thepupil

-

Posts

5,004 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

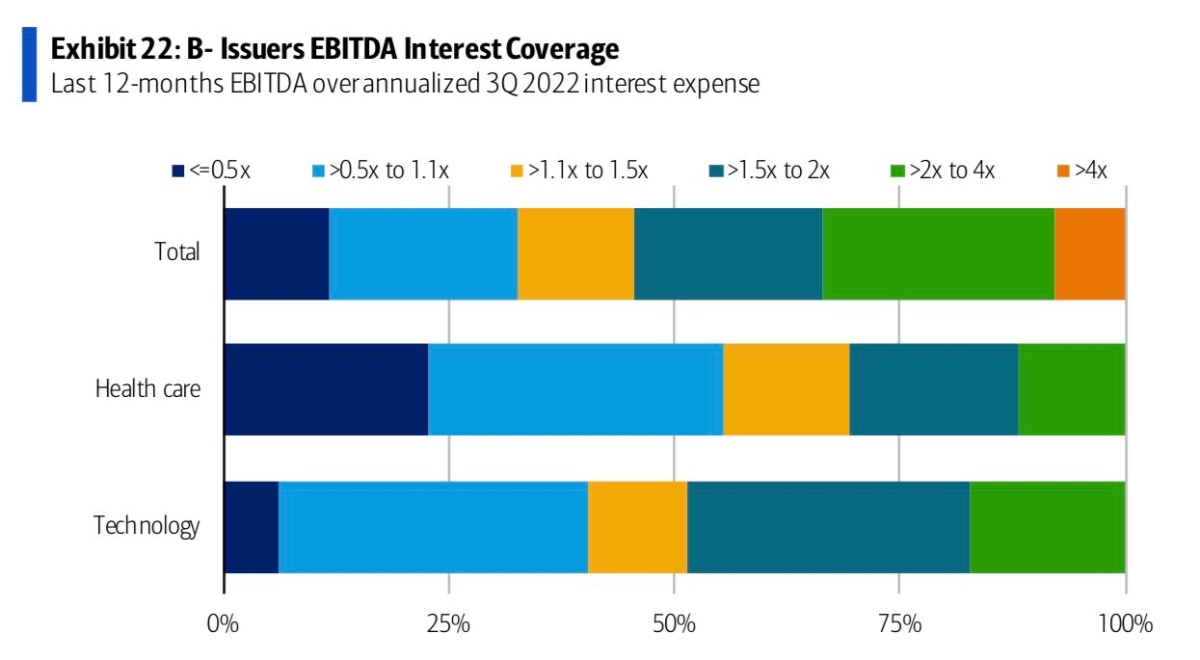

some more credit bear porn. Looks like about 30% of B- rates leveraged loan borrowers are at <1.1x and something like 10% at <0.5x reiterate that “the market” (broad cap weighted indices) has very high credit quality, low leverage, and is very well termed out and that 10+ years of regulations have pushed off this risk off bank b/s’s. Private equity/private credit is where the bodies are buried / will be.

-

Nitor Capital Management - Undisclosed Position

thepupil replied to alxcii's topic in General Discussion

Sounds kind of like Tejon Ranch. They have JV’s on their interstate land with industrial RE that generate cash flow similar to that, it’s a $520mm market cap, it’s a terrible long term performer. the numbers don’t match exactly, but given Nitor’s penchant for JOE and TPL, TRC may be a decent guess. -

from my thinkng out loud on twitter / initial checks it seems that Norfolk isn't going to have to pay much for all this. Nevertheless, I still think it should be down over the las tmonth more than 3-5% relative to peers. For both my parents and my account, I shorted NSC in small size equal to 50% of estimated BNSF exposure for parents and 100% for me. We'll see how it works out. I doubt I'll make / lose very much. but downside probably like 15% (8% after tax) and upside is "more".

-

as someone who has/has had bloomberg for 12 years and is spoiled by it, there's probably nothing more frustrating to say to someone not on a corp's payroll than "if you had this $28K/year service" lol.

-

I'll put my bull hat on here. I don't think markets ever really fully priced in 2% rates / negative real rates, so It's not entirely surprising that they haven't come down more than an academic duration measure might suggest given the move in the 10-30 year treasuries. I'm guilty of this too, but a gentle reminder that the equity risk premium is Total Expected Return on Stock - Expected Return on Bond, though some folks (includng me) will define as earnings yield - bond yield. Both of these remain positive, but assuming LT growth in earnings, the one with total return is obviously much more positive (as there's little differential b/w earnings yields and bond yields at this time).

-

yea same. we use nuclear and natty for power/heating/etc so energy costs haven't been bad at all. but other stuff...a since i bought in 2019: property taxes: +20% insurance: +50% (but it was stupid low before) other maint +30-50%+ (annual mulch, gutter cleaning, that type of stuff as a real estate investor if rents did ever go down because of s/d but the inflated opex stayed the same...NOI would get hurt a lot more obviously.

-

if you want to find the companies that are struggling in this environment. middle market buyout levered to the gills with floating rate debt is where its at. ~40% of companies seeing EBITDA* decline. 100% of companies seeing interest expense rocket up. *and that's PE owned company reported EBITDA. how many you think are super aggressive in trying to show EBITDA growth?.

-

I’ll do some non tech heavyweights when I have time.

-

Not allowed to include the largest companies by rev/mkt cap/ etc but instead should focus on a sideshow basket of unprofitable tech when talking about market fundamentals? greg, cmon man, like I kind of agree with your overall view here, but it’s this type of stuff that pulls me back into uselessly debating you

-

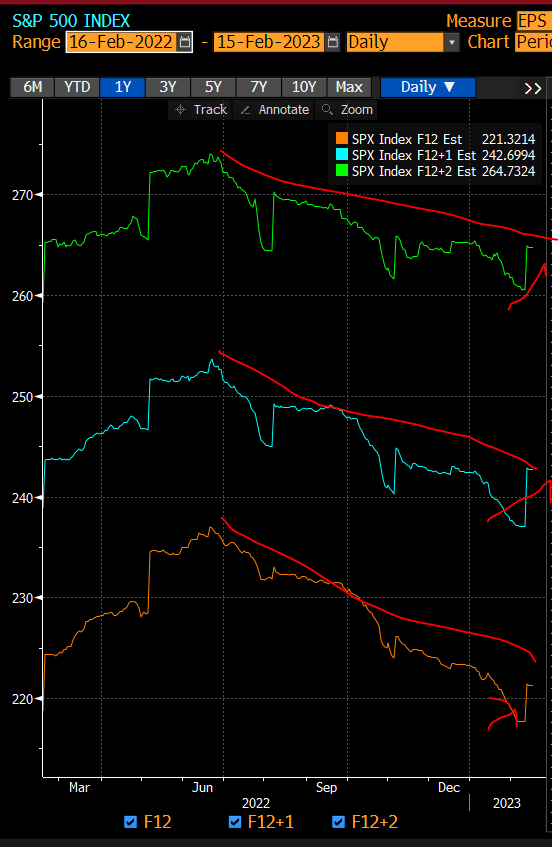

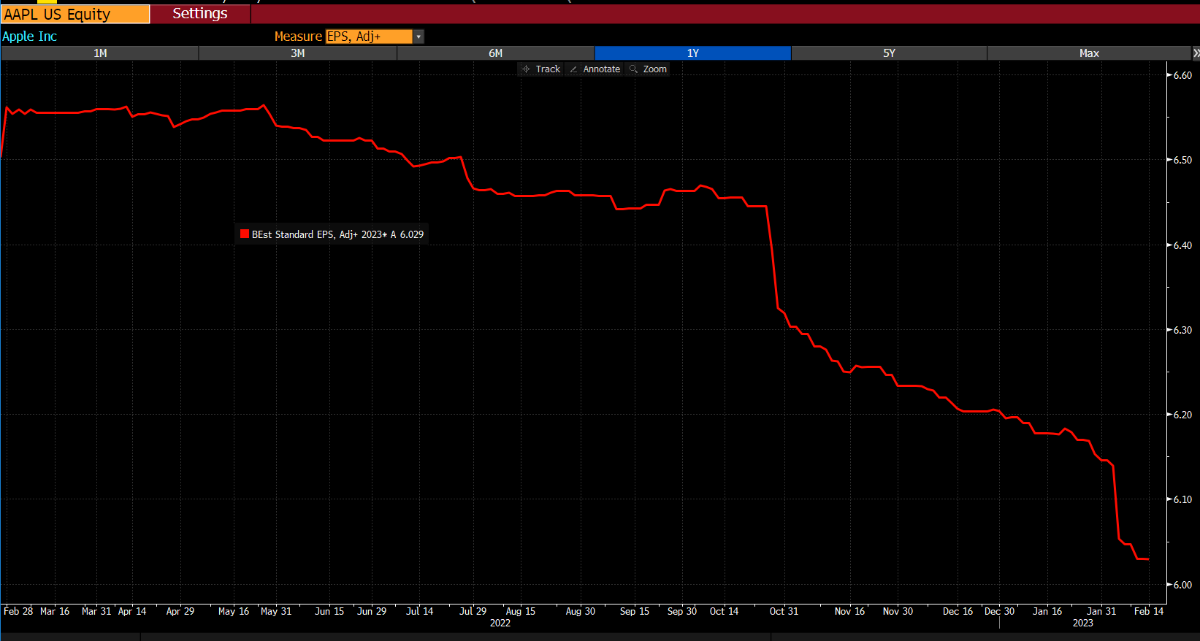

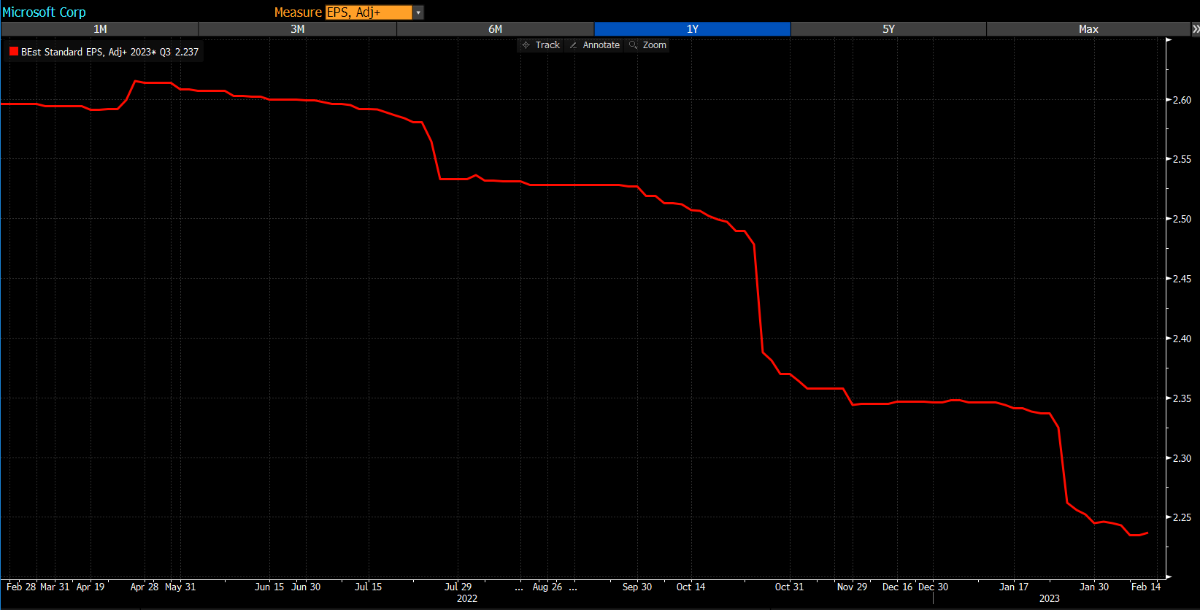

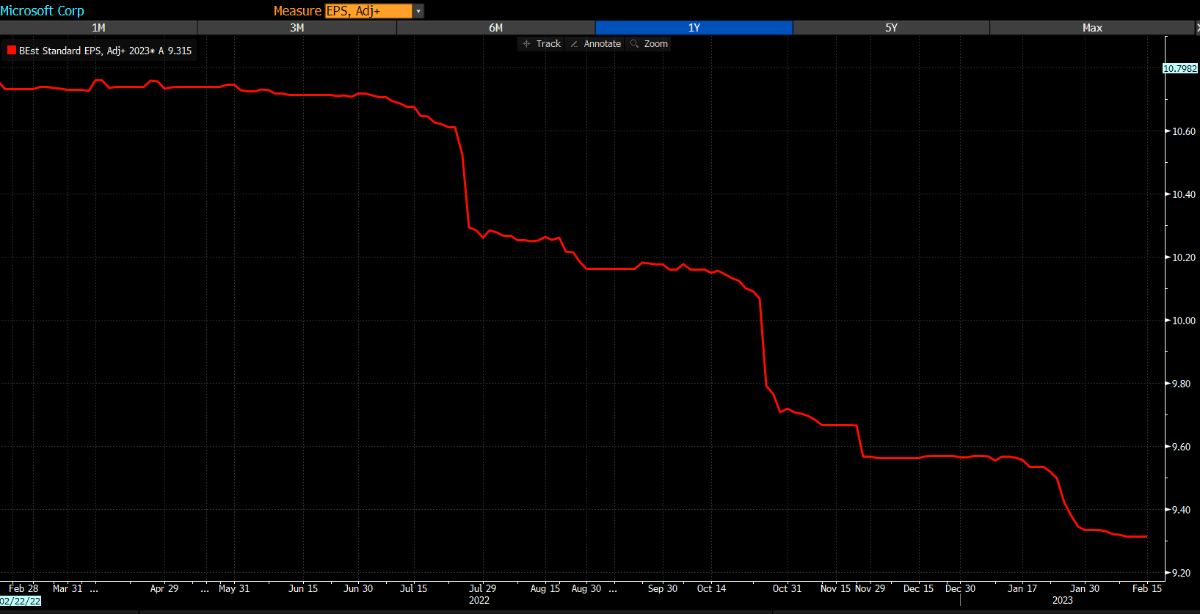

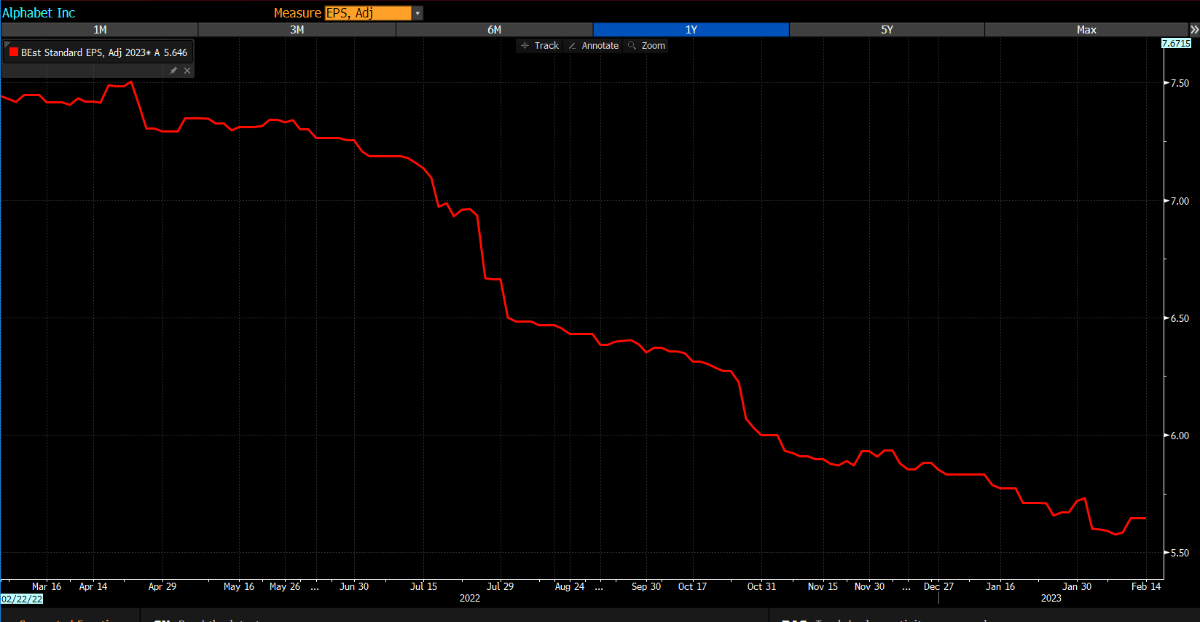

to be clear, this is why you own stocks for the long run. EPS fo brrrr. America!!! But let's not pretend that earnings estimates for the biggest co's and whole market have not done anything but come down for like 3 q's.

-

What are you referring to? Here are the 2023 earnings estimate trajectories of the S&P 500 and 4/5 top components (I skipped AMZN because EPS not relevant)

-

some doom porn for y’all

-

yes. @wabuffohas pointed this out a lot that in aggregate raising rates puts money in households pockets because they have more cash/bonds than debt. obviously that "in aggregate" is doing a lot of work. Someone with $2mm of 1 year treasuries is making $100K risk free that they weren't 2 years ago. anyone (people assets and corporations) with significant net floating rate debt is hurting.

-

Oh man...I'm not that great an investor and it's more from lots of contributions than anything, but here on this semi-anonymous message board, I will brag that I've accumulated about $730K individually and $780K as a couple (grad school's a bitch right!) in various tax advantaged vehicles over 11 years starting from $0. Let that be a little inspiration to the youngsters...I'm inviting the far better investors here to one-up me and inspire further. I can't imagine having 100% of my investment assets be taxable. gross! of course, I've yet to access that, so in no way has that money affected my life other than my ability to brag about it on a semi-anonymous message board.

-

I view it as part of my overall portfolio rather than separate. I don't view it as money that I won't touch until I'm 59.5. The roth conversion ladder if i stop w-2 work prior to then is an option. I doubt I'll w-2 until I'm 59.5. Also you get to roll into your own IRA when you switch jobs. I've done so 4 times in 12 years, so in practice it hasn't been 30 year money but 2-4 year money that one then switch to have full control. One can also monetize in other ways (ROBS, loans, SEPP) etc. It can obviously be very very long term money, but it's not necessarily so. I'm shocked you haven't set up a SEP IRA or something to build a tax advantaged account, particularly given I imagine your style leads to lots of short term gains. c'mon man!

-

I think many people care about indices because it's their only option. My wife and I save $67K/year through tax advantaged vehicles. we save more on top of that, but it's a material amount of money for us and our 401k providers only allow various indices/mutual funds. Unless we quit our jobs we have to buy something with that, so having some opinion on the relative merits of the performance of various asset classes is of some use to me. for me right now I wonder whther I should keep buying bond index, switch to long term bonds, or use it to add international / non USD exposure. my portfolio's always gonna be US stock/RE heavy. for now I think bonds are a better diversifier than non US stocks.

-

I've had 80-100%+ equity exposure since 2013 or so. Gave up shorting or market timing back then and have been better off for it. I'm not a buy an hold investor. My late grandpa was and it worked out wonderfully for him. In practice, I simply do not own many stocks for that long. Looking at current portfolio I've held Berkshire from the beginning (so about 12 years) and Tetragon for 9-10 years now, everything else is from 2019 or later. the venn diagram of "discount to NAV" and "buy and hold for 10+ years" doesn't include too many stocks.

-

a lot of this is repetitive from what I’ve already said, but I have a salt/alcohol induced hangover after a lovely Valentine’s Day dinner and am dehydrated and can’t sleep. I think we’re way too early in all this to declare any kind of “winner” and who was “right”. It’s been a very short time period. I think “bears” would be proven right if we see a “lost decade” type environment where stocks fail to provide much compensation above that of alternatives, specifically bonds, so that’s a 6+ year type of thing and even then will be sensitive as to which point one measures from. “bulls” would be proven right in the opposite case. We’re trying to declare a winner in 6 months vs 6 years. Like if stocks are up 10%/yr for next 7 years and bonds make 4.5%, bulls win. If stocks up 5% yr and bonds make 4.5% but that’s kind of artificial because we don’t have to be bulls or bears and I think the most bearish people on are are 60-80% long stocks and acknowledge that stocks generally provide better LONG term returns. I’d frame it all as an opportunity to not be a one dimensional bear/bull and use the far more competitive yields offered by fixed income to take incrementally less risk and make similar overall portfolio returns. For my whole investment career carrying cash/bonds/etc has been a hugely losing proposition and one was kind of consciously forced to take all equity risk. I’m not hugely bearish or bullish, but do think the game has changed and FI is not so awfully assymetric/betting on breaking the zero bound like it was the last 10 years. we have positive real yields, and nominal FI yields are similar if not greater than (in some cases) the earnings yield on the stock market. Rising rates are scary if you own rate sensitive things (like say highly levered real estate), but ultimately this is a wonderful thing for those with capital who don’t want to be entirely in equities. I’ve never felt more wealthy and secure because I no longer have the Fed competing with me for safe assets/yield. Inflation may be 3% 5% or 10%, but the interest income on my (and my retired parents) slugof safe assets is up 100-300%. A greater balance between the levered equity/asset holders (real estate / PE /etc) and lenders is being achieved. What a time to be a well capitalized rentier!* I think it’s “too good” and want to own some duration because I don’t think it will last. I don’t think I should be able to make 1.6% real in a government guaranteed instrument for 30 years, that’s just a risk free handout to capital. Like why the hell is the US government paying me 7.5% effective interest? It will come down, but it’s still stupid. *now I think if you’re gregmal or dealraker, you’d counter that the rise in yields is a trap and that one will compound at a higher rate just saying in stocks/business for the long run. My response is “yea probably” so but I’m only 70-80% sure if that rather than 100%, and I don’t think owning a little FI is gonna kill me. maybe this is veering on the “bearish” but it does feel to me that outside of the very speculative stuff we are at a point where we’re kind of having our cake and eating it too. Real estate and stocks haven’t really come down too much (in some cases not at all) despite the increase in cost of capital. Sort of a strange, but also a nice opportunity to reevaluate one’s asset allocation without the emotional baggage of a huge drawdown. I realize this thread is about predicting a short term bottom and I keep trying to make it really boring and proselytizing a 20% bond allocation and I shoukd go over to bogleheads and go buy a Buick or something.

-

I bought the current 30 year US treasury a 3.80% yield to add duration to the portfolio as it sell off a little bit. my experience from buying BBB corps last summer/fall is that I don't have the scale to mitigate the transaction costs in those and am probably better off owning duration via govvies. If in 1 year the yield is 4.80%, total return will approximate -12%. If in 1 year the yield is 2.80% total return will approximate +24% booooooring.

-

Investing in triple net lease commercial property

thepupil replied to aws's topic in General Discussion

I don't know everything there is to know about opportunity zones, but my impression was that there was a substantial rehabilitation requirement for OZ's and a fully leased existing Dollar General would not qualify. -

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

thepupil replied to thepupil's topic in General Discussion

Essex only sold 1 building in Q4 2022. It was for 4.3% and $640K / unit. It's probably nicer than their average apartment and in the end who cares because it's just 250 / 57,000 units (0.4%), but for that teensy 0.4% the public company, the stock was/is basically at a 45% discount to PMV on an EV basis and moreso on the equity. -

seeing dealraker's beautiful 401K got me to look at my accounts. what stands out to me when i look at my accounts is that generally, I have a difficult time compounding my taxable accounts because I lead an expensive lifestyle and pay a high tax rate and am not a tax efficient investor. this is despite both of my taxable accounts handily beating the market / making good absolute returns. On the other hand, I have some earlier stage dealraker-esque tax advantaged accounts. The IRA's that result from my first two years' working (2011-2013) and have no contributions since are a material amount of money. So there's a lesson in there for some of the young folks. Max out that tax advantaged untouchable compounding vehicles!

-

This discussion bring up the idea of time horizon. In truth, I don’t know my time horizon. 7-10 years ago, I’d have told you it was 5 decades, but then I plowed a large portion of my accessible net worth into a down payment on a house a few year a ago . So that money was thought of as 50 year money but was actually 5 year money. Maybe I should have invested more conservatively (though that would have been a worse result). Right now if I knew I wanted to work 3 more decades, I’d know my time horizon was super long. If I want to work 5 more years or 3 and start something entrepreneurial, my time horizon is not nearly as long. I think once one reaches a certain level of wealth / income from other sources, one doesn’t really care about drawdowns or volatility, but before then, volatility matters. Before you have “f you” money, before you know what path you’ll take, if there’s a chance you want to access your money for whatever reason before “many years from now”, you care about drawdowns and your time horizon is probably not as long as you think. I don’t have super strong or well formed views here but I don’t think it’s as simple as “young = long time horizon” also when you’re young and have little money, new money is huge percentage of portfolio. Once you have a little scratch, you can’t as easily correct mistakes / invest into drawdowns with new money. $100k/year of savings is more meaningful to a $100k portfolio vs a $1mm or $2mm, so I think drawdown sensitivity increases as you get wealthier, then decreases again if you have so much that you can live well at very low withdrawal rate.

-

of course, to be clear I'm 80% risk assets. I'm just saying it's consistent that if you think stocks need to be at lower multiples to own bonds at similar yields to earnings yields of stocks.

-

I like MBS. government guaranteed like 5% yields. look at the YTW of 4.4%. That means if everyone out there never died/moved/divorced/refi'd etc. they'd be like 20 yr securities yielding 4.4%. it will obviously be higher than that and shorter duration. also look at WA price of $90. so now when people die/move/divorce/default/etc, you make $10 / $90 when that happens. i am a buyer of the bond index which yields 4.5% and it yields more than treasuries in part because of its big slug of MBS.