modiva

-

Posts

95 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by modiva

-

There are any number of reasons why a stock is cheap. Fairfax Financial was trading ridiculously cheap for 5+ years. Microsoft was trading ridiculously cheap for 10+ years. Many 5-10 baggers were trading ridiculously cheap when brilliant investors picked them up. The thesis can be wrong or right, but can only be ascertained in hindsight. Therefore, it’s important to build your own thesis not blindly follow someone else’s.

-

I recently added and now have 22% of my public portfolio in FIH. I started buying 3 years ago so I am sitting around 12% IRR. I believe it is cheap, downside is limited (20-30%) but upside is big (200-300%). I’d call this as an asymmetric opportunity. The fundamentals are very strong with BIAL traffic expected to double in the next 5 years. Besides, it’s a good hedge against US markets and inflation. I am prepared to add if the price drops materially and hold for 3-5 years.

-

Gold, Fairfax India, Physical Assets (Land, Commodities). Interest rates going down (very likely) is good for physical assets.

-

+1. Congratulations to the Fairfax team and the shareholders!

-

+6% YTD. FRFHF & FFXDF (50%), Cash (28%), Gold (7%), Bitcoin (4%), remaining 11% in 4 equities.

-

Thank you @Viking for generously sharing superb insights and willing to debate. Thanks to @Parsad for creating this wonderful forum with such a group of intelligent and wise individuals. Looking forward to continued great run for all the Fairfax stakeholders!! Hoping 2025 to be a break-through year for Fairfax India.

-

The outlier events apply to any business, and so to the entire stock market. The only protection is perhaps having a % in safe assets like cash/gold/treasuries. Although, today’s safe asset might turn out to be unsafe tomorrow. @Parsad @Viking what are your safe assets today and what % of portfolio do you generally keep in them?

-

Thanks @Parsad! Greatly appreciate your thoughtful insights and risks to be aware of.

-

@Parsad @Castanza thanks for sharing your perspectives! I needed to add a caveat to my statement. Fairfax Financials and Fairfax India make up 55% of my portfolio (35% and 20% respectively). My goal is to keep it to around 50% for long time, as long as three conditions are met: 1) The investment thesis doesn't change. Long-term market and company fundamentals, differentiators such as culture, >15% growth 2) Do not exceed any single business sizing to go above 30%, ideally 25%. I view Fairfax Financials and Fairfax India as two different businesses. 3) Stock doesn't get too expensive or too cheap. Consider reducing if it gets too expensive and adding if it gets too cheap, as long as the first two points holds good. What is expensive or cheap can be subjective and varies from one investor to another. I am comfortable with the stock price range: 1x (cheap) - 1.5x (expensive) of book value. Based on the estimated book value for 2024 end ~USD 1100, I am comfortable with making no changes to my portfolio as long as the stock ranges within $1100-$1600 in the next year; and adjust these numbers and review hypothesis every quarter. It's not easy to find undervalued businesses that have strong investment hypothesis as above. All I need is to identify 1 such business in a year but I struggle. 80% of my portfolio is in Fairfax Financials, Fairfax India, Berkshire, and Cash/Gold.

-

Fairfax Financials and Fairfax India make up 55% of my portfolio (35% and 20% respectively). My goal is to keep it to around 50% for long time.

-

That’s what I just did. It didn’t work out yet for early investors…but the odds are in favor of recent investors. It may take a few years for the upside to pan out but the downside is limited.

-

That’s great! Congrats to you and to your daughters for getting into the investment world at a young age guided by their dad!! It can’t get better than that.

-

Thanks @Viking for generously sharing excellent insights, very much appreciated!

-

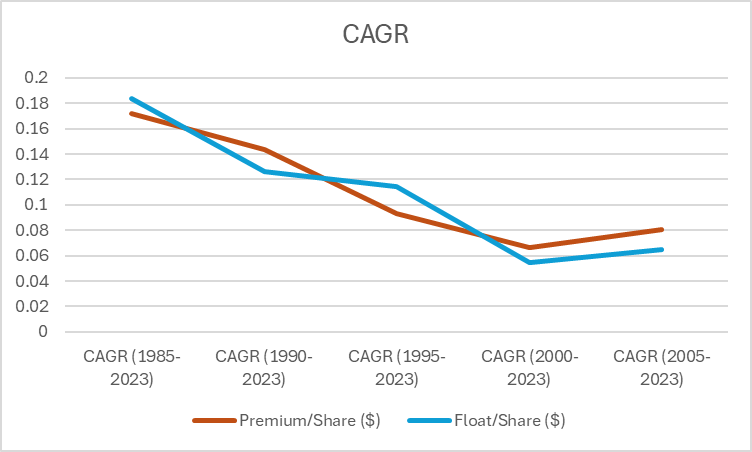

@Viking Thanks for very insightful analysis. While I agree with all of your points, I think the CAGR since inception is misleading metric to look at. What do I mean? If we remove the first 5, 10, 15 years, it is very clear that the numbers don't look stellar but rather average. The low starting point gives a high boost, but once we normalize it, the numbers look average. For example, the float/share since 1985 grew at 18.4% compounded, the growth rate reduces dramatically once we exclude the initial years. The float/share since 1995 grew at 11.4%, and since 2000 grew at just 5.5%. Disclosure: I have 35% of my portfolio in Fairfax, and 15% in Fairfax India.

-

Thank you @Parsad for the commentary!

-

I have 30% weight in Fairfax India with an average cost of $11.5 and an average duration of 18 months. I intend to hold for long as long as the book value is growing every year and no major change in thesis.

-

I am investing in a private oil field in Texas, which has proven quality reserves with reliable monthly distributions, long-term attractive returns and significant upside potential. If anyone is interested to learn and/or participate, I am happy to share details. Please ping me privately.

-

Phenomenal results and outlook. Congrats to all the longs!

-

Thanks Viking and everyone for sharing notes. I couldn't come there in person and had to settle for live webcast which I enjoyed listening to. Besides all the things about strategy, numbers, market etc. I am impressed by their culture. How they treat their people, how they don't do layoffs, the long tenure of the leaders, and importantly how they sustain their culture across geographies and acquisitions. Culture is #1 determinant of long-term scale and success, and their success in this area further reinforces long-term conviction in Fairfax for me.

-

I like Epsilon and have 5% position. No debt. High Cash (about 35% of market cap is cash). Hedged till October (sell gas at high prices). They could buy back all their shares with current cash and 2 years of earnings (Assuming earnings remain same as the last year).

-

Fairfax and Fairfax India (50), Cash (30), remaining in BRK, PXD, EPSN, BAC, CME

-

Correct. By ownership, they have the right to develop and monetize the land. Higher value of the land translates to higher cash flow.

-

Fairfax India has ownership in 460 acres of land near the airport through BIAL. BIAL is currently valued at $2.6B based on discounted cashflow. The land alone could be valued at $0.5-1B, and potentially $2B once it is fully developed. This is based on retail lot pricing and commercial value is generally higher. Based on the current developments such as the 3D Tech Printing Facility, Taj luxury resort, Concert etc., and the vision for luxury retail, business parks, community etc. the value is reasonable. Basically, the land alone makes up 20-40% of current value and 80% of future value.

-

Agreed. For comparison, Fairfax's net debt is twice that of Berkshire's. Fairfax's net debt is ~35% of book, while Berkshire's is ~18% book. Total debt to book is 43% and 25% respectively.

-

BAC, EPSN, add to Fairfax