UK

-

Posts

3,440 -

Joined

-

Days Won

16

Content Type

Profiles

Forums

Events

Everything posted by UK

-

Yes, he even said IIRC, that focus was a reason for his success.

-

I think at this point it might be to late and dangerous to do with yen too (unless you have some great ideas with jpy exposure). Maybe it still could go even lower if they had some kind of currency crisis, but I have no idea how to have any conviction on this, meanwhile it seems already to cheap: https://www.economist.com/big-mac-index Instead, maybe by some wishful thinking, I have some expectations of maybe EUR becoming 'new yen', in terms of carry trade in some not too distant future.

-

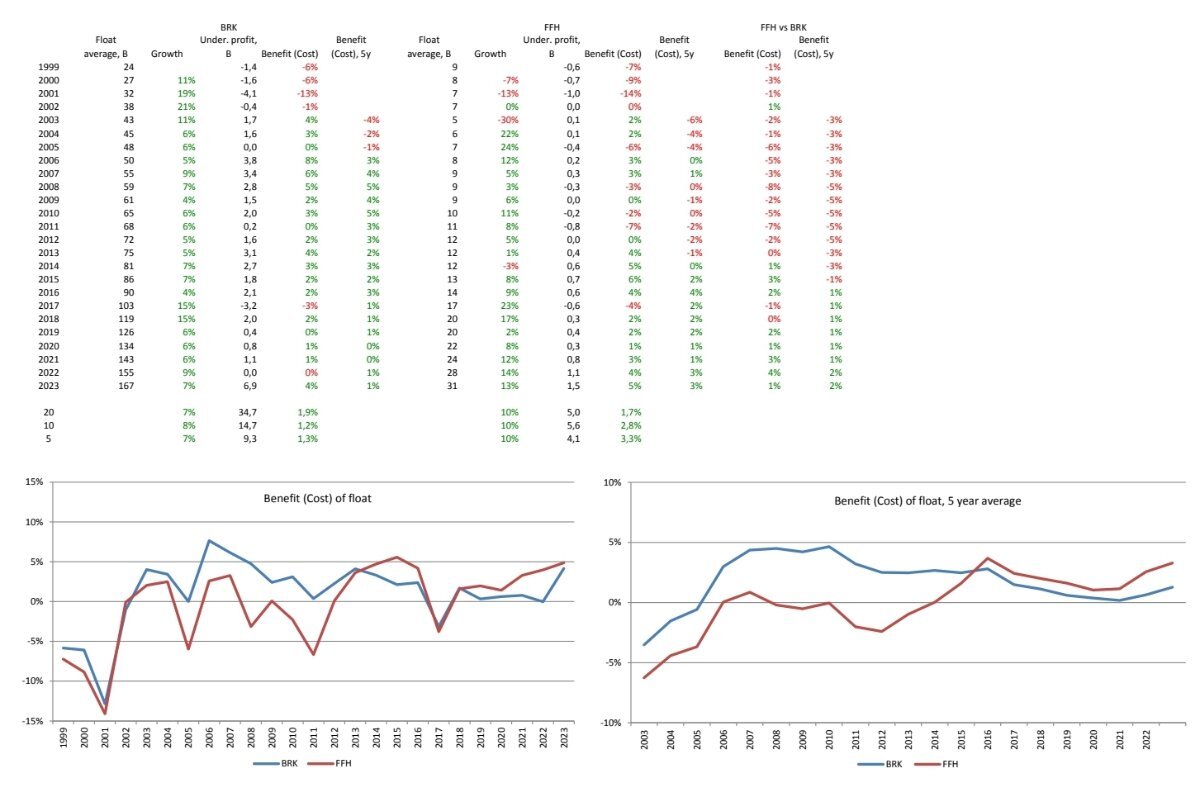

https://www.barrons.com/articles/buy-everest-group-stock-price-pick-reinsurance-cdc6637d I like FFH much better as an investment, but maybe it could be a nice "add on" acquisition for BRK?

-

https://www.google.com/amp/s/www.ukrinform.net/amp/rubric-ato/3898338-zelensky-no-sick-old-man-from-red-square-will-dictate-any-of-his-red-lines-to-ukraine-and-the-ukrainians.html "The sick old man from Red Square, who constantly threatens everyone with a red button, will not dictate any of his red lines to us. How we live, which path we take, and what choices we make will be determined only by Ukraine and Ukrainians. That is how independence works," Zelenskyy said. Zelenskyy recorded a video address from the Sumy region, near the Psel River a few kilometers from the border with Russia. "The border between an independent European state and the number-one terrorist organization in the world. 913 days ago, Russia launched a war against us, including through the Sumy region. It violated not only sovereign borders but also the limits of cruelty and common sense. Its endless goal was one thing: to destroy us. Today, however, we are celebrating Ukraine's 33rd Independence Day. What the enemy brought to our land has now returned to its own home. And those who wanted to turn our lands into a buffer zone must now consider that their country might become a buffer federation," the President said. “Ukrainians always return their debts. And the one who wished a disaster on our land will see it at own home, with interest added. Whoever wants to sow evil on our land will reap its fruits on own territory," Zelensky went on to say. Lannisters always pays their debts:)

-

I agree with you basically 100 percent. Yet I think there are a few exceptions, such as: https://covestreetcapital.com/wp-content/uploads/2015/03/Druckenmiller-_Speech.pdf

-

https://www.reuters.com/world/europe/russian-ambassador-says-us-plans-give-ukraine-carte-blanche-weapons-2024-08-23/ "I tell you sincerely that the president has made a decision," the TASS state news agency quoted Antonov as saying late on Thursday. "I am firmly convinced that everyone will be severely punished for what has happened in Kursk region." The comments by Antonov, who did not provide further details on Putin's plans, came after the Kremlin leader held a meeting on Thursday with senior officials, including the governors of border regions, over two weeks after Ukraine launched its lightning attack, the biggest incursion into Russia by a foreign power since World War Two.

-

-

What is your top 3 business/finance/investing books you've read?

UK replied to schin's topic in General Discussion

+1 -

Movies and TV shows (general recommendation thread)

UK replied to Liberty's topic in General Discussion

Why do you think it was screwed up? I thought it was quite well done, unpredictable till the end? I did not like this episode about the expedition to the north to bring the wight sample:), but what was wrong with the ending? -

What is your top 3 business/finance/investing books you've read?

UK replied to schin's topic in General Discussion

Same for me, in personal finance theme, though it is almost an embarrassment to recommend author these days:). There is also table and even PC or maybe an online game available. Very good and fun to play with kids, shows why it is sometimes harder to escape 'rat race' for a well earning doctor, than a low earning janitor:) -

https://www.reuters.com/markets/commodities/passed-peak-chinas-crude-oil-imports-trend-down-russell-2024-08-22/

-

https://www.insurancejournal.com/news/international/2024/08/15/788486.htm “Unlike previous boom and bust cycles, there are a number of factors—climate trends, an increasingly complex risk environment, and a prolonged period of higher interest rates—that make us believe these improved underwriting margins are likely to last for at least another couple of years if underwriting discipline is maintained,” said AM Best in its report titled “Strong Technical Profits Bolster Momentum for Global Reinsurers.” https://www.swissre.com/media/press-release/pr-20240822-hy-2024-press-release.html P&C Re renewed contracts with USD 4.5 billion in treaty premium volume on 1 July 2024. This represents a 7% volume increase compared with the business that was up for renewal. Overall, P&C Re achieved a price increase of 8% in this renewal round.

-

-

Re insurance/CR: as of recent still ahead of BRK (good enough for me:)).

-

All this really starting to look like the second Prigozhyn moment:). Maybe Kerch bridge will be next... https://www.washingtonpost.com/world/2024/08/16/ukraine-russia-soldiers-conscripts-kursk/ Nikolai and fellow prisoner Sergey, 19, said Ukraine attacked their military headquarters on Aug. 6 and their commanders left without giving instructions on what to do next. Fearing they would be killed if they stayed, the young men walked for three days through forests and swamps and “slept on the cold ground,” Nikolai said. While searching for safety, they came across a group of vehicles decorated with triangles — a symbol Ukraine has painted or taped on all its vehicles crossing into Russia in recent days. “I was trying to remember whether the triangle was our identification sign or not,” Nikolai said. Soon they were surrounded. Ukrainian soldiers grabbed them by the scruff of the neck, he said, checked them for weapons and then gave them food, water and cigarettes. “They came, chatted, told their stories, listened to ours,” he said. Then they tied their hands and covered their eyes and sent them over the border into Ukraine.

-

Perhaps...anyway, all this is well above my paygrade and, at least for now, it seems that because of Kursk, Russia is moving its troops from Kaliningrad and Saint Petersburg districts to Kursk, not the other way:)

-

https://www.washingtonpost.com/world/2024/08/17/kursk-ukraine-russia-energy-ceasefire/ Ukraine’s offensive derails secret efforts for partial cease-fire with Russia, officials say The warring countries were set to hold indirect talks in Qatar on an agreement to halt strikes on energy and power infrastructure, according to officials.

-

+1 Often even with their long positions they end up being too smart and are attracted by unnecessary complex things and then get burned by some important but unknown risk or development. Definitelly some character/ego problems:)

-

This would be very interesting to watch, especially from the distance far enough:). Except for the fact, that since the start of invasion there is nothing else than a constant escallation, so many red lines are being crossed and still there is no much more clarity today on the final resolution possible, then it was two years ago. Most get used to all this, but seeing British tanks driving in Kursk:), I am not against this per se, but personally I am worried at such times a bit for some unforseen concequences / more escallation.

-

https://www.reuters.com/world/kremlin-aide-says-nato-west-helped-ukraine-attack-russia-2024-08-16/ https://www.reuters.com/world/europe/russian-mp-says-ukrainian-incursion-could-lead-global-war-ria-reports-2024-08-16/

-

Interesting take: https://www.cnbc.com/video/2024/08/15/leon-cooperman-nothing-is-overvalued-with-bond-yields-where-they-are.html

-

https://tim.blog/2023/09/07/nassim-nicholas-taleb-scott-patterson/ "If you must panic, panic early"

-

https://www.cnbc.com/2024/08/15/warren-buffett-did-something-curious-with-his-apple-stock-holding.html

-

Since WB has closed his funds years ago, I am not giving my money for anyone else to manage:). But he (Kuppy) seems sometimes to have very high conviction on things and usually swings quite big. I find some of his thougts and ideas very interesting and with high variant perception. I like his thesis on JOE:). At the same time, sometimes I do not understand his writings at all, especially the macro/monetary/commodity scarcity or general "impeding doom" related. But it is not for me to understand everything and nobody is perfect, but I like to follow him.

-

https://13f.info/13f/000194987724000012/compare/000194987724000011 Also some recent 'culling' on display:)