-

Posts

214 -

Joined

-

Last visited

-

Days Won

1

2 Followers

.thumb.png.e9643dd797bb6bfa93083ce1311ba74d.png)

Recent Profile Visitors

2,434 profile views

giulio's Achievements

")

-

FIH, PRM

-

Book recommentations on how to determine multiples when valuing a company

giulio replied to adventurer's topic in Books

No book is going to help because as Munger said "there is no formula I can give you". The best approach is what @DooDiligence suggested, i.e. case studies. Look at some of the best investors' deals and their rationale, try to understand what they saw and how it played out. Importantly, focus on the business dynamics not consensus views. Buffett has written extensively about valuation, remember that multiples are just the inverse of discount rates. No approach is equal. Buffett, Munger, Ackman, Rochon, Howley, John Huber are all worth studying but in the end, YOU must do the work. Start practicing and with time you'll get better and understand what works for you. It is more art than science. Best, G -

Definitely not, imo. I think you need to dig deeper than who's the PM of India, the "Greek economy" or gpw growth (not the metric to overly focus on for insurance). Ffh will have a considerable amount of money to redeploy in the coming years and they can do it globally, across the entire capital structure, opportunistically. You need to take this reinvestment opportunity in consideration to understand where the business will be in 3-5 years. The stock may or may not follow in the same time frame but who cares? N.b. not all their investment will work out. @This2ShallPass iirc both Buffett and Watsa said that the change in bvps should approximate the change in IV over time, not that bv = IV.

-

I believe the reason for ffh extraordinary share performance was the extreme discount to intrinsic value at which it was trading in 2020/2021. You were buying a dollar bill for 50 cents and the dollar would double in a short period of time. You don't get a better scenario than this one. At 300/400 per share you could see the business was easily worth multiples of that. Then, the intrinsic value started growing thanks to higher earnings and buybacks. Share price had a lot of catch up to do, and still has imo. Combining an asset value valuation + look through earnings method made this clear to me in 2021. @This2ShallPass book value is accounting, iv is what matters. A business doing 15% roe, trading at 1.5 book is selling for 10x earnings. Is this expensive? Best, G

-

You could only wish there were more like him and muddy waters!

-

10% pa investing in bonds? How? Btw, I've seen some pretty high estimates for earnings in this thread...have interests expenses, taxes and corporate costs been taken into account?

-

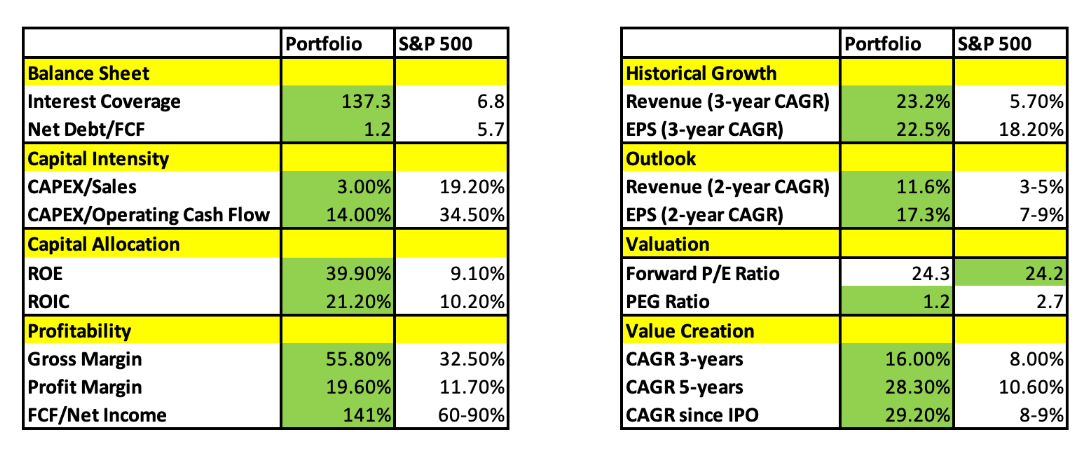

Hi guys, I wanted to get some stats about the s&p500 index so that I can compare it to my portfolio. I can't seem to find them anywhere on the internet. I was looking for something like this Do you know where I can find this info? Thank you in advance! Best, G

-

FIH, EVO

-

Overpaying for an assets is always a bad decision and it ensures that you will earn suboptimal returns. Whether you are an investor or a ceo allocating capital, it does not make any difference. Munger is of course right because he's taking into account the return on incremental capital reinvested. In your case, I think it's worth noting that: 1) if your company has excess cash for a buyback it means that it does not have enough internal opportunities for reinvestment At 40% 2) shares of such a company will hardly trade at a low price. If bv = 100, 40% roe = 40 in earnings, at 15x this equal a price of 600. A buyback at this level equates to 6.7% yield, way lower than your starting 40%. 3) if a company earning 10% roe is selling at 0.5 bv a buyback would be the best course of action as it would yield 20%. You can Pay a very high entry price and still get value, it all depends on your assumptions about capital retained and roiic. There are qualitative aspects to consider of course. If you think high growth lies ahead don't be too conservative in your assumptions. But this does not mean that you can any price. It must incorporated in your estimate of fair value. I hope I have expressed myself clearly enough. Hopes it helps, love the discussion. best, G

-

The published 1982 up to 2021. Book is on amazon if you are interested. I would add to the list Ian Cassel and Paul Andreola. Best, G

-

I believe this does NOT refer to Fairfax ownership in the Meadow UK. FF Meadow Holdings is a sub of Fairfax, 100% owned through its various insurance companies as you listed. FF Meadow then holds a minority stake in Meadow UK, the actual company. Best, G

-

108K shares were bought back and canceled in October. Max price paid $15. https://www.sedi.ca/sedi/SVTItdSelectIssuer?locale=en_CA

-

Good for long term holders that some "investors" buy or sell without any regards for intrinsic value

-

I am of the opposite view. Given how hard they worked to set it up, the difficult regulatory environment and their long term view of India, I believe they will hold on to shares for a long time. They might sell some if valuation gets truly outrageous but they'll keep a majority. Possibly they will increase their stake if allowed to. Best, G

-

Thanks for posting this @SafetyinNumbers. Happy to share my analysis. I review my ffh valuation annually when they release the annual report. As I stated in the other thread, I like to use look through earnings and at fy23 I had IV at around $1800. Using Book value I get $1500 but I am aware buybacks are distorting the calculations. To reach the lower bound of IV the index addition would need to generate a 20% pop in price. If it happens, I WILL NOT sell any shares. The reason being that I would expect ffh to grow IV over time. Simple as that. At $1800 I might trim the position a bit as there are a couple of interesting ideas I would like to add to. Best, G