7c5fd8de88f421#:~:text=loss ratios last year for,the combined ratio looks up TL;DR Strong Growth, Profitable Quarter GWP up 12.1% YoY to ₹2,982 cr (driven by fire +41%, motor steady, health flat) PAT up 36.6% YoY to ₹138 cr, despite lower net retention (65% vs 76%) Investment income surged 32% to ₹372 cr, supporting profit Combined Ratio Worsens (but explained) Combined ratio rose to 108.6% (from 105.4%) due to: Strategic reinsurance (ceding large fire risks) 5-year two-wheeler policies (front-loaded expense, deferred revenue under IFRS) High commissions in growth segments (especially 2W) Segment Highlights Fire/property: +40% GWP, retained little to avoid large losses Motor: TP outperformed industry; 2W surged; OD flat Health: Group health cut back to avoid underpriced deals Loss ratio stable at 70.3%, showing underwriting quality intact Capital & Returns Solvency ratio 2.27x, ample buffer ROE ~13–14% (IFRS basis ROE even higher at 19% annualized) IFRS 17 Impacts New “1/N” premium deferral lowered revenue Lower discount rate (6.3%) increased claim reserves by ₹44 cr Management disclosed IFRS metrics transparently EoM & Regulatory Compliance Within expense caps; leads industry on cost efficiency Avoiding irrational pricing, esp. in group health Sees regulation pushing market toward more rational competition Management Strategy Prioritizing sustainable growth > vanity GWP Tactical reinsurance, selective underwriting, long-term profitability focus Confident combined ratio will improve in H2 as fire/2W impact fades Bottom Line: Strong top-line, resilient underwriting, investment boost, and sound strategy. Management is navigating IFRS, regulation, and market pressure smartly. Execution in H2 will determine if Go Digit justifies its premium valuation. Go Digit General Insurance F1Q26 Earnings Review.pdf GODIGIT_20250728_2001.pdf

-

Interesting point, will pick it up in the Strathcona thread.

-

@SafetyinNumbers good chat, you covered a lot of ground. https://podcasts.apple.com/au/podcast/newcomer-investor/id1662369630?i=1000719376026