.jpeg.66c448bf718e7352b2952f5c41faa6d7.jpeg)

longterminvestor

-

Posts

314 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by longterminvestor

-

.thumb.jpeg.b0384a4135d041bebd0e39ae144d51f4.jpeg)

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Come one. I already mention the coal deal, give something new!!! -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

share your thoughts. thats what this is all about - all trying to learn. "I'll show you mine if you show me yours?" send it. put it out in the ether. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

yes those are TTM PE's. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

My next project is to figure out why AJG trades at higher PE than the other brokers. Anyone have thoughts? There is some chatter AJG has some interest in a coal deal that gives them some tax credits, I am going to research and share. Seems like a logical question with BRO trading at 28X, AON at 26X, WTW at 22X, MMC at 30X, and AJG at 45X - these are all extremely mature businesses and AJG sticks out. Outlier would be a RYAN at 80X and GSHD at 300X - both new in the past 10 years. Will look as well. BRP doesn't have any earnings so it is not in this group. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Did not mention in write up, recent (early-mid September) insider sales are not good to see as well - maybe that's my bias creep. I don't think this is a short or wish ill will on them, just not a business I can partner with. Fanciful structures are more and more prevalent in todays world, I guess as long as its disclosed right? -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

BRP - T. Baldwin's words "BRP Alchemy, where one plus one ultimately enables something more than two" - lets dive in. - The C-Suite is OBSESSED with Adjusted EBITDA. Almost odd how they are amazed with themselves on how good their numbers are. You will catch them saying EBITDA a ton without the "adjusted" coming first which shows they are almost forgetting their numbers are filled with adjustments. The use of metrics and formulas is almost like management knows investors screen the stock based on certain metrics and they do whatever they can to hit those metrics. I am not saying the numbers are false, they are just adjusted like CRAZY. - To grow this fast, debt is the only way. $1.331B of floating debt comes due in 2027. Management got terms in kindest credit market in a generation. Props to them for seizing the moment (better to be lucky than good), lets see how that plays out when they have to replace that debt. -Regarding the moment in time, its almost as if Baldwin saw this confluence of insurance brokerage becoming a fad and capitalized on cheap debt, huge investor interest in brokers, and pounced on the opportunity to do a public offering. 100% credit goes to him for seeing that opportunity, really well done, however it all inures to him and his cohorts benefit, not shareholders. -Everything in the C-Suite just looks cozy. They even have a client as an investor in the operating LLC (The Villages - retirement community in central FL). The owners of that co are all decedents of the original developers of the Villages (moms, brothers, daughters, ect). Just weird to me. Its all disclosed, just seems, well, cozy. - Dual class stock. Buying a share of Class A BRP gets you a piece of the PubCo that has the operating LLC inside where the C-Suite holds all the marbles. Class B Shares are what the Baldwins own, not you. The structure is set up so Mr. Lowry Baldwin has ultimate say on the business and shareholders do not. All the managers have signed an agreement to vote with L. Baldwin. - Tax Receivable Agreement (TRA). Didn't know much about these however the structure exists for Up-C IPO's. Other businesses with this structure are Shake Shack, Interactive Brokers, Goosehead Insurance and Rocket Mortgage. The TRA gives any tax savings the business enjoys back to the founders at a split of 85%. In fact, there is a financial incentive for management to continue losing money because the future net operating loss carryforwards increase the payment into the TRA. Did not do the math (mostly cause I would fail miserably at calculations) however its gotta be in the $100's of millions in future payments to founders through the TRA structure. - Any founder whose business is in a sector that trades on above the line EBITDA multiples with reckless abandon for net income LOVES the TRA because with adjustments, the future payments are not apart of the models analyst build. When market trades the business on EBITDA (and in case of BRP, its "Adjusted EBITDA - never forget that), the TRA will not be accounted for and yet its a huge drag on profitability. - Wake up, BRP loses money on a GAAP basis. Insurance Broker business model is SO GOOD that investor community ignores the fact that BRP has not made money on GAAP basis since inception. This stems from the acquisitions and meteoric revenue growth. Just find it difficult to put out to shareholder community words like "Continuing track record of exceptional operation and financial execution" when the financials are FILLED WITH ADJUSTMENTS. Here's another one, "Investing to drive efficiencies and sustainable long-term profitable growth with a disciplined, return-focused capital allocation strategy". That's just not accurate. There has been no financial return in the business, all the money is going out, maybe in the return is in stock returns but not the operating business itself. -Acquisitions have not slowed, they have stopped. Management knows they have to get balance sheet ready for what's coming. I view that as a positive but if there is some big announcement on acquisition, look at the debt. And with regards to acquisitions, BRP historically has OVERPAID for the business's they bought. They are not disciplined with their poker chips, they just put them all on red and spin the wheel. -Interest Rate Cap Purchases. All the debt is floating so they buy hedges at an expense to cap the interest rate hike risk. This is just a scary thought again because these costs are not included in the "Adjusted EBITDA" numbers management touts from the roof tops however they are real expenses to the business. -Downplaying the rate environment (hard market) as a function the organic growth. Cringeworthy to hear coming out of the CEO's mouth because if you are a broker in the US, a huge part of organic growth is coming from the increases in rate. CEO just dodges questions because he wants investors to believe the organic is coming from the business, not from rate. T. Baldwin quote from Investor Day Nov 2022, "if you look at the 28 percent organic growth, we delivered in the third quarter of this year, only 2.7 percent of that came from a combined tailwind of rate and exposure". In this hard market, I find that almost impossible to believe. Side note, to have the figure down to a fraction of a decimal is weird, it not an easy task to carve out the numbers on organic/exposure basis/rate with millions of policies and the way data is entered into systems - they could be doing something incredible there with tech and tracking - if so good for them and it is incredible - I do not have any insight - I am gonna ask around tho - just find that number difficult to understand how its calculated. Meaning if there is so much noise that goes into agency management systems, it would take an entire team of people just focused on that problem every quarter to get that number accurate to a percentage decimal point - and then you have audits, endorsements, and return premiums - its just not a number I am comfortable seeing disclosed in that manner. My point is management is drinking too much of their own Koolaide and need to wake up. -Investor Day slides mix in premium with revenue to almost make things look bigger than they are. Never forget the words of total shark broker who told me, "We can not spend premium, we can only spend revenue" meaning don't talk about the big $100K premium you just bound, talk about the $10K in revenue that will go to payroll, rent and expenses - small time agencies talk about premium - pros talk rev. -Organic Growth is staggeringly high and management is adamant this will continue. Lets see. Will be tough to sift through the slide decks of the future with a huge amount of footnotes, *, and symbols next to organic growth numbers. The way revenue is earned allows management to play with that, as long as its disclosed seems to be BRP's north star. -Medicare unit is not a great business. I believe its a top line money grab to boost revenue because management needs growth for metrics. Medicare revenue is not worth the same as a middle market revenue yet there is no discount in the business for the Medicare rev. Little deeper dive, one $100,000 revenue account ($1M premium) that has been on books for 5 yrs is worth a TON more than $100,000 in Medicare revenue. -Early acquisitions were not 100% buy outs, they bought only portions of the business. Not a fan of this in an "elevator asset" business where the largest asset being purchased can walk out the door. Very different when buying a pipeline or manufacturing business where the assets are static and yeah, you need people to run the assets, but there's a bunch of invested capital that can not leave the business. This is not true in brokerage, that is just bad capital allocation to me for the long haul however if you are trying to make a quick buck - sure does seem smart. - Dilution: 60,093,228 Class A shares outstanding as of June 30, 2023 vs 33,098,356 Class A Shares outstanding as of Sept 30, 2020. OUCH! -Founder Lowry Baldwin has a history of starting, selling, leaving and doing it again. That is not the kind of founder I want to partner with when one sells the business, walks in the next day to tell their new found owner who wrote a huge check and say "when my non-compete is over, I am outa here". Totally fine to do, live up to contractual obligations he did, however that takes a certain kind of person that I am not a fan of when there are other Chairmen/Chairwomen who want to paint a masterpiece and build forever. For those believers, here is some of the good: - MGA of the Future is definitely the best business they own, followed by Middle Market, and then Personal Lines. MGA of the Future is probably the gem inside this business. - The growth is mind numbing, it took Brown & Brown 70 years to get to $1B in revenue, BRP did it in 11years. - Goosehead vs BRP personal Lines. I believe the BRP personal lines business is larger in revenue that the entire Goosehead business. So if you think Goosehead is properly priced (I do not), then BRP's personal lines business is undervalued inside BRP. Closing: Just seems like founding family is running this business for the benefit of themselves and not shareholders. Ultimately, Insurance Brokerage is such a GREAT business it is idiot proof. Baldwins are not idiots, actually quite the contrary - they have gotten rich being smarter than everyone else and their timing is incredible. Hats off to them! If you were an early seller of your business to BRP and got units in the LLC, you did extremely well (and participated in the TRA) however shareholders from IPO on are just way behind the curve in terms of alignment. Here are their words taken from 10K (Holders being the Pre-IPO Members are "Holders): "Furthermore, Holders’ interests may not be fully aligned with yours, which could lead to actions that are not in your best interests. Because the Holders hold a majority of their economic interests in our business through BRP rather than through BRP Group, they may have conflicting interests with holders of shares of our Class A common stock." -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

You found Poe & Brown in 1994? Thats the kind of business, runway, and management I am searching for - it was magic in a bottle for sure. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

The model is not difficult - it just comes in the difficult to understand mystical wrapper called "insurance". The street even puts brokers in buckets at times with risk bearing insures for comps - not even close to the same model. Brokerage is financial services at the end of the day. Everyone wants the 100X bagger, founder led/founder controlled, serial acquirer, strong ROIC, management in place, durable model, capital light "compounder" - look no further than Brown & Brown. Business was born in 1939 in dusty Daytona Beach, FL by Adrian Brown and Cousin Cov. 10 years later, they had $6,597 in net income. As a kid, Hyatt (son of Adrian and mastermind behind B&B) would hang out in the office and at an early age he understood personal relationships and salesmanship were key, “I would be sitting and listening and saying nothing, and the first 85% of the customer visit was about hunting, fishing, jokes and all that stuff . And then finally the last part was insurance.” Hyatt recalls. Hyatt graduates from University of Florida and immediately turns around and writes a policy for the college as his first "big account". Annual revenue jumps of the business jumps from $42K to $60K. Hyatt later buys the business for $75K and a note worth 10% interest. The annual meetings were held in the office kitchen. (Abbreviated version of origin story taken from the 2008 annual report). Net income from 1949 to 2022 grew from $6,597 to $671.8M - a 10,183,316% increase. $60K topline rev to $3.5B in 2022! Along the way they took on some modest debt (lately they have taken on substantial debt at historically cheap rates to support the acquisitions). 4 parts to the business. Retail, Wholesale, Programs, Services. Retail leads the business with large portion of revenue focusing on the "middle market" accounts where spend is $25K - $250K - they will get into larger accounts and love those but at that stage the bigger "alphabet houses" will be knocking on their door. There is a time when an account can outgrow the capabilities a B&B can provide and the client needs more risk management rather than just transactional insurance. Wholesale is the 2nd bucket of revenue, recently rebranded this as "Bridge Specialty" and this is the intermediary between the retail broker and the insurance company - lots of growth in this space with E&S action and changes in risk bearing market segment. Programs is a niche - think lawyers, plumbers, A/C repair, school buses - something that is homogenous in nature and specialized in 1 arena - they are the experts in that niche and make the retail agent look really good. Services at B&B is super small and has never scaled. I remember describing the business to a fund manager as an early investor - still had not discovered my own personal style of investing (I would stare at charts like I was reading tarot cards waiting for the chart to "speak to me" - hopefully I am not the only person who started like this - please tell me I was not alone!!) - and the fund manager just said "This is a 3rd generation family business, the 3rd generation is always the one who f*cks it up" - that thought was seared into my head and held me back from buying more. My father also held me back from buying more reminding me that owning a large stake in the business you work for is an issue because of the Enron risk (should not have listened to him - different business model entirely). I owned the stock in my PA for a while, not knowing what I had and stupidly sold it - proceeds were rolled into my personal investment in my own insurance agency - so I traded 1 public broker for my own privately held broker - however looking back I could have scratched together the cash another way if I would have tightened my belt - was newly married, buying a house, and pregnant wife so I felt I needed all the cash on hand possible. These are just great lessons of investing and still serve as a good lessons today. Regarding B&B, the question is now about runway - how big can the business get? Time will tell. I am looking forward to the future for some new IPO's on horizon with AssuredPartners, Acrisure, and some others that may/not be looking for some liquidity in the public market. I will be doing a deeper dive into BRP's financials and share my findings. stay tuned. -

Buffett/Berkshire - general news

longterminvestor replied to fareastwarriors's topic in Berkshire Hathaway

Berkshire's Intrinsic Value is an internal yardstick and very much independent of the value of the business. Mr. Buffett's hurdle for any business is 15% return day one and compound from there - believe that is an Alice Schroeder quote. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

This just occurred to me because of the questions. Most retail insurance agents do not even know what binding authority vs. brokerage is/means. The retailer just looks at the price (then the commission), likes/dislikes the language, and presents the quote to the customer. Its a small part of the business. The concept really is more because of the regionality of insurance and pushing costs down stream to give "underwriting authority" to brokers so the carriers can be more efficient with their human capital. People refer to it as having in house quoting authority, or what not. Early in my career an old salt asked me, what is the difference between an agent and a broker? I didn't have the foggiest, and the answer was simple: an agent can bind coverage, a broker needs to ask permission to bind and have the order accepted by the underwriter. unique concept there but powerful. The term "program" is way over used, and everyone has a "special relationship" with "XYZ carrier". just like any other business, gotta trust who you work with and know the game. no need for the thanks. if i can give to the forum, happy to, I have gotten a ton so its only natural to want to give. Glad people are getting something out of it. a huge chunk of my net worth is tied to insurance distribution, been apart of a regional privately owned top 100 agency, watched that get sold off, worked for a big publicly traded broker, and started my own shop from scratch, and then have been acquiring agencies/books of business. i have partners so it helps but we do care more about running a well managed/well run business more than most. its not surprising to me why people dont know much about insurance or distribution, customers/buyers hate insurance. Surveys say people would prefer to go to the dentist than talk to their insurance agent. Powel Brown puts it really well, "Insurance is not a sexy business, we run the ball every down, never throwing deep". and that is just not appealing to many people. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Why does AON, MMC, and other retailers want to do all the work on placing it direct when they can just submit to Ryan, AmWins, CRC - have them do all the work and as the retailer just sit back and wait for terms? you're giving up maybe 3% or 5% or in some cases 7% but doing way less work. Yes, you are giving up contingency payments, yes, you make less money. and Yes, there is some chatter that the bigger shops are going to start trying to pull their wholesale relationships in house and place it direct however the carriers like having a wholesaler involved because there is a little bit more trust and the wholesaler "cleans up" the submission. There are a bunch of carriers who are and will always be wholesale only. Some play both sides. The old saying, retailer goes to lunch and brings back a paper napkin with the specs, the wholesaler prepares the submission. I grew up in a tech age so my submissions were always super tight, the wholesalers like my deals when I send them in because they are super clean with all the information ready to send out. Carriers like tight/clean submissions so they can look at it once, and quote it or move on to next deal. Time is the asset. Wholesale also got stupid, Ryan caused some of it. Retailers were fine working on wholesale deals at 10%, wholesaler taking 5%. But Ryan started paying 11% or 12% (higher in some cases) so then everyone went to 11%-12%. I'm sure the carriers were paying more as well but 10% to 12% is a big swing with volume. and admitted pays 15% so youre kinda fine just leaving it E&S and go find more accounts. I'm jaded because my region is super wholesale focused. Other parts of the country are probably less E&S and more admitted. Its really not about pricing power, its about the accounts and exposures. You might have a retail shop who has 1 class of business, car dealerships, they could probably get tight with a market and grow that channel but most retail shops have tons of classes of business and need the support of multiple wholesalers for the expertise. Professional Liability is a lot different than GL or Property. Back to car dealer example, the market they get tight with might only be writing the Property, Garage Dealers, and Open lot cover, the retailer needs a relationship for the D&O/EPL and there is an opportunity for a wholesale relationship. Or they need capacity for Umbrella. And then you get a call from the owner of your biggest account who has a son who is starting a General Contracting business, you gotta quote that and take care of it before another retailer gets in there and starts asking the son to introduce them to his dad. Next thing you got 10 GC's in your book. it happens all the time. A great coach in insurance told me once, "You can have a couple of pets around, but we are not running a zoo!" I love that line, use it all the time. Having all your eggs in one baskets is great until it isnt. Maybe the carrier gets downgraded from A- to B+ and you have to move the whole book. That sucks when that happens. Its a good thing to have wholesalers around for the retailer. Its work but it also allows the retailer to manage the client relationship - for big accounts sometimes thats a full time job. Haven't even talked about claims or servicing. That takes up alot of time. To leave and start their own shop, Wholesalers need a couple of stable markets and some key markets. Sure, if they want to be business owners and deal with payroll, accounting, HR, hiring new people to service the book, contracts, carrier relations, they could leave. Just dont see much of that happen. Happens more on the retail side for whatever reason. Have not seen a wave of wholesale brokers leave to start up their own shops. It does happen more in retail, partly because of the wholesale market being so easy - wholesaler will open almost anyone with a pulse. 1. Tail winds - IDK, big is big but big doesn't always mean better. Bridge Specialty on that slide deck is Brown and Browns wholesale arm. Thats a whole thing to explain what/why Brown re-named it Bridge Specialty. RPS is owned by AJG. and CRC is owned by BB&T. I mean, Ryan definitely saw an opportunity, them buying All Risk was a big move for Ryan. If E&S continues to grow, all ships will rise with the tide. But you gotta execute. 2. E&S vs Admitted. tough to gauge. I mean most E&S carriers are a subsidiary of a name you would know. Hartford has E&S and Admitted carriers inside their risk bearing entities, same with Zurich, AIG, Travelers, all the big carriers. Travelers admitted might price something and then Northfield (Travelers E&S) may quote the same risk for more/less price - Travelers management would not even know assuming it was a small-mid size account. if it was a big deal, like $500K or something they probably would know. Ryan is incentive is to tell that story because their wagon is hitched to the E&S train. That's truly a macro question - kinda like "Where is inflation gonna be in 3-5 years or where are interest rates in 3-5 years". You could guess but no one knows - its a market place - things happen. 3. Dont know much about the small-medium wholesale broker marketplace for acquisitions - only know retail acquisitions because we are acquiring. Its smaller today for sure. but if i had to guess, theres room. Do not under estimate Ryans ability to attract and train new talent. They really have a machine there, so do other brokers. Constantly hear about them at all the risk management schools getting kids to go brokerage rather than work a desk with a clip on tie at a carrier. Brokerage is much sexier than working for a carrier coming out of college. There are some brokers where all the guys are like 25-30yrs old making $250K+, its like a fraternity. Type A loves that culture. 4. MGA/MGU/Binding - all completely different skill sets and much more dependent on the carriers appetite than the brokers wants/needs. Brokers would love to have the pen and an exclusive program. Thats the killer app in the insurance business. Everyone wants that. Its when the carrier actually grants that authority to a broker that makes the market go WOW. Remember what Mr. Buffett said about what brokers would do for their clients "If you were on a deserted island and whispered a price, brokers would swim to you, with their fins showing". Heres a funny post on an insurance instagram account insurance folks just love, and its spot on about what I am talking about:

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

A) Binding authority, or the pen, is given to a wholesaler where there are strict guidelines on what they can and can not write. For example on property, things like occupancy/tenants, year built, construction class, roof age, distance to coast, updates to electrical system/plumbing/ac with in last 10 years, number of stories, total insured value, cost per foot are all what wholesalers will call "the box". if the risk fits the box, the wholesaler can issue a bindable quote immediately - there are folks that crank out 25-30 of these a day. No need to talk to an underwriter or get approval. The approval was provided when the guidelines were set out to the wholesalers. Maybe you might have a deal that fits 8 of the 10, then you have have to go get approval from the carrier. The pricing is all pre-set with rates and then you get "scheduled credits", you'll hear people say all the time, we maxed out the scheduled credits on this meaning thats as low as the price will get. Then every quarter the auditors will come from the carrier and check a bunch of policies to make sure all the documentation is there and the risk fits the box. if you write a bunch of deals that are not inside the box, you get your contract pulled. no more money making. So there are internal folks at the wholesaler that double check what the newbies are writing to make sure it fits. These are not big deals, they are like $1000-$15000 maybe $20K deals max. As am individual wholesale broker you are not gonna get rich cranking out these deals for the rest of your life, you can make a living. The guys that hit it big are in the brokerage deals, doing $250K-$500K+ deals, thats where the money is. Its always fun writing a new piece of business, big or small, but renewing it is the trick. If you write 10 deals as a wholesaler on binding authority, you gotta renew those 10 next year. It can become tedious and time consuming. And there in lies, the rub, lets say the binding authority deal gets shut down, now you gotta roll the entire book to a new market, lots of work, emails, time, phone calls, you are responsible for notifying the first named insured they are getting non-renewed with statutory time requirements. I mean its a shit load of work. Also, sometimes, the binding authority guys forget to notify and then the retailers catches wind of that and says "you gotta offer renewal" even though the carrier wants off the risk but they are stuck - legally they have to put out terms. So this is like the tail risk of these programs. Shutting something down takes a ton of time. Could take 12-18 months to actually get off all the risks you want to as a risk bearer. The admitted carriers have this but it is on a portal and its retail facing. As a retailer, you can get quotes from admitted markets just as fast, as long as they fit the box. Quick comment of pricing, if you are good in your region and you know the type of account, who the carrier is, you already know what the client is paying. its funny when policies come in redacted and the client thinks they are playing some game. we laugh in the office, "Oh, we got a professional shopper on our hands". We just look up that carrier with a similar class of business in our system, we can tell what they are paying within a 5%-7% margin. I just pass those to the young guys in the office to work on, I want to whale hunt - more fun and obviously better incentive. You are not gonna see wild disparity in pricing. A carrier who quotes a deal, will quote it very similar for the same situation 2 blocks away. But the key is its not always the same situation. For example, same business, same city, 1 is in an old building, 1 is in a brand new building - you are gonna see disparity in pricing. Mostly because the better carriers are gonna jump for the newer building. B) Wholesalers do not take risk at all. there is no "making the quarterly number by writing business". Wholesalers can only grown by getting more submissions from their retail insurance agent partners. The good wholesalers are on the road meeting agents drumming up business, they are not in the office. A wholesaler will call on a retail office for months/years before they start getting flow from a retailer. Because the retailer already has 5-7-10 wholesalers that they are buddies with anyway. The key to wholesale, and retail for that matter, is having markets no one else has. Because an insurance agent/broker can not write business without a carrier partner. An insurance agent/broker is only as good as the carriers they represent. The best agents/brokers have access to the best markets. Period. Full stop. You could have the best relationships with the biggest accounts but without a market to get quotes, you got nothing. When a new market comes into a market, everyone calls and says "we have the exclusive with XYZ carrier". Bullshit, everyone has them or will be getting them. But thats how Wholesalers make new friends in retailers because maybe they got the new market first and the retailer needs that market so the submission comes to that wholesaler and boom, new flow starts to come, team flies in and meets everyone, and now begins a new relationship. Retailers would prefer to write everything admitted, better comp for them and they are closer to the underwriter. A submission will come in, retailer will check the admitted markets for pricing/see if they are blocked, and start negotiating. Wholesale is the second option. its not bad, its just another part of the overall distribution. Insurance is just like NFL. Its a copy cat league. Once somebody starts being successful with a product or a market, everyone hears about it and then everyone wants it - clients are the last to hear about it. they just want to talk price. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Don't know WTW like I want to. They are an amalgamation of a few firms. Just doesn't seem like they have found their footing. One of the guys who was fired for lack of production at Brown runs a team at WTW in my region. That probably taints my view on the business unfairly. A huge team left WTW in my region during the AON/WTW talks. That was a big hit in revenue at that time. Just seems like its a big company looking for leadership and trying to find an identity. Wish I knew more about them. I was consulting for a big account, they had WTW as their agent. Had a call with their "Broking team", and the first thing they said was "We broker deals European style". I guess that may impress some folks but I remember the call was a little weird and I said "Do you accept euros? Cause the client is gonna pay in dollars - lets just get best execution on the trade". Odd they are changing the reporting segment names, just looks like white paint. My post on WTW is getting super negative, and I don't want to be negative, I really don't know the company as well as I know others in the business. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

The Captive was set up by Brown to actually help them write more retail facing insurance. Brown has some programs where they have the pen and because of the hard market, Brown lost capacity to write business. This posed a problem because without capacity Brown could not serve their customers. So they set up their own Captive insurance company to fill the gap/holes in the program and allows them to keep writing the business they want to write. It is SUPER conservative and well done for sure. Big brokers have been doing this for a long time. Usually in big towers where no risk bearing insurance company wants to participate high up in the layers for a small part of the tower for a small premium, so the broker just puts the risk on their balance sheet as like a one off (they might fill the tower later in the year, client may/may not even know). Brown is different because it is more methodical and the Captive is designed to serve the retail production of insurance and the numbers work because its conservative and its re-insured. CFO commented on the conference call the max payout is like $25M, not that much considering the volume on retail commissions the Captive supports. This comment is where Andy mentioned "We look to the Captive acting a little like a contingency payment". What he meant was their lens is they could go through the season without taking a hit on the Captive or take a $25M hit max. A contingency payment is similar because if lets say Brown has $500M premium with Travelers and expects a 5% contingency payment ($25M) if the book performs well, then Brown gets $25M but if the Travelers book has a hick-up - maybe some big claims, and Travelers does not pay the $25M, Andy is trying to compare the Captive in that fashion. Its $25M in revenue as contingent payment or nothing because of claims VS. Nothing because there were no claims or a $25M loss in expense due to an event. There's probably a tax treatment for the loss as well that reduces the hit (dont know this, just speculating). The captive supports Cal Fire and Florida Wind. Unknown, if its 1 or a couple captives. The actuaries call that "diverse". It may be or may not be. But its helping Brown make money on the commission side and they are not taking ALL the risk, its shared. Its actually a total cultural shift for Brown - cardinal rule for Brown is "We are not in the risk bearing business". One of their other culture statements is "We are in the money making business" so when you cant make money selling insurance because their is no insurance, you gotta get creative. I give the management at Brown credit for setting this up, shows they can change. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

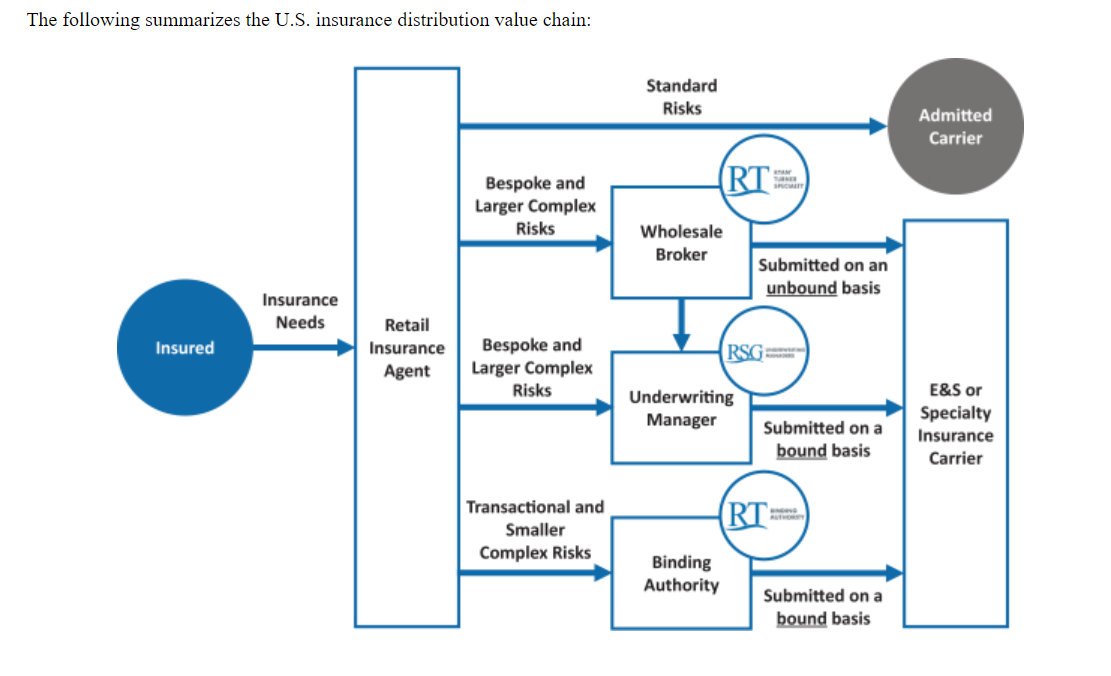

First on Ryan, then Kinsale. This is what RYAN are building (see below - taken from Ryan's S1). Actually pretty good for the thread on what the actual insurance distribution landscape looks like. Efficient in some ways, others not so much, but insurance is just hard to put in a portal and spit out a quote - case in point look at Lemonade (LMND). The chart shows how vital the retail facing insurance agent is to the distribution system. Pat Ryan owns too much of AON so he couldn't be a retail facing agent, so he just took the wholesale segment by storm. The underlined "bound" terminology is SUPER important. When you as the MGA/MGU can bind, it means the insurance company has given you the underwriting authority. In the trade, its called "the pen", meaning you can write it. This is where the MGA/MGU does all the work and really the insurance company just sits back, manages the book, collects checks and pays claims. Wholesale Brokerage is where a retailer needs help placing a portion of an account the admitted market wont write period or wont write competitively. In my region, wholesale is a huge part of the business. When ever people refer to the E&S market or Non-Admitted market, a wholesale broker is involved. Pat Ryan put it best, E&S is freedom of rate and form. Meaning carriers can charge whatever they want and throw down whatever coverage they want. Versus the admitted market where the carriers have to sit in front of the insurance commissioner, get the coverage language approved and file the rates they want to charge for approval. EVERYONE that Ryan hires is like 25 and super Type A. Young and aggressive. You can call a random number at Ryan in a region you need to place a risk and get an immediate pick up or call back in like 2 hours. Never fails, they dont know who you are but they are ready to talk about a deal. Its pretty incredible. I'm sure there are lots of folks who call back but it is seriously a culture thing at Ryan. And the older folks who are there were bought in a acquisition. I'm long RYAN and probably should have bought more. I bought some more when it tanked after earnings a like 2 Quarters ago. Pat Ryan was buying big chunks himself. Which I loved. The story of how Ryan got started is pretty awesome. For another time. KINSALE 2nd tier risk bearing insurance company who writes the stuff no one else wants to write. They will quote things no one else will. I have not looked at the business as investment, but we trade with them and they will turn things quickly. Gonna be on the tougher classes of business for sure with some language that is favorable to them, not the insured. Doesn't make them a bad market, this is just how companies grow up into bigger risk bearing companies. Gotta get your start on stuff no one else will write. There are worse insurance companies than Kinsale so they are not bad, they just are a carrier who doesn't have any polish. Markel started this way, and actually Markel and Kinsale compete on business in my market.

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

According the Lloyd's Chief of Markets, Patrick Tiernan - 50% of the business written at Lloyds is US Based, 10% Canada, and 40% is the rest of the world. Decent stat but tough to really use because of the regional nature of insurance and the risk bearing companies being localized. Tough to say what foreign markets are growth markets. If trying to handicap where growth markets will come, my hunch is where ever there is a growing debt market for real estate/business in general - insurance will follow. Where ever there is a contractual obligation, insurance will follow. No debt, no contracts - no insurance. That's true in the US at least. Client might purchase super cheap insurance but not like what a bank or a contract will require. Its gonna come from where you think it comes from, maturing economies, growing GPD's. Other item is the non-competes - just don't know how well they stick internationally (never did the work on it). They have to be decent or guys like Brown wouldn't be playing. The non-compete is one of the most important parts of the brokerage business in the US. (Forgive me if I already said this), When a retail facing agency, the one who gets the paper work signed and collects the money from the insured/the buyer, signs an agreement with a carrier/wholesaler/MGA/MGU (we will make up some more acronyms soon enough), the agreement says the AGENCY owns the expirations of the book of business with the carrier/wholesaler/MGA/MGU. The AGENCY is the one who owns the relationship, individual producers will not have agreements with carriers, the agencies do. Now, the actual broker/producer may have ownership in their book, the actual accounts - could be a split where if the producer leaves, they can buy it at a price from the agency - usually pre-determined in the producer agreement with the agency, or like in the case of the big publicly traded brokers - the producers don't own a darn thing, zero, zilch. That's the asset. The book is the asset. Important to note contractually, the carriers do not own anything, theoretically the carriers/wholesalers/MGA/MGU's serve the retail facing brokers, if the broker wants to move it (tells the insured hey lets move from this carrier to that carrier) they move it. I'm sure the set up is similar internationally but just never seen one. Theoretical because it is supposed to be a symbiotic relationship. But sometimes it is not so sympatico, brokers threaten carriers all the time "if you dont do this for me, im gonna move my book" bla bla. I've never done business that way but people totally do. Or the inverse, there is only 1 carrier who will quote, so that carrier owns that particular market/line of business in that class of exposure. Had a call just today where we were trying to negotiate some language on an endorsement and the wholesale counterpart said "We are one of MunichRe's largest money makers, they will do what we say". I was like, ok, thats fine with me. I have placed accounts internationally and its usually a paper work/clerical nightmare as a US based Broker. For example, the Bahamas really makes it tough to write business there if you are a US Broker (Bahamas Insurance Commissioner wants the money to stay in the Bahamas). Probably similar in other countries as well. Again, the regionality of insurance is important - each region of the world has their own set of unique things and when a broker shows up in that market, they are probably gonna get smoked because they dont know the players. I tried to place a deal in Hong Kong once, made 1 phone call to a friend, referred me to the Asia team, and immediately got told they had seen this account 3 times in the past 3 years. They did quote for me but was impressed how easy it was to get someone who could help me. Placed a deal in Mexico and just found a broker in Mexico who specializes is placing Mexican risks for US Brokers, we just split the commission. Other item I have heard a ton about, specifically in South America, is the stamping of policies - specifically in Reinsurance. Important because when there is a stamp, the premium is noted and the taxes/fees are collected by the regulating insurance body. In South America, and other international countries, where the stamping is not really regulated, the carrier might quote $100,000 for a risk, and the broker tells the client its $120,000. So in addition to the commission, broker pockets an extra $20K when they collect the money from client. Again, much easier in re-insurance but I am sure it happens a decent amount. Would have to assume (famous last words) with big public brokers this doesn't happen but.... Hope this is helpful, glad I can share something where I have some background. Everyone on site is always nice and helpful. Been selling insurance for 16 years and family been doing it since early 1930's. I'll end with a quote a I heard, just thought it was 1000% accurate. "Insurance Brokerage business is A+ money for C+ players". The public brokers are not C+ but there are some folks who work there that are definitely C+ at best and pull down some serious cash. 2nd Best business in the world, Software I guess has to be better. Said that to someone once, and they said Churches are the best business in the world. No taxes. Cheers! -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

The bigger you as an individual producer get, the less you want to leave because you are making enough money to stay and don't really want to "start over". You would leave to a competitor if they promised to foot the legal bill. And it may get ugly with clients who are on the margin - long time clients don't care about lawsuits but newish clients will be confused when the producer they work with is getting sued. Reason to leave is if a broker is entrepreneurial and wants their own freedom. But at a point, the money doesn't motivate people. I know a guy who has an $10M revenue book and makes 20% commission on that book. One hurdle leaving would be a couple of the markets he works with will not honor an "agent of record letter" so the business is stuck at the shop hes with. That Producer could make double anywhere else but he is just gonna stay. He is showered with stock so I guess it evens out. Still tough to argue why a smart intelligent broker with actual clients would work for a big shop. But if the producer doesnt want to run payroll, manage employees, deal with office BS and just sell - then a big shop is where they would be best suited. Difference between the big publicly traded brokers is how the teams are set up. Some producers hunt alone and some need teams to support their books. Some shops are very financially analytical about the set up running individual book P&L's and others just run with pooled support teams/resources. Insurance Office of America (IOA) has a model where the producer gets the lionshare of the revenue with a centralized service team offsite. You are buying a book of business with a 95% renewal retention. The acquisitions are the "extra growth". Hard to mess up an insurance agency. An idiot could run an insurance agency with 20% to the bottom line. With some financial reporting and diligence, that idiot could get it to 35% but would have to cut Producer comp and that usually causes issues with producers. Other item is account minimums. Some of the bigger shops wont touch an account unless it can hit $25,000 revenue ($200,000 - $250,000 premium rough number). That culling of the book usually gets distributed to the better local/independent shops who can write smaller accounts profitably. Great example of why I work at my own shop, phone rang Wednesday with a new deal, spent 3 hours Wednesday teeing up some applications, making the submission look tight, spent Thursday working the phones, and Friday quotes came in, bound coverage 6pm for $100,000 premium. Will make $12,000 for 2 days worth of work. and it will renew next year because the contract requires the coverage. Almost impossible to shop what we did based on the class of business. So yeah, growth can come from anywhere - you never know what is gonna happen when the phone rings. As a client, all the brokers go to the same markets and there is some favoritism (usually with a certain underwriter/producer, not on a company level) with certain brokers but overall everyone gets "the same price". Clients who bank with a local bank with typically have an insurance broker who is "local" rather than a big name insurance broker. Lockton (privately held) gets a good look because of their private nature from some key accounts. Best way I have thought about it is if you sell insurance and your fraternity brother became the CEO of a huge company, you could write the account but might get a little out of sorts quickly if you dont have the claims support/service team ready to keep up with clients needs. But again, there is no limit to what a small shop could do if the relationship with the client is there verses the big shops. The client is the boss. The key for any producer is equity in the book, if they have that, and the shop sells, they will get a payout. Most people/clients, generally, are conditioned to think bigger is better. But we write some nice accounts the big shops would love to have however clients will never go to the big shop because they know pricing will be the same and the client is happy with what they already have. Clients get that there are only a few markets in their space that can write their account. If the producer is serving up their account annually, and gives a market summary, that is all the protection you need as a producer. However, if you just send the account but never really work it and a competing shop sends the account and gets better execution, thats the risk. I dont feel it has anything to do with size or being public, I believe its how the account is sold to the market, how the risk is sold to insurance underwriters. So in that case, one could be made to look pretty stupid if a market quotes an account for another agent, and never quoted it for the incumbent agent. Overseas is where new growth is - economies are maturing and insurance is being purchased with more frequency and size. US is one of the biggest markets, not because businesses want to de-risk by purchasing insurance, its because it is mandated. Bank lends you money to buy an asset, bank will require insurance, have a fleet of trucks with a loan, need to insure the trucks, and the state regulatory body will want a copy of insurance as well. Leasing a new office space? Landlord requires insurance. This is not the case globally but is starting to become more prevalent. -

WSJ featured 2 articles on rising auto insurance cost as well. https://www.wsj.com/articles/auto-insurers-rising-rates-are-no-accident-11674589118 https://www.wsj.com/articles/car-insurance-rates-are-soaring-with-little-relief-in-sight-66138e2a

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

MarshBerry puts out a study on agencies. Last one I saw showed count for agencies is roughly 36,000. The majority of these businesses are just what you see in your town/city - a retail walk up office in a stripe center where the owner has a couple employees and runs all expense through the business. 60% (21,000) are under $500K in revenue so they are small and not acquirable. Next cohort is $500K-$2.5M which is about 11,000. So 88% of the market is sub $2.5M revenue. Owner is the largest producer, owner writes the checks, its kinda funny to see some of these antique businesses - a testament to the staying power of insurance brokerage for sure. These are still not "businesses", they are just little sleepy offices where people buy insurance with maybe a handful of "large accounts". Its the next tiers where things start to get organized - proper Controller/CFO where you might have a small management team running the business. There are roughly 2500 $2.5M - $10M revenue shops. And then the air thins at the top, $10M - $100M like 680, and $100M+ is like 45. With the bigger shops, you have multiple owners - producers who are producing buying into the agency. Teams of producers or large single producer will leave big shops and starting up their own deal (thats what we did). Couple of smaller shops band together to get above the $2.5M - $3.5M mark and then sell due to the big lift in multiples. Specifically with BRO, they are smart, intelligent managers who understand price paid and will not chase a deal. They really were the pioneer in the buying of smaller agencies in the early 2000's and built a machine. Multiples have probably peaked and with interest rates inching up, values have already started to come down. Risk for BRO is producers leaving, they have to keep them happy with no reason to leave. This is an elevator asset business. Even if they leave, some young good looking producer will be sent out and save the day on a majority of the deals. People inherently don't like change, its pretty incredible actually how people complain about insurance but do little to shop around overall - an account that is a shopper will always shop but most just want decent service and phone/emails answered. It's really hard to poke holes in business model. And BRO is better than most on how the business is managed. Florida will always loom tough for insurance in 4 distinct areas - Least Diverse (Risk bearers like diversification), Least Predictable (wind blows or it doesn't no one knows when and how much), Capital of Litigation, and Capital of Fraud. This is a tough place to do business as an insurance company. HOWEVER, state needs insurance and people will use agents. Unknown how marketplace shakes out but the brokers are not disintermediated with state funds selling direct (my opinion). Florida is still one of the fastest growing states and obviously needs insurance to support debt on homes/businesses and employees/cars. BRO is definitely aware of the need for growth. Prediction is more growth comes internationally rather than domestically. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

saw this and will give you some thoughts later. -

Buffett/Berkshire - general news

longterminvestor replied to fareastwarriors's topic in Berkshire Hathaway

Note was written with a hint of tone that is atypical to the Berkshire news releases. Second time I have noticed tone difference coming out of news from Berkshire, first time was also in relation to the Japanese investments. Above quote is just odd. Not odd that Mr. Able/Mr. Buffett want to own more, just odd that there is a quote saying same. -

Interview with Kara Raiguel - CEO of GenRe

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Good report. Thought it was interesting how PB commented on PL/D&O market with lots of capacity due to market pull back on property – risk bearers needed to deploy capacity and they are now competing on PL/D&O. he goes “I am not saying that, but some would say that”. Just thought that was funny. Can confirm we are seeing that, we just doubled the limit on a D&O placement for publicly traded company for the same price last year – 2X limit for same premium. Regarding Florida/Citizens Insurance question. I was in a meeting once at Brown – this is 10+ yrs ago and the word was “Where Florida goes, so does the rest of the company”. PB downplayed Florida yesterday on the call – my gut/my opinion, Florida insurance plays into BRO revenue/earnings – materially. I think I know why management is attempting to dissuade street from thinking BRO is buoyed to Florida. Here is some data: As per 10K’s, revenue in Florida as a percentage of revenue: 2022 - 19% of total revenue comes from 55 offices in Florida 2021 – 18% of total revenue comes from 55 offices in Florida 2020 – 19% of total revenue comes from 55 offices in Florida 2019 – no breakout – mentions 52 offices and headquarters in Florida 2018 – no breakout – mentions 46 offices and headquarters in Florida 2017 – no breakout – mentions 41 offices and headquarters in Florida 2016 – no breakout – mentions 41 offices and headquarters in Florida 2015 – no breakout - mentions 41 offices and headquarters in Florida 2014 – no breakout - mentions 41 offices and headquarters in Florida % numbers above from 2020-2022 are deceiving because Atlanta wholesale office’s produce huge amounts of Florida borne business and yet the “office”, as you know, is in Georgia – not Florida. There could be other wholesale offices outside Florida that have relationships with Florida agents and place deals in Florida – would be tough to get a “to the penny” number on % of revenue deriving from Florida based on the way reporting goes so Brown reporting by office geographic location is logical. CITIZENS REVENUE BREAKOUT FROM K’s YEARS AGO: 2014 - $3.8M 2013 - $5.7M 2012 - $6.4M 2011 - $7.8M 2010 - $8.3M PB’s comment on Citizens commission was 100% accurate. Premiums are higher today than they were when Citizens played into the market in 2006-07 – 2015ish. Risk is legislature reduces commission at some point if premiums continue to rise however for the work we are putting in as agents, gonna be tough to justify. But that politics, not insurance (I guess they go hand in hand). Also – did a quick search in AON, Willis, Marsh 10K’s – no mention of Florida at all and revenue aggregation in Florida. WTW disclosed 21% of revenue generated from UK Aon disclosed 55% of consolidated revenue is non-US Marsh is a little different – 51% of company revenue is insurance, 10% reinsurance, and 39% consulting. Marsh does disclose 51% of total revenue was from outside US -

iSavings bonds yielding 7.12% currently

longterminvestor replied to Spekulatius's topic in General Discussion

Found this on Treasury Direct. Pretty nicely presented. i-bond-rate-chart.pdf -

Here is some more chatter on what Berkshire is doing in Florida marketplace. Berkshire - Florida Citizens program.pdf