UK

-

Posts

1,847 -

Joined

-

Days Won

14

Content Type

Profiles

Forums

Events

Posts posted by UK

-

-

-

-

China lowered the stamp duty on stock trades for the first time since 2008, marking a major attempt to restore confidence in the world’s second-largest equity market.

...

The reduction has the potential to trigger a knee-jerk rally in China’s $9.6 trillion equity market, which is highly sensitive to policy shifts that impact market liquidity. The cut is a boon for Chinese brokerages as well as quantitative hedge funds that use rapid-fire trading strategies.

...

They have also guided mutual fund managers to step up purchases of their own equity funds, cut handling fees on stock transactions and encouraged companies to step up share buybacks. China adjusted the stamp duty on stock trading several times in the past. In May 2007, it raised the rate to 0.3% to cool a rally that was drawing more than 300,000 new investors a day. In April 2008, the government slashed the levy to 0.1% to support the market after a plunge, spurring a bull run the following year.

-

Commodity exporters are especially exposed to China’s slowdown. The country guzzles almost a fifth of the world’s oil, half of its refined copper, nickel and zinc, and more than three-fifths of its iron ore. China’s property woes will mean that it requires less of such supplies. That will be a knock for countries such as Zambia, where exports of copper and other metals to China amount to 20% of gdp, and Australia, a big supplier of coal and iron (see chart 1). On August 22nd bhp, an Australian firm and the world’s biggest miner, reported its lowest annual profit in three years, and warned that China’s stimulus efforts were not producing changes on the ground.

...

Weak spots in the West include Germany (see chart 2). Faltering demand from China is one reason why the country’s economy has stagnated of late. And some Western firms are exposed through their reliance on the country for revenues. In 2021 the 200 biggest multinationals in America, Europe and Japan made 13% of their sales in China, earning $700bn. Tesla is more exposed still, making around a fifth of its sales in China; Qualcomm, a chipmaker, makes a staggering two-thirds.

...

Provided the slowdown does not escalate into full-blown crisis, the pain will remain concentrated. Sales to China account for only 4-8% of business for all listed firms in America, Europe and Japan. Exports from America, Britain, France and Spain come to 1-2% of their respective outputs. Even in Germany, with an export share of 4%, it would take China collapsing to generate a sizeable hit to its economy.

...

But what if things go badly wrong in China? Under a worst-case scenario, a property meltdown could reverberate through the world’s financial markets. A study by the Bank of England in 2018 found that a “hard landing” in China, where economic growth fell from 7% to -1%, would cause global asset prices to fall and rich-world currencies to rise as investors rushed in the direction of safer assets. Overall, British gdp would drop by 1.2%. Although most Western financial institutions have relatively little exposure to China, there are exceptions, such as hsbc and Standard Chartered, two British banks.

-

If Mr Posen is right, China is stuck. If spending is weak because households and entrepreneurs fear the party’s intrusive policymaking, their spirits will not revive until Mr Xi commits to self-restraint—a commitment that he cannot credibly make. Even if the setbacks of the past two years have chastened him, he cannot prove he will not change his mind again. The party lacks the power to limit its own power.

...

If China’s government acts with urgency, it has the tools it requires in order to engineer a recovery in the latter part of this year. But will it use them? Mr Xi lacks the credibility or focus of previous leaders. He now prizes greatness over growth, security over efficiency and resilience over comfort. He wants to fortify the economy, not gratify consumers. These competing priorities may prevent China’s rulers from doing whatever it takes to revive demand. Mr Xi no longer wants growth at all costs. And so the country has not had it. At growing cost.

-

American politicians are keener than ever to juice the economy with government cash, a shift that’s already helping to drive up borrowing costs and looks likely to keep them high long after the inflation emergency is over. The outlook for the federal budget right now is essentially unprecedented—crisis-size deficits as far as the eye can see, even though the economy appears to be in good health. That prospect is making investors uneasy, as demonstrated by yields on benchmark 10-year Treasuries climbing above 4.3% this week, their highest levels since 2007. Other borrowing costs are rising in tandem: The average rate on a 30-year fixed mortgage has surged above 7% for the first time in more than two decades.

...

In a strong economy with low unemployment, American politicians “really have no impetus to think they need to change anything,” says Oksana Aronov, head of market strategy for alternative fixed income at J.P. Morgan Asset Management. “You have a tremendous amount of fiscal spending—an unprecedented amount in non-war times. There are a lot of factors coming together to push long-end rates higher.” The consequences stretch beyond the $25 trillion Treasury market. American housing is now less affordable than at any time since the 1980s, and it will become even less so if rising yields on US government debt pull mortgage rates north of 8%. Stocks may also suffer, since higher financing costs for corporations eat into profits. “History tells us that no asset class is really going to escape this entirely,” Aronov says.

...

For all the fretting, it’s hard to map out a path that leads to a full-blown bond meltdown in the US, like the ones that threatened European economies last decade and are commonplace in emerging markets such as Argentina. Not only does the US borrow in its own currency, giving it the ability to print more money in a pinch, but Treasuries—despite what ratings firms say—still represent the strongest of global safe haven assets, which ensures that demand for them will remain robust until an attractive alternative materializes. Also, economists have been raising the alarm over the level of US debt for decades, arguably undermining their case with vague and premature warnings of doom. “It’s not clear at all that we can identify in advance a particular level of federal debt that would trigger a crisis,” says Karen Dynan, an economics professor at Harvard. “There’s no consensus among experts.”

-

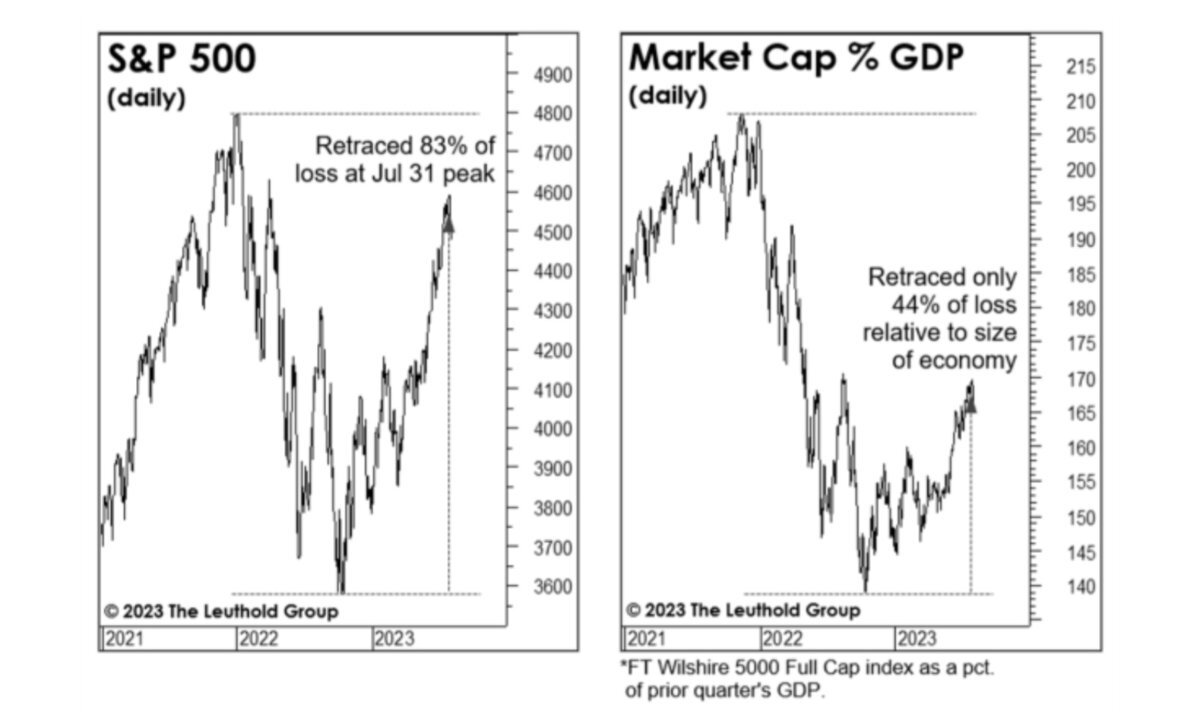

Equities rose for the first time in four weeks, with the S&P 500 now recovering roughly 65% of last year’s bear-market drop. Factor in inflation, however, and the size of the retracement is less — only about 45%, adjusting for the consumer price index. Plotting the S&P 500’s value against nominal gross domestic product shows a similarly paltry recovery compared with the size of the economy, according to data compiled by Doug Ramsey at the Leuthold Group.

-

"We expect the anti-gambling crackdown... to eliminate 20% to 70% of live streaming revenue, depending on each platform's exposure," Charlie Chai, an analyst at 86Research, said. "It should take two quarters for the impact to be fully absorbed a third in Q2, and the remaining two-thirds in Q3." In their earnings report, Tencent said it was adjusting its live streaming business to become more "music-centric" while Huya said it was working to make the platform atmosphere "healthier". Cloud Music said it was reinforcing its "internal controls mechanism... and adopting stricter monitoring over irregular user activities".

While Chinese authorities say they have ended a years-long, wide-ranging regulatory crackdown on its technology sector, scrutiny has continued as Beijing looks to rectify social and business activities in line with socialist norms. -

https://www.economist.com/leaders/2023/08/24/why-chinas-economy-wont-be-fixed

Why does the government keep making mistakes? One reason is that short-term growth is no longer the priority of the Chinese Communist Party (ccp). The signs are that Mr Xi believes China must prepare for sustained economic and, potentially, military conflict with America. Today, therefore, he emphasises China’s pursuit of national greatness, security and resilience. He is willing to make material sacrifices to achieve those goals, and to the extent he wants growth, it must be “high quality”.

-

19 hours ago, SafetyinNumbers said:

It’s not gambling, it’s just being open to the possibility given how underowned it is by Canadian funds. At the beginning of 1995, I probably would have sold at 1.5x BV and missed the 6x in 4 years as the multiple expanded to 3x while the ROE was “only” 20%/year. History may not repeat but it could rhyme.Who knows, given FFH liquidity...maybe also if we somehow move all good information available here to reddit forums:)))

-

8 minutes ago, Spekulatius said:

@UK Investors are supposed to act like aimless flies and not like a beehive where a queen controls everything. I guess Li Bei does not believe in Adam Smith.

I agree and I took no offence after reading this:)

-

1 hour ago, Parsad said:

At today's prices, if I liquidate FFH, even with higher fair value prices for the insurance subs, I might get 1-1.2 times book after paying off the debt...at best!

If I liquidated Macy's today, just the store in Herald Square alone is worth more than the entire company. So forget the retail brick and mortar business, forget the online Macy's business, forget Bloomingdales, forget BlueMercury. Just selling the real estate will pay off the debt and get me what the market value of the company is.

Then if you look at it from a P/E basis...at current prices, I would get my money back from FFH in 8-10 years...whereas even with the lower earnings for this quarter as they liquidated 10% of their inventory, Macy's would give me my money back in 4-5 years.

I don't need Macy's to hit it out of the park. I just need Macy's to keep up with its peer group. If it can do that over the next couple of years, the market at some point will revalue it back up to around 10-12 times earnings. And if they manage to get a double, then it might get valued at 13-15 times earnings.

And what's the worst that could happen to Macy's in the next few years? Another pandemic? Tougher competition? Reduced consumption? They've plowed through all of that before.

I'm by no means saying people should sell Fairfax and buy Macy's. 25% of my portfolio is still Fairfax. But I'm certainly comfortable buying a chunk of Macy's based on P/E and liquidation value. I think it will return to fair value just like META did at some point.

Cheers!

Thank you for the answer! I will try to read and think about this more.

But a. FFH is trading more like at 5-6 PE vs M at 4-5 next year earnings and I think that visibility of normalized earnings into next 2-3 years is much better at FFH? So isn't this valuation difference much smaller? b. to what could happen, well I do not anticipate this, but if there is a big recession or spending slowdown in the next 2-3 years, retail business could suffer (at least short term and btw M has more than 2x EBITDA net debt), while insurance (at least in terms of demand etc) would still be fine?

And then, if you look at these two in terms of buy and forget, it is not even close? Meaning insurance as a business will hardly face any disruptions, here it is also operated by owner etc, while M is kinda the opposite, no?

-

A top Chinese hedge fund has blamed foreign investors for sinking the stock market. Li Bei, founder of Shanghai Banxia Investment Management Center, said in an article posted on social media platform WeChat that overseas investors have stirred up market volatility and, “taken together, they are a bunch of aimless flies.”

-

33 minutes ago, Haryana said:

The glorification of the War of 1812 happened just 10 years ago and a resurgent Trump could retrample NAFTA and NATO.

I agree, the thing with NATO could be really scary, especially for me:). But how it would improve relations between India and China? Really I do not have any idea how to foresee such things and more importantly how to profit from them, even if forecast is right. All I see is really attractive opportunity on a micro level with Tencent via Prosus, but just think (or am afraid) at this time it is to difficult to make such investment, especially in larger size, due too all this geopolitical/political issues, which are still not going to the right direction, to say the least. I hope this will change.

-

5 minutes ago, Haryana said:

Conflicts and cooperation will continue in cycles. Even the most cuddly neighbours of the world, Canada and USA have had recent moments of intensity during the lumber dispute and the rewrite of NAFTA by Trump. Not to mention the glorification of the War of 1812 by the Harper government when the great Canadian warriors burnt down the White House to black soot.

Sure, but this happened more than 200 years ago, I agree, that things could change with India and China too, but I do not have such a long horizon:).

-

4 hours ago, Haryana said:

India has discouraged its companies from trading with — and investing in — China, banned some mobile phone applications developed by its neighbor and cut back on the issuing of visas to Chinese nationals. The border dispute has eroded India’s trust in China and undermined public and political will to maintain relations, India’s National Security Adviser Ajit Doval told his Chinese counterpart and Foreign Minister Wang Yi on the sidelines of a BRICS meeting in July, according to a Ministry of External Affairs statement.

-

On 8/23/2023 at 10:05 PM, Parsad said:

This is just too much work! I would rather wait for something else to get dirt cheap and just buy that. Structural changes could lead to higher returns and justify a higher valuation, but this starts to get into "six-foot, seven-foot hurdle" territory. I have no advantage and my estimate of margin of safety could be VERY wrong! Cheers!

Not to derail the thread, but since I recently tried to look at it: does M seems somehow a lower hurdle for you vs FFH, even at current prices? I may be very wrong on M, no strong opinion on it, but especially for a big and surer bet, I actually think it is the opposite, meaning why even bother with M, if FFH is still so cheap?*

*initially was questioning something similar about META vs GOOG a year ago:)

-

Three years ago, China cracked down on a booming real estate sector to reduce risk and make homes more affordable—part of President Xi Jinping’s “common prosperity” drive.

Beijing may have gone too far, it now seems. Country Garden Holdings Co., a developer that was once a pillar of the industry, is on the verge of default, suggesting no company is too big to fail. There are signs the situation is spiraling, too. More developers are on the brink, home prices are collapsing in smaller cities, and fears of contagion have spread to the nation’s $60 trillion financial system. When shadow bank Zhongrong International Trust Co. missed payments on dozens of high-yield investment products this month, investors protested outside its headquarters in the Chinese capital.

“Property booms and busts are typically extreme but especially in China’s case,” says George Magnus, author of Red Flags: Why Xi’s China Is in Jeopardy. “The sector is so big in relation to the economy and so significant in terms of household savings and confidence.”

...

While the property woes have spread to China’s giant commercial banks—the amount of soured real estate loans at the 10 biggest lenders will likely soar to $120 billion next year assuming the rate of nonperforming loans triples from 2022, according to Bloomberg Intelligence—the bigger concern is falling home prices. Official statistics show a steady drip of monthly declines of less than 1%; reports on the ground from agents show drops of 15% or more in some areas over the last two years. Even though it helps Beijing’s affordability push, the dropping home values have shattered consumer confidence. After years of price gains, Chinese consumers had come to see real estate as a can’t-miss investment, prompting some to buy multiple apartments to profit from the rally. For those who borrowed to do so, paying their expensive mortgages will make less and less sense the lower property values go.

...

“With luck, and robust policymaking, China might transition to a less real-estate-dependent economy in the coming decade,” says Red Flags author Magnus. “But it could also be a very messy process and entail financial instability and economic and social disruption.”

-

1

1

-

-

But these fixes were not Beijing’s first choice. It set in motion a plan before the pandemic to inject state-owned assets into the companies and permit them to enter new business areas to generate enough cash to service debt on their own. This was known as the “market-oriented transformation” model.

...

For example, Guizhou province is home to some of the country’s most financially strained LGFVs, yet owns the country’s second-largest company by market value: liquor producer Kweichow Moutai Co., worth about 2.23 trillion yuan. The company was pressured into buying a stake in a local road-building LGFV when it ran into financial trouble in 2020. Moutai shareholders, which include investment funds and retail investors, were not happy, and have resisted further cash injections.

-

-

-

7 hours ago, Luca said:

Xi is not an idiot that doesnt understand markets and capitalism and basically wants to clone Mao now.

https://www.wsj.com/articles/xi-jinping-putin-china-russia-relations-11671030896

“I have a similar personality to yours,” Mr. Xi told Mr. Putin during his visit to Moscow.

https://www.nytimes.com/2023/08/15/opinion/china-russia-dictators-xi-putin.html

Aging dictators have less time to reshape the world — and more memories of being obeyed at home and dissed abroad for their conduct. They become increasingly repressive and aggressive as power goes to their heads. Surrounded by sycophants, they make disastrous decisions again and again. They start pondering their legacies and wondering why they haven’t received the global respect they think they deserve or achieved the glory that would etch their names among history’s greats. They may decide that they don’t want to go down as a merely transitional figure. It’s a combustible combination: an autocrat who is overconfident and aggrieved and in a hurry.

-

1 hour ago, jfan said:

The Insurance Market Cycle: Hard Versus Soft Markets - Cottingham & Butler (cottinghambutler.com)

I understand your thought process here about the cyclical nature of the insurance business as well as interest rates affecting it. It would be lovely to have a hard market that last as long as the recent soft market. I certainly can come up with a narrative that interest rates will likely remain higher for longer vs returning back to their lows over the past decade. With many insurance companies mal-positioned over the past decade (in terms of their investment portfolio), how many of them will have the capacity to write more policies, or raise capital at attractive valuations to do so? Furthermore, with higher interest rates, will alternative sources of capital (eg private equity) have increasing difficulties raising funds effectively to buy these poorly performing insurance companies?

Am I way off base if I assume that the average hard market typically last 4 years? And if this one started in 2018, the cycle should have moderated at this stage and more premium growth unlikely to persist? If the above narrative plays out, how much longer could a semi-hard market last? one? two? more years?

This is very interesting info, thanks! As I think about all this, I am coming to maybe such conclusions: a. insurance cycle impossible to predict over longer term, but it is unlikely to remain always beneficial, however b. even with underwriting results at zero, FFH is still cheap, and c. as with other important things (investments etc), when insurance cycle turns negative, the extent of negative consequences will also depend on what decisions FFH will take and how they will execute, and I think there is some basis for optimism here, looking at how they managed everything in the last 5 years?

-

6 hours ago, Viking said:

@StubbleJumper My point with the PE in my post was to highlight that it is absurdly low for Fairfax right now. Fairfax's stock price today of $828 makes sense if Fairfax was earning about $80 per year (and assuming earnings grow modestly in the future). It is a well run P&C insurer so trading at a PE of 10 is hardly an aggressive multiple to attach.

My current estimate is Fairfax will earn $160 this year. And with slightly conservative assumptions, earnings will grow in 2024 and 2025. That is not in the same universe as $80 in earnings.

So a buyer of Fairfax's stock today at $828 is getting $80 in estimated 2023 earnings for free ($160-$80). That is one hell of a discount for something that might or might not happen in 2026 or later. It doesn't make any rational sense. It is too large.

Yes, my earnings estimate for 2023 might be a little high. And it also might be a little low. We are almost 8 months through the year.

My thesis is investors are way underestimating what a 'normalized' amount of earnings is for Fairfax today. Yes, the future is uncertain. There are risks. But there are also opportunities. Some income streams will face headwinds. At the same time other income streams will experience tailwinds.

Viking, again, thank you very much for sharing your work and thoughts!

It is really almost impossible anything to add to it, but one thing, I am not sure if really you assumptions could be called "slightly conservative". I do not think at all that you have to be conservative or that these numbers are impossible, or that there could not be further positive upsides or surprises etc, but incorporating CR of 96 or less for longer term, I think is quite optimistic (possible but not sure if probable). Regardless I agree very much with your general thinking and however you look at FFH today (or even at CR 98 or 100), either on absolute or on relative, it is still to cheap and you still do not need scales to see if patient is way too fat here:). I also like very much that FFH (as also BRK but with lesser degree) is very well positioned if rates will stay higher/normal for longer or ever. But most importantly, it finally seems that at this stage, in order for them to do really well, say to earn their 15 per cent target for longer term, all they have to do is just not to do anything really stupid, to paraphrase Munger:). And if they will do something clever, as they did many times in different areas in recent 5 years, then even better! Given that, I do not understand how it is not selling at least 1.2-1.3 BV already and would not be shocked to see them trade at some 1.5 BV in mid term and my plan is just to hold it. Unless something really stupid is done, but I do not expect this at all:)

Russia-Ukrainian War

in General Discussion

Posted

Hey, this supposed to be funny:). Anyone?

Question: what was the largest city taken over by Russia in it's war in Ukraine so far?