All Activity

- Past hour

-

Grand Old Perverts Bunch of rapists and closet cases.

-

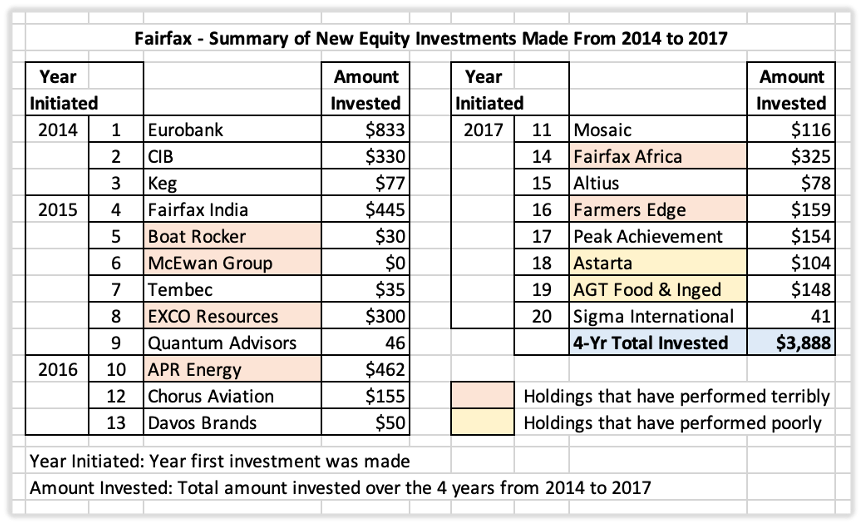

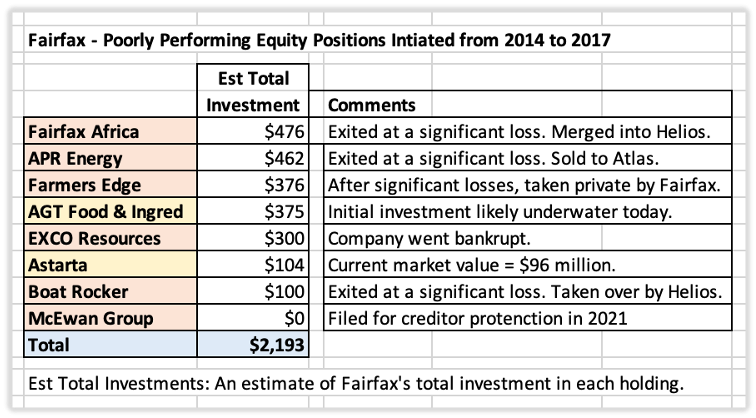

A Review of 2014 to 2017: Old Fairfax – Too Many “Chronically-Leaking Boats” This article #3 in my historical review of some of Fairfax's investments. “My conclusion from my own experiences and from much observation of other businesses is that a good managerial record (measured by economic returns) is far more a function of what business boat you get into than it is of how effectively you row… Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” – Warren Buffett – Berkshire Hathaway 1985AR Fairfax defines value investing as purchasing securities at prices below intrinsic value while maintaining a margin of safety. The approach is explicitly long term and places unusual emphasis on downside protection and the avoidance of permanent capital loss. From 2014 to 2017, Fairfax doubled the size of its insurance business through aggressive international expansion. As a result, the company's investment portfolio grew significantly. Fairfax also expanded its equity holdings. During this four-year period, it established approximately 20 new positions and invested roughly $3.9 billion. The results were mixed. A number of investments performed well. Unfortunately, many did not. New Purchases: Too Many Clunkers Over the years, Fairfax invested approximately $2.2 billion in eight companies that would go on to produce disappointing results. Two investments largely went nowhere: Astarta AGT Food and Ingredients While neither investment resulted in a significant loss of capital, both generated little return for shareholders over a decade. The opportunity cost was substantial. Capital tied up in stagnant investments cannot be deployed into better opportunities. Six other investments performed much worse: Fairfax Africa EXCO Resources APR Energy Farmers Edge Boat Rocker McEwan Group These investments resulted in significant capital losses. Given Fairfax's emphasis on downside protection and avoiding permanent capital loss, the results were particularly disappointing. What Was the Problem? The problem was not that Fairfax had losing investments. Every investor has losers. The problem was that too many investments shared the same weaknesses. A pattern emerged across many of the holdings: Weak management Weak balance sheets Weak profitability Many suffered from all three. From 2014 to 2017, Fairfax accumulated too many businesses that could fairly be described as chronically-leaking boats. The Overall Portfolio Was Getting Worse The problem extended beyond the new purchases. At the same time Fairfax was making these investments, its equity hedges were forcing the company to sell some of its strongest holdings. Several existing investments were also struggling, including BlackBerry, Resolute Forest Products and Recipe. Fairfax was selling some of its better businesses while adding a number of weaker ones. The overall quality of the equity portfolio was deteriorating. Why This Was a Problem for Fairfax Weak businesses tend to share two characteristics. First, they often consume capital. Companies with weak economics frequently require additional investment simply to survive. Second, they demand management attention. Turnarounds are rarely passive investments. Neither was a good fit for Fairfax. Years of losses from the equity hedges had already reduced financial flexibility. At the same time, Fairfax operated with a highly decentralized structure and a lean head office. The company was not built to oversee numerous troubled businesses simultaneously. As business performance deteriorated, many investments required additional capital and more management attention. The situation became increasingly difficult to manage. The Real Lesson In hindsight, the issue was not bad luck. The issue was process. Fairfax's investment framework had drifted too far toward lower-quality businesses at precisely the time the company needed to move in the opposite direction. “Time is the enemy of the terrible company.” Many of the companies Fairfax was buying required additional capital, intensive oversight and successful turnarounds to generate acceptable returns. Those requirements were increasingly at odds with Fairfax's decentralized operating model and lean corporate structure. The result was a growing mismatch between the businesses Fairfax was buying and the organization Fairfax had become. Fairfax eventually recognized the problem and adjusted its approach. The result was the birth of what I like to call New Fairfax. That article - the last in our series - will be out tomorrow.

-

Make it 3

-

Sure thing @Blake - do you approve of topless trannies running around the White House lawn? Is that dignified enough for you?

-

Yeah, was kind of thinking the same thing.

-

this narrative of Prem supposedly making capital allocation decisions for philanthropic reasons is tired.

- Today

-

Why are all you Trumpies so ferociously obsessed with trans people? I feel like I could count on two hands how many I've seen in my entire life. I'm starting to realize that much of human behavior is actually inverse to itself: extreme arrogance masking insecurity, anger veiling fear, that sort of thing. Why then are some of you so fixated on trans people? Is there something you would like to share with the class @cubsfan?

-

In Trump world, any level of taxation is basically socialism at the same time that spending $10 trillion on defense is essential and "You better not touch my Social Security money."

-

Can I please see this propaganda?

-

Hmmm... let me meet somewhere in the middle with the Trump bunch. I personally don't like Platner and think it's kind of crazy that the Democrats are championing someone who had a totenkopf tattoo and espouses antisemitic content. Now then, is it crazy that I also don't approve of having a felon as our president? How about not supporting a man who instigated his followers into storming the U.S. Capitol building? Am I crazy for thinking that Trump blowing out budget deficits isn't good for the long-term health of our economy? Here I go trying to bang my head against the wall again.

-

Charles is actually doing a great job as a King. He had lots of time to prepare.

-

Ah the jealousy begins - we'll be sure and bring back the Biden trannies just for you next year.

-

If the deal was digitally signed on Sunday why are they waiting until Friday to release the details? And if they're sending JD Vance out there to fluff the media in advance without providing details, it really doesnt bode well.

-

Gayest event ever. Lots of half naked men. Too bad Trump didn’t take his shirt off.

-

Got a bid, and closed Oct'26 LQDA $20 puts sold in Feb to fund OTM calls at that time. They had ~20% premium in Feb.

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

rogermunibond replied to tnathan's topic in General Discussion

FT on the very soft insurance market https://giftarticle.ft.com/giftarticle/actions/redeem/ec8c2ca1-1026-43cc-b91b-bbffcba72dd8

-

Blakes just mad he fell for the oil bros propaganda

-

Bread & Circuses

-

Word of advice....if you find yourself taking the opposite with just as firm of a stance you're likely just as bad of a rational thinker as the ones you're criticizing.

-

Has the real estate angle been discussed any where, that would interest me more. Although I don't think it worked out very well when they took that angle with ToysRus

-

Do you think they did the deal to help a Canadian Company? ex like how Blackberry investment likely was about saving a Canadian company (my guess)? or do you think they understand Canada better? I think there is a lot of hidden value in Andrew Peller real estate portfolio that could be unearthed with Capital that Andrew Peller could not.

-

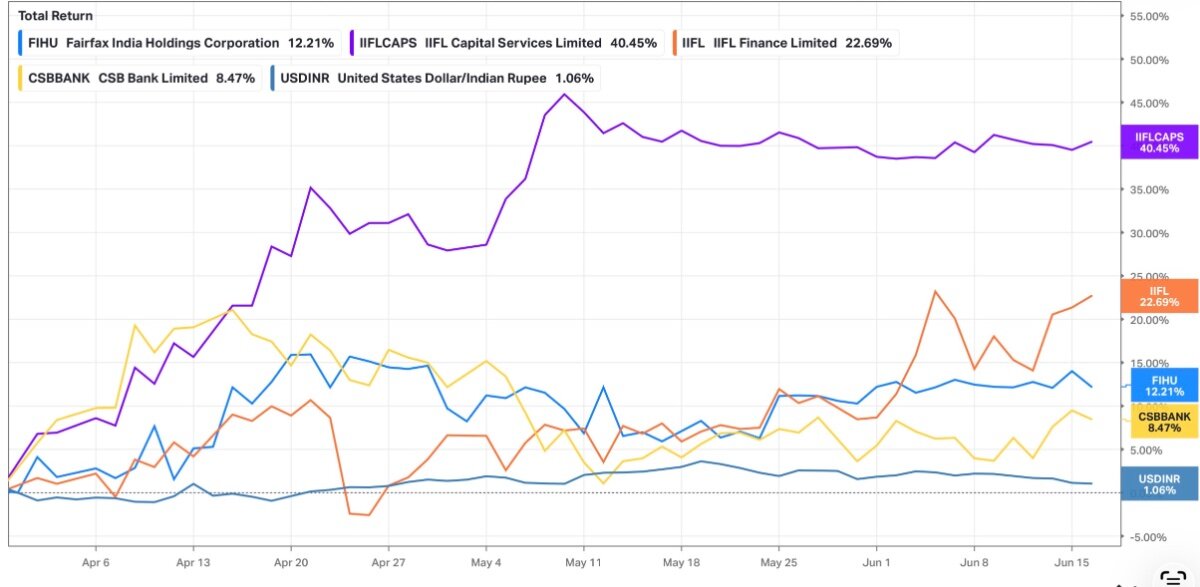

One would think oil plunging would be bullish for Indian stocks. FWIW, the rupee is less of a headwind this quarter vs last and the public market portfolio has bounced a decent amount. I assume BIAL valuation will continue to accrete. I added some today too.

-

All I will say Fairfax often has many headscratching investments! If this wasn't in Canada, would they have bought it?

-

Trying to argue with Trump supporters is like deciding to slam your head repeatedly into a brick wall. The wall of course never budges, and all you get at the end is a horrible headache.

-

It's too bad they decided to attack us earlier this year. It's also been hard working with them considering they withdrew from the JCPOA.