Credit Default Swaps (2005-2009): Fairfax's Version of The Big Short

I am finally getting around to updating parts of my book. This is a fun one.

“Sizing is 70% to 80% of the equation. It’s not whether you’re right or wrong, it’s how much you make when you’re right and how much you lose when you’re wrong.” Stanley Druckenmiller

In The Big Short, Michael Lewis tells the story of a small group of investors who recognized the risks building in the U.S. housing market and positioned themselves to profit when the system eventually broke.

The best-known participants were Michael Burry at Scion Capital, Steve Eisman at FrontPoint Partners, and Charlie Geller and Jamie Shipley at Brownfield Capital.

A small Canadian property and casualty insurer could easily have been added to that list.

Fairfax Financial.

While the investors featured in The Big Short purchased credit default swaps tied directly to subprime mortgages, Fairfax built a broader portfolio of protection against systemic financial risk. The objective, however, was similar: profit from — and protect against — a severe disruption in the financial system.

The trade would become one of the most successful investments in Fairfax's history.

Insurance Against a Financial Crisis

A credit default swap (CDS) is essentially insurance against default. The buyer pays a premium, and in return the seller agrees to compensate the buyer if a specified company or security experiences a credit event such as bankruptcy or default.

The attraction of a CDS is its asymmetry. If nothing happens, the buyer loses only the premium paid. If credit conditions deteriorate, the value of the CDS can increase many times over.

In The Big Short movie, a large investor in Burry's fund summed up the trade perfectly: “In other words, we lose millions until something that has never happened before happens?” Burry replied: “That's right.”

That was essentially Fairfax's position.

Management believed the global financial system was becoming increasingly fragile. Credit standards were deteriorating, leverage was rising, and financial institutions were taking risks that were poorly understood by both regulators and investors.

As Fairfax explained in its 2005 Annual Report:

“The company has invested approximately $250 in 5-year to 10-year credit default swaps on a number of companies, primarily financial institutions, to provide protection against systemic financial risk arising from financial difficulties these entities could experience in a more difficult financial environment.” Fairfax 2005AR

The original concern centered on Fairfax's reinsurance counterparties. If a severe financial crisis occurred, would the institutions Fairfax relied upon remain financially sound?

As management dug deeper, they discovered that many of these firms had significant exposure to mortgage-related assets and other risky securities.

The more they researched, the more protection they purchased.

Fairfax began building its CDS position in 2002 and continued adding through early 2007.

Looking Wrong Before Being Right

Initially, the trade appeared to be a mistake.

The position was expensive to carry and Fairfax recorded losses of approximately $102 million in 2005 and another $76 million in 2006 as credit spreads tightened and financial markets continued to strengthen.

Like Michael Burry, Fairfax looked wrong for several years before it was ultimately proven right.

By 2006, however, cracks were beginning to appear in the U.S. housing market. Early in 2007, conditions deteriorated rapidly. Fairfax responded by increasing its CDS exposure.

Then the financial system began to unravel.

The Payoff

As credit spreads widened and financial institutions came under increasing pressure, the value of Fairfax's CDS positions surged.

By the end of 2007, Fairfax had recorded approximately $1 billion in gains. Another $1 billion followed in 2008 as the financial crisis intensified. Most of the positions were sold during 2008 and early 2009, locking in extraordinary profits.

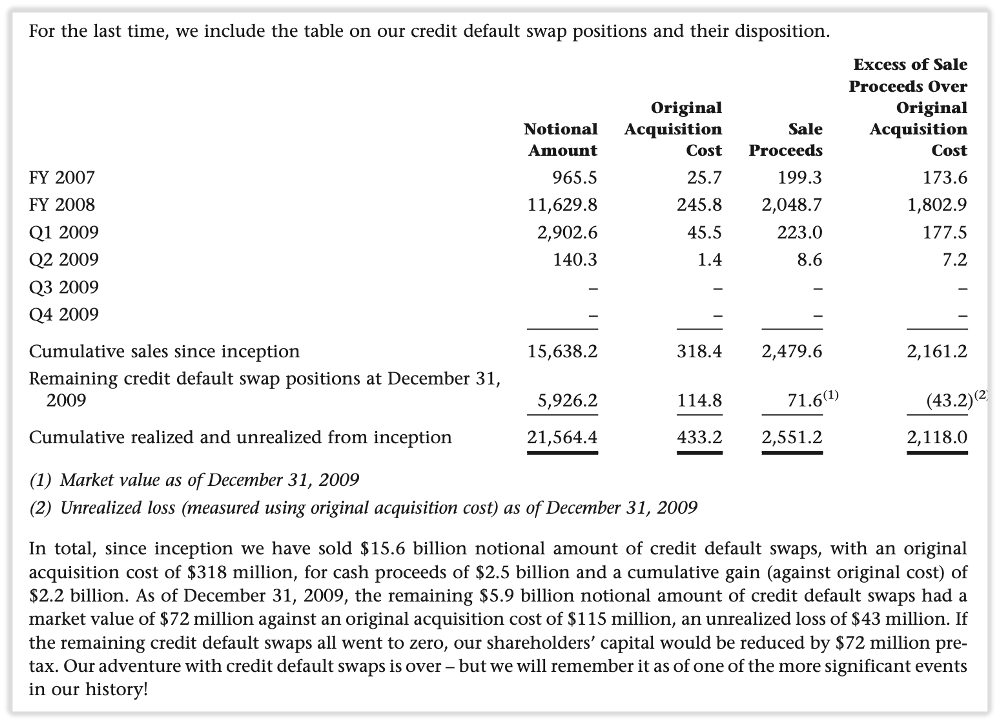

In total, Fairfax invested approximately $433 million and realized gains of roughly $2.1 billion.

For perspective, Fairfax's common shareholders' equity at the end of 2008 was approximately $4.9 billion. The CDS trade materially strengthened the company's balance sheet at one of the most difficult periods in modern financial history.

How did Fairfax compare with some of the investors featured in The Big Short?

Scion Capital: approximately $2.7 billion

FrontPoint Partners: approximately $1 billion

Brownfield Capital: approximately $50 million

Fairfax Financial: approximately $2.1 billion

Fairfax sized the position exceptionally well.

The Impact on Shareholders

Shareholders were major beneficiaries.

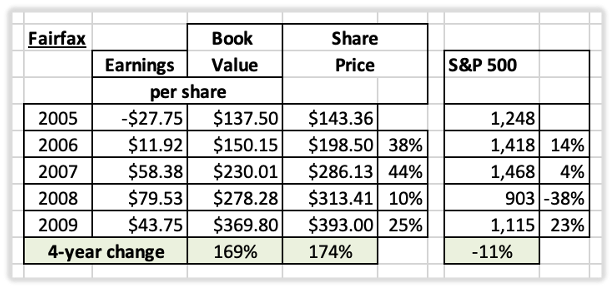

From 2005 to 2009, Fairfax shares increased approximately 174%, while the S&P 500 declined 11%.

During one of the most challenging periods in modern financial history, Fairfax dramatically outperformed the broader market.

Lessons for Investors

The CDS trade highlights several characteristics that have long defined Fairfax.

First, Fairfax excelled at risk management. The original purpose of the CDS position was not speculation. It was protection against a financial crisis that management believed was becoming increasingly likely.

Second, management was willing to follow the evidence wherever it led, even when that meant taking a highly contrarian position.

Third, Fairfax demonstrated patience and temperament. The trade generated losses for years before producing extraordinary gains.

Finally, Fairfax sized the opportunity aggressively. Identifying a great investment is important, but as Druckenmiller observed, returns are often driven as much by position size as by being right. Fairfax continued adding to the position as the evidence strengthened and the opportunity improved.

The CDS trade ultimately delivered both protection and enormous profits.

More importantly, it revealed the core strengths of Fairfax's investment culture: independent thinking, deep research, patience, conviction, and a willingness to act when risk and opportunity are mispriced.

Those qualities helped Fairfax execute one of the greatest investments in its history.

----------

COBF and the Trade of a Lifetime

The period was also memorable for members of the Corner of Berkshire & Fairfax (COBF) investing forum.

At the time, Fairfax was the target of a high-profile short attack and its shares traded at what many forum members believed was a deeply discounted valuation.

Many investors on the forum understood Fairfax's CDS position and recognized its potential value. As conditions in the U.S. housing market deteriorated, they believed Fairfax was likely to generate enormous gains if a financial crisis unfolded. Yet the stock price appeared to reflect little of that possibility.

As a result, a number of forum members made concentrated investments in Fairfax shares during 2005 and 2006.

A few went even further, purchasing long-dated call options (LEAPS) on Fairfax stock, which traded on the NYSE at the time.

For some, it became the investment of a lifetime.

----------

Brian Bradstreet Explains the CDS Trade

The following excerpt is from Fair and Friendly: The First 25 Years of Fairfax (2010). Bradstreet explains how Fairfax's concern about reinsurance counterparties eventually led to one of the most successful investments in the company's history.

When I looked at that, I got scared. The more I looked into those reinsurance companies, the more scared I got. The investment markets were bubbly. There was a lot of crazy risk-taking. We ourselves on the fixed-income side were being offered Ponzi-type stuff that came with an AA or AAA rating. So I began to fear that the reinsurance companies we were relying on to pay us might buy this junk and get into trouble and we wouldn't get paid. That would blow us right out of the water. And so I asked, How can we protect ourselves?

With the help of our analysts, I started researching all these reinsurance companies to see how many treasury bonds they did or didn't own. If they owned a lot, I could rest easy. If they didn't own a lot, that meant they might not be able to pay us. What we found was that pretty well all of them, including the best of them like AIG, were taking enormous risks. That was our initial screening. Then we started to dig more, company by company, and we realized they owned all these asset-backed, mortgage-backed, high-yield bonds, which were pronounced as safe as treasury bonds but were in fact pure risk.

One way to protect ourselves was to buy credit default swaps (CDSs), which were just appearing on the market around this time. They were basically bankruptcy insurance on the reinsurers. But I soon realized that we couldn't buy enough contracts on enough reinsurance companies to be diversified and fully protected. Then it occurred to me, Why don't we buy protection on the companies that are standing behind what the reinsurance companies are buying? If I was worried about the high-risk mortgage business, for example, why not buy insurance on the mortgage insurers in the United States? So we did. The next step was to buy insurance on the mortgage-lending companies like Fannie Mae and Freddie Mac, which were supposed to be government-backed but weren't in legal terms. Fannie Mae, for example, had $80 of exposure for every $1 of common equity, so it was a very good bet to fail.

We bought our first contracts in 2003 and our last ones in December 2007. We just kept buying more and more, first five-year, then seven-year, because they were so cheap. By the end of 2006 we had invested $276 million in CDSs that the market valued at $72 million. At any other place I would have been kicked out on the street. Not here though. I remember going into an investment committee meeting where Prem asked, "What's the best idea we've got?" Francis Chou, who's a pretty shy guy, piped up, "Buy more credit default insurance." I didn't have the guts to say it.

Brian Bradstreet – Source: Fair and Friendly: The First 25 Years of Fairfax

----------

In Fairfax's 2009 Annual Report, Prem Watsa closed the chapter on the company's credit default swap strategy.

Fairfax had invested approximately $433 million and generated cumulative gains of roughly $2.1 billion, making it one of the most successful investments in the company's history. The trade protected Fairfax during the financial crisis, materially strengthened its balance sheet, and helped position the company for the years that followed. As Prem noted, it would remain "one of the more significant events in our history."