.jpeg.66c448bf718e7352b2952f5c41faa6d7.jpeg)

longterminvestor

-

Posts

372 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by longterminvestor

-

.thumb.jpeg.b0384a4135d041bebd0e39ae144d51f4.jpeg)

iSavings bonds yielding 7.12% currently

longterminvestor replied to Spekulatius's topic in General Discussion

For those who bought IBonds in 2021-2022, the fixed portion of the coupon was 0.00%. IBonds are now being issued with a 0.90% fixed component to the rate. Curious if it makes sense to redeem the ones I have with and buy new with fixed component. Return on these has been satisfactory. -

I cringe as well at my younger self and I am only 40. A quote that rings true here, didn't hit me when I first heard it, took me a while to actually understand it: "Youth is wasted on the young".

-

@ParsadThe word clarity struck me in your comments. The tandem of Mr. Buffett rattling off statistics from say a 1954 annual report and Mr. Munger chiming in with customary crusty curmudgeon comment - concise, accurate, and wise 1000%. Both of them playing off each other will be what I miss. The best 1-2 punch in the business I am aware of for sure! I think its the wisdom, I could listen to Mr. Buffett describe the mechanics of a toilet paper manufacturing business for days. Call me crazy, or just call me a Berkshire shareholder - fine with either. I am reminded of the summer camp I attended as a child. Family run, founded by larger than life father who had 2 sons. The founder was legendary and ran the camp with great gusto. The sons took it over both with their distinct roles. One was front facing campers with great oration/leadership and the other was back of the house and lead from behind. Each had their own sons later who came into the camp and now run. I had pleasure of seeing the later 2 regimes run the camp. And the transition was uneasy at first however overtime it just felt like home again. The camp, very much like Berkshire, has a culture where everyone just knew where to go, what to do, the standards never changed. Amazing actually to think back that all the counselors were top tier athletes/scholars and thus campers all aspired to greatness because we were around greatness (average of your best 5 friends theory). Berkshire is like that, it will live on, and in the future we will yearn for the way things were or wonder what Mr. Buffett/Mr. Munger would do, how would they handle this/that situation - totally natural. I'm with you though, it does make me sad to think of the future without them. I am forever grateful for the time we all have had and what a ride it has been. People were worried about this 20 years ago and look at them, 20 years later. It really is an amazing achievement, the painting of Berkshire as Mr. Buffett refers. @ParsadTHANK YOU for your gift of COBF. it is a great community of like minded folks and will endure. Speaking of that, how old are you? Have you picked out your Gregg and Ajit? hehe. Cheers!

-

Rare Ted Weschler Interview (!!)

longterminvestor replied to ValueMaven's topic in Berkshire Hathaway

Didn't want to start a new thread, so I just stuck this in here. Podcast from Nebraska Furniture Mart Podcast series called "I AM HOME" with Todd Combs. https://pca.st/aar0wkxj?utm_source=substack&utm_medium=email -

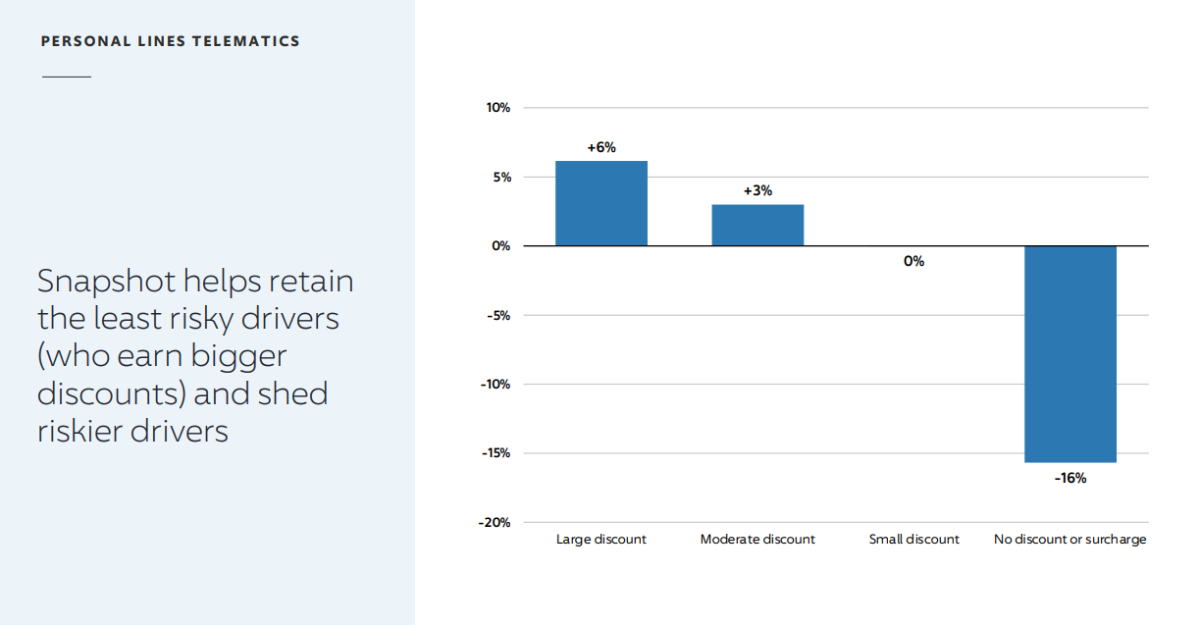

The whole point of this exercise is Progressive is the first one to price using real time driver feedback data that is fed into a super computer so my opinion, Progressive is getting the best data to make pricing decision. Is it possible that they are underpricing, I guess. I would tend to agree with you if this was some new kid on the block however Progressive is a proven stable VERY intelligent underwriter who has pioneered an entire new way to underwrite and price risk. I dont have much else on this topic.

-

No, I am not saying GEICO is mis-pricing product. I am saying GEICO has to increase the price of their product due to the type of drivers they are now getting due to Progressive getting/retaining better Drivers. And GEICO has always won business on price alone, no other value proposition they offer - they are the low cost provider. Where as Progressive allows independent agents to package the Progressive Auto with other lines of business. Progressive policy count/premium volume is growing and GEICO is shrinking as previously evidenced with financials and slides.

-

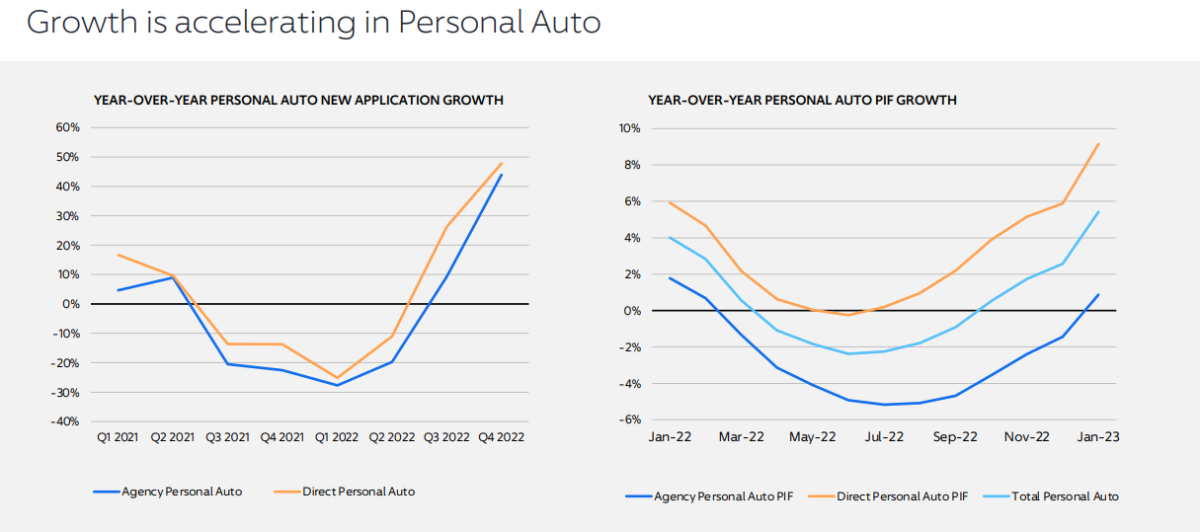

Match rate to risk. I believe GEICO is getting the more risky drivers and has to price for that risk. If Progressive is attracting more good insureds defined as people who are generally safer and ultimately file less claims, their individual premium charged will actually go down over time (Progressive calls this their "Discount Loyalty Program" or something like that) but more policies in force means Progressive is growing top line. Conversely, GEICO is taking on clients who potentially could file more claims (the ones Progressive doesn't want), their rate charged needs to be higher. GEICO is not "raising rate/premium for raising sake". The premium is up for the individual policy because they are taking on an insured that is less predictable and the margin of safety needs to be included in the rate making formula - this is pure Buffett. However top line is shrinking because they are losing long time customers. GEICO's entire premise is price, auto insurance is a commodity - policies are basically the same at personal auto level and loyalty comes with with getting best price - compete on price. And very clearly, they are losing on price, and they are losing the better risks on price. This is my point. GEICO barely puts out anything public as granular as you are asking for. Here are the Numbers the way I see them: GEICO premium 2020- $34,928B, 2021 - $38,395B, and 2022 - $39,107B - thats a 12% growth rate from 2020-2022 Progressive personal lines premium 2020- $32,620B, 2021 - $35,373B, and 2022 - $37,880B - thats a 16% growth rate from 2020-2022 Comping off 2020 with COVID skews numbers but its what I had infront of me - if you have more questions I can dig some more. This is just the way I see it, I hope I am wrong for Berkshire, I hope they are figuring this out. Just concerning how poorly Progressive is LAPPING GEICO. And Progressives number for Q1 YOY are at a 22% growth rate. GEICO has not published Q1. BUT premium written for GIECO in Q4 2022 YOY was actually down, less than last year, premium is shrinking, another way to call that is negative growth. see slide deck from Progressive regarding attracting/retaining better drivers, this is public information: see slide deck regarding Progressive premium growth: been busy with my day job, sorry for the late reply. Insurance in Florida is going nutty.

-

who is the broker you are placing the order?

-

Rare Ted Weschler Interview (!!)

longterminvestor replied to ValueMaven's topic in Berkshire Hathaway

I have found positioning sizing to be harder than finding ideas I like/understand. -

Who will join the board in 10+ years?

longterminvestor replied to yesman182's topic in Berkshire Hathaway

Bloomstran would love it. Secretly (not-so-secretly) been eyeing (lobbying) the job for years. -

Who will join the board in 10+ years?

longterminvestor replied to yesman182's topic in Berkshire Hathaway

Ackman? -

Bad Risk is relative. Its not a bad risk if its priced correctly. The consumer is complaining, "my premium went up" but its probably insurance company matching the risk with the rate. Many moons ago it was a crap shoot on rates but the risk was super small - no possibility for $500,000 claim either from a Jury/settlement or just the limits on the policy were just smaller. Now, the max payout is larger. I mean, think about it like this - the auto insurance value is pretty great/amazing. Look at what you are getting. Lets say average rate in $100/month for Comp/Collision on a Audi Q5 (middle of the road decent/nice car) and $250K/$500K limit (forgetting PIP/UM). That's $1200/yr for a max payout out of $550,000 PER ACCIDENT. Meaning one could have multiple accidents in 1 year - each time $550,000 is at risk. Every time the vehicle is on the road there is a risk of $550,000. The risk is reduced when the car is parked to $50,000 (comprehensive/collison risk only). A few years ago Progressive saw the max payouts rising and needed a way to attract "their kind of driver" and they built it from scratch. GEICO just spent more money on caveman ads. All is not lost for GEICO. Brand and loyalty mean a lot - and Progressive may make a mistake. Its a bad risk when you mispriced the rate charged on the exposure. Mr. Buffett and Mr. Jain have repeatedly told us, solid underwriting is matching rate with risk.

-

I can take a stab at this. Early in my career, a Senior Underwriter gave me a similar lesson. His point was (paraphrasing) Don't look at policy count/premium retention needing to stay at 100% - if it is, it's actually a bad outcome. The underwriter explained 100% retention as "we left money on the table". Deepening the lesson a tad to Progressive vs GEICO, and GEICO's lacking investment in Analytics, Progressive has been gaining market share using a tool that allows them to price risk at renewal based on usage. When insured comes with no history, similar formula to GEICO (tons of data goes into this first stage) and then what analytics does at renewal (more specifically having real time feed back on breaking, speeds, miles driven, ect) it allows Progressive to price out the customers they do not want faster and price in the customers they do want during the upcoming renewals. GEICO did not invest in that technology, Progressive invested heavily. And frankly, it shows in the numbers. And what I see happening, even worse for Berkshire/GEICO, is Progressive is keeping the "good risks" and GEICO is picking up those "bad risk" - I see GEICO as pricing for the "scraps". The above is underwriting driver behavior - there are many more factors that load in (referenced above as macro) - geography (wind load in FL vs quake load in CA vs Flood load in MS vs no load for CAT in Iowa), similar is big city/small town so that's zip code, theft/crime rates, regulatory environments with insurance commissioners (and lobbyist with who insurance companies work with) to set the actual rates, new law perhaps - we call this regulatory arbitrage - changes like liability for DUI in Arkansas is different in FL - the bar who served can be held liable in Arkansas.....and the law could change in future which could change the rating loads with new liability in court room (Nuclear Verdicts), and more specifically to the risk (micro) youthful drivers in household, family members in household of driving age, getting married/divorced. All of this factors into pricing, as the life of the insured changes, as the economics of auto/driving habits change, pricing will change. It can get very technical, to those who continue to wonder about price - the answer is simple to me. If you want "best price" today, with ALL the data available on you/family readily accessible with a credit pull and a LexusNexus ping, then you gotta shop every 6 months - period. Full Stop. And shopping around takes work - unload that to a broker or do-it-yourself direct with no representation. Your option.

-

Next Berkshire acquisition speculation

longterminvestor replied to gfp's topic in Berkshire Hathaway

exactly. you get it. However management of Allegheny have a "duty to shareholders as a public company to extract the highest value". and thats why its sooo hard for Mr. Buffett to buy outright public companies. Private companies don't have that MO (they do but its different). -

Next Berkshire acquisition speculation

longterminvestor replied to gfp's topic in Berkshire Hathaway

CEO of Allegheny sent Mr. Buffett the annual report. and Mr. Buffett replied back saying "hey I am in town next week, you wanna have dinner?" Mr. Buffett does not leave Omaha for anybody any more, and he is randomly roaming the North East US? He knew exactly what he was doing, and it worked swimmingly. -

Next Berkshire acquisition speculation

longterminvestor replied to gfp's topic in Berkshire Hathaway

Allegheny is alot like Berkshire in many ways - the way its run, decentralized. It was actually railroad company in the beginning (akin to Berkshire in textiles). Pivoted to other businesses over time and then found insurance in the the 80's. Today I am less focused on what Mr. Buffett says (we can pretty much predict what he is gonna say on particular topics), and more on what he choses not to say. Mr. Buffett does not care about choppy markets - he's thinking in decades. MY opinion, he (we) stole Allegheny. 1.26X book based on Allegany's position as a stand alone public company, however inside Berkshire its worth way more because as a subsidiary it gains so much more leverage with regulators on admitted capital (can leave bonds and buy equities) and also no longer needs to purchase reinsurance (cheap or expensive, its an expense to the business) to take risks Berkshire already wants to take more risk on. Go shop period, I mean the message was clear to me. "Ummmm, dear shareholders Allegheny, our CEO has met with gods gift to insurance and prior boss, ie Berkshire Hathaway and Mr. Buffett, and we have a deal to sell the firm (sorry Goldman Sachs, you don't get a fat fee, Mr. Buffett wrote the deal on a napkin). We respectfully asked for Berkshire paper and Mr. Buffett promptly rebutted with Benjamin's only - no Berk paper. Oh and because we are a public company, we owe it to you to find a topping bid - Mr. Buffett graciously gave us less than a month (25 days) to find someone willing to write a check for $12B+ cash not subject to financing and with no adverse change clause. And even if we do "find someone" to write a check for $12B+ we will probably ignore it because its a short term home for our managers/employees, new owners will load with debt and re-sell to someone else. With that said, we are patiently waiting by the fax machine for some bids, we will let you know what comes in." Here is a letter that shows Mr. Buffett builds relationships far ahead of when those "seeds" grow into "trees". Mr. Buffett is credited Mr. Burns with teachings of rail roads in the 2000's. Mr. Burns did not have the money/ability to act on rails, Mr. Buffett did. -

Next Berkshire acquisition speculation

longterminvestor replied to gfp's topic in Berkshire Hathaway

Not a good comp for a lot of reasons, its risk bearing insurance, Mr. Buffett has a long standing relationship with CEO of Alleghany, Mr. Buffett has also been following Alleghany for 50+yrs. I am uncertain if the "best thing for shareholders of Alleghany" was to sell, however if they were going to sell, the only home would be Berkshire. And that "go-shop" period was a little song and dance, my opinion. Great buy for Berkshire, shareholders of Alleghany got an okay result. Better result would have been Berkshire issuing paper however Mr. Buffet ain't giving up any paper right now where Berkshire's valuation. -

Rare Ted Weschler Interview (!!)

longterminvestor replied to ValueMaven's topic in Berkshire Hathaway

Here it is in PDF TED LETTER.pdf -

Not bothered by the brevity (I expected a short letter). I appreciated section about the traits to seek in a partner. The simple lessons of life and business ring truer now than ever before. I still find myself making spreadsheets - trying to find nuggets in the dark corners of the balance sheet/P&L. Maybe I need to relax a little there and heed the words, find someone who can laugh and teach something at the same time. The letter sans summary of equity holdings just tells me to think more about the operating businesses inside Berkshire. Mr. Buffett even enlarged the font a touch so the letter was even shorter than you may think! (I will save the word count for the obsessed hungry 23 year old...that would have been something I would have done years ago....hehe) Mr. Buffett doesn't even have to write a letter or sit on stage at this point but he still does. Thank you Mr. Buffett for your teachings.

-

Buffett/Berkshire - general news

longterminvestor replied to fareastwarriors's topic in Berkshire Hathaway

OUCH! At least he puts it out there for the world to see. Gotta respect that. -

Rare Ted Weschler Interview (!!)

longterminvestor replied to ValueMaven's topic in Berkshire Hathaway

there is a tool inside Microsoft word that I have used for this. Didnt know there was a website that did it as well. thx. -

Rare Ted Weschler Interview (!!)

longterminvestor replied to ValueMaven's topic in Berkshire Hathaway

I'm the sucker whose helping. -

Rare Ted Weschler Interview (!!)

longterminvestor replied to ValueMaven's topic in Berkshire Hathaway

New interview: -

Buffett/Berkshire - general news

longterminvestor replied to fareastwarriors's topic in Berkshire Hathaway

Fisher Island. 5th most wealthy zip code in the US. Property Search Application - Miami-Dade County.pdf -

I appreciate the lead - thanks. its getting closer, just need the other publicly traded auto carriers here with data as presented.