Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Well i lightened up on my Fairfax position today. Why? 1.) i was way, way overweight. Especially given the recent run-up. My strategy with Fairfax is to have a core position i hold as long as the story remains intact (the Fairfax story is actually getting better). I trade around that core holding - buy more when the stock sells of (like last Sept/Oct) and lighten up when the stock pops (like now). This strategy has worked exceptionally well since Fairfax hit its pandemic lows in Oct 2020. 2.) tax reasons. My wife and i do not have day jobs. Selling Fairfax in our taxable accounts realizes some pretty big capital gains (we were up 35% on those positions) that we will pay minimal tax on (given it will be our only income for the year). In Canada capital gains receive very favourable tax treatment. Fairfax remains a little over 30% of my total portfolio - so i am still way overweight. Oil is about 30% (mostly SU). Cash is up to 35%. Misc is 5% (US financials and Fairfax India). I recently sold my big tech and dividend stocks for 6-8% gains (over 6 weeks). My total portfolio is up about 8% to start the year so i am happy to lock in gains and raise some cash (that will earn +3%) while i wait for the next fat pitch.

-

@Xerxes i am not following your logic…

-

@StubbleJumper, i agree it is important to keep a level head. Point taken. i think the challenge when trying to value Fairfax is the numbers from the past 3 years really don’t help us much when trying to determine what an appropriate price for the stock should be today. So we are kind of in uncharted territory. I will not be surprised if the stock continues to move higher. I also will not be surprised if the stock goes back to US$500. This will make it difficult for current shareholders who are not in the stock for the long term (or who are way overweight like me). ————— My guess is BV Dec 31, 2022 will come in at about $635-$640/share. Pet insurance will deliver $40/share after tax all by itself. Another $30/share seems reasonable for underwriting profit, interest and div income, share of profit of associates and investment gains (market to market equities were up +$300 million in Q4). So looks to me like stock is currently trading at about 1xBV. My guess is Fairfax will earn about $105/share in 2023. That would put BV at $740 Dec 31, 2023. My $105 is already looking low. Why? 1.) Ambridge was sold for $400 million and will likely involved a sizable gain ($10/share after tax?). 2.) Equity markets are starting the year strong ( - example: 1.95 million Fairfax shares x $150/share gain over 2023 = $300 million pre-tax gain). - example: earnings at Eurobank are really starting to move. The stock is popping (i realize it is not mark to market). Perhaps they are allowed to start a dividend in 2023. 3.) Bond yields have really come down a little further out on the curve (3 years and further out) so we likely will see decent gains on the bond portfolio in 2023. 4.) Fairfax has been supporting/cultivating a large number of private holdings that it could chose to monetize: Exco, AGT, Bauer, etc. it has a large number of ‘hidden’ assets. My guess is we get a couple of more monetizations in 2023. 5.) Digit IPO: this will be a big deal when it happens. We know Digit has the approvals. We just don’t know the timing. Lots of buzz about India right now… 6.) share buybacks: do they go big again? I think its pretty safe to assume share count is coming down minimum of 2% but it could easily be higher. So based on what i know today, i think Fairfax should earn about $105/share in 2023. That is my conservative number. If a few of the things i note above happen, earnings will likely be higher. If we get the Digit IPO, earnings could easily be much higher (+$130/share). ————— Earnings are very important. Equally important for an undervalued stock like Fairfax is what happens to the multiple. Why is 1x BV the appropriate number? That is comically low for a company like Fairfax - as it exists today. Fairfax should be able to deliver ROE of over 15% for at least the next few years. Does a 1.3 or even a 1.4 multiple not make sense? Over time Mr Market does get valuation right. If BV is US$635 (at Dec 31) x multiple of 1.3 = $825/share. If Fairfax earns $105/share in 2023, it the stock was trading at $825 = forward PE of 8x. Hardly expensive. So to me, the stock today trading at $640 looks crazy cheap. When will Mr Market agree with me? No idea. But it does look to me like the Fairfax pendulum is slowly swinging from fear to neutral. If Fairfax can deliver the good in 2023 and 2024 (like they have the last couple of years) i think there is a good chance the pendulum swings to greed - and we see the multiple go to the higher end of the band.

-

Sanjeev, can you please add the rocket emoji to the toolbar? Fairfax closed today at $640. $10 dividend is being deposited tomorrow (=$650) Stock was trading at $450 in early October = 45% return in 3 months. Time to sell? Stock is trading at 1x BV. And about 6x 2023 earnings. That hardly looks expensive. It actually looks dirt cheap. What a bizarre set up.

-

The property cat market and reinsurance is something to watch moving forward. Fairfax has a significant reinsurance business so it will be interesting to learn what sort of rate increases they have been getting. ————— Here is what Brown and Brown Insurance had to say on their Q4 call this morning: “From an insurance standpoint, certain markets have been and remain in significant turmoil. Pricing for CAT property both commercial and residential was under pressure through the third quarter. Then Ian slammed into Florida. This caused 1/1 reinsurance treaties to be bound at higher attachment points and materially higher rates. As a result, we saw incremental price increases and lower limits being offered for placements in late Q4 of last year and early this year. The placement of CAT property in Q4 last year and January of this year with some of the most difficult placements we've experienced in decades with rates increasing 20% to 40% or more. However, properties of lesser construction quality or that have experienced losses could be much higher and I mean much higher than this range. As a result, we had customers unable to buy or afford full limits and therefore ended up increasing their deductibles or purchasing loss limit in order to manage our cost of insurance. In certain cases, this was not possible as lending institutions or condo associations would not allow lower limits or significantly higher deductibles. Admitted market rate increases were similar to prior quarters and were up 3% to 7% across most lines with the outlier being workers' compensation rates which remained down 1% to 3%. The placement of professional liability and excess liability remain competitive with rates down 5% to up 5%, with public company D&O rates down 5% to down 20% or more. Regarding cyber, the story is similar to the last few quarters with rates and deductibles continuing to increase but we did see some slight moderation during the quarter.” ————— Question: Greg Peters …So, when I think about '23, …how will those variables -- like the June first renewals on property CAT…, how will that affect your organic results for this year -- this upcoming year? Answer: Powell Brown …As it relates to the CAT property pricing, the variable there, Greg, as you know is not as much our -- I mean, it is there are certain limitations on ability to present limits in some instances. But it's more of -- in my opinion, it's more of an affordability issue. And so, if you think about if you've been giving rate increases, let's just say to yourself on your own personal lines homeowners, if you've got an increase of let's say 10% a year for four or five years in a row and then all of a sudden we came on the fifth year and gave you a 25% increase, there is a -- the buyers are tiring of that. And so, having said that, availability of capacity in this market is unlike anything I've ever seen, I've only been in the insurance industry for 33 years now. So, there's a lot more to go, but I've not ever seen anything like this and we will continue to provide solutions to our customers. But sometimes the example I think we used last time and I would use it again is, if you have an entity, and they're paying $800,000 for their property and the renewal is a $1.8 million, and they say, what can we buy for $1 million, which can't buy anymore insurance, we can't afford it. So, we're seeing that more and more, Greg. So, the CAT pricing that is going to -- is it more of a wildcard. The other thing that we're seeing is in the CAT capacity and accessing it in some instances, there is commission pressure downward on some of those placements now. So, a lot of people just think, well, as the rate goes up X, then you're going to -- your commission goes up X if you're on commission as opposed to a fee and that is true sometimes, but in this case, they might cut your commission one or two points, and so we're seeing that as well. So that's a harder one to answer, Greg.

-

Sanjeev, i am happy to throw my thoughts about Fairfax against the wall to see what sticks. Other posters add a great deal of value (most of which i steal for my next update). We are all slowly learning just how 1.) undervalued Fairfax got back in 2020. 2.) well positioned the company is for the current environment (extended hard market, rising interest rates and outperformance of value/cyclical equites). 3.) well the management team at Fairfax is executing. We are in that Peter Lynch stage today where the story is continually getting materially better. So even though the stock has been going up a lot it remains cheap. ————— Regarding attending the Fairfax AGM, yes, i plan on attending this year (no overlap with family vacation this year). I look forward to meeting other board members who are able to make it.

-

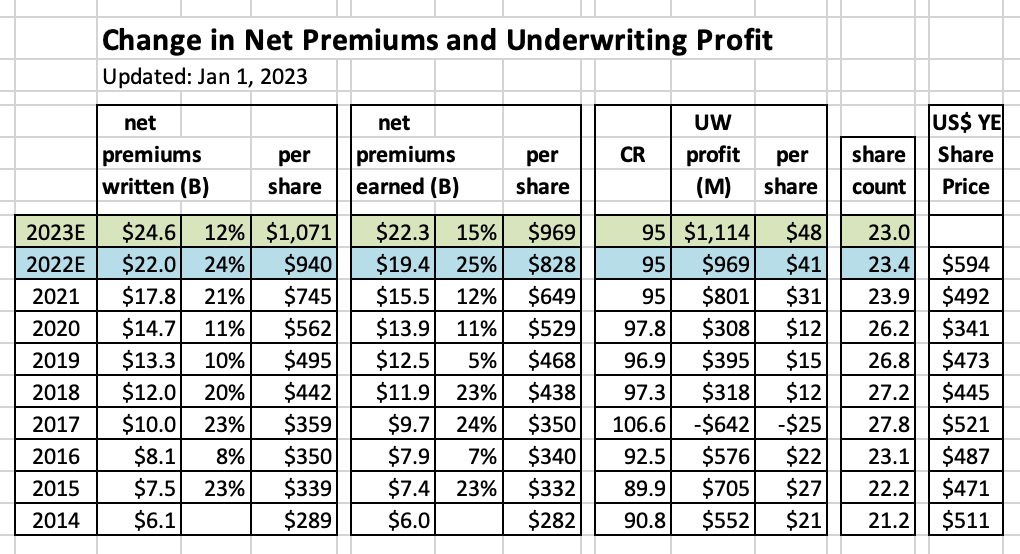

P&C insurance earnings started today with Travelers. Sounds like the hard market in insurance is continuing into 2023 with no signs of a slowdown. WR Berkley reports after close on Thursday; we should have a good handle on trends after they report. What does this mean for Fairfax? We should see strong top line growth again in Q4 (20%?). And with an exceptionally hard market in reinsurance, perhaps Fairfax can deliver another year of 20% top line growth in 2023. If they can do this, that would put net written premiums at around $26.5 billion in 2023, which would be double what they were in 2019 ($13.3 billion). That would be amazing. The Fairfax story just keeps getting better… ————— Alan Schnitzer - Travelers Chairman and Chief Executive Officer on Q4 conference call: “And let me spend just a second on the pricing environment because that seemed like it was part of your question, and I’ve seen a number of you write about it this morning. So I think it’s hard to characterize this pricing environment as anything other than very strong. At 10.1% that RPC is spot on an eight-quarter average. So incredibly stable and near record levels. Small movements between pure rate and exposure, but I would emphasize small movements between rate and exposure. The breadth of the pricing gains across our book is very strong and very consistent. I don’t think you can assess the pricing environment without looking at retention and given where that is literally record levels and given the profitability very strong. The pricing gains that we achieved were broad-based, led by property, auto, umbrella and CMP. And then you take all that against the margins that we printed and we just – we feel fantastic about the pricing and the overall execution this year. And again, we’re going to go out and do it again in ‘23.

-

I estimated Fairfax's equity portfolio increased about $1 billion in Q4. Of the total, about $380 million was mark to market (about $17/share pre-tax). My numbers are usually decent directional guides. Given the hot start in equity markets in January, I thought it would be interesting to see how Fairfax's portfolio is doing YTD in Q1. My spreadsheet estimates Fairfax's portfolio is up about $640 million so far in Q1. About $225 million is mark to market ($10/share). Not too shabby. Big movers: 1.) Eurobank +$212 million 2.) Fairfax India +$134 3.) Stelco +$75 4.) Blackberry +$47 5.) FFH TRS +$43 6.) Micron +$41 Fairfax Equity Holdings Jan 23 2022.xlsx

-

@StevieV yes, that was a typo on my part. Meant 2024. I edited my post. Thanks for catching my error.

-

Fairfax is trading at about US$600 today. Fairfax getting to a share price of US$1,000 anytime sounds like a cruel joke. Right? Actually, i think there is a fairly credible path for Fairfax to get to $1,000 in about 24 months. Assumptions: 1.) CR = 95 or lower for 2023 & 2024 2.) return on investment portfolio of 6.2% for 2023 & 2024 3.) Mr. Market valuing shares at multiple of 1.2 x BV in Jan 2025 I don’t think these are heroic assumptions. A successful Digit IPO would likely accelerate the time line. A material share buyback would also accelerate the time line. Of my three assumptions above, i am least confident in 3.) and the multiple Mr Market attaches to Fairfax. Sentiment in Fairfax is improving. And if Fairfax is able to deliver back to back years of ROE of 16% that should push the P/BV multiple higher. (Alternatively, if Fairfax generates slightly higher earnings than my estimates over the next 2 years, they could get to $1,000 share price with a 1.1 x multiple.) Bottom line, it will be interesting to see what happens. I am focussed on Fairfax and their results (and execution). Strong earnings will translate into a higher stock price. Multiple expansion will be gravy. ————— Well, lets do some basic math… - Sept 30, 2022 BV = $570 - Dec 31, 2022 BV = $635 (my estimate) - 2023 estimated earnings = $105/share - Dec 31, 2023 BV = $740 - 1.1 x BV = $810 - 1.2 x BV = $890 - 2024 estimated earnings = $115/share - Dec 31, 2024 BV = $855/share - 1.1 x BV = $945 - 1.2 x BV = $1,026

-

@StubbleJumper thanks for the insight. Makes a lot of sense. Lets keep our fingers crossed that the hard market keeps rolling…

-

@StubbleJumper thanks for the comments. So is it the 95CR or 6.2% return on the investment portfolio that you think is inflated (on a normalized basis). Or is it that the $22 billion in net written premiums or $51 billion investment portfolio that is inflated? Or some combination of the two? I understand the hard market has to end at some point. For a number of reasons it looks like it will continue to power on in 2023 (we will know much more in another week or two as insurance companies start reporting). The investment side of the ledger looks very favourable for Fairfax looking forward. The size of the investment portfolio is growing. Interest income is growing. And fall in interest rates will likely result in sizable gains in the bond portfolio. Much of Fairfax’s stock portfolio has been marked down so we should see nice gains in equities moving forward. Yes, i am ‘leaning out’ with my estimates. The hard market could quickly pivot to a soft market in 2023. And we could see another leg down in the current bear market for stocks. And interest rates across the curve could shoot higher. These events would likely drive Fairfax’s stock lower. So, we will see…

-

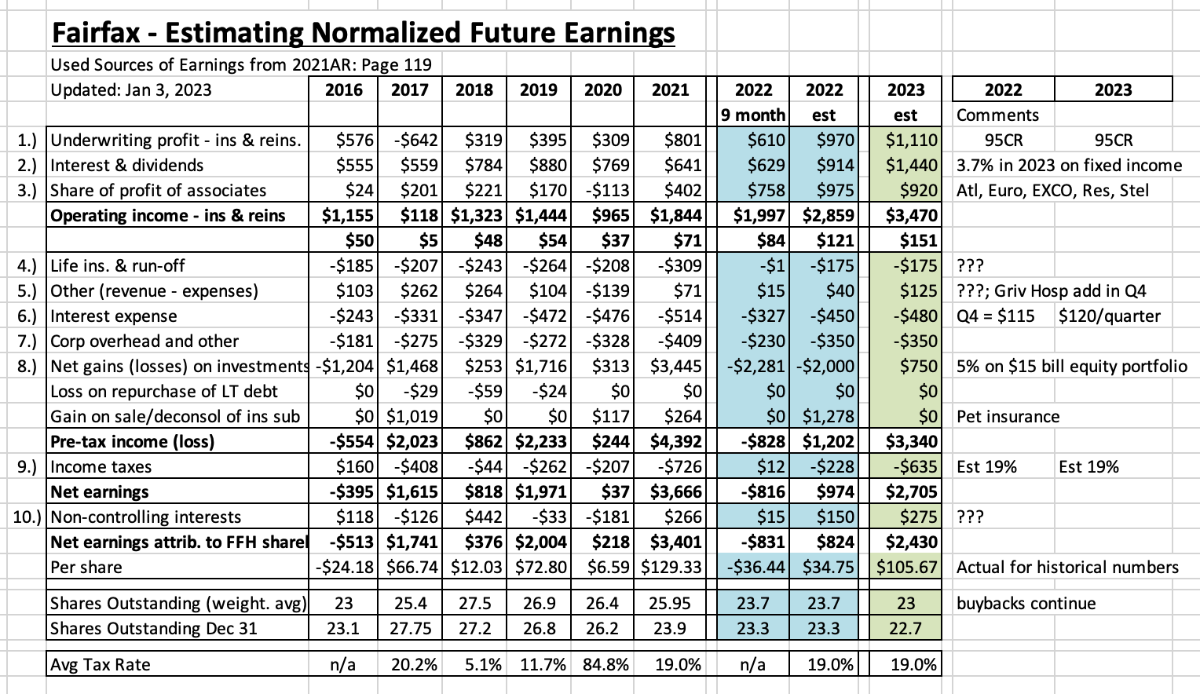

Two key inputs used to value Fairfax is combined ratio and return on its investment portfolio. My current estimate is for Fairfax to earn about $105/share in 2023 (what i call ‘normalized’ earnings). Sept 30, 2022 BV is $570. $105/share in annual earnings would put Fairfax’s ROE in the high teens. $105/share in earnings assumes a 95 CR and a 6.2% return on Fairfax’s investment portfolio. Neither estimate is aggressive, in my mind. Why? 1.) The hard market in insurance is in its 4th year and is expanding to reinsurance. The top line is growing at 20% (yes, this will slow). The hard market should impact underwriting profitability (in a positive way) over time. From 2013-2016, Fairfax generated an average CR of 91 (it has happened in the recent past). I think it is likely that Fairfax’s CR improves from here. Every 1 point improvement on the CR = $220 million increase in underwriting profit. 2.) A 6.2% return on its investment portfolio moving forward is not aggressive. In fact, it is probably conservative. Why? Interest rates have moved much higher over the past year. And we have just had a bear market in equities so of Fairfax’s equity holdings have been market down. Fairfax also was an aggressive buyer of equities in 2022 at very attractive prices… which bodes well for future returns. What does a 6.2% return on the investment portfolio look like? - interest income of $1.34 billion = 3.7% yield on $36 billion fixed income portfolio - equity return of $1.845 billion = 11.5% on $15 billion equity portfolio - equity return = dividends ($100) + share of profit of assoc ($920) + other ($125) + net gains ($700) If Fairfax is able to achieve a 7% return on its investment portfolio (0.8% increase fro my estimates of 6.2%) = $400 million increase in pre-tax earnings. 3.) Fairfax wild cards. We already know Ambridge is being sold for $400 million in 1H 2023, and likely for a significant gain. What else is coming? If we get a Digit IPO in 2023 then my guess is we could easily see Fairfax book a $1 billion gain. That is not part of my $105/share earnings estimate. Fairfax has lots of other levers it could pull in 2023 to surface more hidden value on its balance sheet. 4.) Share buybacks are another wild card. Fairfax will likely be generating record operating earnings in 2023. If they wanted, Fairfax could take out 1.2 million shares (5% of total) = $780 million (avg cost of $650/share). Conclusion: i think my earnings estimate of $105/share for 2023 is not aggressive. But earnings of $105/share suggests Fairfax is capable of earnings high teens ROE moving forward (17 to 18% ish). Shares are trading at $600. My guess is BV will be around $630-$640 at Dec 31. So investors today are able to buy for 0.95 x BV a well run insurance company that is poised to generate high teens ROE in the coming years. ————- Common shareholders equity at Sept 30, 2022 = $13.36 billion. Common shares effectively outstanding Sept 30, 2022 = 23.4 million BV/share = $569.97

-

Yesterday, I read Morningstar’s summary of their report for Fairfax. I thought what they wrote was pretty accurate. Just reading the Morningstar summary, an investor would be stupid to buy a share of Fairfax. So why am I so bullish on Fairfax? Because I am focussed on the present and the future. Graham (the guy who taught Buffett) teaches us a stock is simply worth the present value of its future cash flows. Yes, the past matters... but what matters much more is the future. The Morningstar report is focussed pretty much solely on the past. And this is generally ok for most companies. But it does not work for companies where things have changed. Turnarounds. And lots of important things have changed at Fairfax over the past few years. Things that will have a big, positive impact on earnings in 2023 and future years. This explains, at least partially, why it takes turnaround type stocks like Fairfax so long to re-rate. It takes years of excellent results before analysts and investors get comfortable that things have indeed changed in a sustainable way for the better. Only after the new and improved financial results are embedded in historical results will the ‘narrative’ change. This actually makes sense for a company like Fairfax that was so out of favour. ————— So what is Morningstar missing in their report? 1.) Growth in net premiums written: this has grown at Fairfax over the past 8 years from $6 billion (2014) to estimated $22 billion (2022) for compounded growth of 17% per year. That is pretty impressive. 2.) Underwriting: While Fairfax did post a poor average CR of just under 100 over the 4 years from 2017-2020, over the past 9 years the average CR is 95.7. Importantly, the CR in 2021 was 95 and 2022 is estimated to come in around 95 as well. I would not call underwriting at a CR of 95 ‘relatively poor’ as Morningstar does. 3.) Increase in interest rates, how Fairfax was positioned, and the impact on interest income in 2022 and the future: Fairfax has a fixed income portfolio of $36 billion; as the insurance business has grown over the past 8 years so has the fixed income portfolio. As those of us on the board know, Fairfax took the average duration of their bond portfolio to 1.2 years at Dec 31, 2021. This caused interest income to fall dramatically in 2021. Who cares? Well, for those not paying attention, interest rates have spiked higher and this is… drum roll please… resulting in spiking interest income. As a result, Fairfax is poised to deliver record underwriting profit ($1.1 billion) and record interest and dividend income ($1.4 billion) in 2023. $2.5 billion / 23.4 million shares = US$107/share. Current stock price is US$600. They should earn even more in 2024. The positioning of the duration of bond portfolio was an example of a ‘bold bet’ that is paying off exceptionally well for shareholders (driving billions in future value). 4.) ‘Watsa’s ability to produce alpha on the investment side’: Fairfax IS delivering alpha. - share of profit of associates: will come in at a record $975 million in 2022 and $920 million in 2023 and future years. - asset monetizations: pet insurance was just sold for close to $1 billion after tax gain. Resolute Forest Products was sold for $623 million (plus $183 million CVR). Ambridge Partners was just sold for $400 million. Conclusion: Fairfax, as it exists today, is misunderstood. Most analysts and investors are stuck in the past. The good news is a stock is worth the present value of its future cash flows. And that is true for Fairfax. So what is an investor to do? Patience and time. Fairfax needs to deliver results. The narrative will slowly change and reflect the current reality. And Fairfax shareholders should be rewarded handsomely. —————- Morningstar: While Its Primary Business Is Insurance, Fairfax Is in Some Ways More of an Investment Fund “While its primary business is insurance, Fairfax is in some ways more of an investment fund. Chairman and CEO Prem Watsa has a history of bold investment bets and has shown a willingness to be unorthodox when it comes to portfolio construction. As a result, compared with other insurers, the company's results tend to be driven more by results on the investment side. We're somewhat skeptical of this approach, as we believe disciplined underwriting is a more maintainable path to long-term value creation, and Fairfax's underwriting record is relatively poor. Fairfax collected a multibillion-dollar windfall during the financial crisis thanks to some large bearish bets but then remained cautious for many years afterward, resulting in weak overall results despite a significant improvement in underwriting performance over time. We think Fairfax's performance will continue to hinge on whether Watsa's investment theses play out, and the company has pivoted on this front. Due to his bearish view, Watsa had fully hedged the company's still substantial equity portfolio in the post-crisis years. However, following the U.S. election of Donald Trump as president, Watsa did an about-face and banked on a strong equity market. Watsa’s optimism has largely worked to the company's advantage in recent years, but it has come with some volatility and the company essentially locked in the poor book value growth it had experienced through 2016. As the market turned in 2020, Fairfax went though a period of volatility but finished the year with a modest reduction in book value per share. During 2021, the company's bullish stance was a positive, before becoming a drag again in 2022. We think investors attracted to the stock due to a belief in Watsa’s ability to produce alpha on the investment side should consider his record over the past decade, which includes some big wins but also substantial losses and missed opportunities. Fairfax has seen a lot of ups and downs, but since Watsa took control in the mid-'80s, its performance has been trending toward mediocrity. In the near term, however, strong industry pricing should be a material tailwind for Fairfax and its peers.

-

Great up-to-date summary of why commodities are in a secular bull market. John Polomny is very well spoken (and now part of YouTube channel listings).

-

“After spending many years in Wall Street and after making and losing millions of dollars I want to tell you this: It never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I've known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine that is, they made no real money out of it. Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money. It is literally true that millions come easier to a trader after he knows how to trade than hundreds did in the days of his ignorance.” ― Edwin Lefèvre, Reminiscences of a Stock Operator ————— Fairfax India was trading at $9.50 Oct 31. Everyone KNEW it was wicked cheap. The only thing we didn’t know back then is the timing of when the stock would move higher. So here we are 10 weeks later and the stock is now trading 50% higher at $14.50. Who coulda known? Well, we all knew. Everyone on this board should have made out like a bandit with Fairfax India. It was a gift. All an investor had to do to make big money was buy (it was unambiguously crazy cheap) and SIT TIGHT. Fairfax India, at $14.50 is still cheap: trading well below BV. Prospects for India have rarely looked better. ————— What caused the move? probably a couple of things happening at the same time: 1.) excellent executions by the management team at Fairfax India 2.) opportunistic buybacks by Fairfax India: management team at Fairfax India monetized some assets over the past 18 months, locking in gains and raising cash 3.) investor sentiment towards India is improving. US$ weakness. Emerging market strength. 4.) halo effect from Fairfax: sentiment in Fairfax is improving and this will improve sentiment towards Fairfax India. Investors no longer hate Fairfax. Probably at neutral. Probably love in another year. ————— Recipe was another good example of the exact same thing when it traded around C$12 in 2022. Wicked cheap. Fairfax saw the gift and took it private at $20.73/share, which was probably a steal. Good for them. Everyone on this board KNEW Recipe was dirt cheap at under $12. What we didn’t know was the timing of the spike higher. Again, all an investor had to do to make big money was buy it and SIT TIGHT. ————— Fairfax is a great current example. Stock is trading at US$600. BV Dec 31, 2022, could be around $640. 1.2 x BV = stock price of $768; suggests 28% upside to stock price. Looking out 1 year BV could be around $730. 1.2 x BV = stock price of $875; suggests 45% upside to stock price from where it is trading today. 12 months is not that far away. At some point in time, stocks that are dirt cheap eventually move to fair value. Often they actually move from undervalued all the way to overvalued. Why? Does it matter? The important thing is to be right with your analysis. Scale your position size appropriately. And then sit tight. i have made a bunch of money trading in and out of Fairfax the past couple of years. I have been lucky. Because a big move is coming. Moving forward my plan is to try and sit tight. Because that is how the big money is made.

-

January IEA oil report: rising global demand, slowing supply. Pretty bullish set up. https://www.iea.org/reports/oil-market-report-january-2023 - Global oil demand is set to rise by 1.9 mb/d in 2023, to a record 101.7 mb/d, with nearly half the gain from China following the lifting of its Covid restrictions. Jet fuel remains the largest source of growth, up 840 kb/d. OECD oil demand slumped by 900 kb/d in 4Q22 as weak industrial activity and weather effects lowered use, while non-OECD demand was 500 kb/d higher. - World oil supply growth in 2023 is set to slow to 1 mb/d following last year’s OPEC+ led growth of 4.7 mb/d. An overall non-OPEC+ rise of 1.9 mb/d will be tempered by an OPEC+ drop of 870 kb/d due to expected declines in Russia. The US ranks as the world’s leading source of supply growth and, along with Canada, Brazil and Guyana, hits an annual production record for a second straight year.

-

@SafetyinNumbers Zero interest rates impacted Fairfax more than peers over the past couple of years. That is because Fairfax has well below average duration (when compared to peers) on their bond portfolio. They were a freakish 1.2 years average duration at Dec 31, 2021. This means interest income was low and falling pretty dramatically the past couple of years. In short, Fairfax dramatically under-earned in interest income when compared to peers (and adjusting for size of portfolio) over the past couple of years. However, this is quickly reversing. And if interest rates stay higher for longer (allowing Fairfax to reinvest most of its low duration portfolio at much higher rates) then Fairfax could catch and pass some peers (in terms of total portfolio yield) in 2023. The ‘run rate’ for interest and dividend income was $950 million at Q2 and $1.2 billion in Q3. It will be very interesting to see what run rate they report for Q4. If Fairfax is able to get the interest yield on their $36 billion bond portfolio to something around 4% = $1.44 billion in interest income, then i think analysts and investors will start to drink the Fairfax Kool-Aid again. That would be US$60/share in just interest income. Nuts for a $600 stock.

-

It is encouraging to see the pop in Fairfax India’s stock price the past couple of months. I wonder if Fairfax India has been active on the share buyback front. We will find out when they report Q4. 2023 should be an interesting year. I wonder if we see an Anchorage IPO at some point. Fairfax India has been monetizing some assets the past couple of years, most recently 9.8% of IIFL Wealth. Fairfax’s ownership of Fairfax India is up to 42%. Is there a maximum it can go to? Or can Fairfax just keep increasing its stake each year? ————— I expect Fairfax to be active in India in 2023. Fairfax India is their preferred vehicle to grow in India. The problem is how do you put a significant chunk of new money into Fairfax India? You can’t raise it in the public markets (with such a low share price). Perhaps Fairfax will begin investing directly again in new opportunities in India. Perhaps with partners like OMERS etc if the transactions are large. ————— June 2022: “Billionaire investor Prem Watsa proposes to have $7 billion more worth of investments in India over the next five years where he believes the country is in an "impressive" phase with the goal of 10% economic growth in front of it.” - https://economictimes.indiatimes.com/markets/stocks/news/watsa-plans-to-invest-7-billion-more/articleshow/92026294.cms?from=mdr

-

@gfp thanks for posting. Nice to see Fairfax getting some well served press. What I really liked about the article: 1.) it provides a concise, easy to understand history of Fairfax and bridges nicely to where the company is at today. This is not easy to do with Fairfax. 2.) identifies Fairfax as a GROWTH company. On this board we have done a good job of highlighting how cheap Fairfax is - looking at PE (about 6 x 2023 estimated normalized earnings) or P/BV (about 0.95 x Dec 31, 2022 estimated BV). Fairfax has grown like crazy. Over 9 years (2014-2023), a very long time, it has compounded net premiums at an incredible rate of 16% per year. Net premiums are up 300% over the past 9 years - from $6.1 billion to $24.6 billion in 2023 (my estimate). ---------- And growth is one of the critical inputs in determining an appropriate P/BV multiple for insurance companies. The really interesting things with Fairfax is the growth of 16% per year HAS ALREADY HAPPENED. But it is not yet priced into the stock price. That is a great set up for current shareholders. Multiple expansion will come... Mr. Market will eventually figure it out. And growing earnings + multiple expansion + lower share count = exceptional returns for investors.

-

@StubbleJumper capital allocation will be super interesting to watch with Fairfax in 2023. Driven by hard market (20% top line growth), much higher interest rates (spiking interest income) and continued asset monetizations, Fairfax looks like it is in a multi-year period where it will have $2 to $3 billion to allocate each and every year. Asset monetizations late in 2022: proceeds of $1.4 billion pet insurance sale (Oct). Fairfax India also closed on ICICI Wealth sale late last year. Asset monetizations 1H2023: Resolute sale ($600 million) and Ambridge ($400 million) set to close in 1H 2023 What will Fairfax do with all the cash they are generating? Capital allocation options: 1.) strong financial position - top priority. Cash at hold co was US$800 million at the end of Q3, well below $1 billion minimum target. Makes sense to me Fairfax will want to get this to $1.1 billion = $300 million 2.) dividend: at US$10 paid in late January = $234 million 3.) grow insurance in hard market: Fairfax has said repeatedly this is a top pick. It appears the hard market is continuing into 2023. Most insurance subs look well capitalized to fund growth on their own; perhaps C&F (keep some proceeds from pet insurance sale) and Brit get top ups. 4.) Runoff: might need a top up of $200 million or so. Lots of long tail stuff (impact of inflation?)… we will know much more when Fairfax reports Q4 (and they have completed their actuarial review). The top 4 items are pretty straight forward. Deciding what to do among the remaining options is where things get really interesting. The weightings are what i wonder about. 5.) Mergers and acquisitions: other than bolt on purchases (like Singapore Re in 2021), Fairfax has said repeatedly that they are done with big insurance purchases. They are happy with their global footprint. Fairfax actually has been a seller (at attractive prices): runoff in 2021, pet insurance in 2022 and Ambridge so far in 2023. 6.) FFH stock buybacks: it is a given Fairfax will buy back stock in 2023. I think a stock buyback of 500,000 shares is a good baseline number = 2% of shares outstanding. This is similar to where 2022 will likely come in. 7.) buy back minority interests (Allied, Odyssey and Brit): Fairfax was very active on this front in 2022, spending $750million to buy back a significant chunk of Allied. My guess is we see another spend of $500-$750 million in 2023. - some on the board feel this activity is similar to Fairfax doing a buyback. It does result in Fairfax shareholders owning a larger share of Fairfax earnings. 8.) buy equities - current holdings: Fairfax’s biggest spend in 2022 was increasing its ownership of existing equity holdings = $1.14 billion. Makes sense we see a step down here in 2023. a.) take private: Recipe = US$340 million, Grivalia Hospitality = $195 million b.) increasing ownership: Kennedy Wilson, Fairfax India, Altas, Altius, Ensign, John Keels, Foran, Myrilineos = $800 million in total. 9.) buy equities - new positions: Fairfax spent a significant amount on large cap equities/private equity in 2022 = $550 million. Perhaps Fairfax increases this amount in 2023. a.) large cap US: Bank of America, Chevron, Occidental, Micron (add) = $350 million b.) private equity: JAB investment fund = $200 (another $250 million in notes) When you look back at 2022 you see a very balanced approach by Fairfax: - grow insurance +20% in hard market - opportunistic - pay $10 dividend - sell high: pet insurance - opportunistic - buy back Fairfax stock - opportunistic - take out minority partners - increase ownership of equities already owned - opportunistic - seed new equity positions - opportunistic For 2023 i see Fairfax doing more of the same as 2022. Balance. Rational. And as a shareholder, i applaud it. Lots of low risk / high return decisions that will benefit shareholders for years to come. What changes from 2022 could we see in 2023? 1.) I think we will see some more purchases in India; and perhaps a very large one. I love Fairfax’s long term track record in India. But big purchases and Fairfax still makes me nervous… so we will see. 2.) perhaps we see Fairfax get more active on the stock buyback front. But i am not sure. Looking at 2022, Fairfax appears to prefer buying other equities trading at bear market lows. 3.) large cap US stocks: coming out of the Great Financial Crisis, Fairfax was flush with cash (thank you credit default swaps) and they put more than $1 billion into large cap US stocks. Looks like they might be doing the same thing again. Bottom line, i love how Fairfax allocated capital so far in 2022. And i look forward to seeing what they did in Q4 and what they do in 2023. Interesting and exciting times for Fairfax shareholders.

-

@Sweet There is always new news. That is why forecasts are usually always wrong. And that is not because people making forecasts are stupid. Investors need to attach probabilities to forecasts and expected future outcomes. Tail events can happen. Bottom line, record warm temperatures in Europe in winter have impacted the accuracy of forecasts from 3 and 4 months ago. That is a wonderful outcome for Europe. Does Europe (and the world) no longer have energy issues? Of course we do. How will it all play out? Not sure. Oil stocks are a 20% weighting for me today. I remain bullish on the sector (especially looking out a year or two). Happy to collect close to a 5% dividend and wait and see what happens. I expect we will see wicked volatility.

-

I am of the opinion that Fairfax shifted their equity investing approach somewhere around 2018. Since 2018 they are just making much, much better decisions with their equity investments (especially when compared to 2016-2017). Paul left Fairfax in 2019 and i wonder if his leaving was not tied to Fairfax’s shift in strategy with its equity holdings (‘fit’, i like to call it). Fairfax Africa was Paul’s baby and it was a complete dog costing Fairfax hundreds of millions in cash and also significant damage to its reputation (lots of investors in Fairfax blindly invested in Fairfax Africa too and lost their shirts). It has taken Fairfax years to ‘fix’ the many poorly performing equity investments purchased before 2018. Paul continues to be Executive Chairman of Recipe and that stock was a another dog for minority shareholders who owned it long term. Clearly Paul didn’t leave Fairfax to ‘retire’. What companies does he continue to be actively involved with? He is currently CEO and Executive Chairman with Greenfirst. That company has ‘old Fairfax’ written all over it (poorly managed, terrible cost structure, very tough current environment). Where do minority shareholders fit? Good luck. Paul is also involved with Torstar. Currently he and Bitove are engaged in a very public falling out. I am not suggesting Paul is not an outstanding person. Or that he will not make himself and shareholders a bunch of money moving forward. Having said that, i am very happy that Fairfax appears to have learned from their past mistakes and has moved up the quality ladder (with top notch management at the top of the list) when making equity purchases. i think it is very instructive to look at who replaced Paul at Fairfax… Peter Clarke. Peter does not look like he is actively driving the bus on equity purchases. I don’t know this but his role in the company appears to be a little different than Paul’s role was in the past. Fairfax has a $51-$52 billion investment portfolio. They look well positioned today in terms of management.

-

@cwericb i am confused. When i read the press release from Chorus’ web site it sounds to me like the debentures Fairfax owned were repaid early. And the 24 millions warrants Fairfax had expired worthless. Does this not mean that Fairfax no longer has an investment in Chorus? ————— - https://www.newswire.ca/news-releases/chorus-aviation-announces-redemption-of-its-6-00-senior-debentures-and-sale-of-two-wholly-owned-aircraft-873908141.html ————— - https://chorusaviation.com/chorus-aviation-closes-redemption-of-its-6-00-senior-debentures/ HALIFAX, NS, Dec. 29, 2022 /CNW/ – Chorus Aviation Inc. ("Chorus") (TSX: CHR) today announced that it has closed the redemption of $115,000,000 principal amount of Chorus’ 6.00% Senior Debentures due December 31, 2024 (the "Debentures"), representing all of the Debentures that were outstanding immediately prior to the redemption. Chorus previously announced its intention to redeem the Debentures on December 14, 2022. The Debentures were secured by certain Dash 8-100 and Dash 8-300 aircraft and real estate property owned by Chorus’ subsidiaries (the "Collateral Security"). The Collateral Security has now been released. In connection with the issuance of the Debentures, Chorus issued 24,242,424.242 warrants to affiliates of Fairfax Financial Holdings Limited ("Fairfax") entitling the holder thereof to acquire, on exercise of each warrant and subject to certain adjustments, one Class A Variable Voting Share or Class B Voting Share of Chorus at a price of $8.25 per share (the "Warrants"). The Warrants have now expired.

-

Fairfax has been simplifying the ownership structure of its assets in India. It owned IIFL Finance and IIFL Wealth both directly and via Fairfax India. Late in 2021 it sold its direct holdings in IIFL Finance and IIFL Wealth. In 2022, Fairfax India sold its holding of IIFL Wealth down to a 3.8% positio. Why? It appears at least one reason was to get their ownership of various assets in India compliant with regulators to allow a Digit IPO. —————- Fairfax bought 49.2% ownership position in Quantum Mutual Funds for $43 million in 2015. It would be interesting to know what the position is worth today… - https://www.business-standard.com/article/markets/fairfax-to-buy-49-2-stake-in-quantum-advisors-115110600879_1.html —————- Fairfax looks to settle mutual fund cross-holding norms case with Sebi - https://economictimes.indiatimes.com/markets/stocks/news/fairfax-looks-to-settle-mutual-fund-cross-holding-norms-case-with-sebi/articleshow/93883299.cms?from=mdr —————- “The Securities and Exchange Board of India (Sebi) rules do not allow any entity to hold more than a 10 per cent stake in more than one mutual fund house. Fairfax has more than 10 per cent shareholding in two mutual fund houses - Quantum Mutual Fund and IIFL Mutual Fund.” “HWIC Asia, an affiliate of Fairfax Financial Holdings, has a 49.2 per cent stake in Quantum Advisors, the sponsor of Quantum Asset Management Company and Quantum Mutual Fund.” “Similarly, FIH Mauritius Investments, an entity of Fairfax Group, owns a 13.62 per cent stake in IIFL Wealth Management, which is the sponsor of IIFL AMC and IIFL Mutual Fund, the latest shareholding data with BSE showed.” “The capital markets regulator, in October 2021, issued a show cause notice against Fairfax Financial Holdings Limited (FFHL), the ultimate parent entity of Fairfax Group, alleging a violation of mutual fund rules by FFHL, according to the draft IPO documents of Go Digit General Insurance Limited.” “Go Digit, a firm backed by Canada-based Fairfax Group, filed preliminary papers with Sebi on August 14 to raise funds through an initial public offering (IPO).” “FFHL had filed a settlement application dated June 3, 2022, with Sebi under the Sebi (Settlement Proceedings) Regulation, 2018," the company disclosed in the draft IPO documents. “The company further said that FIH Mauritius Investments, in which FFHL indirectly holds shares, has since entered into a binding agreement for the sale of certain of its shareholding in IIFL Wealth Management, the sponsor of IIFL Asset Management and IIFL Trustee.”