Leaderboard

Popular Content

Showing content with the highest reputation on 02/14/2025 in all areas

-

Here is Francis's Q4 activity as disclosed on the 13F (so, no foreign info, OTC info, etc) https://www.dataroma.com/m/m_activity.php?m=ca&typ=a The Chou Associates portfolio (again, 13F) here https://www.dataroma.com/m/holdings.php?m=ca Sold completely out of Navient and Occidental1 point

-

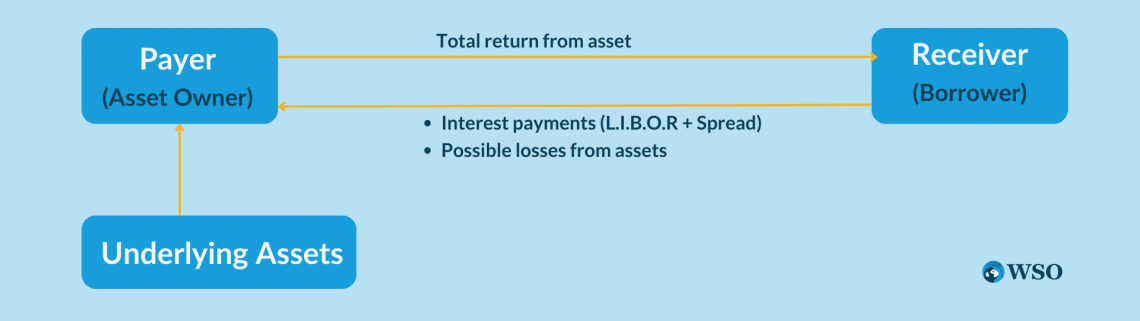

I'm not sure I followed your post but that doesn't mean it isn't right. Basically it's just a financing deal - the banks hedge their end of the contract so they aren't taking any directional risk. That could mean balancing a portion of it with other market participants that want to put the opposite TRS on (unlikely in the case of Fairfax stock but quite likely for other assets) or, as in this case, just buying the shares to offset the directional risk completely. The fees and interest rate are where the bank makes money. They are the bookie, not a fellow gambler. The counterparty also gets the dividend, which is factored in to what they charge FFH. There is a cost to Fairfax to keep the trade going. But when the contracts are terminated - the hedge shares become available to either hit the market for sale, or as is more likely here, get bought up by indexers and closet indexers when Fairfax gets added to the S&P / TSX 60 index.1 point

-

we probably need to pin this, but the bank (counterparty) is price agnostic, Fairfax is renting their balance sheet and taking the directional risk.

1 point

1 point -

because banks are “financial services” companies and they are providing financial services to a corporate client, who has decided to take a position on itself and needs a product that fits the needs. Ideally banks makes their dough via fees And not taking a directional position for or against the corporate client. I.e so they would have been long the FFH shares to balance the TRS, if the risk officer was clear minded1 point

-

We’ll find out in 3 weeks I guess.1 point