sleepydragon

-

Posts

2,315 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by sleepydragon

-

Which is the better stock to purchase today: JPM or BAC?

sleepydragon replied to Viking's topic in General Discussion

I think WFC is much better than JPM and certainly BAC. JPM and BAC has much higher personnel cost due to their investment banking business. On the traditional lending side, WFC has more foot soldiers and do give more attentions to customers. When I applied for mortgage for my house, I had better experience with WFC compared to BAC. I think BAC's checking and online investments are better deal than WFC for retail customers, but WFC is definitely more aggressive in trying to lead me money. -

I use American Express Servo card. it's a pre-paid charge card. There's no point, but I believe using it will save you much more than what you would get with other 3% cash back cards. The reason is: You have to put money in the account before you can spend it. Each day you can at most fund it with $200 from a credit card (unlimited from a checking account). This is similar to when you are using cash, where you are actively keep tracking mentally how much you are spending. Using the card will dramatically cut down your spending. I got one for my wife. :)

-

35.65%

-

It was much cheaper when I bought Sbux Leaps in April 2009 - stock was at $10. Unfortunately, well you know.... well, about 2 years, my wife said I shall buy SBUX. She's an art major, who can't even do multiplication well, and of course have no idea about investing. I gave her a lesson about P/E and value investing and then rejected her buy recommendation.

-

SBUX is actually trading at a much reasonable PE compared to the other two stocks. It's PE (29) is not much higher than KO (~24). It's a company with great brand and growth prospect.

-

Buffett/Berkshire - general news

sleepydragon replied to fareastwarriors's topic in Berkshire Hathaway

I think it’s much more likely that she got lucky. She can’t have been the first woman to try. He may have started to realize just at that time that he needed more help for some of these things. To be fair, consider this: she was a new MBA graduate in 2009. During the summer of 2008, she had internship with Lehman Brothers, Bank of America, and 85 Broad (85 Broad is a None-profit organization founded by Women MDs/Partners at Goldman sachs). In 2008, every banks was firing people, nobody was hired. Lehman bankrupted. Yet, she got 3 jobs. And she had no real world work experience, especially in finance(before MBA, she was an undergraduate at harvard). After graduation, she got a job with Warren Buffet when I think she could be the only person in her MBA class who got a job. -

Buffett Says ‘No-Brainer’ to Get Mortgage to Short Rates

sleepydragon replied to dcollon's topic in Berkshire Hathaway

i feel the point of 30-yr mortgage is that it allows me the maximum leverage /minimal monthly payment to buy the bigger house now. Even if i would be selling the house 5 or 7 years later, it's beneficial to get 30-year loan now which allow me the maximum leverage at a low cost. If rate go higher when I buy a new house 7 years later, I can get a shorter-term loan, perhaps paying the same interest rate i am paying now, but by then I would have had more equity in the house and can pay a bigger down payment. -

they still holding blackberry, that's what I care :)

-

deere

-

how about BYD or Disca?

-

GS buy back shares because if an employee's income exceed a median level, 80% of the pay is deferred and paid in stocks. All the partners in GS are heavily in GS stock ownership, so they keep buying back. even in 2008.

-

Corner of Berkshire & Fairfax Fund - Poll Q2'14

sleepydragon replied to Ross812's topic in General Discussion

no tesla. haha. and this vote has a long bias. should allow people cast negative votes and then take the sum for each stock. you can also try long the top highest voted and short the lowest voted. but where can I vote? too late this year .. -

Corner of Berkshire & Fairfax Fund - Poll Q2'14

sleepydragon replied to Ross812's topic in General Discussion

how to vote? -

and DTV is selling below 10x pre tax earning.

-

in my opinion, spx is essentially a momentum strategy. you are always buying yesterday's winners. it will work well as economy gets better. brk is more like a strategy that benefit from short term reversions. the big four will be able to buy more stocks if the market dips, and web can buy more stocks at low. brk's company will also have large sums in capex when other companies can't invest when market is not good. it's like a version of Graham's dollar averaging method. over the long term it will surely beat the market.

-

Blackberry: Why the Shorts and Analysts Have it Wrong

sleepydragon replied to LowIQinvestor's topic in General Discussion

i agree with you. on the other hand, they are making real progress on their device business. it's a real possibility that they will stop losing money on that business. now imagine it becomes even slightly cash flow positive, then bbry become a very interesting company with these other optionalities. how much will you value it at at that time, for a company with a good brand, a lot of cash, proven new management, growing again, etc... valuation will still be expensive. but it would have changed from a distressed company to growth company again. An example was LVS when it was at 4 dollars. -

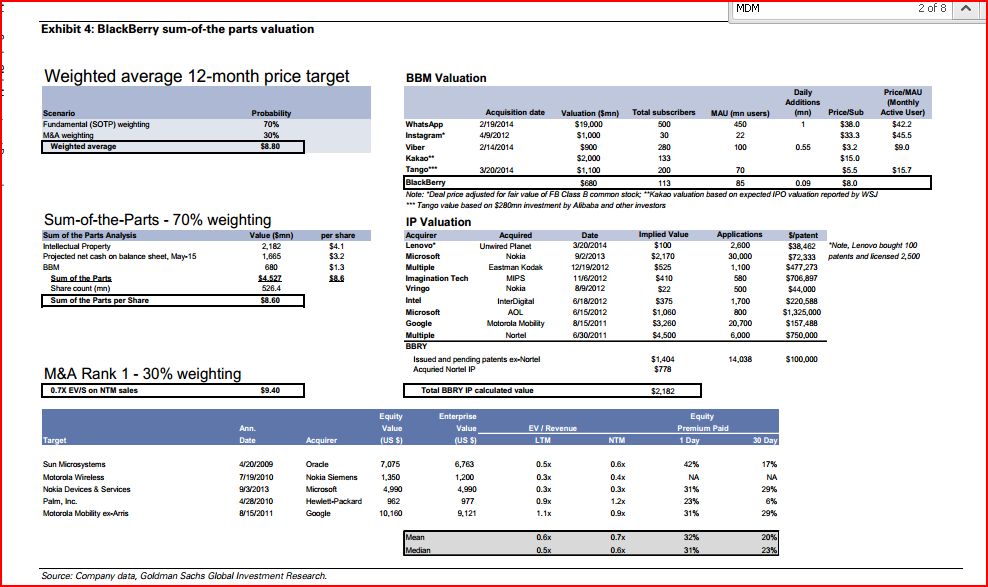

Blackberry: Why the Shorts and Analysts Have it Wrong

sleepydragon replied to LowIQinvestor's topic in General Discussion

Good to hear! I am long blackberry since john chen joined. I think their MDM revenue is not much yet. It's a new source of revenue - estimated at only 65m by Goldman's research (attached). According to GS's sum-of-parts (attached), it's worth $8.60. However, they didn't count the MDM and QNX. I am not sure about MDM, but I know QNX is comparable to Wind Rivers Systems' vxWorks operating systems. Intel bought Wind Rivers Systems for $889mn in 2009. They currently have 2.5+ billion cash. Sure, they got 1b+ debts. but it's only 5% interest and is not dilutive until Fairfax converts (when that happens, the stock will be a lot higher). They could sell more assets like patents or BBM. Use that money to buy another company or get more revenue. They are on track to make their device division to stop draining cash by partnering with Foxconn. Market cap is only 4.3bn. They could also be bought too -- by, say SYMC. SYMC is dying due to PC. it will be great if SYMC can break into mobile security by buying BBRY.