.jpeg.66c448bf718e7352b2952f5c41faa6d7.jpeg)

longterminvestor

-

Posts

383 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by longterminvestor

-

.thumb.jpeg.b0384a4135d041bebd0e39ae144d51f4.jpeg)

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

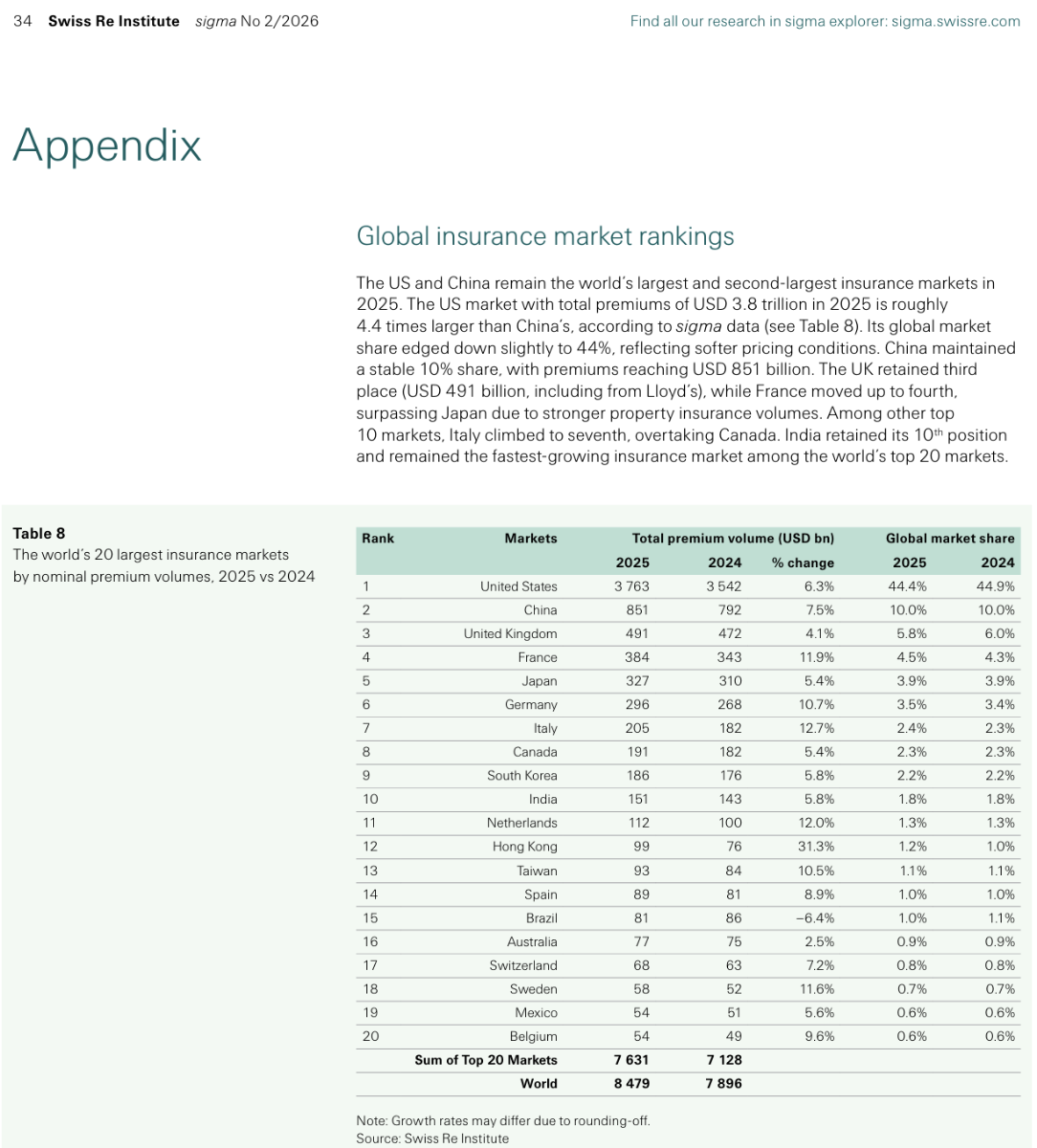

Global insurance market according to SwissRe. 44% of global premium comes from US ($3.7T). China is #2 with 10% global share. Can not shake thought.....GEEZE, the US loves buying insurance!! Or brokers are really good at selling to US buyers of insurance. Old timer told me once, "Insurance is never bought, it's sold". As world economies mature, expect a global lift in premiums. Hence brokers looking internationally for growth. Strikes me how low the base is for some very mature economies. WOWZERS, 31% growth in Hong Kong?!? Other note, there is 1 market in the top 20 with decline, Brazil. Not picking on Brazil, just sticks out globally there is 1 market with a decline and all 19 markets (and global sum) are growing. Relative GDP's, Canada & Brazil are similar however Canada buys 2X+ amount of insurance than Brazil. Mature economies demand insurance to mitigate risk, its a natural progression. Developer want to build a data center on cheap land with access to cheap power? Capital markets will provide investment capital to build however demand their investment is insured. Just another item for attorneys to fight over. Brokers coin it when capital markets demand contractual insurance cover. 2026-07-sri-world-insurance-sigma.pdf

-

250 years ago, we decided after much debate, a life of tyranny was no life at all. The usurpations of a crown 3500 miles away became insufferable. After repeated petitions for redress went unanswered, we declared our independence from King George’s heavy hand. This declaration from the shackles of British rule birthed the American Spirit. The ideals of America were not given. We had to take them. We fought for the dignity and freedom of religion, speech, press, and assembly. We fought for equality in the eyes of our creator. We fought for life, liberty, and the pursuit of happiness. And we won! Once achieved, these freedoms have unleashed the greatest nation the world has ever known. Today is a celebration of the American Spirit. May we never give into tyranny. Happy 250th Birthday America! Home of the Brave! Fly your Red, White, & Blue with Pride!

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Missed this one @adventurer. Did a little writing on Hard/Soft in previous post but we can go further. Going long brokers in a hard market and short brokers in a soft market is similar to going long Goldman/Schwab in a bull market and shorting in a bear market. Looks easy but not as easy as it looks. #1 - Its difficult to generalize overall market as Hard/Soft overall due to the subsections of insurance. Property market going hard/soft gets the most attention, especially in CAT regions because the swings are huge. So any broker/carrier who writes CAT business, are subject to large swings up or down in market cycle. Homeowners gets alot of attention but generally is not a good barometer of where market is because its typically written admitted and state governments look for votes and voters are sensitive to homeowners premium. So soft homeowners doesn't mean soft everywhere. Each "line of business" has its own cycle AND each line of business is either being placed admitted or non-admitted (E&S) which will have its own cycle as well. Commercial Auto, Property, Casualty, Umbrella, Workers Comp, Professional Liability, D&O, EPL, Cyber, Homeowners, and personal auto are all different lines of business and are all being placed either admitted or E&S. Meaning Commercial Auto can be soft while Casualty is hard. Professional can be hard while Work Comp can be soft. There are also sub-categories for each. Property is broken up by CAT/Non-CAT. Commercial Auto is broken up in Trucking (interstate & intrastate), local service, fleet (250+units), even a personal fav "non-emergency medical transport", Casualty is broken up by class as well, Habitational (Hab for short), Lessors Risk, Heavy Products Liability, ect. And the complicate things further, the regionality of insurance plays by line of business's hard/soft cycle. Meaning Commercial Auto in NY can be hard while Commercial Auto in Texas can be soft. EPL (Employment Practices Liability) is a good one because Cali EPL is much harder than other parts of US. You could take a firm with 100 employees in Iowa, EPL spend might be $12K with a $10K retention - Move that account to Cali, spend is $25K with $50K retention. If you listen to the conference calls of brokers and carriers, they will break out their own rate increases/decreases for each line of business (LOB) - some even do it by region. For example, Property could be down 5-10% while CAT Property could be down 25-35%. Long winded answer to say when someone says "Its a hard market", make them explain what area of the market is hard because I could tell you 5 other marketplaces that are super soft at any given time while others are just flat. EXCERPT FROM BRO Q1 CALL DISCUSSING RATES: From a commercial insurance standpoint, the changes in rates remained relatively consistent with prior quarters except for CAT property, which declined further than in the fourth quarter of last year. Pricing for employee benefits was fairly similar to prior quarters with medical costs up 8% to 10% and pharmacy costs up over 10%. We continue to consult and advise our customers on multiple strategies that can be employed to manage high-cost claimants and pharmacy spend. We leverage our extensive consultative solutions to deliver high-impact strategy for population health, captives, stop loss and carve-outs for certain services. Shifting to the rate environment, the admitted P&C markets continue to be in the range of flat to up 5% versus prior year but did moderate slightly as compared to last quarter. Workers' comp rates remained flat to down 3%, while we saw a few states increase rates modestly. For non-CAT property overall, rates remained down 5% to up 5%, depending on the loss experience and the location. For casualty lines, rates increased 2% to 5% for primary layers, with excess layers increasing materially more. For professional liability, rates remained similar to the last couple quarters and were down 5% to up 5%. Shifting to the E&S market, let's split the conversation between property and casualty. For property, both wind and quake rates declined -- rate declines were modestly more than we experienced in Q4 of last year. Most of our placements for the quarter were down 15% to 35%. At the end of the quarter, we saw placements above and below this range. Generally, customers are capturing most of the savings. However, some are utilizing the savings to decrease deductibles, increase limits or buy other lines of coverage. These tactics are common when rates are moderating or declining. On the casualty front, not much has changed versus prior quarters. The ability to get higher limits is extremely challenging. Pricing continued to increase. Primary layers are becoming more expensive, and carriers are decreasing the limits they'll offer. We do not expect this trend to change materially over the coming quarters. #2 - Relationships with brokers and carriers are symbiotic and very tight - not at all antagonistic. A good broker builds a super strong relationship with a carrier and thats how a broker can win new deals. A broker is only as good as their carrier relationships allow them to be good. You could have the best account in the world as a broker, but if your reputation sucks with carriers, no one will help you place the deal. Wholesale has changed this dynamic because retailer is once removed from carrier relationship. When a tough deal needs to be placed, a broker will call their best relationship and say "hey, need you on this one" and carrier will think outside the box on that account because of the relationship - Underwriter can make an accommodation based on the risk, the account, or as a broker accommodation. Brokers are constantly trying to get better terms in the risk transfer market and need good/great relationships to do that for their clients. Think about it, at the end of the day, its the insurance company who pays the broker (using client funds). So naturally, brokers have to have good relations with carriers. Generally, I do not see how brokers zig while carriers zag. If carriers are taking in less premium, that means they are paying less commissions to brokers. If a carrier is growing, that means its being fed business by brokers - carriers are bringing in more business and paying commissions to do so. Brokers are always trying to get carriers to write deals they dont want to write and ask for higher commissions. A broker can not get one or both if the relationship is "antagonistic". On a personal note, as a broker, our team may interact with a typical client a dozen times throughout the year for general service/issues/questions ect. Our team will interact with a typical underwriter 4-5 times a day via email/phone on the 10-12 deals we are trying to place that given week. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Listened to this podcast, RYAN section only. I'm, self admittedly, a tough critic. They are directionally correct with a few things however they make assumptions that are not accurate. Again, bodes to the thesis that distribution and the consumption of P&C insurance is greatly mis-understood. Property Casualty insurance overall is just mis-understood. There are just mechanics to insurance that are 3 & 4 layers deep that can confuse the highly intelligent investors/buyers of insurance which supports a role for brokers in the digital world for the foreseeable future. One assumption made was "Admitted vs. E&S" and why business flows into those marketplaces respectively. #1 - Every broker is incentivized to place business in the admitted market. Typically, not always, but typically an admitted placement has no wholesaler so theres no split on commission. There are certain niches/carriers who pay as high as 22%-25% commission and as a retailer placing that direct, there is no split with wholesaler - typical commission is 15%-17.5% admitted - E&S varies but 10%-12% net to retailer and 7.5%-10% net to wholesaler (Gross 17.5% to 22% is norm in wholesale + FEES....many transactional E&S policies have a $250/$500 fee in addition to commission that goes to wholesaler - some have $2500/$5000 placement fees). The extra kicker is the contingent commissions paid as well in both scenarios - when retail places admitted direct - contingents go to retailer, when placed wholesale - contingents paid to wholesaler. The reason for "preferred wholesalers" is driven by an arrangement with retail/wholesale where there could be a split on contingents so naturally a retailer will want to load up with 1 wholesaler if the retailer participates on contingents placed thru wholesale channel. Bored yet? Putting folks to sleep? Probably....thats the opportunity...insurance transaction usually just ends with "okay, lets just buy this already and deal with it next year. Its so odd actually. Its true not every retail agency can have the expertise to write up every deal that comes across the desk so naturally a wholebroker is engaged to work on accounts where no admitted market will write OR a retailer does not have an agreement to place with the admitted market who potentially could write that business. But the retailer will not "disclose" to buyer of insurance "Hey, I know XYZ admitted carrier can write this well for you but we do not have an agreement to place business with them so I recommend you call Bob down the street, he can help you and I will pass". That never happens, the retailer will just send deal to E&S market and put a deal together, and if the relationship with client/broker is decent and the price is right - the deal will trade E&S. When a large broker purchases an agency, the first thing they are gonna do is cull the E&S book and see what admitted's will offer terms on whats already there. The accretion on revenue is significant. Recently acquired broker who has $10M of premium spend E&S and getting paid 10% ($1M revenue), if that can be rolled admitted, and make 15%-17.5% or even 20%, that is a large increase in revenue for the recently acquired shop to a favored admitted carrier who has a large relationship with admitted XYZ carrier and immediately appoints newly acquired retailer. In those situations, folks like RYAN, AmWins, RPS, Bridge - will lose - but retail broker/client win. Directionally correct because E&S has been growing significantly over the past 7-10 years. Mostly because the playbook relies on a lazy retailer. Theres lost of follow up and convincing that needs to happen to get an admitted carrier to write "new" business - they just ask lots of questions (they are underwriters...obviously they ask questions). But many times an E&S brokered deal can be put together faster so if speed is the game, E&S is the cure. RYAN, AmWins, CRC have been building an army of sales folks getting weekly meetings with retailers saying "let us do the placement of coverage, you manage the client relationship." -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Thanks. Found it: https://podcasts.apple.com/us/podcast/scuttleslops-openai-valuation-ryan-specialty/id1786912203?i=1000774614060 -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Hub International files for IPO. Top 10 brokerage firm globally. When there is more info available, will do more of a deep dive. 1 of many articles below: https://www.insurancebusinessmag.com/us/news/breaking-news/hub-international-files-for-ipo--whats-it-worth-580619.aspx -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

article is behind a paywall. when it went to print, speculators followed hence the volume/price spike. https://www.insuranceinsiderus.com/login-access?returnUrl=%2F&zephr_sso_ott=rhsIeg -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Maybe this will help folks understand of hard/soft market cycles. Insurance market "hard vs soft" is identical to stock market "bull vs bear". Bull Market = Soft Market attitudes, Bear Market = Hard Market attitudes. In a Soft market, underwriters lose their minds, make irrational decisions with regards to fundamentals, no fear - everything is rosy, care free, underwriters say "YES" alot and "everyone is making money" attitude persists. In a soft market, the old school underwriters say "this can not go on forever" and the new guys say "you guys are dinosaurs, we are killing it".....until the roof falls in...or doesn't...thats the bet. Soft market means terms conditions get sweeter and price goes down = bad equation for insurance companies. and brokers have a field day because they are getting BETTER market execution for their clients albeit commission revenue does compress HOWEVER good brokers can sell more product into a soft market cycle. In a soft market, as a broker you just send an underwriter a competitor quote and say "youre gonna let this other idiot make all the money?" BOOM, they match or beat the price and in many cases they will increase the commission to sell their deal. Brokers really don't do a good job in soft markets for their clients because price alone is what the clients care about but a good broker can enhance the terms and conditions to the paper contract in a soft market with ease. A Hard market on the other hand, underwriters set the price, terms, conditions cause they know they are winning. Imagine being an underwriter for financial D&O for banks in 2007. You could put out quotes with a bankruptcy exclusion for a bank in a D&O policy and win! That defines what underwriters CAN DO in a hard market. Hard market you can put a roof exclusion on a property policy and client will still buy it. NUTZ right? Buyers/Brokers loose their minds in a hard market because things get tough, every underwriter says no. Gotta stick with your partners through the cycles. Its an amazing game. Mr. Buffett wins in a hard market. because he knows the risk is the same, its just he can charge more in a hard market. Think of it this way, does the hurricane know its a hard market when its coming to Florida or Texas? The hurricane doesn't care! It's coming (or not coming) just the same. The odds are the same either way, its the capacity being put into the market that drives drive up or down, hard or soft. Its just like stocks, the market doesn't know what you paid for the stock as much as you stare at it and fondle it, the price of the equity will go where it goes based on fear and greed or fundamentals of a good/great business. Just like the insurance cycles hard vs. soft. A good risk is a good risk whether its a hard or soft market, good risks just get better execution. ALL stock brokers look like kings in a bull market, just like insurance brokers look like kings in a soft market. The inverse its true as well for bear market/hard market. Dumb money shows up in a soft market. Smart money waits for the hard market. They very much rhyme. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

When you are worth $5B+, a couple mil is like our version of a cup of coffee. haha -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

substack doing a decent job describing industry. Says a BRO specific substack is forthcoming. Roughly right but I am a tough critic on details/mechanics. Writer has some nuance off buts a decent attempt to get understanding of distribution. https://open.substack.com/pub/eaglepointcapital/p/insurance-brokers-softening-market?utm_campaign=post-expanded-share&utm_medium=web -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Looking at Price to Cash Flow, BRO (13Xish) is cheaper than AJG (20X ish). WTW is cheapest on Price/Cash Flow however just seems like WTW is a wounded bird. Dont know the WTW business that well to comment but there was a large write off that scared me (WTW got smoked on a deal). I also like the fact that BRO is growing from a smaller base. But thats a personal thing. Big can get bigger, but there is more room for small to get big/bigger. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Believe "Graham Number" uses P/B in the calculation. My opinion, P/B has no bearing on insurance brokers because 65%+ of assets on balance sheet are Goodwill and Amortizable intangibles. The rest is cash, some of the cash is theirs and most of it belongs to their carrier partners or customers. Not trying to take away from the buying opportunity. Admittedly, I was early on the call to arms. I have bought at $96, $93, $78, $69, and $59. Obviously not very price sensitive. At first just saw, oh great I can own it, then as the price fell, in Mr. Buffett's words, the dog has "caught the car". I hope to buy more as cash becomes available, its a business I like and understand. As a student of insurance brokers and BRO specifically, its a business I know well and am confident in management. These are the tough times to hold any business, when the price is down significantly. Hard to predict market would hate on BRO so much. I was not buying early on any metrics or ratios. I just want to own BRO for a long long time (already owned and sold at a different time). I am pleased to have Mr. Market selling it in to me and others. Any buybacks at this point are very accretive considering Accession/RS was purchased using $5B+ on stock roughly at $100/share. Total consideration was $9.8B for $1.7B of revenue - call it 5.7X revenue. There's some hocus-pocus metrics math on what BRO actually paid using EBITDA or EV/EBITDA or multiple of EBITDA(easiest measure is the crudest - price / revenue). Remember, the 5.7X revenues was paid using stock valued at $100 to purchase roughly 50% of Accession/RS. If you take the current run rate pre-acquisition of call it $5.5B + $1.7B of Accession/RS you have $7B. That means the business is currently trading at 2.7X revenues ($18.78B Market cap). Buybacks are great uses of capital today (and paying down debt) so if you paid 5.7X using stock that trades at 2.7X, seems like an opportunity AS LONG AS everyone stays. When your stock is overvalued, use as currency. When its undervalued, buy it back. RISKS: BRO management has had to "re-tool" to manage the size of growing organization. One of my risks I see is management has not done enough work on "BRO culture works for 10K employees, can it work on 25K+?". There has been some cultural drift away from decentralization and more centralization which is gonna happen with a larger org. One of the things that always made/makes BRO special is the lack of "lets check with headquarters on this". -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Its hard to "grow organically" when your revenue is tied to premiums that are being reduced due to softening market. If client paid $1M last year, and this year they pay $500K, revenue will be down 50% however you have a REALLY HAPPY CLIENT. Which is the goal right, happy clients? 50% reductions are happening for some clients. Fine with results. More than fine. Buybacks will be meaningful if there are no targets at their price. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Integration risk in the insurance broker biz is simple. You are not focusing on systems, products, offices, profitability, or new business - the 100% metric for if a deal works is if the people stay - specifically the producers or teams. Yes, AJG talks about the "Candy Store" which is all the new products AJG will share with AP however AP has some products, due to their size, that AJG likes and wants to use so there is some cross pollination going on. And yes the overlap of dual roles in accounting or admin will sort itself out and there will be some cost savings by merging 2 offices in the same city/town (could take a few years to let the office leases to tail out) but very simple - the AJG management team is focused on making sure the real producers at AP are happy and will stay on long term, if that's the case, then the "integration worked". All the computer stuff and accounting "synergies" will figure themselves out. In many cases, the brokers all use the same computer systems anyway (I am unfamiliar with computer management systems of AJG & AP) however they all are similar in their own way. Just understand this, AP and AJG were fiercely competing on deals and now they are no longer competing so in a large merger like this one, the clients are the ones that get frustrated because now there is 1 less broker to compete on their business so a "professional" shopper has to now go find a new fish broker to "bid" their business if they think having multiple brokers help get their premium/terms down (everyone has their opinions on that). Many many times the accounts are so complex the client couldnt even shop their deal if they wanted to. Not enough capacity in market in some cases to support multiple proposals. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

London. Place will make your head spin for sure. You can win big or get smoked. Used to be a boys club. Still is but corporations have taken all the fun out of selling insurance. Part of the success is there is no UK CNBC on the floor interviewing brokers and UW's. They quietly make or lose money. When Mr. Buffett decides to take 5% of everything running through your syndicate, you know you are doing something right. Love love Loyds, I am heading over there in the Fall for some biz stuff. Its how business used to be, still stuck in time and may be up-ended with tech but who knows. Still a place you can get a risk placed if you know who to call and how to get the right people in the room. Recently upgraded to A+ which should have been for many years. IF you are researching, understand the concept of Central Committee or Central Fund. Thats key. Hint its kinda like FDIC insurance on banks. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Gonna defer to the GOAT and his opinions on this. Teed up to point where Mr. Buffett references the "General Agency System" which is parlance for MGA (Managing General Agent). Folks have been predicting the death of MGA's since the 1960's. NICO still TODAY, 60 years later, writes business through MGA's. NICO may have some pockets of direct biz or other lines in different channels - MGA's are a huge part of NICO's sauce. There are tons of reasons why MGA's provide value. See below -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Greenberg/Chubb also fired a shot across the bow. Including a Substack found and Greenberg's letter referenced. #stayfrosty 2025-chubb-letter-to-shareholders-from-evan-greenberg.pdf Chubb's CEO Just Challenged the Entire MGA Model.pdf -

2025 Annual Report - Greg Abel's first annual letter

longterminvestor replied to backtothebeach's topic in Berkshire Hathaway

Don't agree with sentiment of the announcement being "un-Berkshire-like". On the contrary, I see the announcement as more of Mr. Abel telling us "Hey, I am gonna doing this, I am gonna tell you now because I need you shareholders to trust me, cause I will will buy more in the future and will not announce a thing ", its a chiefs kiss. It was Mr. Abel telling the world "I am the boss now" in a kind way. Now he will return to Omaha to tend the flock. Mr. Buffett has taught Mr. Abel, probably bred into him at birth, to think long term. 1 announcement letting the world know "we are in the market" is very much Berkshire - Mr. Abel does not want to upset/spook long term A shareholders, my opinion. Yes, announcing you are a buyer hurts short term because you cant gather the shares you want quickly and in size. Private sales direct to Berkshire I believe is where the real size lies, open market is fine tho. This is a chess game. Mr. Buffett has had 60 years to think about how the movie goes on, he has thought about it alot. And his brain is highly geared towards playing at a level much more intensely than Mr. Market, and hope Mr. Abel inherits the bag of tricks under Mr. Buffett's desk. This change at home office is a coronation, this is not just oh, yeah, we are swapping out CEO's. This is a very personal thing - very much like passing the crown - I mean the GDP of Luxembourg is rivals Berkshire's earnings. Announce away I say, sit back and watch the world turn. This is a forever game, 2 months is nothing. This is a non-event. -

2025 Annual Report - Greg Abel's first annual letter

longterminvestor replied to backtothebeach's topic in Berkshire Hathaway

I am gonna give this a go (hold my beer @gfp). All based on recent 10K dated January 31, 2026, latest proxy dated May 3rd, 2025, and Gift letter from Mr. Buffett dated November 10th, 2025. So math below does not account for Mr. Abel's purchases or latest buybacks. Only smoke me in the comments if my underlying thesis is wrong, not basic share counts outstanding pls. As of Jan 31, 2026 10 K shares outstanding 511,820 A kind out (A Share price @ $745,200) 1,389,605,139 B kind out (B Share price @ $497.20) Voting is 1 A share to 10,000 B share Monetary value is 1 A share to 1,500 B share (monetary doesn't mean anything in the voting conversation) Mr. Buffett owned 206,539 A kind as of latest proxy and converted 1,800 A kind into 2,700,000 B kind and then gave them away...leaving him with 204,559 of the A kind as of now. Meaning Mr. Buffett controls 39.9% of the Berkshire vote....between us and Mr. Buffett we control the firm, ha! so...do the math...overtime, if Mr. Buffett's A shares are 100% ALL CONVERTED to B shares based on todays A Shares outstanding (511,820) minus Mr. Buffett's remaining (204,559) only 307,261 A shares will remain. Post 100% convert of Mr. Buffett A shares to converted B shares adding to already outstanding B, Total B will amount to 1,696,443,639. Totals if 100% of Mr. Buffett's A shares are converted to B: 307,261 A kind out - representing 65% of vote 1,696,443,639 B kind out - representing 35% of vote Voting Totals 307,261 A kind out - 307,261 votes (1 for 1) 1,696,443,639 B kind out - 169,644 votes (10,000 for 1) TOTAL VOTES OF ALL - 476,905 total (adding the converted 10,000 to 1 B and 1 for 1 A) Monetary Values (based on $745,200 for A & $497.20 for B) 307,261 A kind out - $228.97B 1,696,443,639 B kind out - $843.47B LETS NOT BURY THE LEDE! Lets say you are Mr. McRich and you want to buy 15% of outstanding votes of Berkshire Hathaway after Mr. Buffett dies. To wrestle just 15% control using A shares only, you have to #1. find them & #2. spend $53.31B! And if those Big A's won't sell to Mr. McRich....then you have to settle for the Baby B kind...you'd spend $355.675B (715.358M B Shares) which would represent 15% voting thru B only. Obviously you could do a combination of both spending less for the same 15%. Congress moves faster than Berkshire shareholders, 15% is not enough to get anything done vs. the remaining 85% "dyed-in-the-wool" Berkshire faithful.....I COULD NOT resist the textile pun there. There's probably and easier way to explain this using better math functions but this is how my brain sees the voting situation at Berkshire post Mr. Buffett. Hope this assessment passes the COBF seal of approval. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

RYAN trying to pass a law in Florida to make them the exclusive broker for State Insurance Company Citizens Clearing House....gotta love insurance brokers. https://www.insurancejournal.com/news/southeast/2026/02/09/857332.htm -

Buffett/Berkshire - general news

longterminvestor replied to fareastwarriors's topic in Berkshire Hathaway

you read it because its the intelligent thing to do. Its called the "Steelman" approach, a lesson taught to us by Mr. Munger. The practice of understanding an argument, usually the opposition, before sharing your thoughts allows for more fruit understanding of the underlying issue - its the pursuit of truth, not just opining because we are right and someone else is wrong. When you walk in their moccasins, you can bath in the idea. Its a way to invert the issue. Steelman is the opposite of strawman. I love doing it, it teaches me a lot. And to the author of the twitter post, yeah, most ideas are misplaced. Like the amount of leverage used in the comps. Mr. Buffett and Mr. Munger have told us time and time again, countless billions and billions have been left on the side of the road due to the lack of leverage at Berkshire - just so they could sleep at night. Not a terrible outcome, and something I appreciate very much. Leverage can do many things besides juice returns, it can lead to ruin just the same. -

2025 Annual Report - Greg Abel's first annual letter

longterminvestor replied to backtothebeach's topic in Berkshire Hathaway

Funny you bring up GEICO float vs. the rest of the book's float. I used to discounted GEICO float for a long time and focused on the CAT/Super CAT re-insurance business. I was looking at size only, the large numbers were awesome. I was not keying in on consistency/growth and other factors with reference to float. True, the CAT/Super CAT float is larger but lumpy vs. GEICO float. GEICO float is basically "take to the bank" float with very little surprises (sans hurricane/quake/COVID-19 payback). My study of GEICO has led me to Progressive and what they are doing (really interesting). Seems like GEICO is back in the game, had to do a lot of things to get that "car back on the road", seems like Todd had to be the bad guy and now new guy gets to take all the credit for Todd's hard work. I have thought deeply about float in general. and my study is pretty simple, float is easy to find. all you have to do is mis-price risk and float will find you. the key to enduring float is pricing the risk "your way" and then whatever comes in, is good business and the deserved results will find you. There are classes of insurance business with loss ratios sub 30% or even sub 40% but you can not build an enduring business on that class, its too competitive. Too many people shooting at it to drive the price down. Those lines of business are also not that large, relatively small. Again, back to the size problem, if Berkshire wants to build a business, the TAM has to be big. That's why Berkshire loves the personal auto market, because its predictable and the TAM is super large. -

2025 Annual Report - Greg Abel's first annual letter

longterminvestor replied to backtothebeach's topic in Berkshire Hathaway

"Chairman of the Board" is Mr. Buffett for now but not forever. Will watch that sentence in 10K for the years to come. Thanks for sharing -

2025 Annual Report - Greg Abel's first annual letter

longterminvestor replied to backtothebeach's topic in Berkshire Hathaway

Mr. Buffett is intentionally converting the shares to B and gifting to foundations. I have thought deeply about this and ultimately if a fund or individual accumulate enough of Mr. Buffett's A shares, that would be bad for Berkshire shareholders writ large - that kind of power in the wrong hands could be dangerous to the culture of Berkshire. There are curious consequences I have considered when Mr. Buffett converts his A to B causing the amount of A shares outstanding to be reduced is control. The A shares really should trade at a premium to B...but that wont happen because of the quick buck arbs can make. The A Kind in size, real size, should trade at a premium...but the arb market will take care of anyone "trimming" their A's by buying the A and converting to B. So basically after Mr. Buffett converts his A to B it will be VERY VERY hard to accumulate enough shares (A or B) to "control" Berkshire. I have believed this was the intent for many years. The size of Berkshire has also helped this problem. And I think this is what Mr. Buffett was trying to figure out once his wife passed. From my reading, it seemed Mr. Buffett's attitude when Mrs. Buffett was alive, was pretty simple - accumulate a big pile and have Mrs. Buffett give it all away. The "monetary value" of the shares after a point meant very little to Mr. Buffett after a point, his concern IMO its about the control of Berkshire that he cares mostly about. Mr. Buffett does keep score with money, as Mr. Munger has said "Warren, you are the most extreme lover of the big pile". Mr. Buffett laughed and said "That's true". -

2025 Annual Report - Greg Abel's first annual letter

longterminvestor replied to backtothebeach's topic in Berkshire Hathaway

Actually the folks on manufacturing line at Clayton DO CARE because the profitability of each home built is apart of their pay - its a bonus. And this goes to exactly what Mr. Abel is talking about, CULTURE. The culture of Clayton is such that employees are incentivized to NOT WASTE shareholder capital and do what they can to keep jobs under-budget. Felt compelled enough to mention because this is not always the case at subs inside BRK however the decentralized model is supposed to take care of little things like this, Mr. Buffett has done what he can to incentive managers of the subs to create schemes that celebrate profitability (winning) and when subs are losing money - managers lose as well. the comp plans for managers are fascinating at Berkshire.