UK

-

Posts

1,847 -

Joined

-

Days Won

14

Content Type

Profiles

Forums

Events

Posts posted by UK

-

-

4 hours ago, Viking said:

2.) combined ratio = 93.9. This was an elevated quarter for catastrophe losses… so this is a very good result. What happened? “…prudent expense management and decreased catastrophe losses.” Reading that in a Fairfax press release is music to my ears. Fairfax said they were decreasing Brit’s exposure to catastrophes and it appears we are seeing the benefits of this play out (probably company wide). My thesis is Fairfax has been slowly improving the quality of their insurance businesses for the last decade (under Andy Barnard’s leadership) and results this quarter support this idea. And how about Allied World’s CR of 91%… this sub looks like it has supplanted Odyssey as Fairfax’s top performing insurance sub.

Thanks Viking! The underwriting results, which was my biggest worry (as usual:)), are just awesome, especially while considering context!

-

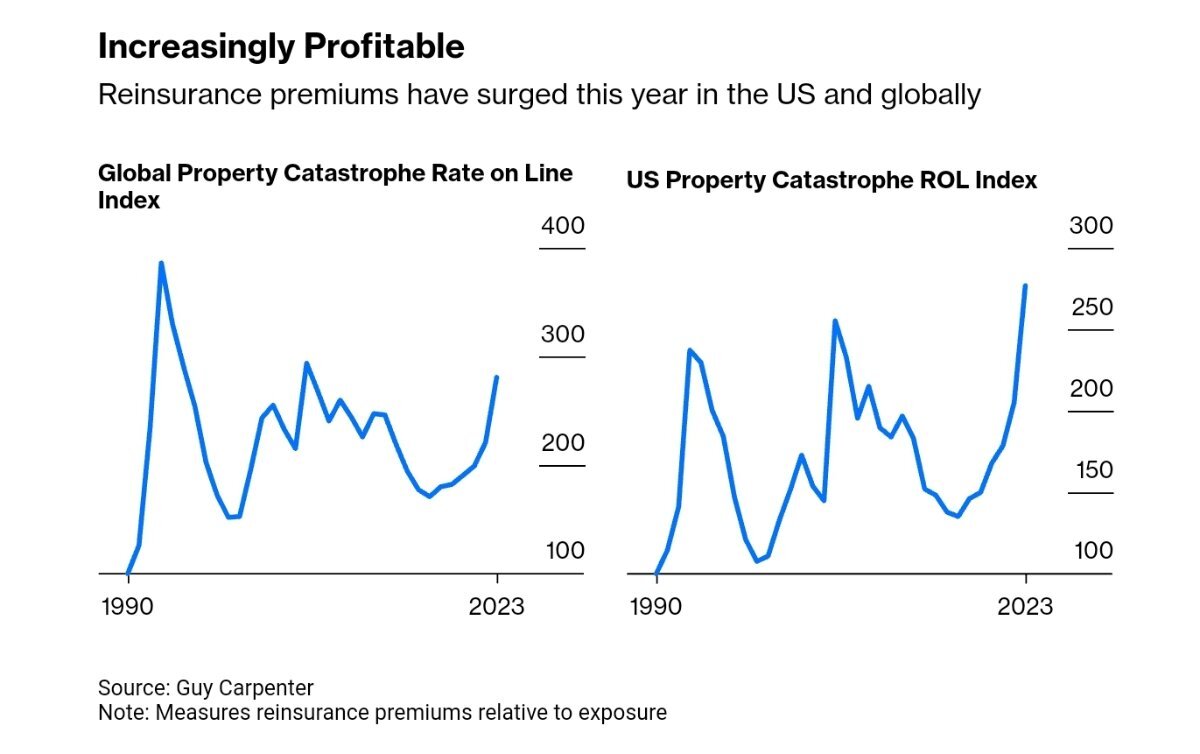

This has been an inflated year for natural disasters in the U.S. The number of U.S. potential billion-dollar weather and climate disasters in 2023 through June has exceeded every year tracked by that point besides 2017, with 12 such events so far, according to the National Oceanic and Atmospheric Administration’s National Centers for Environmental Information. The average from 1980 to 2022, adjusting costs for inflation, was around eight annually.

https://www.wsj.com/articles/home-insurers-are-charging-more-and-insuring-less-9e948113

“We’re still seeing the industry having an underwriting loss this year continuing out to 2025,” said Dale Porfilio, chief insurance officer at industry body the Insurance Information Institute. The institute expects that “the cycle of continuing to take rates upward is going to continue for the next two years,” Porfilio said.

...

The escalating cost of catastrophes is reflected in a steep increase in premiums for the reinsurance coverage that home-insurance companies buy to pass on some of their risk. Depending on the state regulator, those higher premiums can feed directly through to the price charged to homeowners, Fox said. His firm’s data shows reinsurance premiums were up on average 33% for June 1 renewals, which includes many Florida carriers, and 50% for renewals at the start of this year.

The question of whether reinsurance prices will keep rising, piling more pressure on home-insurance premiums, depends a lot on what happens in the second half of this year, according to Fox. “There’s a fork in the road ahead,” he said. “If we have another major hurricane or some medium-size hurricanes or a spate of wildfires…that [reinsurance] price will go up again.” -

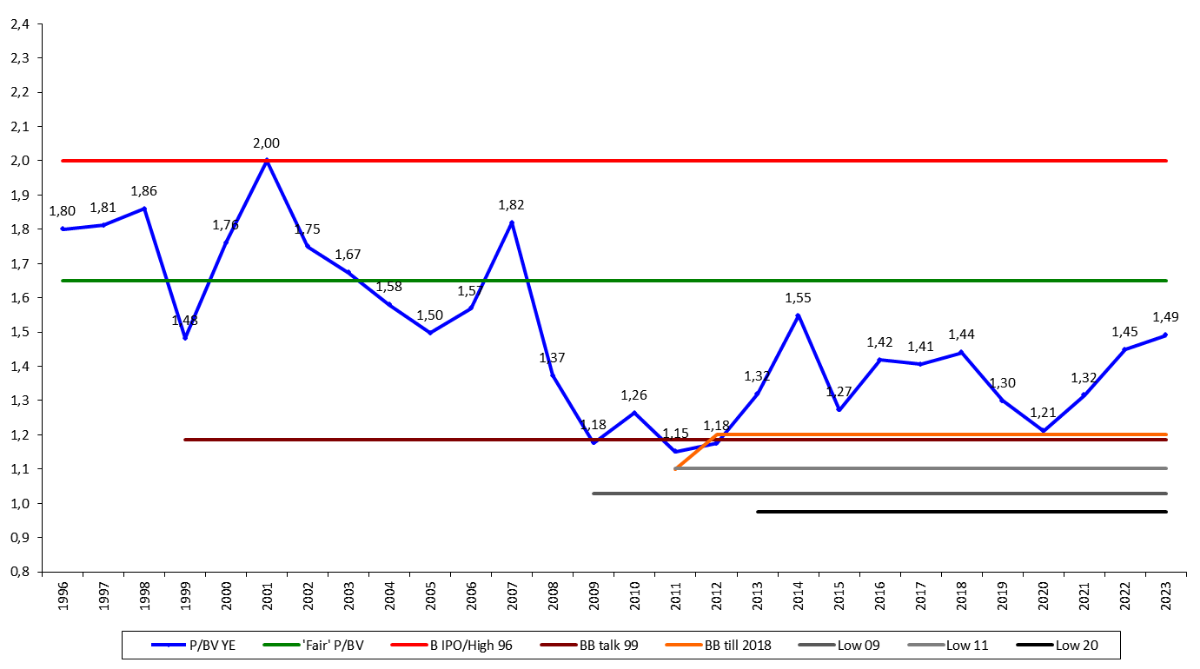

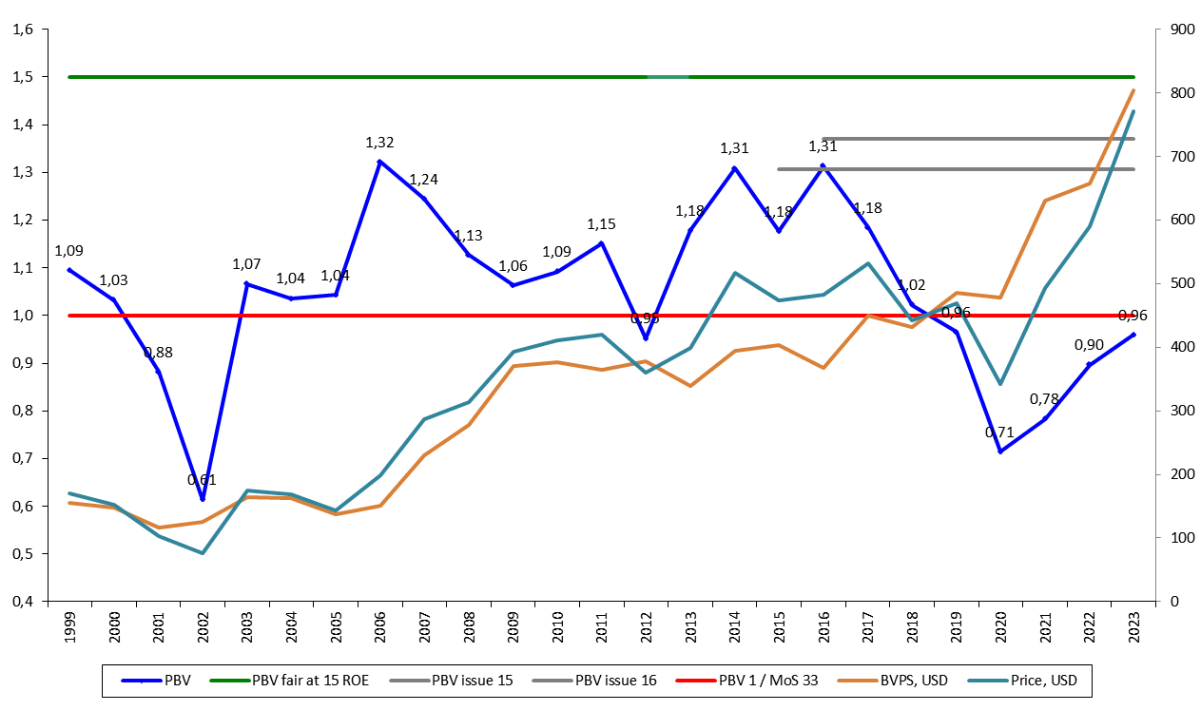

My best guess (and hope) it is because of the very good price performance of share price of FFH recently and in a last few years, but it is really hard to understand why it is still trading today at only 1 PBV and not at some 1.2 or 1.3 already. However you look, on absolute or on relative, it does not make sense.

-

-

The value of this forum is unbelievable. To illustrate, based on recent history:), basically all one had to do is to read everything carefully and than at least to follow Parsad into META, Viking into FFH and Greg into JOE...not to mention many other great ideas and posters!

-

7 hours ago, mattee2264 said:

And if that continues to be the case and inflation remains low and interest rates can fall back to around 3-4% (above pre-COVID levels) but very manageable in a growing economy then there is nothing much to worry about.

I think one could worry somewhat about this or maybe should in the future if market continues to do what it did in 1H:

7 hours ago, mattee2264 said:And during a bull market it is easy to have a longer term horizon and get excited over such things. But investors have a tendency to become very short term oriented when sentiment reverses. Case in point dot com bubble when some very good companies who would clearly benefit from the internet changing the world in much the same way AI eventually will still sold off massively.

But in my humble opinion it is still to early and more importantly not at a such an extreme point yet to make any big market calls. Maybe it is the case with some AI related or other hot things (avoid), maybe already even somewhat with big tech (avoid or be less greedy/more selective), but even in case of general market (not to hot, not to cold, no opinion), but especially the universe of not so magnificent another 493 companies or companies not even in SNP500, I think you can still find/own things to be quite excited about.

-

One more:

“What’s happened, particularly in the US stock market, has taken a lot of people by surprise,” he said.

SentimenTrader suggests the shift may endure. Unlike in the past, corporate insiders are big buyers, while technicals like subdued volatility and bullish options are keeping equity sentiment elevated. The only other two instances when stocks versus bond sentiment were so wide apart were in 2003 and 2009 “both coming out of protracted bear markets and indicating a dramatic shift in investor expectations,” said Jason Goepfert, director of research at Sundial Capital Research and SentimenTrader, which analyzes futures positioning, surveys, options activity and fund flows. “Both preceded new bull markets.” -

2 hours ago, scorpioncapital said:

is anyone worried about a nuclear war, followed by deflation, a rush to certain continents vs others, panic, and some companies doing well that sell radiation monitors, or even Amazon delivering essential goods via robots?

Not necessarily about such scenarios, but sure I am worried about what is going on. But then again: 'If a problem is fixable, then there is no need to worry. If it is not fixable, then there is no help in worrying'.

-

These factors explain why General Valery Zaluzhny, Ukraine’s top general, decided to throw in fresh legs on July 26th. He has been forced to adapt his original plan. Brigades from Ukraine’s 9th Corps had been expected to fight their way to Russia’s main line of defence. Then the 10th Corps, in essence a second echelon, including three Western-equipped brigades, were to be deployed to fight their way through the strongest defences. Finally, light, fast-moving air-assault units were supposed to exploit any breakthrough, pouring through the hard-won breach.

In the event, 9th Corps struggled. Advances that were supposed to be completed in days ended up taking weeks. Ukraine was unable to deploy whole brigades, instead breaking them down into smaller units. Some experts worry that 10th Corps has now been thrown in prematurely. The main Russian line is still kilometres away and 10th Corps’s units might be worn down before they get there, leaving them too exhausted to punch through.Western officials play down these concerns. “I think they timed it well,” says one. Ukraine is in a “very strong operational position”, says another, pointing to the turmoil in Russia’s senior ranks, including the decision in early July to sack General Ivan Popov, who commanded a big portion of Russian forces in southern Ukraine. Russian military bloggers have described heavy losses of Russian artillery pieces in recent weeks.

However, a fluid war of manoeuvre is likely to remain a stretch for a force cobbled together in a few months. The Russian verb peremalyvat (to grind through) is invoked on both sides. But Ukraine’s junior commanders, having seen their units gutted over the past 18 months, refuse to send their new citizen army into a meat-grinder in the way that Russia did in Bakhmut. As Ukraine has become more European, Ben Wallace, Britain’s defence minister, recently suggested, it has acquired “a Western European caution”.

Some American and European military officials argue that Ukrainian commanders have in fact been too slow to strike with their new brigades, a mistake that they think Ukraine committed last year in Kherson, when tens of thousands of Russian troops withdrew east over the Dnieper river with their equipment. Ukrainian commanders chafe at the idea that they should gamble their army in circumstances that nato generals have never faced.

The 10th Corps’s assault is a break with that hesitation. And the upside of the aversion to casualties thus far is that many Ukrainian units are in better shape than planners had assumed. Brigades that assaulted Russian positions were expected to be left with only a third of their original strength. Thanks in part to well-armoured Western vehicles, they have taken a lighter knock. Even so, the commitment of 10th Corps is a fateful moment for General Zaluzhny, a cautious commander with the weight of Ukrainian and allied expectations on his shoulders. “This is the last big decision for Zaluzhny to make this summer,” says the Western official. “The die is cast.”

-

On July 28th it took that reasoning a leap forward by announcing it would for the first time start to arm Taiwan from America’s own military stocks, as it has done repeatedly for Ukraine. The main difference is that it has not invoked an “emergency” to justify the move. Instead, it believes the arms supplies will help forestall a war across the Taiwan Strait. The military move may instead provoke a new crisis. China will not accept American claims that it is nothing out of the ordinary, and represents “no change” in America’s Taiwan policy. After all, America is shifting from selling weapons to Taiwan to subsidising its armed forces.

-

What once was a posture of skepticism has morphed into something approaching investor euphoria. Cash and hedges are out, replaced by demand for everything from small caps to meme stocks. Fueling the surge is data showing the US economy is thriving amid mounting evidence the Federal Reserve is beating inflation. All the optimism has sent the S&P 500 to the brink of its sixth advance in seven months and pushed prices in the Nasdaq 100 to almost 35 times profit. It’s manna for bulls — even as it leaves them with precious little wiggle room should anything in the economy or monetary policy not unfold as hoped. “It’s dangerous and consensus, but it’s late July, so who feels like fighting it?” said Peter Tchir, head of macro strategy at Academy Securities. “We are now at stage where people feel obligated to fully commit capital. Hawkish Fed not an excuse right now, and claiming recession is hard to justify as well.”

Good news on the economy is sucking more and more investors into risky assets. A steady expansion in speculative spirits has pushed equity positioning to the highest level since January 2022. Investors have a clear overweight exposure to stocks after long refusing to budge off their underweight positioning, according to Deutsche Bank AG. At the same time, a wide array of hedging metrics is showing low demand for downside protection. Put premiums for both Invesco QQQ Trust Series 1 (QQQ) and the SPDR S&P 500 ETF Trust (SPY) are hovering around the lowest levels in at least a decade, according to RBC Capital Markets. Additionally, investors are buying more calls to chase the rally while spending less to protect their gains. “The market is just not ready to let go of the positive narrative. Hedging is outrageously cheap,” said Amy Wu Silverman, head of derivatives strategy at RBC Capital Markets. “There’s more driving of demand of calls from folks who are underperforming than those who have done well and need to hedge.”

-

-

This is very interesting discussion!

Recently there is a lot of publicity about all this climate, weather, increasing catastrophe costs and 'uninsurable' future, such as:

https://www.wsj.com/articles/business-insurance-roiled-by-climate-inflation-205049df

https://www.wsj.com/articles/insurers-are-in-the-hot-seat-on-climate-change-74e27330

Climate change “has the potential of changing the insurance business profoundly and making part of the world un-insurable,” Gonzalo Gortazar, CaixaBank SA’s chief executive officer, said in an interview with Bloomberg TV Friday. “It’s not happening yet, but if we keep moving in that direction this is something we will have to face in due course.”

Yet, is that represents more of a threat (unexpected losses, regulatory risks, etc) or an opportunity (increasing market, better pricing, etc) for insurance/reinsurance companies? Perhaps everything will come down even more to execution quality of any particular company? Could all this negative publicity at least help improve pricing somewhat:)?

-

-

https://en.interfax.com.ua/news/investments/924955.html

The international insurance group Fairfax Financial Holdings (Canada) has increased its stake in the Ukrainian agricultural holding Ovostar (Ovostar Union) to 17.499% from 10.39%, the company announced on the Warsaw Stock Exchange on Tuesday.

-

-

-

-

-

https://www.barrons.com/articles/travelers-stock-climate-change-insurance-investing-6a8535e1

Unusually high catastrophe losses left The Travelers , a New York-based property and casualty insurer, in the red last quarter, but the stock rose nevertheless. That underscores a misperception about insurance stocks. Investors aren’t betting on the weather and the damage it brings, which can fluctuate drastically from year to year even as climate change makes storms more intense. What matters is how insurers charge for and manage that risk over longer periods. Although insurance companies’ balance sheets have been hammered by increasingly frequent and severe natural catastrophes in recent years, their stocks haven’t plunged. Insurance shares in the S&P 500 index are down about 1% since the beginning of the year, but up by 13% from a year ago. Investors aren’t losing faith in the group because insurers have been able to boost premium rates, taking in revenue that they will invest to cover future losses. Many have also been pulling out of risky markets, including California and Florida, where they couldn’t charge high enough rates to make profits, given the storms and wildfires that plague those states. The Travelers (TRV) is an example of how it is playing out. On Thursday, the company reported a loss of $14 million in its second quarter, or seven cents per share, a sharp fall from the $551 million in income, or $2.27 per share, it recorded in the same quarter last year. The red ink was mainly due to higher catastrophe losses from “numerous severe wind and hail storms in multiple states,” according to the company. In the second quarter, the firm paid $1.5 billion in catastrophe damages, twice as much as the $746 million in the year-earlier period. “We had six events surpassed the $100 million mark in Q2, the most ever for a single quarter since we began disclosing the table in 2013,” said CFO Daniel Frey on a call to discuss the results with investors. Nevertheless, the stock gained 1.8% in Thursday trading as investors were more focused on the firm’s net written premiums, which grew 14% from last year to $10.3 billion. Net written premiums—the amount collected minus payments for reinsurance—in the business insurance segment increased by 18%, partially driven by higher rates for renewed policies. And despite the higher prices, retention was strong at 88%, according to the firm. In the personal insurance line, net written premiums were 13% higher than in the year-earlier quarter.

-

16 hours ago, Gregmal said:

Tangentially, Ive been amazed at how much St Joe and Fairfax have in common today. I own both and the story arc of dated perceptions and 180 degree differences between those perceptions and realities is still very encouraging. If I had cash Id plow it into both without a second thought. See little reason to be "waiting with dry powder for an opportunity" thats sitting right in front of us all.

Like you I have my predispositions. Every few weeks I look for a reason to sell Fairfax because my bias says its a trading sardine. I give it some thought, look for reasons to sell, and conclude theres just no real justification for doing so. So much of investing is about challenging our biases and perceptions and evolving into situations that might seem uncomfortable before everyone else finds them comfortable.

This is very interesting, thanks for sharing! This is how I feel about both these companies too. I first bought some FFH maybe in the end of 2012 (or similar time), when there was a dip and they reached 3 year or so low, after they were thrown from the MSCI Canada or some other index, but the next 10 years, due to their bearish positioning and mistakes, it was love and hate or on and of holding for me (that is more of a trading sardine) and I never get enough conviction to make it a big position. But from the last year (and I was already maybe 1-2 years to late, and many thanks to Viking, Parsad and others for sharing their analysis and thinking on FFH) I do not see it as a trading sardine anymore. And they are still cheap on absolute and 'value today', while at the same time with improving results and also in a position to re-rate at least some 30-50 per cent relatively. I also followed JOE (together with Berkowitz) from a long time ago, but until covid and later reading all discussion here (again, many thanks to Gregmal and others) last year, I also did not have enough conviction to make it a large position. What is interesting, while FFH is already cheap on current results, JOE is maybe more in a 'value tomorrow' bucket (if you insist for having a view on future results to value it), but at the same time, if you look at it through possible NAV (as per latest discussion) it seems to me also like 'value today':). So here you are, you have two understandable, owner/large investor operated companies, with perhaps little if any disruption risks, with quickly growing/improving results, still cheap and not discovered or loved by market too much (with hopefully still wrong perceptions) to buy and do not touch, if nothing unexpected occurs (or they double or triple too quickly-lets hope for this scenario:)), for at least the next 3 or 5 years. I am not sure I have enough conviction at this time to suggest owning only them two, but even if you do not have much better ideas, adding BRKB and at least one other postiion will give you a well diversified portfolio, as per Munger:))).

-

-

Not much on the current market temperature, but otherwise quite good memo from Marks on this whole market calling/timing issue:

https://www.oaktreecapital.com/insights/memo/taking-the-temperature

While on the subject of buying too soon, I want to spend a minute on an interesting question: Which is worse, buying at the top or selling at the bottom? For me the answer is easy: the latter. If you buy at what later turns out to have been a market top, you’ll suffer a downward fluctuation. But that isn’t cause for concern if the long-term thesis remains intact. And, anyway, the next top is usually higher than the last top, meaning you’re likely to be ahead eventually. But if you sell at a market bottom, you render that downward fluctuation permanent, and, even more importantly, you get off the escalator of a rising economy and rising markets that has made so many long-term investors rich. This is why I describe selling at the bottom as the cardinal sin in investing.

-

Remembered while thinking about this Magnificent 7 problem:)

Fairfax 2023

in Fairfax Financial

Posted

WSJ: This has been an inflated year for natural disasters in the U.S. The number of U.S. potential billion-dollar weather and climate disasters in 2023 through June has exceeded every year tracked by that point besides 2017, with 12 such events so far, according to the National Oceanic and Atmospheric Administration’s National Centers for Environmental Information. The average from 1980 to 2022, adjusting costs for inflation, was around eight annually.

FFH: The consolidated combined ratio of the property and casualty insurance and reinsurance operations was 93.9%, producing an underwriting profit of $337.5 million, compared to a combined ratio of 94.1% and an underwriting profit of $301.7 million in 2022, driven by continued growth in business volumes (net insurance revenue increased by 6.2%), prudent expense management and decreased catastrophe losses of $134.8 million or 2.4 combined ratio points in the quarter.