SafetyinNumbers

-

Posts

2,819 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

They would have more liquidity by adding the to the TRS vs share buybacks all else being equal.

-

If they bought the shares back, we would find out within the first 10 days of December.

-

If Fairfax added or reduced its TRS position this month what would you think? Keep in mind we wouldn’t find out until February and the news would accompany earnings so if it does happen it will be difficult to tell how the market takes it. There was a cross of ~216k shares last Tuesday at the close which is why I’m asking. That cross could be related to something entirely different but changes to the TRS are a possibility.

-

Glider hopefully is right that the tax losses on FDGE can be used by Fairfax and there could also the potential for lottery ticket returns based on making a further investment which probably be more difficult to do as a public stock. That’s a trade I might make too so I’m not put off by it. I think Fairfax is an expected value investor and I don’t think that will change as long as Prem is in charge. Most investors want them to use the same heuristics they do to make investments and so most investors will be constantly frustrated. Not averaging down is one of those heuristics. Investors prefer FFH get a steady 12% on their equity portfolio vs a lumpy 15% even though FFH itself is a lumpy 15% investment. Arguably the floor returns are higher for FFH now than in the past decade because of the change in the interest rate environment and the high float to book value ratio.

-

Quants love consistent earnings and analysts predicting growing earnings. Fairfax should have more consistent earnings the next few years given the structure of the bond portfolio.

-

On the face of it, it’s bigger, more liquid and has a larger dividend.

-

Maybe it’s because of Viking’s email or becsuse MKL was so disappointing but RBC is now calling FFH one of its preferred names taking over for MKL.

-

If Fairfax wasn't the 30th biggest weight in the S&P/TSX, it would be harder to disagree with your odds. The narrative will be around Buffett of the North, or India or Greece or Digit or something we don't know about yet but the mechanism is based on how active equity strategies are managed. I think those 3% odds are over 50% if Fairfax executes and given the set up, I don't think it's that big an if.

-

I would argue that with passive being much greater competition for active managers than ever before, the move has the potential to be even more pronounced. As long as BV is growing at a healthy rate, the multiple will keep expanding. IFC trades at ~2.5x BV based on a ~13% ROE average for the past 10 years. It’s BV hasn’t grown this year but it’s expected to resume so it’s kept it’s multiple so far. For Fairfax, expectations are relatively low for forward BV growth (10% at 1x?) despite all of the evidence to the contrary.

-

I did the math and it’s just under $2000/sh after accounting for the dividend unless I screwed it up. @vinod1 where would you set the odds on book value being > $2777 (current BV + 2000 - dividends) in exactly 10 years and where would you set the over/under on BV in 10 years?

-

I think the price will ultimately drive the narrative which will increase Social Value from a negative to a positive. The price will move as long as Fairfax executes and grows book value 10%+ which I argue is hard not to do given the float to book value ratio. As it becomes a bigger part of the index, active managers will have to buy it and they will need a rationale. The analysts will also need reasons to increase their price target. The narrative will change because the multiple expanded not the other way around. Some investors will argue float is valuable and businesses that generate float are worth more than book value. Others might appreciate how quickly dividends and associates income are growing as Viking pointed out. After some big gains in the equity portfolio some PMs will talk about the cheap exposure to Greece and India. The negatives will become positives. That’s my bet anyway, it’s still a bet as there are no sure things but the probability is high in my opinion. The beauty is at this price, it’s a free option. The more skeptical current holders are the longer it will take as extant holders determine the selling price. The institutional buyers use VWAP so they are price takers while sellers are price makers. It will be fun to see how it plays out. It’s been a good run for 3 years already as weight in the index has more than doubled from 45bps to ~100bps now. There is no reason for that to stop unless FFH book value growth stalls for a few years. It’s just hard to see how that happens in the next 5 years.

-

That’s great. He didn’t respond to me when I sent him the podcast. He cites a lot of of factors that have nothing to do with intrinsic value. My market model is Market Value = Intrinsic Value + Social Value. Social Value can be positive or negative. For Tesla it’s hugely positive. For Fairfax, it’s hugely negative. I only invest in things with negative SV. The big downside of that approach is that the cost of equity capital is high which means less flexibility and more risk.

-

I heard from a KW institutional investor in August who had heard the Business Brew podcast on Fairfax that ultimately decided to switch their position from KW to FFH. One of their reasons for selling was because they thought management compensation was too high. I’ll add, the high dividend makes it harder to grow but probably helps with valuation.

-

And they are at about 43% now? Does that make it less of an issue for you @This2ShallPass?

-

The original institutional investors (OMERS, Fidelity and Markel, I think) who negotiated this deal on behalf of minority shareholders are the ones who have let us down. In theory, they were counting on themselves to be buying to close the discount every three years to avoid this dilution. Unfortunately, the key decision makers are probably out of their jobs and there isn’t any capital for stocks outside their benchmark. This is the first performance period where it’s meaningful so let’s see what they do. FWIW, they have bought more than enough stock back at lower or similar prices to offset the dilution but I think most people think about it like you do.

-

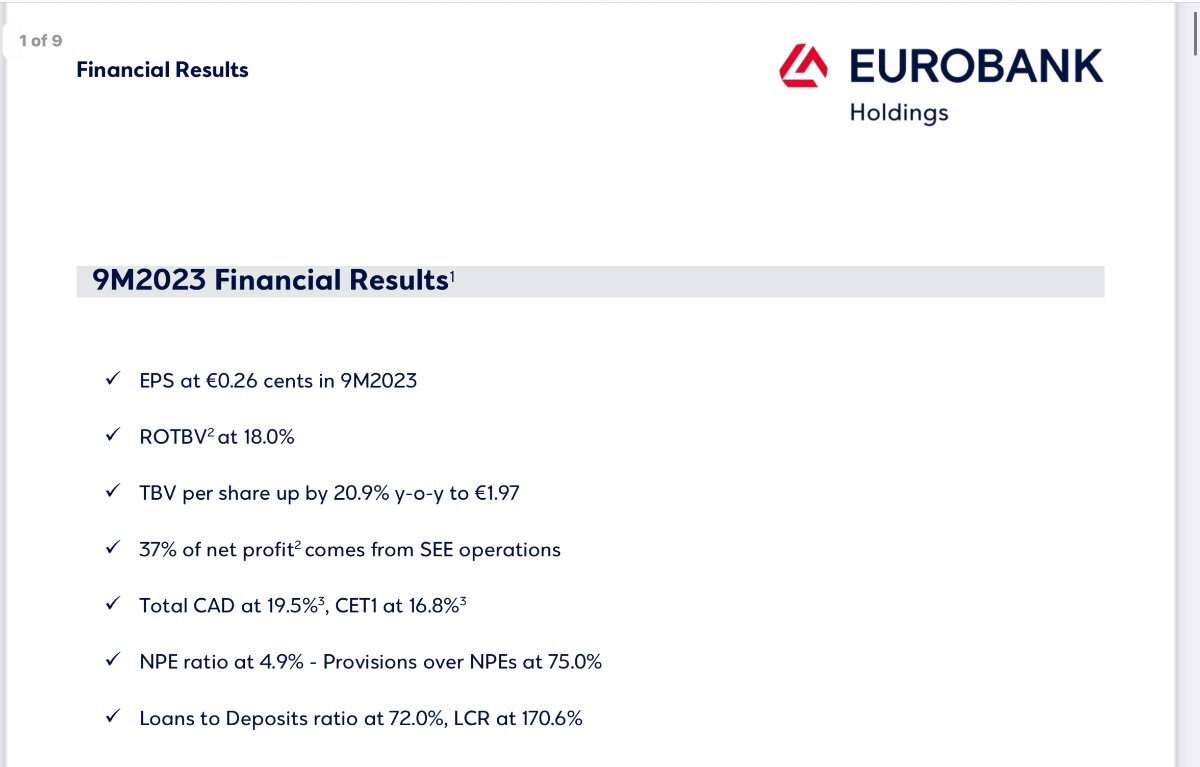

Strong numbers out of Eurobank after the close. Looks to be ~5x P/E. Cash dividends to start next year which will probably help the share price but since FFH equity accounts for it our on an equity basis, it’s about US$85 of book value earning a 20% return.

-

I think their goal is long term capital appreciation investing in India. They are expected value investors so they have a bunch of different bets most of which have worked out very well while some haven’t. It’s kind of what one would expect in an opportunistic portfolio. I run my portfolio similarly so maybe I’m not as bothered by it as you are. I think the IPO will finally give FIH a low cost of capital to use as currency for acquisitions which might accelerate growth as they have been capital starved since the last secondary in 2017. If most are sellers like you then maybe the discount won’t close.

-

That’s a terminal growth rate. The most it could be is nominal GDP. Presumably the forecast period growth rate is a lot higher or the current valuation is incredibly cheap. Maybe both. To call it a distraction implies the analysts and PMs don’t have to time to analyze the company.

-

If the current discount rate is too high. Then the present value is significantly higher. Maybe they don’t want to write up a discount purchase too quickly. They increased the discount rate by ~7% since the end of last year and are still up ~40%. Why do you think it’s a distraction for management?

-

Is there anyway to assess midyear or is there only an annual update?

-

100% agree. The slowing of premium growth in Q3 and very high investment income going forward increases the possibility of much higher surplus capital at the insurance companies. I’m not an insurance expert so I’m wondering what’s the best way to assess what Fairfax’s surplus capital position is now, what it might get to and where it will be used? The analysts are currently assuming a declining ROE as capital builds presumably because they assume low return opportunities for that capital. They already have very low assumptions for associates income and capital gains on the equity portfolio so there are multiple opportunities for upside surprises.

-

He covers ~25 companies and has no clients. I don’t think it matters much to him. His analysis is basically, “a lumpy 15 isn’t worth owning”

-

it would be nice if everyone who trimmed FFH bought FIH. The discount would close in no time.

-

I think it’s too soon to start trimming. Maybe once it gets into the S&P/TSX 60. I appreciate that some people have insanely large positions though so each his own! I still expect the index chase to continue and eventually when the stock is 1.5-2x book value, the analysts may start to model earnings growth which will finally get the quants and their active counterparts involved.

-

Thanks for the insight and the link! Last Q3 and the switch to IFRS17 really made me think about “reserve management” more holistically. It makes sense that Fairfax would reserve more aggressively than peers because of their incentive structures and tax deferral advantages. Last Q3, outside of CAT, the combined ratio was 85% which seemed like a flex. They have recently highlighted on conference calls that even with a significant CAT event, underwriting profit should be able to offset it which I don’t think most analysts have appreciated.