WayWardCloud

-

Posts

367 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by WayWardCloud

-

Ah! It's hard to get the tone of a written post sometimes. I just opened the bonds threads for the first time ever and read the last 3 pages. Now I need an ibuprofen, why would you do this to me Happy Saturday!

-

Yep. Japanese equities in general seem to have a mind of their own and I actually love how decorrelated from other markets and sometimes from any kind of logic they are, it makes them a great portfolio diversificator. Thanks for the advice Gregmal! Wouldn't my bonds rise in value as their rates go lower?

-

Hopefully! I'd happily dip a toe back into Nintendo at 8000 Yens. Bought some Amazon on Friday for 3.1% of my net worth. Hoping to get more at $185 which would be a forward EV/EBITDA of 12. Maybe I'm delulu after 15 years of mega cap US tech crushing everything else but I find big tech cheap right now, especially Alphabet, so buying the dip seems like a no brainer.

-

Thanks for sharing your thoughts! How to you calculate the retail margins? I was considering adding Amazon in order to own the whole US cloud and I agree they hold very very good cards, unfortunately I have no confidence in the management since Bezos and his OG team all left at once and that makes it hard to pull the trigger. -Jassy does not seem like he has it in him to CEO. He has not made a significant mark to the business since taking over or even articulated a clear plan. His annual letter sounded like a list of quarterly numbers a branch manager would send to their boss internally rather than a vision. -They were opening hairdressers and cashier-less stores nobody wanted meanwhile got caught off guard by LLMs. -Their vision for Alexa 2.0 with AI is completely missing the point in my opinion. -They've been circling around healthcare for a decade without ever pulling the trigger -They're behind in self driving cars (Waymo) and robotics (using Nvidia's Omniverse) which they should lead given their logistics roots. -They insist to run like a startup (day 1) which makes a lot of obviously stupid projects be tried wasting billions instead of accepting it's day 2 and they're a mature behemoth like Tim Cook did at Apple. Good news is that Bezos is apparently back full time and he's focusing on AI. He's an actual freaking genius. Never understood why people think Elon is so smart when CEOs like Bezos, Dimon or Nadella run circles around his k-holed brain. Also EV/EBITDA chart looks like a floor has been reached so this could rebound really nicely quickly. Given that they are the incumbent in cloud it just feels like they have more to lose than to gain and I wouldn't like to have the engineers at Microsoft and Google breathing down my neck. Of course the pie can and probably will just grow for all three. There was just a little bit too much hair in the story for me but I do believe Amazon is a buy at these levels.

-

Added to Alphabet (4%>6%) and started a new position in Microsoft (0%>5%). I want to ride the trend of cloud providers. I don't find their Capex to be as crazy as everyone says when you compare them to the size of the company. They were just under-investing and milking the cow before and now they have a clear path to grow into something big and exciting so they go for it. Rational. Even if AI models end up commodified, serving them will require massive server capacity for LLM inference and for hosting the apps ecosystem built atop. Worse come the worse they decelerate and take a couple of years to grow into their infrastructure investments just like Amazon did when they went too big with their warehouses during COVID, not the end of the world. But that is not at all the scenario I believe into so I'm happy to bet against the bears here. The amount of brain power and talent at these companies we get to own for reasonable-ish valuations is extremely high so good things should keep happening albeit with potholes here and there. Wake me up with the bubble talks if they ever trade at PE 50+

-

Great thread idea! Thanks for starting it. Not the 50% down you're asking for but AirBnB and Universal Music are two wonderful companies that have IPOed 3-4 years ago at a high price and their stock has gone nowhere while business has grown. I own both. (much more excited about AirBnB, I wouldn't personally add to Universal at today's price)

-

If the AI bubble like the Internet, in what year are we now?

WayWardCloud replied to james22's topic in General Discussion

Why on Earth are we forbidding China to buy chips yet allowing Meta to release their models open source?? If this is such strategic tech protect it all the way! (real question, no expert) -

Supposedly, she's killing it!

-

I love that this has become an egg-centric thread

-

Are you investing in a tax free account Luke? Kudos for being able to revisit your thesis and change your mind but it sounds like an awful lot of movement recently so I'm curious. All world index fund and chill sounds great! I'm not sure whether China or the US will do better in the next decade or whether the market is fairly priced or if cheaper valuations are around the corner but I would suggest finding both a country allocation and an asset allocation that you can stick with long term, regardless of what your latest macro reads have convinced you of. Otherwise I worry you could be running the risk of jumping off one train when it's reached its maximum pessimism and onto another when it's reached its maximum optimism. Thanks for sharing your adventures!

-

Thanks Kab60 this is interesting! Figma is a tool for quickly designing the looks of an app or website (=UX/UI) before committing to the final version and asking a programmer to actually code the thing. Adobe's equivalent software was called "XD" but Figma being a cloud-based app it was usable straight from your browser and had a better real-time collaborative quality to it which made XD lose that battle. Adobe then attempted to buy Figma instead but the EU and UK regulators blocked the merger so they discontinued XD all together and moved on. The other main competing app for web design was called "Sketch" (not sure from what company made it) and they also closed down. So yes Figma came out of nowhere a few years ago and took over most of the UX/UI industry. The core of Adobe software suite is aimed at 1/photo editing : Photoshop, LightRoom 2/Video Editing : Premiere, After Effects, Audition 3/PDF editing : Acrobat (their original product) 4/Physical prints (books, magazines, billboards): Illustrator 5/Web design: XD (still exists but they stopped updating it), InDesign (for buttons and logos) So there is definitely an overlap on 5/ but that's only one of their many offerings. Maybe your friend specializes in selling web design tools only, do you know? Adobe doesn't break down which software is responsible for what percentage of their revenue (and most clients buy the whole suite anyway) but they have kept growing their revenue every single year while Figma took over UI/UX so it can't be that big of a slice of their portfolio. For perspective, Figma does 0.6B in revenue and Adobe 21B.

-

Happy to have put it on your radar! Looks like you're going to get a better entry point that I, too. I bought at $428. Hoping to get more at $380.

-

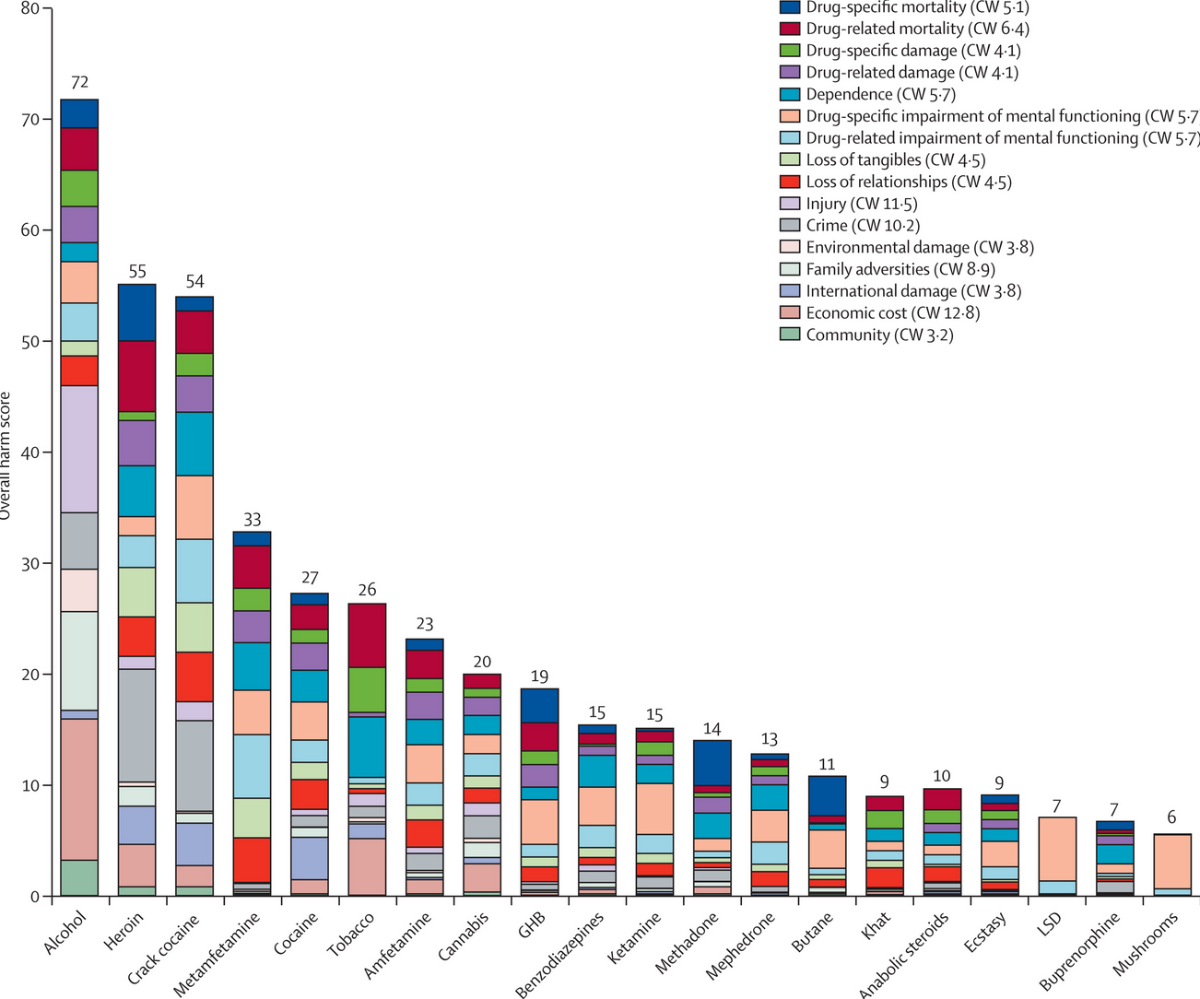

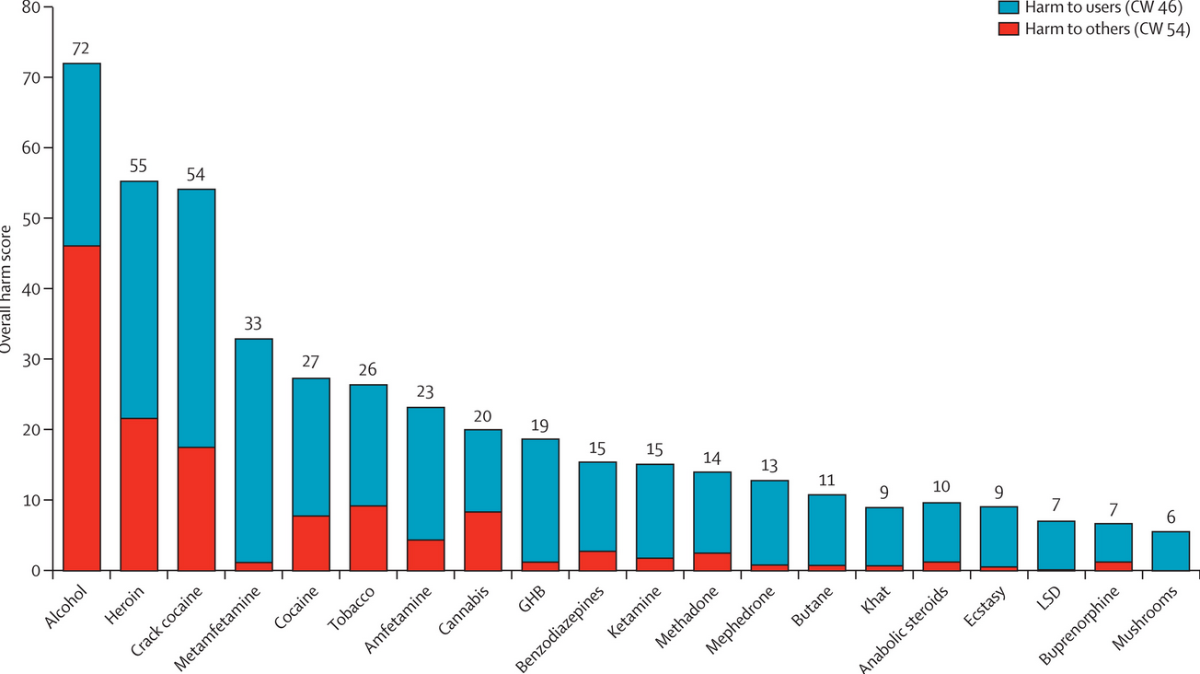

Here is the most thorough study on harm from drugs to self and to society I could find. It's unfortunately 15 years old but I doubt much has changed. I think you might just be more numb to the ravages of alcohol because it's been around for centuries in western culture, unlike cannabis. https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(10)61462-6/abstract

-

So definitely avoid Tesla (high PE, low margins), maybe avoid Amazon (low margins), and we're peachy I don't understand what the big fuss is about concentration and even less about cash as a % of market cap. Those are perhaps not cheap but reasonable valuations for some of the absolute best companies that have ever existed in the history of capitalism. The last drop came from tech and that was only 3 years ago I don't think the next one will come from there.

-

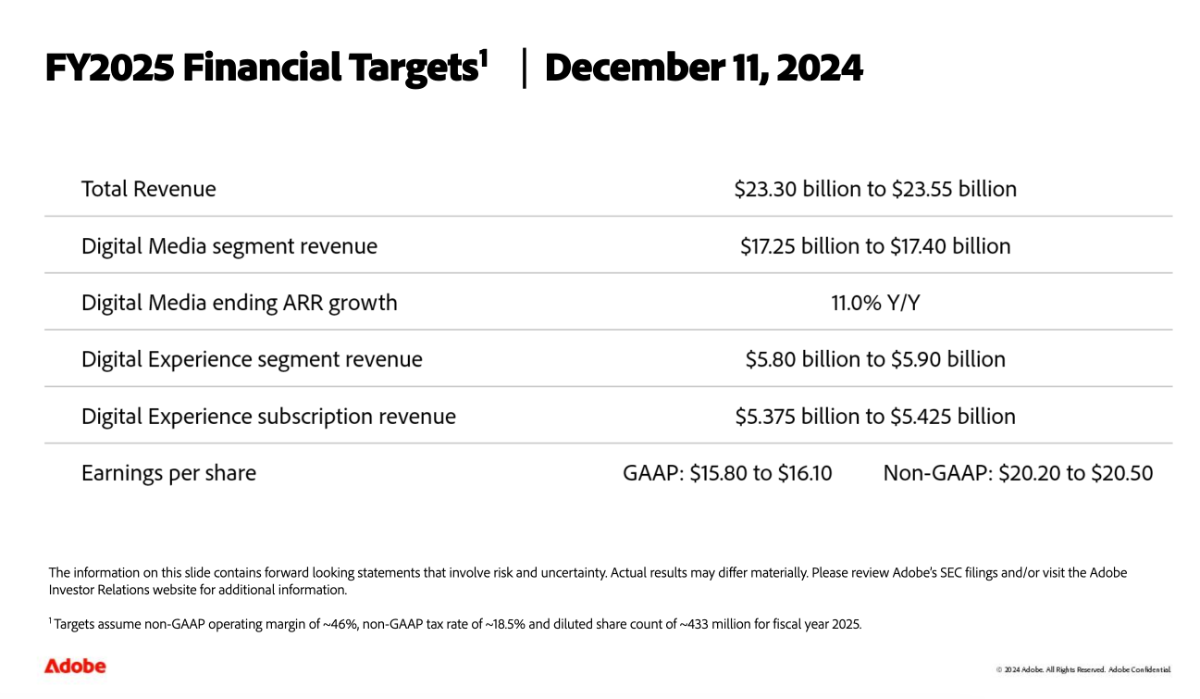

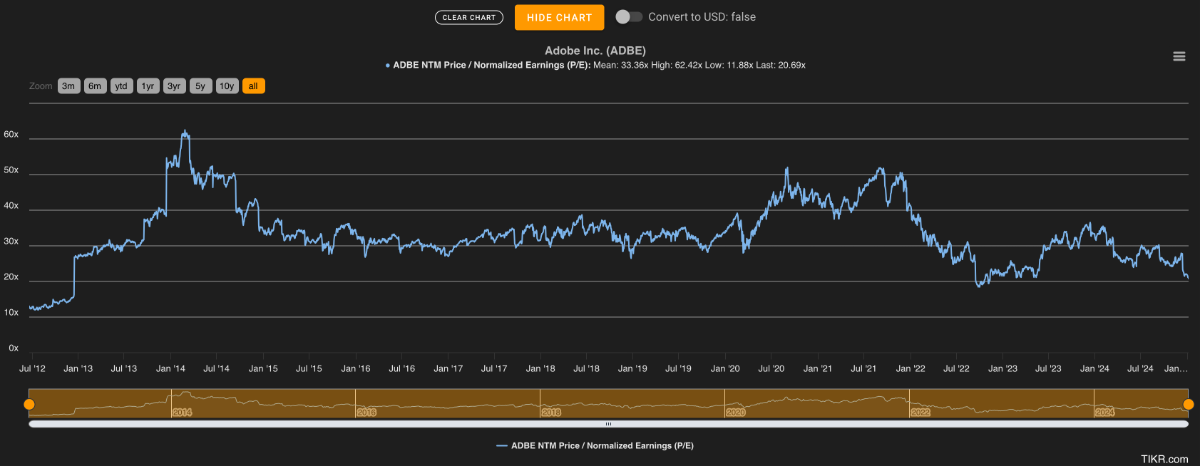

Should have mentioned forward PE, my bad! I find a 2025 GAAP PE of 26 and non-GAAP of 20.5. If you compare to previous years it really is much cheaper than it used to be except for the brief September 2022 dip which was a great time to buy.

-

Thanks for the color @Cod Liver Oil, this is why I LOVE this forum! Figma really is awesome and I wish they didn't back away from the merger, that does worry me a bit. I see Runway, Midjourney, Sora as great exciting new tools you plug into a bigger environment. If they stay superior to Firefly over the long run and at a low enough cost per generation to make a profit they may take a big slice of the new TAM of AI generated images that's being created. I don't see how this disrupts Adobe's legacy software too much just like I couldn't see how generative LLMs were disruptive to Google Search. It feels more adjacent than replacement and if anything it will create more content to touch up. But then again I'm not an AI head designer (that sounds really cool!)

-

For the past week I've been buying ADOBE. It went from trading at PEs in the mid-30s for a decade to a PE of 20 now over AI competition fears and subdued growth. I've been wanting to own this forever because Adobe Premiere is my main work tool in post production video. I don't care where the AI generated images are coming from (Adobe's in-house LLM called Firefly or one of the competitors such as Midjourney or Sora) I guarantee you it's going to be fed right back into Premiere if video and into Photoshop if photo. There are workflow pipelines involving many different artists at every company that nobody wants to risk changing and Adobe is the master at integrating them all seamlessly together. Video editing/visual effects/color correction/sound design/graphic design all have to integrate together and turnaround times for projects are often as short as 24 hours for social content. Adobe is much more than one cool app they're an integrated platform. When another company comes up with a cool shiny new tool (it happens all the time, especially in VFX), you feed the new tool's output back into your Adobe environment and then a year or two later Adobe releases an update and starts doing the same thing natively. This is what happened with speech-to-text for example. MANY really good automated transcription websites popped up all of a sudden when natural language recognition got much better and we would export entire podcasts to them, get a transcript and feed that data right back into Adobe. Now speech-to-text is a tool in the suite and I've never paid any of those sites ever again. They don't have to be first or best they just have to stay on top of what their users want and incrementally add those functions to their software following the kaizen method to keep us locked in, which they've been historically great at. I've missed the boat on investing in big AI winners (should have seen Nvidia coming) but I've been good at identifying what I call the mistake losers and I believe the AI bear case for Adobe is wrong here. This reminds me of how Alphabet initially traded down on AI fears even though they have the world's number one AI team. Adobe will incur increased capex yes but I am willing to bet they will emerge with an untouched or strengthened competitive position. You get to own a mature deeply entrenched high margins enterprise software company with predictable subscription revenues and a high pricing power (if they doubled their prices I can't imagine a single professional would switch), possibly at the dawn of a golden age in fully digitally created image/video content. FCF yield is around 5% and growth 10% with a chance of picking back up to 15%+ in 2026-7.

-

Thanks for your interest! How I reinvest will depend on where I see opportunities by the time I get the cash but if it were today I would simply buy more of VT (Vanguard All World Stocks) and VTC (Vanguard US Corporate Bonds). Probably something like 25% Bonds 75% Stocks. I'm not seeing anything super obvious so better simply sit in the index with a defensive-ish allocation (I usually don't have any bonds) and do something else with my time. I'm both French and American. As you accurately guessed both countries make their claims which makes paying taxes a bit complex. They have entered an agreement called FATCA (Foreign Account Tax Compliance Act) which is very one-sided: the US demands detailed information about every account their fiscal residents own in the whole world but gives absolutely no information back to the friendly foreign countries. This was my grandparents condo. In France, you have the possibility to bequeath a house when you're still alive by splitting the ownership between "nue propriété" (ownership of the walls) and "usufruit" (rights to enjoyment). You bequeath the former to your kids, or in this case grand-kids, but hang on to the later for the rest of your life. You pay a tax right away to do the split but less than what the estate tax would have been at the moment of death. My grand-parents did just that about 25 years ago when my brother and I were still kids so no estate tax was due. The downside is then my cost basis is considered at the time of the split, not of their passing, and since real estate went up a lot the initial bill was super high. However, there are gradual write-offs for each year of ownership until 30 years where profits are completely written off so any real estate sold after 30 years of ownership in France is tax free. Since we're at 25 already there isn't too much due (about 8% of the total value of the place). On the US side you do not have to pay federal inheritance tax when inheriting from a foreign parent so that's taken care of. When it comes to taxing the profits however the IRS doesn't recognize any of this "nue propriété" / "usufruit" split thing. In their eyes the date of effective inheritance and thus the cost basis is the death of the parent, so that's much more recent. For the past three years real estate in Paris has trended slightly down so no profits no taxes. Fun fact: if it did go up in price but the Euro/Dollar went down I would not have been able to claim a loss in my investment due to FX. Exchange rates are not taken into account when calculating the tax basis. Fun fact 2:You cannot defer capital gains tax on the sale of the property by reinvesting the proceeds into a US one because foreign real estate is not considered "like-kind property".

-

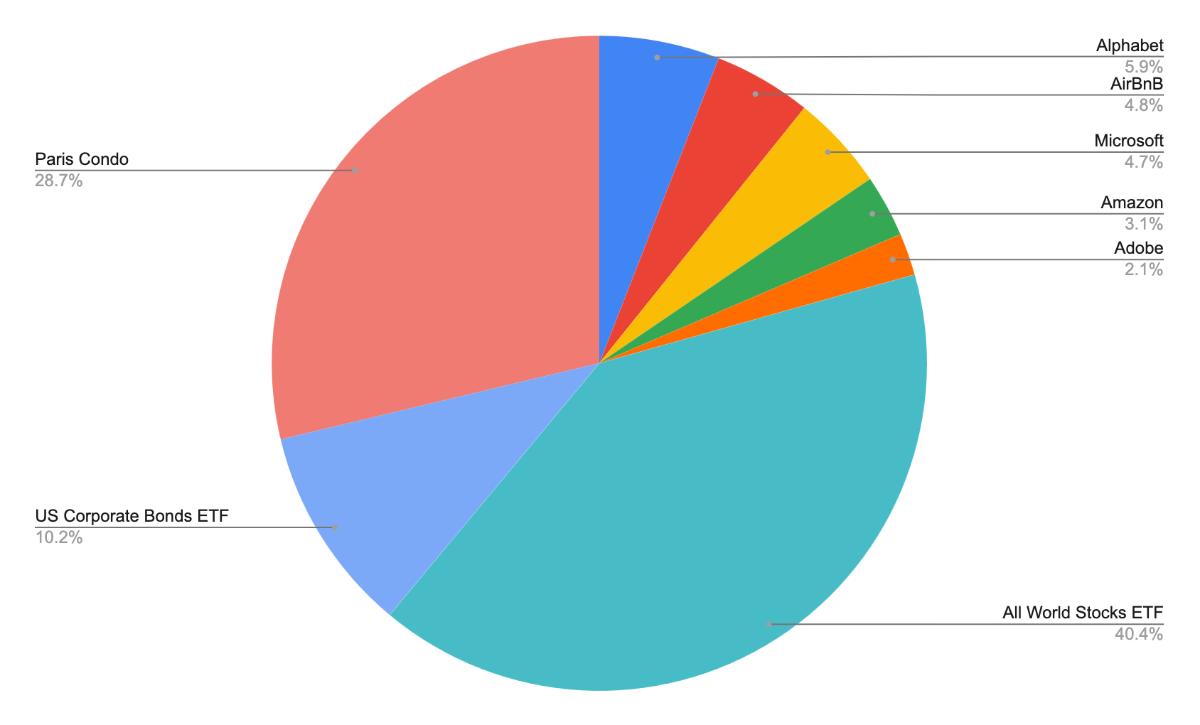

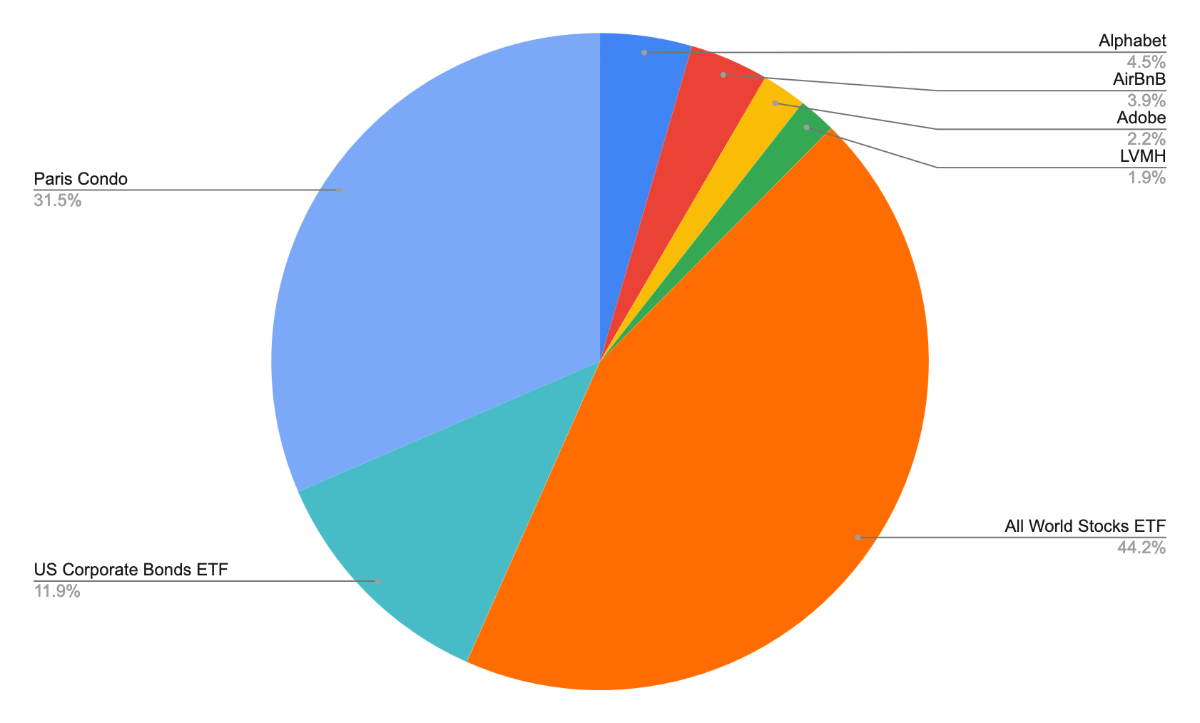

This is 95% of my net worth. Mostly in taxable unfortunately. The Real Estate is going to be sold within 12 months.

-

Got some more AirBnB Also finally decided to pay for a yearly subscription to tikr.com terminal, they're having a 20% off winter discount and they're my go to for quickly checking numbers on new ideas.

-

I went through 2024 almost entirely in passive index funds with the exception of owning GOOGL. Recently I've added AirBnB as well as a sliver of LVMH. Good luck everyone and thanks for sharing your thoughts!

-

Great topic! Thanks for starting it. I'm thinking companies like Appian which provides custom made software for government agencies so they can operate with less staff.

-

Yep. Georgia as well. So much for the theory Putin would stop at Ukraine.

-

Thanks for sharing, it sounds interesting! Have you heard of Recursion (RxRx)? They use robotics to systematically experiment with biology and they plan to sell this data library to big AI models to forage through. The goals is to accelerate pharma research by being able to predict more interactions in software. 2B market cap 500 employees.

-

Joint Sword-2024B is already over