TwoCitiesCapital

-

Posts

6,303 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

Wish I had the trading acumen of you guys! The ride from 65k to 30k (or maybe 20k) has not been as fun as the ride from 10k to 65k was. Kind of crazy the crash is happening in an environment where countries are literally adopting it as use for legal tender...something the bears NEVER thought would happen...but here we are. I still think it's possible we hit 100k this cycle, but certainly looking less and less likely. 65k top is by far the shallowest of all prior booms - even 100k would have been shallow by comparison but we'll see.

-

To be clear, it wasn't the stablecoin that dropped to zero. The stablecoin dropped to ~0.60 which was the amount of actual backing it had. Any shortfall from a dollar was supposed to be arbitraged by the issuance of the Titan tokens which were valuable at the time. Edited b/c this explains it better: https://thedefiant.io/iron-finance-implodes-after-bank-run/

-

I dunno. Other "inflation hedges" like precious metals also got crucified. Silver is down 6% today. Gold? 4%. Long bonds are up. S&P is down while Nasdaq is up suggesting it's not just rates but ALL longer duration proxies outperforming. None of that seems right in response to a 0.05% hike in the IOER or inflation concerns being justified. The bond market has been saying there would be no sustainable inflation all along. I wonder if its time for commodities to catch down to that. I say that as someone who is heavily in commodity companies - not b/c of inflation fears but because they were dirt cheap from 2015 - 2020.

-

https://www.coindesk.com/iron-finance-defi-titan-iron-price-drop Algorithmic stablecoin loses its peg. I have concerns about algorithmic stablecoins. They make more sense to me than fiat backed ones (to the extent crypto should NOT rely on fiat inputs), but I struggle with the incentive structure of maintaining pegs in environments of fierce selling. I know ones like DAI are overcollateralized which is great, but if there is a wave of selling and the collateral value falls, the solution is to liquidate more of that collateral and put more pressure on the price resulting in waterfall liquidation like scenarios. The primary way to reduce the threat of waterfall liquidations? Collateralize with something less volatile and uncorrelated with crypto in general - i.e. stablecoins issued by the likes of Coinbase (USDC) which makes DAI just as centralized and just as dependent on fiat. It would be cool if DeFi could find a way to reliably fix this and have an algorithmic stable coin that is actually stable and not backed by fiat, but I don't think we're quite there yet.

-

Fed "surprised" the market by projecting two rate hikes (0.50%) over the next 18 month period and the long-bond rallies like crazy in response. Bond market is even LESS convinced of inflation after the Fed meeting acknowledging it and suggesting they'll accelerate rate hikes from prior projections.

-

Harley Bassman (the fixed income guru behind this ETF product) talks in depth about this on the Macro Voices podcast. I don't recall what the actual "delta" was, but he goes into detail about thinking about sizing in that conversation and provides examples of how much you'd expect this thing to move.

-

I'm considering buying more shares at $13 to try to tender for $15. Wouldn't be mad if I get stuck with them though.

-

I agree. I just think 'eventually' is likely later this decade or the next one IF it happens. My working theory is that demographics, globalization, technological advancement, and private sector debt explosion have all be disinflationary/deflationary over the last 1-2 decades. These factors offset the money printing and is why inflation hawks were wrong each time about massive inflation. After 2-3 decades of limited consumer price inflation, politicians will get comfortable with the idea that money really is free. And that will be precisely the point where the disinflationary drags from these offsetting factors is waning. I could see how we MIGHT get inflation in that environment. But even with demographics, productivity advancement from internet/personal computing/mobile phones, partial reversal of global supply chains, and less reliance on US dollar in global trade (from lower oil consumption) all moving away from being disinflationary, we would still have other deflationary/disinflationary trends to contend with. Technological advancement and productivity gains from A.I. may be massively deflationary. Consumer debt balances will likely grow and any rise in interest rates throttles discretionary spending and thus inflation/economic growth. The trillions printed may largely remain trapped as excess reserves and not circulated throughout the broader economy. Etc. etc. etc. It's a high bar to get lasting inflation in the U.S. and I can't see how it occurs any time soon without something major (like the loss of reserve status) occurring first.

-

Not to mention the very act of banks hoarding cash, as opposed to lending, is contractionary and disinflationary. This entire economy is floated on credit growth - you cut the growth rate of credit and the impacts on economic growth are dramatic. I can't speak for the big banks, but I know bankers here in the Midwest for local credit unions and the like. They're sitting on tons of cash too, but not because they think prices are rising. It's because they don't have enough money good projects to invest it in and things are arguably shakier today than they were 2-years ago when rates were higher. Or that inflation is already captured in the elevated inflation figures were CURRENTLY seeing and we're on the brink of massive disinflation unless donut prices go up by ANOTHER 50% over the next 2-years. To get consistently elevated inflation, you need consistently rising prices. And those prices need to rise at the same, or an accelerating rate. If a house changes in value from 100k to 200k in a year, your housing inflation rate is 100%. If it goes up by another 100k in year 2, housing inflation is only 50%. If it goes up by another 100k in year 3, inflation drops to 33%. The drop from 100%, to 50%, to 33% is disinflation - a slowing rate of inflation. Any bonds priced for 100% inflation at the beginning of this trend will PRINT MONEY in the environment of 50% and 33% inflation. The bond market knows this and will NOT move to reflect current inflation unless if it becomes convinced that inflation is sustainable and accelerating. So who cares that donuts were up 50% over the past 2-years? That impact is already captured in today's inflation figures and bond yields. All that matters going forward is if they go up another 50% or more over the next 2. B/c if they don't, the impact is disinflationary. What is going to drive a 50% increase in donut prices over the next 2-years? Ongoing stimulus? Ongoing supply chain disruptions? Ongoing wage hikes? Ongoing inelasticity of consumer demand? Most of these seem one-off and dare I say...transitory?

-

Utility bills? Mine are mostly unchanged from the last year. Real estate costs? Most people buy real estate with debt. And while the price of real estate has gone up, the interest on the debt has come down. The net effect? Real estate is MORE affordable today (from a monthly payment stand point) than it was 1-2 years back. Even rents in many major cities are down. Skilled Labor? Do you have data to back this up? The primary rises in wages I've seen have been at the lower-end of the payment spectrum where it's directly in competition with gov't stimulus. As someone who works in finance, I'm not seeing exploding wages here. We'll see a rise in lower-end wages, but it will likely be a one-time effect. Also, the reduction in stimulus will likely offset much of the impact as incomes are reduced as stimulus is phased out. Healthcare and education have been massively inflationary for the past two decades even while overall inflation remained muted. I don't view their continued trend as the start of a new normal for inflation rates. We can debate as to the causes, but it's not stimulus or supply related.

-

They can be transitory in that they only happen once. If we get 5% inflation for a year and then sub 2% inflation thereafter, then you're not getting 10-year yields much above 2%. Right now we're seeing large amount of inflation - much of it from a low base effect, supply disruptions, and trillions in direct stimulus. None of those is expected to last. Higher minimum wage will persist, but if it doesn't go up at the same rate every year (it won't), then it can only support a lower and lower inflation rate going forward. IMO, we still have several disinflationary forces that are still in play that have been in play for decades: 1) Demographics 2) Debt Loads 3) Technology/Innovation/Productivity Demographics may flip to being neutral later this decade, but the other two are likely to persist and all 3 are still active now. As this plays out, maybe those factors change. Maybe we get trillion-plus dollar stimulus implemented every 9-12 months and I have to change opinions about it persisting. Or maybe something else happens on the global scale to continue to disrupt supply chains. Or maybe businesses have to continue to compete with unemployment benefits to hire workers and the labor market remains artificially tight. But I'm not currently convinced ANY of that will happen into 2022 which means after the one-time transitory impacts of higher prices in 2021, nominal prices will begin to revert to the sub-2% inflation mark we were seeing pre-pandemic.

-

How Come No One is Talking About Resolute?

TwoCitiesCapital replied to Parsad's topic in Fairfax Financial

My understanding is that equity investments are accounted for at cost. Subsequent earnings of the investment proportionally increase the carrying cost. Losses and cash dividends paid would reduce the carrying cost. I don't know the return on vs return of capital characterization. My best guess is that the dividend will be taxable to Fairfax and that the characterization of 'return on' vs 'return of' is determined by the payer of the dividend and NOT the receiver or their method of accounting. -

**Corrected** Deal was oversubscribed w/ $1.6 billion interest. Only $500 million in bonds issued, but 4x oversubscription of the initial offering can't be ignored - particularly in light of the 50% decline in price.

-

I would rather we NOT fall to 18k just given my sizable allocation to this, but if we do I'd be buying hand over fist. I reinitiated my DCA once we fell below 40k and will be doubling it if we go below 30k. Price action in the short term means very little. We all know that. Momentum is broken, social sentiment is negative at the moment, but the fundamentals march onwards. Would add that few here saw the rise to 65k as confirmation that they were wrong and should be participating. Dunno why the drop to 32k serves as evidence that they shouldn't be. Seems like a very selective use framework and is a recipe to get whipsawed in markets. In 3-years, I don't think it'll matter if you bought at 18k, 28k, or 58k. They'll all probably look like good deals in hindsight.

-

Just ignore it. There have been several hypothesis of when this would be decided and each has come and gone. Don't think about it. Don't watch. One day it'll be up 100-200% or down 90% and you'll know what the decision was.

-

I know Panama, Paraguay, and El Salvadore aren't on anyone's radar. I know that by themselves they don't constitute much additional demand than say MicroStrategy issuing 2 billion in coverts to buy BTC. But just think back 12 months ago when people thought it was laughable and ridiculous that ANY country or company would accept BTC. 'It's too volatile'. 'Why would they give up their sovereignty over their own money'. ETC. ETC. ETC. Now those same arguments are having to be walked back and watered down. Those individuals now have to explain why Paypal and Square and Visa are all working in cryptos. Why Mass Mutual, Paul Tudor Jones, Stanley Druckenmiller, etc. are all investing in it. Those people are having to justify why Panama and Paraguay and El Salvadore don't matter and have to explain why this isn't the start of something bigger. Every day, the bear argument gets diluted and watered down while the bulls are justified.

-

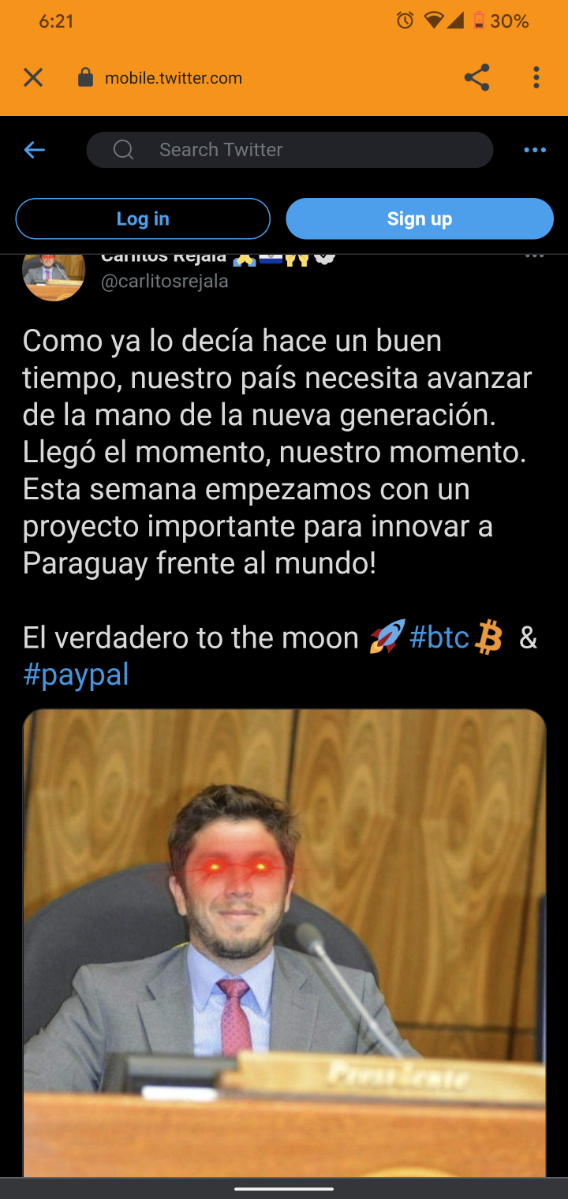

Paraguay legislative leader has hinted at some form of policy adoption towards Bitcoin today on Twitter. Using my Google translate skills, basically says innovation bis necessary and Paraguay will lead the world with this innovation. **laser eyes**

-

And now for the 3rd chapter of this story: U.S. Recovered Millions in Ransom From Colonial Pipeline Hackers https://www.bloomberg.com/news/articles/2021-06-07/doj-to-discuss-ransomware-attack-on-colonial-pipeline-on-monday Can we put to bed the "BTC is GREAT for criminals" narrative now?!?!? Why anyone believes having a public ledger identifying all of the wallets criminal proceeds go into - and where that money is spent - is good for criminals hasn't put any thought into what that means for the criminals enjoying their proceeds. USD Cash is still WAY better for criminal activities so maybe we should drop the 'disgusting' and 'evil' USD for something that is morally superior? Or at the very least we can stop bringing back this intellectually dishonest argument against BTC.

-

I'm not a tax professional, but I'd imagine the IRS doesn't care how other countries' treat it. Maybe it goes to court and some judge comes down on them, but I doubt they'll change their taxation policy or the taxable nature of crypto transactions as a result of anything El Salvador has done.

-

https://finance.yahoo.com/news/el-salvador-plans-bill-adopt-034739503.html El Salvador looking to legalize BTC for payments and potentially add it to the countries' reserves. Small country for sure. But this is how it starts.

-

Started off as a 10-15% position for me. Has receded over the years as my opportunistic adds have not kept up with my overall portfolio growth in other positions. Quite honestly, the brain damage for me would have been worse if it had been larger. It's been frustrating watching this languish and do nothing for ~10-years. Obviously I'll regret not having more of it IF we get the outcome we want, but I have to ask myself at what cost? I would feel way worse if I had 30% of my portfolio in this for the last 10-years instead of 10-15%. And while resolution seems around the corner and I did add a hair recently, it's ALWAYS seemed like resolution was around the corner for the last 10-years and we've been wrong the whole way so far. What matters is the outcome, but you have to survive the journey too!

-

https://www.wsj.com/articles/bitcoins-reliance-on-stablecoins-harks-back-to-the-wild-west-of-finance-11622115246 A fairly critical piece in the WSJ on stablecoins. Honestly - I agree. Stablecoins exist today out of convenience since there are no easy/quick on/off ramps to fiat. Digital currencies backed by CBs may change that (if ERC-20 compatible - or compatible with whichever smart contract chain dominates), but it is worth noting that crypto is STILL reliant on fiat stores of value. Maybe that changes once BTC becomes less volatile and wrapped BTC can replace stable coins - or some other alternative comes up - but it is an interesting reminder at the irony of the existence of stablecoins pegged to fiat.

-

The wait that never ends

-

This happened last time too. Fairfax was excluded from the entire run-up in BB, but fell sympathetically with it when it collapsed. Was a decent time to be adding shares on the offchance that they were able to monetize. I see a similar set-up now.

-

Yearn.Fi released their first quarter report. Made over $5 million in Q1. 30% more than the entirety of 2020 in a single quarter and are still launching more vaults/strategies. Think of Yearn vaults as mutual funds that aggregate investors' capital to lower fees (transaction fee to move $20 is the same to move $20 million and significantly less than 1 million people each moving $20). This puts Yearn token at a P/E of like 100x (total capitalization/annualized Q1), but how many years do you need to grow as at 4-6x before that becomes reasonable? 1-2. And 2 weeks ago you could've had it for 40% less. DeFi is blowing up.