SafetyinNumbers

-

Posts

2,818 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Earnings estimates should be going up over the next few weeks for Q3 which might bring in some quant buying ahead of Q3 reporting.

-

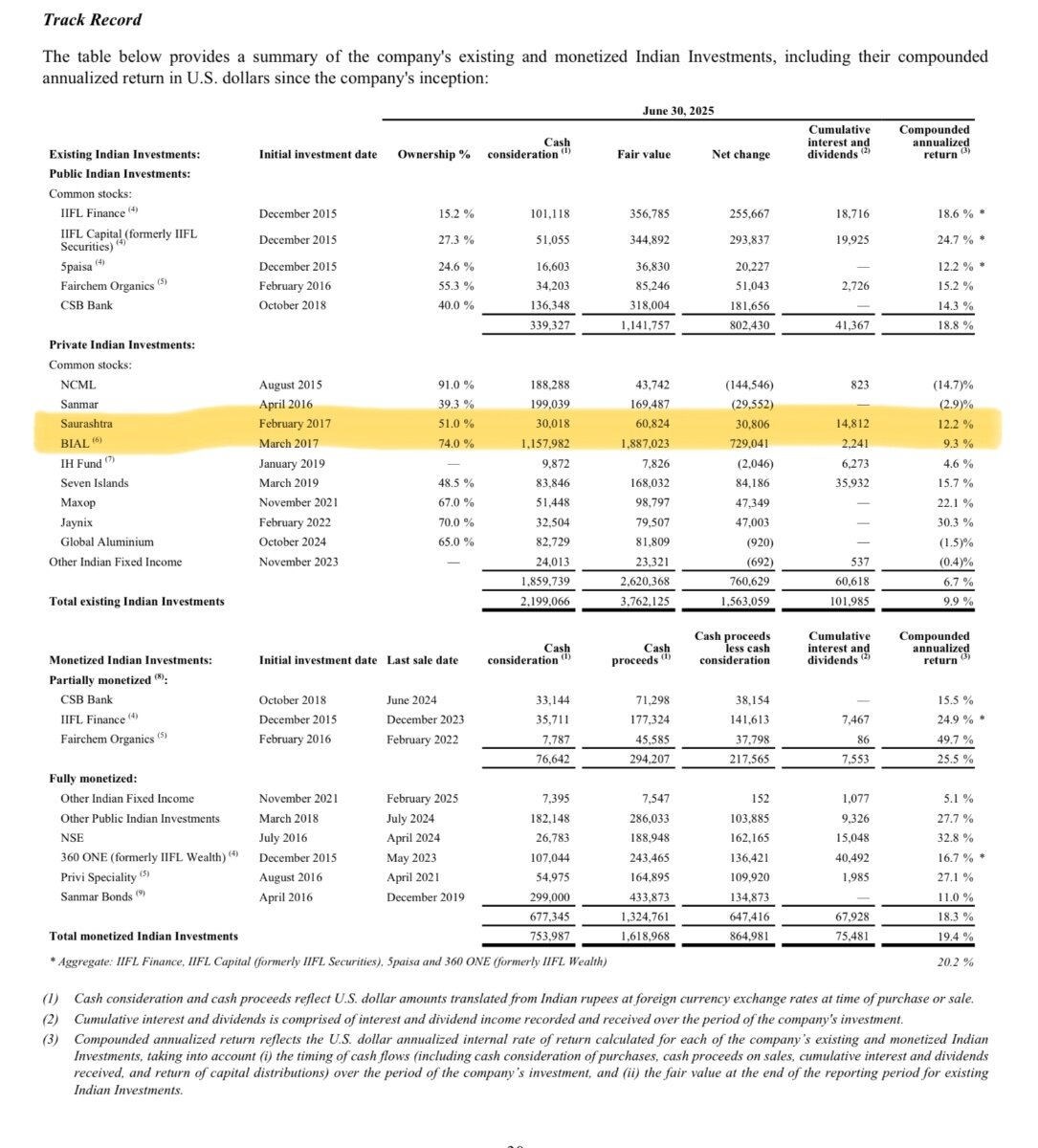

I think their strategy is to buy businesses that can CAGR 15%+ over long periods of time. Some are small and some are big but each investment they make grows their network. Over long periods of time that should yield dividends. I think everything in the private portfolio is marked conservatively in varying degrees such that intrinsic value (after performance fees) is probably closer to $35 vs the stated BVPS. That makes the CAGR starting net of IPO fees closer to ~13% since inception. Hopefully IDBI leads to a GP/LP structure where they can earn fees that offset the fees they pay Fairfax.

-

TLDR: Equity hedges and low interest rates.

-

At the time, Canada had proposed increasing the inclusion rate for capital gains to two thirds from half which would have increased the effective tax rate from 27% to 36%. It was ultimately not enacted.

-

It’s been helpful for the buyback.

-

It seems like he did buy the shares he sold on margin. Maybe that’s true for the rest too.

-

Still lots of our shareholders are happy to sell their shares at <10x earnings and have for the past 4 years. In part, maybe because the positions have become so big for some of them including some on this board but it is still interesting.

-

According to Perplexity, historically, if it’s been this quiet until this point in the season there haven’t been major hurricanes but analogs are only useful until the exception. It seems like we are set up for an another quarterly beat for Q3 at least. Estimates are pretty low anticipating cat losses and I assume they have a pile of reserves to release which might boost underwriting profit more than expected. Analysts will probably start increasing their estimates in October as they do their Q3 previews which will likely get quants buying.

-

KW doing an interesting transaction with help with some friends which I assume includes Fairfax. Hopefully adding some higher yielding fixed income to the portfolio. https://www.businesswire.com/news/home/20250918957991/en/Kennedy-Wilson-to-Acquire-Toll-Brothers-Apartment-Living-Platform-for-%24347-Million-Adding-Over-%245-Billion-of-Assets-Under-Management

-

How do you define heavy exposure to supercats? How do you think softer insurance markets impact near term results?

-

Is that just because of the number of companies in each of the 60 and the 500? Both are based on float, both have a committee decide if it should go in. The TSX 60 is not that different from the 60 biggest floats. The names that are in the completion index that are bigger than the smallest names in the 60 just haven’t had a chance to go in since there haven’t been any openings. The S&P 500 has spots open up regularly because it has more spots so large names get a chance to go in more often.

-

It matters a lot to their valuation multiples. TD estimates that the passive demand for S&P 500 members is 17%+ of the float.

-

Fairfax tends to do what’s best for the company. If management thought selling was the right thing to do there isn’t much of a decision to make.

-

Is there any money indexed to this?

-

The 60 is more comparable to the S&P 500. Both are committee based, market cap weighted and both are part of the S&P Global 1200. DJIA is a price based index.

-

What makes you say they exited early?

-

I’m sure they are still short a share. Literally one share so they can say they are still short.

-

Not a distraction to build a network such that other entrepreneurs with good businesses will seek out partnering with Fairfax over other options. Fairfax is playing a very long game.

-

Muddy Waters was throwing mud. They never had any ammo.

-

There were some distributions so return is a bit higher. Was marked at $61m.

-

If we lost money we wouldn’t get paid. If we were wrong on a big position we would get shown the door. Definitely stressful but understandable as a prop desk is all leverage on the bank’s capital. I don’t have any book recommendations with respect to that. I think my market structure thesis allows me to supersize my position in FFH and to use leverage generally. Really I’m just trying to understand if there are any factors that I’m missing that impact my intrinsic value estimate. Ultimately though share prices are just supply and demand. Most investors think the market is efficient so a lower price makes people assume someone knows something of course sometimes they do. That’s what makes the game hard.

-

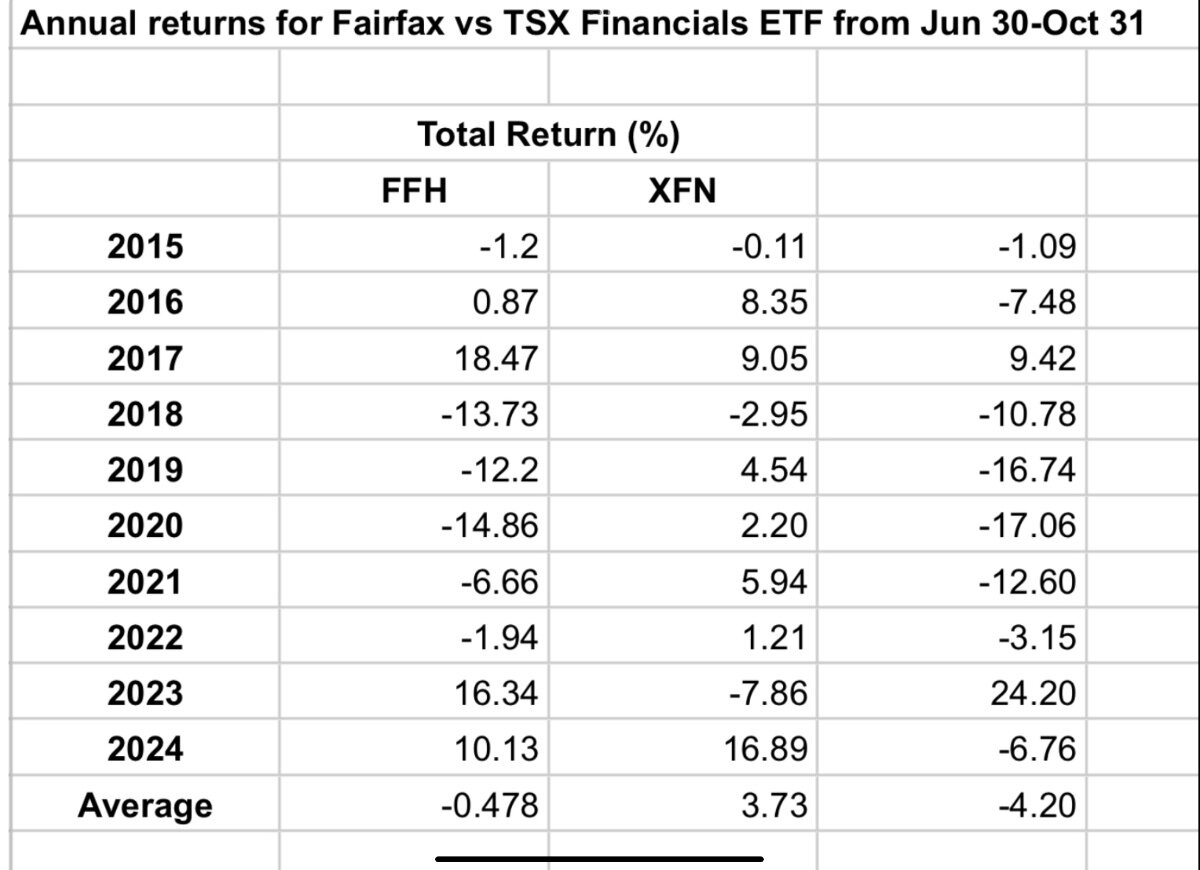

I was trained to always understand why my positions weren’t “working” because I usually had a someone at the bank looking over my shoulder asking me why I was losing money It makes sense when one considers how money is managed and who the marginal buyers and sellers are. No high turnover PM wants to look stupid owning a company that insures against hurricanes during hurricane season. If they lose money, they should have known better. From November through to Q1 earnings there is a lot of good news with three earnings reports, the shareholder letter and the AGM. I think @kodiak calling FFH a fat pitch on the Business Brew podcast helped defeat seasonality in 2023 or it was just that investment income and float were growing so fast that long term investors offset the marginal sellers.

-

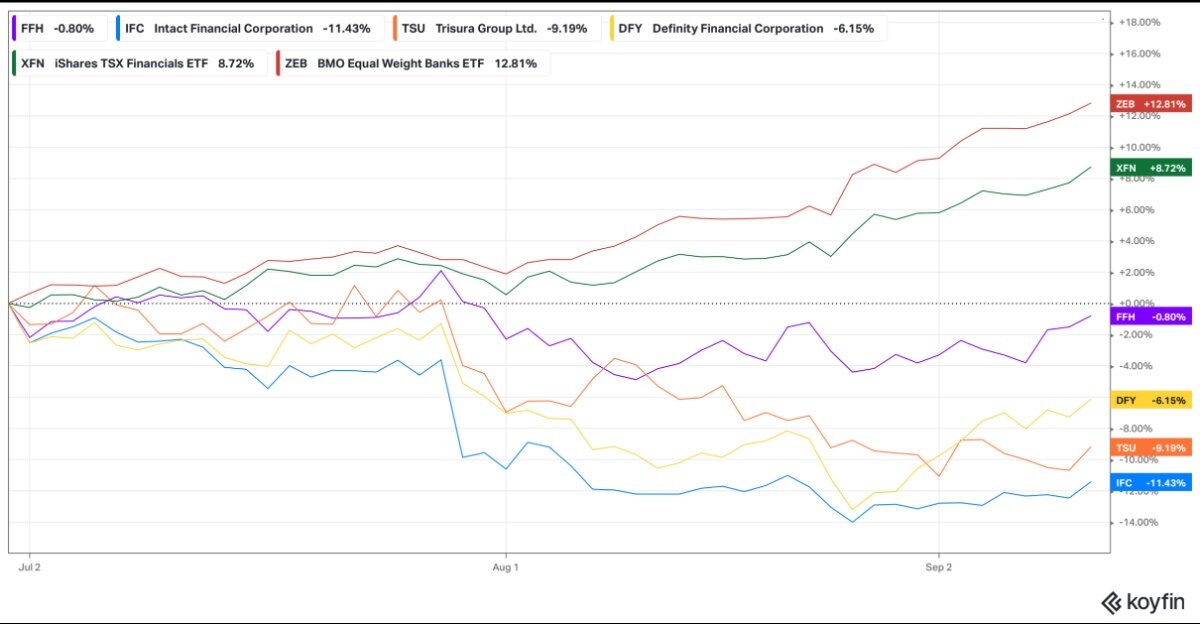

I still try to understand the flows. I think I have a good idea why we are going sideways recently including the historical underperformance during hurricane season and this year the rotation out of P&C insurers into more economically sensitive financials like banks. FFH has actually outperformed in a pretty big way vs the other P&C insurers.

-

I probably don’t have to use leverage too but I am.

-

I bought a few shares at $2340 a few weeks ago. It’s still over 50% as a percentage of net assets but I couldn’t help myself. It’s been a big mindset change for me to add at higher prices but the longer I own it, the better I understand the business and how cheap it is on an absolute and relative basis.