SafetyinNumbers

-

Posts

2,819 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Using low expectations instead of realistic expectations has kept investors out of the stock or encouraged them to sell too soon for years. Good for the rest of us, I suppose.

-

Regular marking up of BIAL provides some predictable book value growth for FIH. That might make it easier to own thus shrinking the discount.

-

I wouldn’t think of it as 1% dilution because they buy all of the shares contemporaneously with the grant. They could give them extra cash but instead they buy shares and stick them in treasury.

-

Just a separate bet. I guess it would be a hedge since you are long the stock.

-

I like Annie Duke’s idea about putting it in terms of bets. So the question is how much would you bet on FRFHF NOT doubling over the next 5 years? That is, if total return hits 100% within 5 years, the bets over and you lose.

-

The yield curve might also get steeper which means higher long term rates. Credit spreads could widen. They could invest more with KW and get higher mortgage rates or invest more in real property at higher cap rates. It also takes time for lower rates to work their way through the portfolio given duration. If the average coupon falls from 5% to 4%, then the equity portfolio has to do 12%. That still doesn’t seem like a high hurdle given how low carrying value is vs fair value for big chunks of the equity portfolio.

-

You may not appreciate how 3:1 investments:equity leverage works when interest rates are normal like they are now. With fixed income book (two thirds) doing 5%, if only takes a 10% return on the equity book (one third) to get to a 20% pre tax return on equity as long as underwriting is offsetting head office costs including financing costs which it is more than doing now. Meanwhile the equity book might do much better than 10%. Eurobank is over 10% of the portfolio at carrying value but contributes at a 20% return on investment because it’s marked at 5x earnings. That means the hurdle rate for the rest of the portfolio is lower.

-

They issued a lot more equity for operating companies after that including Dairy Queen, Net Jets, Gen Re and BNSF. I think we’ll only see FFH issue stock for insurance acquisitions or if they need to fortify the balance sheet. Both seem unlikely in the foreseeable future given the valuation and fortress like balance sheet, respectively.

-

That’s probably true but as @Vikinghas pointed out, it also reduces the volatility of earnings and increases the earnings. They can also restructure the balance sheet to improve ROI without as much reflexivity risk.

-

Exactly right and it’s all explained by the IFRS accounting rules and Fairfax’s own conservatism. Fairfax didn’t start buying 20%+ positions until 2012 from what I can tell. The nature of the accounting is that mistakes are written off quickly. If they ultimately recover the returns look outstanding on a lower cost base. For the successes, we only get to accrete the net earnings in the book value. We don’t get the benefit of the multiple of those earnings or expansion in the multiple in book value until it’s sold but once again the returns look great. The accounting suppressed this flywheel until the last few years but now it’s in swing. Combine this with 3:1 leverage and you can see why I’m so bullish on forward ROE.

-

I think this is another generalization that is providing an opportunity to buy back stock cheap. First, the street is selling the stock on lower GWP but they are using less reinsurance so NWP is growing faster. That’s important for returns which is what Fairfax is focused on as long term investors. It’s ironic that guys like Bloomstran don’t like Fairfax because they use reinsurance but now it allows them to grow NWP/share in a soft market without writing bad business. Fairfax’s diversification and decentralization helps with this. Asia is uncorrelated to other insurance markets and Fairfax has traditionally passed through a lot of the risk to reinsurers. Lately they have been ceding less. Second, they are very conservative on reserving so underwriting profit should be buffeted by strong reserve releases for years to come. Excess reserves are just future equity masquerading as a liability. Third, they can buy in minority interests at very low valuations which is very accretive and has the same effect as growing net premiums/share. Consolidating Digit starting in Q1 will also help with this,

-

It also boosts future ROE all else being equal as the earnings power is unchanged when current earnings are used for buybacks. Further, I think it’s better to think of ROE as a range as opposed to static. 15-25% average ROE over the next 5 years has a 90% confidence inferval in my mind given what we know about the leverage and gains that will make their way into income over the next 5 years.

-

For the most part yes. They cannot use insurance subsidiaries investment portfolio to buyback stock as some seem to think they can. It sounds like you rather they keep more excess capital at the insurance subs to make equity investments when they already seem to be overweight fixed income and avoid buybacks.

-

This strategy requires very good stock picking to achieve outsized returns as there is less leverage over time. Fairfax’s strategy doesn’t but it might achieve them nonetheless.

-

Q4 and FY results tomorrow - predictions?

SafetyinNumbers replied to dartmonkey's topic in Fairfax Financial

Is Poseidon still reporting quarterly earnings? They also come in in a quarter lag. -

Because that what competes for capital at the holdco. This is not Berkshire, this is Fairfax. I think they want to maintain the investments:equity leverage at 3:1 to help meet their 15% BVPS growth target. If they lose this discipline then our expected returns risk dropping to BRK’s over time.

-

Q4 and FY results tomorrow - predictions?

SafetyinNumbers replied to dartmonkey's topic in Fairfax Financial

ORLA is marked to market every quarter so the gain will only be from the mark at the end of Q3. -

The only alternative to buybacks are buying in the minority interests which can be deferred as the financing cost is fixed or buying other insurance companies. I don’t see other high quality insurance companies trading at FFH’s valuation.

-

I think this comes back to the difference between the holding company and the insurance subsidiaries. It seems like the holdco owns insurance companies and the TRS. The holdco doesn’t have much excess capital as it uses it for buybacks. We know where a lot of the future capital will be spent at the holdco: buying back stock at good prices, buying in the minority interests at fixed prices and buying in the TRS wherever they trade and presumably when the stock is more expensive. The insurance subsidiaries seem to have a lot of excess capital to do deals. I’m not sure why they need to own more fixed income than the float. There is probably $6b available to switch from fixed income into equities if the right opportunities came along. Maybe that’s KW and IDBI in the near term but they are always generating more capital.

-

They are sending up as much as they can. There are regulatory limits and they need to retain some capital at the insurance subsidiaries for growth in premiums.

-

I wish y’all would stop confusing the insurance subsidiary investment decisions with the holding company investment decisions.

-

This is likely set up this way so that FFH doesn’t have to consolidate the KW debt. My guess is Fairfax will be well protected in the shareholder agreement.

-

This comments are mainly focused on the narrative to explain the discount but ultimately it will come down to supply and demand of shares. Passive demand is going up, buybacks bring supply down. The larger unrealized gains investors have the less likely they are to sell shares for tax reasons also reduces supply. Maybe we’ll need another hard market for momentum investors to jump back in for revenue/float growth to get the multiple really going but in the meantime shares will be bought back and minority interests bought in which provides excellent growth on per share basis.

-

The accounting made those acquisitions look bad but my guess is the economics were on average pretty great.

-

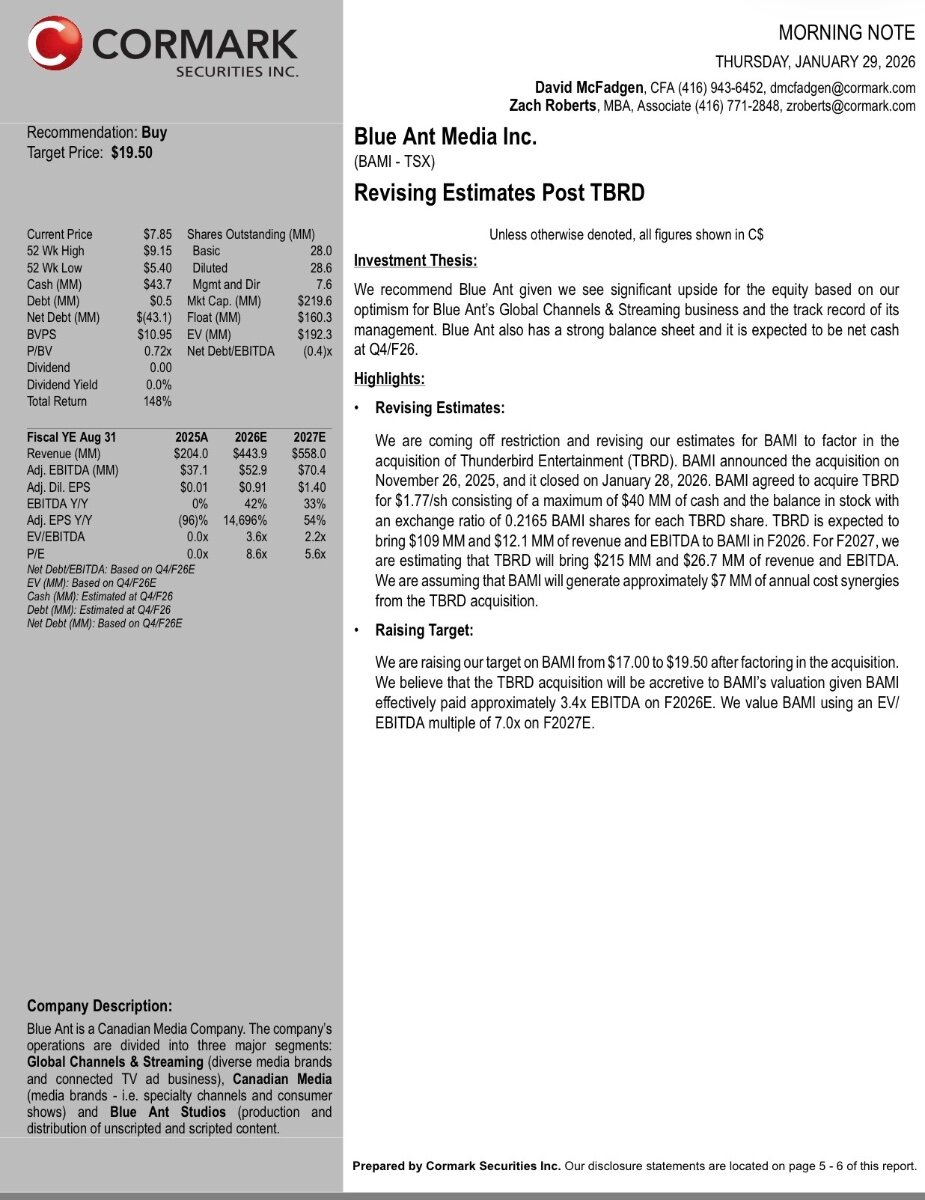

Cormark likes BAMI. They have it earning $1.40 in their fiscal 2027 ending in August so < 5x P/E on their estimates. $19.50 target is based on 7x EV/EBITDA.