philly value

-

Posts

117 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by philly value

-

-1.2%, which after a start to the year that included Ocwen and ASPS, feels pretty good.

-

How do you select between the stock and its bonds?

philly value replied to Cardboard's topic in General Discussion

It's not a question you can give a blanket answer to because every situation is different, but let's say you can lump these situations into two categories: (1) situations where the bonds are still trading on a yield basis, and an outcome in which the bond is paid until maturity is still likely, and (2) situations where bonds are trading on a recovery basis, and it's highly unlikely they survive to be paid out as scheduled. In (1), it is about choosing an appropriate risk-reward within the capital structure, and comparing your perceived risk of the assets versus the expected returns on the stock and the debt. I don't think there is much of a blanket statement to make here other than you obviously take higher risk with the equity position and expect to be rewarded with a higher expected return, and you need to be comparing the yield of the bonds to whatever you think a reasonable return on the stock is. How big of a spread there should be obviously will depend on the business itself and how volatile you expect its value to be, how much debt there is versus equity, where the particular tranche of debt you are evaluating is sitting within the capital structure and how much security there is in how the agreement / other agreements are structured, etc. In (2), unless you believe the market has it completely wrong, if you are seeing things trade in the 50s or below, most likely the debt is no longer trading on a yield basis where someone is thinking about the spread they need to be rewarded in order to buy the paper [with exceptions, clearly a very high duration bond i.e. a newly issued 30 yr treasury could trade at 50 just based on yield]. Instead, it's trading on where people think recovery value is in a restructuring, whether in court or out of court. In these situations, the equity is also no longer a security that is trading based on expected required returns - it's an out of the money option on the value of the business. Playing with buying the equity in this case is usually a foolish game; it's highly likely the equity is a zero or near zero. Investing in distressed debt can be rewarding but is really best suited for specialists and people who can actually get involved in the process, not retail investors. So I would simply avoid this type of situation from the perspective of someone at home. -

What is the extent of the 'opportunity' in the oil market?

philly value replied to bmichaud's topic in General Discussion

I think it depends on what you are looking for. If you are looking to make a macro bet on oil or gas prices, that is easy to do and there is clearly an "opportunity" where prices are currently very volatile. In terms of betting on producers, I'm not sure there is an opportunity and fairly sure that there isn't an attractive opportunity for the small individual investor. For the small individual investor who is mostly stuck investing in equities, you face the issue that you are not betting on the long-term success of the producer, you are betting on the very near-term success of the commodity price environment essentially. You are really buying a short-term highly levered option, not an equity interest in a business. When you see debt tranches trading on a recovery basis and no longer on a yield basis then you know the equity is not trading on a long-term business valuation basis anymore. Even if you can buy the debt and normally be in a position to own the company, many of the smaller producers at least (let's say up to several billion in TEV before the crash for sure, but even larger ones) are in a position where, in Chapter 11 bankruptcy, they are finding it difficult or impossible to reorganize because there is not a real business to organize around at current prices. At $40 oil and $2 gas, few of these guys can produce positive unlevered free cash flow with a sensible drilling program. If you can't even produce FCF on an unlevered basis, there is no room for debt capacity, at which point you have everyone in the capital structure forced to take equity in a reorganized, zero earnings company. It's not an attractive proposition. What has happened in a few cases and seems likely to happen is that the Chapter 11 process turns into a liquidation and the assets are sold to someone who can sit on the assets or absorb them into a bigger organization. And if that happens, even if you held the debt you are going to be closing your position via an asset sale in the current depressed pricing environment - you don't get a piece of the business in order to make money if pricing and the business recover. So effectively my view is that if you are taking a macro view on prices, express that view directly and bet on prices. I think trying to bet on producers is little more than a levered short-term play on prices at this point, in most cases. -

Oil, wow, WTF happened to all of the oil bugs on this site?

philly value replied to opihiman2's topic in General Discussion

I never did understand what possible purpose allowing corporations to have bankruptcy protection served. It protects the poorly run firm from the consequences of its decisions at the expense of its creditors and competitors. If you just let poorly run firms die and allow the creditors to split up and sell off any assets, then the creditors get something and the better run competitors have one less competitor and can remain strong. Like every form of protectionism it protects the bad actors at the expense of the good actors, inverting the incentives, and makes the entire industry/economy weaker. It's like watering the weeds and poisoning the flowers. I understand the sentiment but I think a world without the Chapter 11 process would be much worse for virtually all parties involved. On the creditor side, the best interests test which is a requirement to confirm a plan of reorganization addresses pretty firmly the idea that creditors could obtain a higher recovery in a liquidation. A plan is only confirmed if it can be shown to provide recoveries to creditors higher than recoveries in a liquidation. A "bad business" which should no longer exist, in which the market value of the assets is greater than going-concern value, should not emerge from Chapter 11 as a reorganized business. Do some slip through the cracks, of course, but this is the guiding principle behind the process - the purpose being that for a very large number of situations, the company has a capital structure that doesn't work with the financial reality, but is still worth more as a business than a bunch of assets to be liquidated. The one area where there is obviously a net loss to the system is advisory fees, which tend to be very substantial in a prolonged Chapter 11. That said, even in a liquidation if there is contention among the creditor classes there would likely still be substantial legal fees, if not the same level of financial advisory fees. -

Nobody knows of course if things will go lower or even much lower, the only thing is if you are paying a reasonable price for what you are buying today. Things are flopping all around today but currently the S&P 500 at 1882 is trading at roughly 16X 2015 earnings (according to Cap IQ) which in the interest rate environment we're in seems reasonable. Apple at $99 this morning I think was trading at 6.4X TEV/LTM FCF. That seems more than reasonable even given the risks there.

-

There's two arguments, first being that profit margins are peaking and the forces that have driven them there can't propel them further higher; the second being the idea of mean reversion, so profit margins must fall back to where they've been. I dont think i've done anywhere near enough research to be qualified to talk to either point, but my intuition points to the first argument being likely true and the second having little basis to support it. Quite simply it seems to me that when you read about Corporate America 40 years ago versus today, the focus on efficiency is there today much more than it once was. There simply isn't the ability to hide and allow inefficiencies to persist anymore. The rise of private equity and more recently of shareholder activism has to play some role in that.

-

I doubt there is any way you could completely kill this bias. To me, what is most important is that I never invest in something I don't understand because a "guru" owns it. As people say, the guru isn't going to tell you when to sell vs load up when something bad happens. I can't invest in things where I am unable to independently assess the value, because you need to be able to understand how value changes over time in response to new information.

-

Pray tell how you made money from listening to his "7-10 predicted returns of various assets over the past 15 years". Some facts please. I'm not sure about the interim predictions, but if you followed their forecasts from late 90s you would have bought REITs and emerging market equities and done very well, avoiding the S&P which they predicted would have a negative return for the decade. Their return projections in the depths of the recent crisis would have led you to re enter the U.S equity market.

-

Yeah, as much as past performance doesn't determine future results, it is hard to get excited about putting money in a distressed fund that returned just over 7%/yr from 2009-present. That said, two caveats are (a) they have very much underperformed over the past year, so the numbers looked a lot better from '09-13, and (b) the fund inception was late 2009, at a point when the best bargains were long gone. But really, distressed debt is an asset class you expect to be able to do OK in virtually any economic environment, because there are always bad businesses and bad capital structures even in good times. But the big money returns come from the funds raised in 08, in early 2000s, in late 80s, etc. You got 20, 30, 40% IRR or more from the best funds in those years. The returns in other environments can be good but will generally not be amazing. And now is a particularly tough time to get into this market. There has been a significant structural change in the market over the past two decades, in which distressed debt is now a legitimate asset class, and tons of funds allocate capital towards distressed or are dedicated distressed players. And so in an environment like today where there are few big distressed opportunities, things easily get bid up to levels where the risk/reward is hardly attractive. Caesars debt a year ago was ridiculously overpriced (second-lien, anyway) but plenty of "good" funds piling in because, what else is out there that you can make a big position out of? With energy, you hear of all the money raised to pile into distressed energy debt; a lot of that may be talk vs. real money, but still, that gives an idea of the sentiment of the market today.

-

POLL: When Buffett is gone, whither BRK's intrinsic value?

philly value replied to cobafdek's topic in Berkshire Hathaway

I wasn't on this board until a few months ago, but from looking back do agree somewhat that I am surprised that the level of optimism in certain names today appears not much lower than it was several years ago at much lower valuations. Looking back at the AAPL thread, for example, it seems there was not nearly as much enthusiasm as I would have expected a great business trading at ~15-20% FCF yield in mid-2013 to generate. That said, IMO this part of the cycle more than any is when talk of valuation is important, and when checking your assumptions carefully with others is likely to be useful. It was much easier a few years ago to throw darts and find something that was reasonably priced or underpriced. -

POLL: When Buffett is gone, whither BRK's intrinsic value?

philly value replied to cobafdek's topic in Berkshire Hathaway

Can't dispute that the two have done an incredible job. But in the bigger picture, their performance on a few billion of capital means little to the overall performance of Berkshire. And my guess is, if they were required to make investments of the size that would really move the needle at Berkshire, they would no longer be outperforming to the degree they have. -

Sure. But assuming your investment analysis is accurate, the optimal investments at an 11% discount rate are the same as the optimal investments at an 8% discount rate. You have more options to choose from at an 8% discount rate, but they are suboptimal. If you are using the same discount rate for all companies, then yes, it's clearly just a matter of "how low are you willing to go?" to find opportunities, and I guess the rate you choose becomes more about the macro environment than anything else (clearly the rate you use to discount cash flows must be lower today than in the 1980s). But using the same discount rate for all companies is a bit of a stretch. Personally, I may be happy to invest in a stock like KO if, based on my best projections of future cash flows, I expect a return of 8% per year. Given that even 30-yr treasuries are sub-3%, earning an expected 8% return on a "safe" stock like Coke would be highly attractive. On the other hand, if based on my best projections of future cash flows, I expected an 8% return from investing in Facebook, I wouldn't do it. The risk of those cash flows that I project being far off the mark is too high relative to an 8% rate of return. I would want a much higher expected rate of return, maybe closer to 15%. So I guess it comes down to how you handle risk in your valuation. Perhaps you use a low discount rate for all companies, but devise different scenarios and probability-weight them in order to come up with a valuation. Or, you come up with expected cash flows and discount them at a rate in line with the level of risk to achieving them, depending on the company. The difference a discount rate makes is huge. For Fastenal, at an 8% discount rate, my model says I should be willing to pay $65-70 for the stock. At an 11% discount rate, I should pay no more than ~$35. There are some times that the opportunity and the business are so obvious that you don't even need to project cash flows or think about a discount rate (AAPL at $380 per share is the best recent example I can think of). But it seems to me that with situations like Fastenal, you can't avoid thinking about future cash flows and a proper discount rate. Looking at the current multiple on earnings or cash flow and "eye-balling it" isn't much help in that kind of scenario.

-

POLL: When Buffett is gone, whither BRK's intrinsic value?

philly value replied to cobafdek's topic in Berkshire Hathaway

Regardless of whether or not Buffett stays, Berkshire is getting close to (what appears to be) a size where it can no longer retain all of its earnings. I mean, if you just think mathematically, if BRK grew at 10% a year, it would be something like a $1.5 trillion market value company in 15 years. That certainly isn't impossible, after all Apple is a single business and could reach $1T in market cap, but my guess is that it isn't long before a dividend or share buyback are instituted regularly. If so, it seems to me that the role of capital allocation at Berkshire will become *slightly* less important in its overall performance, with most of the performance differential vs. the market relying on how Berkshire's wholly-owned businesses perform versus the market. And thus, I'd expect that the incremental advantage in capital allocation that Buffett's talents provide may be reduced going forward, reducing the impact that his leaving has on future performance. The wild card is whether or not selling a whole business to Berkshire is still attractive after Buffett leaves; my guess is that as long as the acquisition philosophy remains the same, Berkshire will remain a good place to sell for certain owners versus alternatives (private equity, public markets, etc). Basically, my point is, if we were investing in a $50M stock fund, I'd pay a sizeable premium for Buffett to manage it over almost anyone else. But Berkshire is so far removed from that that I'm not sure how much Buffett is really worth these days over another capable person who believes in the same basic capital allocation principles. Could be totally off base but my two cents. -

I find this statement pretty funny. I don't think anyone is enough of a genius at stock selection that choosing a discount rate is at all difficult compared to that. Pick a random number between 8 and 15%. It is not going to have that big an effect on your returns, as long as you are willing to put in a lot of work to find investments that exceed your hurdle rate. I'm not sure what you define as "stock picking." To me, "Stock picking" in the value investing world is buying businesses where the price is sufficiently below your estimate of the value of the business as to allow a margin of safety. We can observe stock prices. We can only estimate business values, and to do so necessarily requires the use of a discount rate. Stock picking and the choice of a proper discount rate for a particular stream of cash flows go hand in hand. You can't pick stocks without first picking a discount rate.

-

Choosing a discount rate to use in a valuation is one of the most difficult things I've encountered so far in value investing. There isn't any real, useful advice from the experts. Guys like Buffett and Klarman will tell you what not to use - beta / CAPM - but will not tell you what to use instead. To me, a lot of times when I do a DCF I will solve for an implied discount rate based on the market price, which doesn't change anything fundamentally but makes comparison between opportunities a bit easier IMO. But it's really hard to know (a) what is a good framework to use in calculating the discount rate you would want for a given stock (obviously some stocks are riskier than others, in that the cash flows you project are less certain to occur, and thus a higher discount rate is warranted), (b) how do you account for low interest rates, do you use higher rates assuming they will go up? What if this results in you buying nothing, are you then relying on a macro forecast that rates will rise? Looking at Fastenal and did a DCF yesterday, and get an implied discount rate of 8-10% depending on aggressive of my projections, although all were relatively conservative compared to analyst forecasts. Is 8-10% good enough? In this environment, it seems like it may be...but I don't know.

-

Who owns all these 30 year mortgages at low rates?

philly value replied to LongHaul's topic in General Discussion

Seems to me the political ramifications of 30 year mortgages going away means that the government will find a way to continue their existence. I bet a large percentage of the people buying homes would be unable to afford them if they were forced into shorter term loans. -

As well stated as it could be. As to them unloading their outsized BRK position for other opportunities is what they are expected to do being a fund manager. Surely AV will do fine. But, what if you held a 60% position for longer than the 41 months, say, for 5, 10 years, won't that beg the question to investees, "Why don't I do that myself?" redeem 60% and avoid paying fees. It is very difficult to "do nothing" while managing money for others. Even if it is the correct thing to do. IMO, the years 2008-9-10-11...probably represented the best ever years for an individual investor willing to be bold and unfettered like Meacham. On the flipside, as we are now finding out, some of the worst years for the fund management world. Hedge funds are closing in droves, money is flowing out of active funds to index funds etc. The book that they all read like sheep was obviously wrong. Managers like Meacham are the true exception. I'm amazed how Tom Russo has managed to run his fund with as little turnover as he has. A number of his core positions have been the same for decades now.

-

Wouldn't the "little guy" be able to mimic his strategy perfectly by buying BRK stock? Haha, well I think the point he was making was for those looking to learn from Buffett on running their own investment portfolios, Buffett's success w/ Berkshire is not necessarily as relevant as studying his partnership days, as many of the contributors to BRK returns (leverage, buyouts, special deals) are not available to small investors. I think it's the same point as what others have said - it's remarkable the vehicle Buffett has created through Berkshire, in particular its ability to earn high returns despite tons of capital, and within the very limited opportunity set he now has, he is doing great things - but for those of us managing tiny sums, the possibilities are so much wider that it's best to marvel at rather than try to copy what Buffett has done within his much smaller opportunity set.

-

It's a legitimate point, no doubt. The investment gurus that we base our philosophy of investing on and look to for advice are themselves biased by having lived during an unbelievable bull market. The future seems unlikely to provide returns as strong as what we have seen over the past 30 years. The key is, what can you actively do with this "hunch" to improve performance? That's the key to me and why I'm inclined to stick with micro-level investing and accepting that the macro economy will affect my investments in some way.

-

Well, that's the case with anyone who is a value investor, isn't it? One of the core principles of value investing is to focus on micro factors and ignore macro factors. Given the extreme difficulty of predicting the macro economy, this is one of the strengths of the strategy IMO.

-

It's hard to interpret the meaning of a fund made up of funds we don't know underperforming the market. I do think the idea of a fund of funds with multiple layers of fees is ridiculous. While the guy is of course just talking his own book, I do think that looking purely at the 2009-present period in order to evaluate whether a fund can beat the market is a bit unfair. U.S. equities have just killed everything else over this period, and anyone who has not been 100% long U.S. equities has likely underperformed. As an example, it seems to me that it'd be a mistake to take a view that a fund like Baupost underperforming over this period means that they will underperform across a long period of differing market conditions.

-

The idea that happiness = reality - expectations always made a lot of sense to me. Of course, one can then argue whether or not maximizing happiness is the end goal. The widespread rejection of the "Experience machine" experiment suggests it isn't. Humans are odd creatures I guess, most of us are driven to want to set challenges and pursue difficult tasks that run counter to the maximization of emotional and physical well-being.

-

Seth Klarman: What I've learned from Warren Buffett

philly value replied to tede02's topic in Berkshire Hathaway

I think Klarmans book doesn't add much to other texts on value investing, but IMO it is the best single book to read as an introduction to value philosophy. It manages to cover the core concepts as well as anyone, and also adds in tidbits on why institutional investors are likely to underperform and some examples of where one might find interesting opportunities. It also touches a bit on trading and portfolio management as well as the concept of reflexivity in stock prices, all of which I've never heard another value investor discuss. -

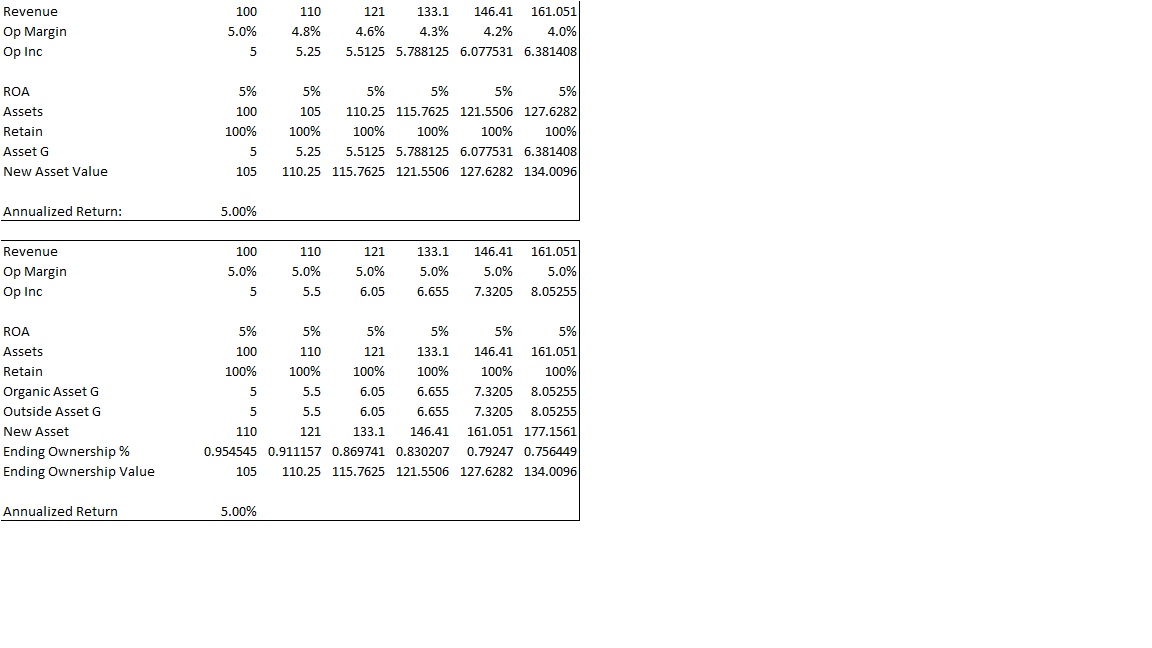

@KCLarkin: I assume by growth you mean revenue growth. If so, the answer is that both will provide the same stock return. However, unless you assume constant outside investment, the China stock is not sustainable. Forgetting ROE because leverage will complicate things, if you have a stock w/ 5% ROA and 100% reinvestment, in order to get 10% revenue growth, you need to assume that operating margins continually decline. I did this as a six year calculation, and in year 6, operating margin had been reduced to 4% from 5%. So it does not fit the requirement that margins remain the same. But you raise a really interesting point that may be applicable to the situation in China and/or other economies growing quickly. If you assume that the firm is able to raise capital equal to 5% of its beginning assets each year, you can have 10% revenue growth while holding margins fixed, and with return for the original investors remains at 5% per year. However, I think in the U.S, and in general looking at the aggregate market instead of one company, this is less important of a consideration over long time periods. If you are looking at the world stock market, then movements of capital between equities will not increase the total stock, so the question is if you anticipate capital flowing from other assets into stocks.

-

You have two companies with the following stable profiles: China Inc Growth = 10% ROE = 5% P/B = 1 America Inc Growth = 5% ROE = 10% P/B = 1 Which one will have higher total stock returns? "All else equal" means holding margins fixed.