LC

-

Posts

8,237 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by LC

-

25% tariffs on Canadian and Mexican imports.

LC replied to SharperDingaan's topic in General Discussion

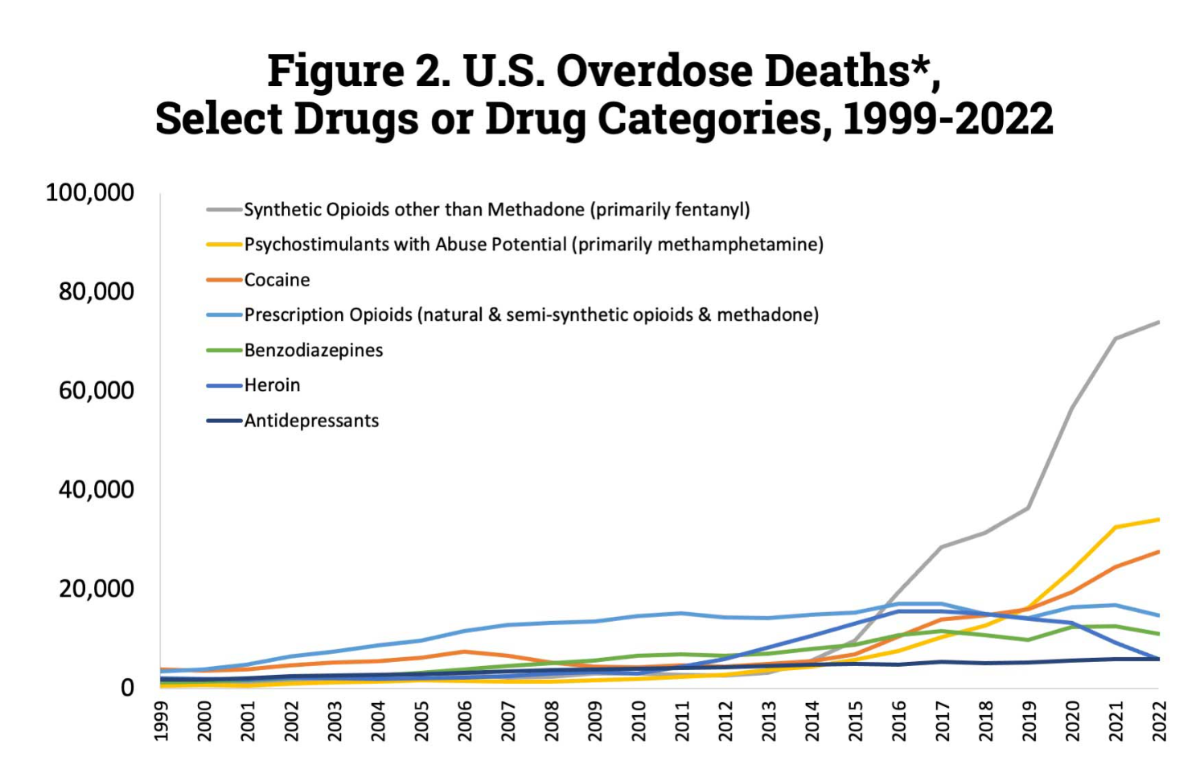

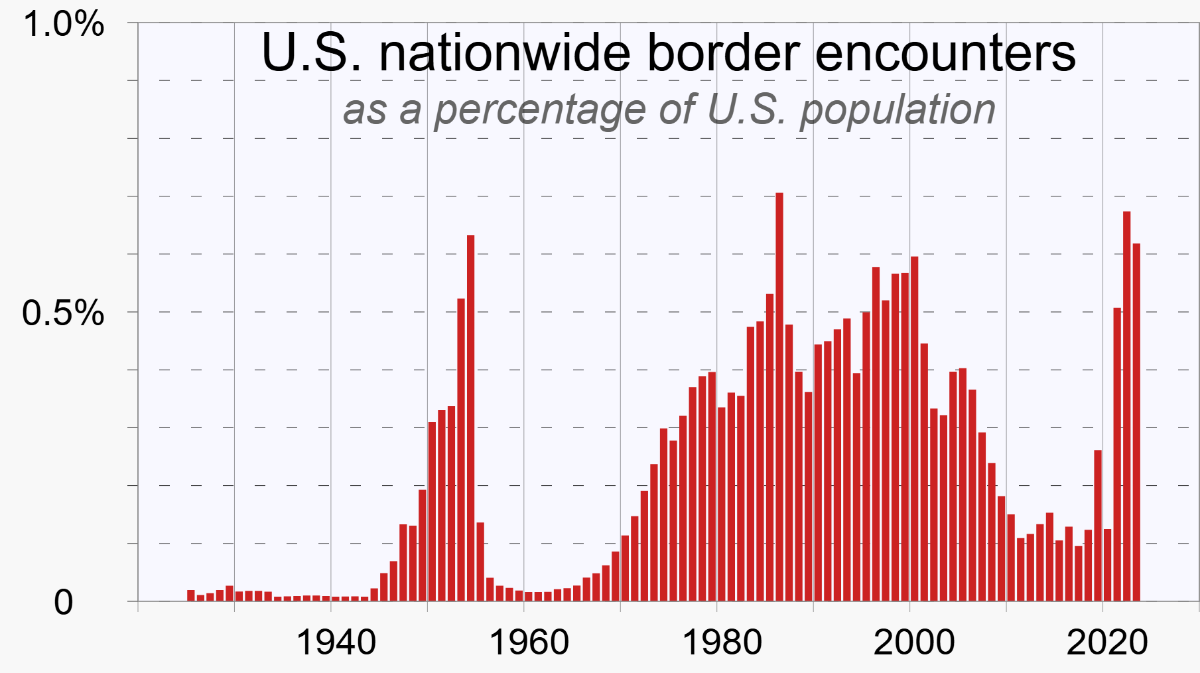

To be fair I just quoted your post, not sure what I distorted. But I don't see how Trump's 1st term was a fentanyl success. Looks like that's when it started taking off. Nor do I see his actions having any impact on border incidents. Instead it looks like the trend beginning 2010 maintained thru 2019. Maybe we should be thanking Obama instead

-

25% tariffs on Canadian and Mexican imports.

LC replied to SharperDingaan's topic in General Discussion

Tariffs are going to stop illegal drugs, sex trafficking, and illegal immigration. Remember when Nixon imposed 10% tariffs across the board in the 70s, and it totally solved the War on Drugs? Yeahhhhhhh.... -

I recently sold my UMG swing trade - 22->27 or so. I think it's a good business but the stock performance never seems to reflect this. On Airbnb, what do you make of VRBO? It is owned by Expedia, valued at 20B vs. 80B for ABNB. Slightly less of a disparity on an EV basis (41b vs. ~93b) Expedia has other assets as well (hotels.com, trivago, etc. etc.)

-

Thanks, I had a good laugh at that one

-

Insurance is a pretty great business to be in - it gets all these free benefits from human nature. People see all these headlines about catastrophes the past few years, with big total loss numbers...it triggers some part of human nature to say, sure it's OK to spend X on insurance. Not to mention the news media loves to report on doom & gloom, further putting the message in front of people. And then once you buy insurance, it's only purchases you make that you work to actively avoid using. So you've got human nature, the media, society-at-large...all working to support your volume and pricing. And then you've got the individual policyholders all working to help keep your loss ratios down. Sure there is competition, but everyone really rises when the tide comes in.

-

Money - I've outperformed the SP500 by 15-25 points, at least each of the last 4 years. Further back too but I don't have the figured offhand. It gives me something to do, and I get to help friends and family. Plus I don't like to just buy an index. I want to know what I am buying, and I want a good price. That wrests some control over the outcome away from Mr. Market. And I don't think the odds are stacked against small investors. Yes 50% of all active management will underperform by definition - but think about that in terms of dollars. The US market is 60 trillion. Add in Canada, Europe, China etc. Call it 100 trillion total. A guy with a few million has a lot of advantages - you've just got to be on the right side of 50 trillion. That seems achievable considering we're not trying to move billions or even hundreds of millions.

-

The proceeds. If I made as much money from skiing or hiking or fishing or travelling smoking drinking eating etc...I would do that instead, in a heartbeat.

-

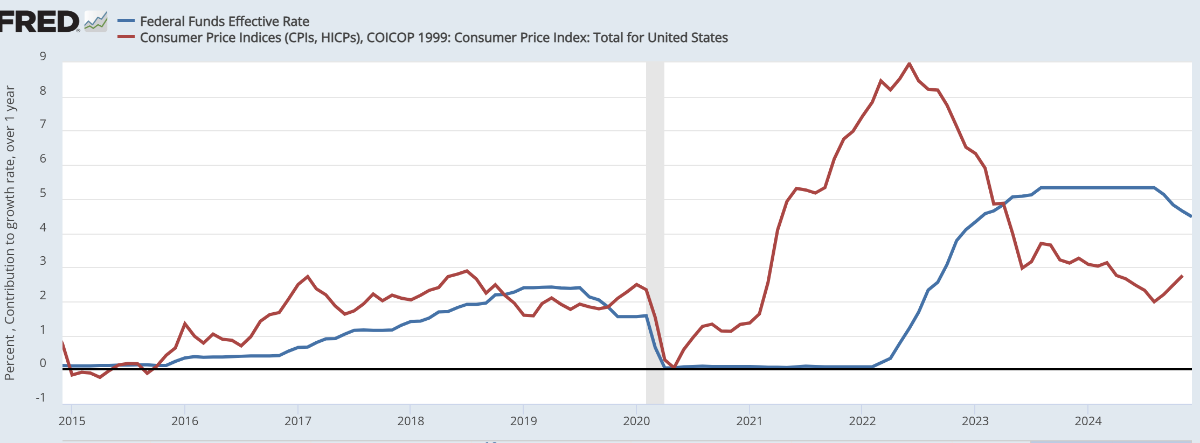

Which is the leading indicator here? Is it that inflation eventually migrates to the fed funds rate, or does the fed set its rates to manage existing inflation? How do you reconcile this statement with the inflation diverging from fed rates during COVID? Obviously inflation caused by idiosyncratic factors -> but the FRB then comes in behind and raises rates to meet inflation.

-

Barring some disability, I think people are generally good at what they focus on. Maybe we just focus on the wrong thing?

-

Fair enough - I too had a similar cost basis but sold in the 15s. And I have been waiting to re-enter in the 12/13 range but it will probably not happen.

-

Really think it is fully valued even at 18?

-

Ultimately these are PD/LGD/EAD models - similar to credit scoring but also include some valuation component of the underlying real estate during various scenarios (HPI down 5%, 10%, etc.). We also bake in a haircut to liquidate.

-

There are a variety of factors - for the US market blackrock built an incredible model that took macro factors, and applied them at the zip code and zoning level...for the entire country. was a massive model and very detailed. it was used to model potential losses on ABS products. For Korea it was again for modelling losses under various economic circumstances at the overall portfolio level. If I have some time tomorrow I will try and dig up the documentation. But it was the most difficult portfolio to model because historical losses were so low. And it's difficult to sell "yeah we expect 0.0005% losses in cases where the country GDP drops 20% (or whatever)". So we took the nearest/most similar countries historical behavior (default rates, valuations etc.) as a proxy. And we hired some dudes from SK to provide some local color. Their words were "it is very, very disgraceful to default on your home in SK. you do not do it". We sold the portfolio soon after so didn't really look into that to see if it was true, hence my tongue in cheek comment.

-

I own a little Kyoto financial. I should’ve just bought Nintendo. korean real estate DOES. NOT. DEFAULT. not sure why but ages ago we were tasked with modeling Korean secured defaults. Had like 500k defaults on a 5b+ portfolio. Korean real estate DOES. Not default! (Take this with a grain of salt, this was 10+ years ago)

-

I figured you would get at least a chuckle out of it I mean, that's a matter of debate. And different people value different things. I think there are issues on both sides - neither is perfect. What I think we can both agree on is that nobody can say that they didn't get what they asked for. If people in the US complain about homelessness etc. - well why did you vote for Trump? If people in the EU complain they can't build individual wealth - well why are you voting for semi-socialists?

-

Do your own research and prove me wrong. Assuming you won't, allow me to draw the logical conclusions for you: So based on your dismissive comment, post-ACA, medical debt is no longer a leading cause of bankruptcy. Therefore the ACA reduced total bankruptcies caused by medical debt, from 62% to some much lower amount. The ACA, being a European/socialist inspired piece of regulation, has therefore saved hundreds of thousands of people each year from bankruptcy. I look forward to seeing your posts on how European regulations save millions from bankruptcy due to medical debt.

-

Outdated info but this is what 4 minutes of google searching produced: The article by Himmelstein et al1 in this issue of the The American Journal of Medicine documents that health care expenses were the most common cause of bankruptcy in the United States in 2007, accounting for 62% of US bankruptcies compared with 8% in 1981.2 Most bankruptcies occurred in middle-class citizens with health insurance, further evidence that our current health care system, based on for-profit, employment-based health insurance, is not working. Millions of Americans have limited access to health care because they cannot afford health insurance. Millions of others, such as those who have to file for bankruptcy because of health care costs, have inadequate health insurance. It is estimated that 1 in 5 Americans goes without health insurance or has inadequate health insurance.3

-

No I disagree. I think Fairfax has a complex business structure and it is not clear where growth will come from. And partly I think it should trade at a lower multiple for that reason. (Disclosure FFH is still like 35-40% of my portfolio) A big portion of the earnings growth in the past few years has come from expertly trading the bond portfolio. The second largest portion has been from the extension of the insurance hard market. The third largest portion has been growth and valuation expansion in its underlying investments. Now, at best it is a difficult exercise to gain confidence that those three avenues of growth will continue. The bond portfolio: If rates fall, they can sell and realize some gains. But then they will be subject to reinvestment risk. If rates stay the same, the only place growth can come from is increasing the portfolio size. More on that below. Insurance/Primary LOB: Does anyone know when a hard market will/will not end? I don't think so. I believe management is already allocating capital by buying-out minority partners, rather than writing more business. So management probably thinks the hard market is slowing. This also has the effect of slowing growth in the size of the bond portfolio, since they are not bringing in more premiums. So you have factors slowing growth in their two primary income drivers. Underlying investments: There are many diverse investments, they are small in size, and this is not Fairfax's primary business. Prem has a spotty record here. This is the classic conglomerate discount. In other words, if Prem et al cannot clearly state where growth will come from, why should this trade at a premium?

-

I agree with this. I think he could've lowered earlier too, but being like 3-6 months late to the party is not a knock against him. Frankly you could argue he took an appropriately conservative path. Right from wikipedia, his job is to: Congress established three key objectives for monetary policy in the Federal Reserve Act: maximizing employment, stabilizing prices, and moderating long-term interest rates 4.1% unemployment is pretty freaking low. Inflation reads have stabilized. The 10-year is pretty moderate at 4.6% and he has been lowering. Not sure what more I can expect from the guy.

-

Most economic theory and business experience would suggest not to expect long term underwriting profitability for the industry as a whole. Large scale insurance is a commodity business, pricing is transparent, and there are many sophisticated participants. Maybe a continued string of catastrophes (Los Angeles for example) will help sustain pricing in the near term. And maybe some thesis is that climate change will create an upward shift in catastrophe frequency and/or severity. Not sure that is really knowable, however. The other long thesis is regulatory capture, which could limit entrants and protect pricing. I don't know much about that as it's state-level, I take folks like Buffett at their word when they talk about insurance industry dynamics.

-

Oh c'mon! Don't leave us hanging, buddy!

-

I think it's an underrated point. Keeping COVID gains during 2022 (IIRC I broke even - congrats on a great 2022 for you!) solidified some life changes for me. And then being able to dump a lot of that into Fairfax - worked out very well. Matching performance or outperforming during good years is of course the goal, but to extend a popular analogy - holding onto your pants when the tide pulls out is how you build wealth.

-

It was - Berkshire (my value market indicator) at what like 170? Such a skewed risk reward. Either the world falls apart or it doesn't. Just bet everything but the house on the world not falling apart. Leaps on everything. Should've bet the house too, not like the bank could've come to repossess it without getting within 6ft

-

25% tariffs on Canadian and Mexican imports.

LC replied to SharperDingaan's topic in General Discussion

Stumpy should be talking about taxing Russian and Chinese goods - the mutual antagonists of US and CA. In my experience a lot of Americans casually dismiss Canada, because they are ignorant of our shared history. I still wear my Poppy every year! -

We threw our wedding party in prospect park - no permit (what permit?), informally catered by about 6 nyc restaurants that to this day still crush it. A never-forgotten shout out to venerio's for the best cheesecake in the city. The sister- and father- in law hauling catering size portions of food all over brooklyn via the B & Q. Did the ceremony right past a pedestrian tunnel (this one, in fact) leading to the boathouse. Weather was perfect. Musical accompaniment as provided by the busker sitting in the tunnel with a saxaphone (tipped generously). A random group of 4 firefighters, in uniform, did us a solid by holding back passer-bys for the big moment. They did unfortunately turn down our best man's offer to provide nude entertainment for the party afterwards. That was a real bummer. Partied all night at a friend's brownstone a block away, kind of trashed the place right before she sold it to some author and his wife ("is it a safe neighborhood here?"). I still remember the hash circle that my old man set up with my degenerate 20-something friends in Angela's bedroom...drugs probably dug out from his tackle box from the 70s. "Gin and juice" was the drink. Thanks, Tom - next time swap out the cucumbers for fresh ones so we're not all eating gin-soaked garnish. Sweet Sarah from Corpus Cristi (bless up) who saved us plates of food. Even the Pakistani guy who ran the bodega came by with a few packs of cigs as a wedding present. At some point a 275 lb man dressed as a hipster-lumberjack and a 120 lb woman wearing a Tigger leotard swapped outfits. I do remember pulling about 50 pins out of my then-wife's hair. My neighbors gladly hosted the afterparty. A jar of coins were stolen by a gay friend who also hit on my mother all night. Gina, Sexy Pervy Mark, and Gina's John (she was (is?) a dominatrix) I believe bought us a hotel room. It's a bit hazy of a memory. Spek, we would've got you absolutely trashed